A Novel Perspective on Prioritizing Investment Projects under Future Uncertainty: Integrating Robustness Analysis with the Net Present Value Model

-

Sheng Shao

and

Ali Sorourkhah

and

Ali Sorourkhah

Abstract

Investment decisions are important because they involve significant capital in a business. According to the literature, experts agree that a net present value (NPV) approach is better suited for evaluating investment projects’ feasibility. Practically, the NPV method does not account for uncertainty in calculating the expected return on investment. Investments may be susceptible to random events such as natural disasters or economic instability that hinder the expected return on investment. While previous research has attempted to address uncertainty using fuzzy approaches, these approaches mainly focus on data-centric uncertainty. The focus of this study is on the uncertain environmental conditions where changes in macroeconomic, political, and other indicators can influence decision outcomes. This study conceptualizes and implements combining the NPV approach with robust analysis as an efficient and practical method in decision-making under uncertainty and unpredictability. The proposed algorithm was implemented in a case study on investment project selection in Tannakabon, Iran. The results indicate that considering future scenarios, the restaurant investment project is the most suitable among the seven projects. In contrast, the cafe investment project is the least appropriate option available.

1 Introduction

Decision-making in the investment domain is a critical process that requires a thorough examination and an accurate understanding of various factors (Seifollahi, 2023). Investment plans require capital, planning, and careful conditions analysis for equipping a production centre or establishing a new business (Balaei et al., 2023). In this process, individuals must define their objectives, assess risks and returns, and compare options (Shahbeyk & Banihashemi, 2023). The significance of investment decisions lies in the fact that they involve a substantial amount of capital in a business (Kaviani et al., 2023). It is a reality that when making an investment decision, recovery of that decision is generally impossible, or at least, it will be highly costly (Seyed Nezhad Fahim & Gholami Gelsefid, 2023). Additionally, investments usually significantly impact the business’s future cash flows, especially those likely to generate cash flows after several years (Ghahremani-Nahr et al., 2022; Shemshad & Karim, 2023). Making incorrect decisions in this area can have financially irreparable consequences for the decision-maker (investor), individuals involved in the business, and, ultimately, the relevant social environment (Patil et al., 2023). Historical evidence indicates that many such decisions are not based on scientific models. Furthermore, when such analyses are conducted, an appropriate approach to dealing with conditions (complexity or uncertainty) is not adopted (Esmaeil Darjani et al., 2023).

In the economic evaluation and the selection of investment options, net present value (NPV) is the most common indicator for evaluating investment options (Mongkoldhumrongkul, 2023), so that 75% of firms calculate it when deciding on investment projects (Brealey et al., 2020). The NPV method’s theoretical basis is money’s time value. Understanding the value of money over time is crucial for evaluating various investments with different returns, costs, and benefits at different times (Loucks, 2022) so that modern methods for evaluating the effectiveness of projects take into account the value of money over time (Bugrov & Bugrova, 2020). The NPV method converts net cash flows over the project’s lifetime into the sum of present values equivalent to the predetermined target rate of return (Bragolusi & D’Alpaos, 2022). The NPV equals the algebraic sum of the present value of all cash inflows and the present value of all cash outflows. When NPV is positive, the project will still have residual income after repaying the principal and interest. When NPV is zero, nothing is gained after repaying the principal and interest, and when NPV is negative, the project will not be profitable enough (Shou, 2022). The advantage of NPV is that it considers the time value of money and uses all net cash flows of the project throughout the calculation period. Its weakness is that it cannot directly reflect the actual return level of the investment project dynamically (Sanam & Sartien, 2022) and, most importantly, assumes that the expected cash flow will certainly be realized at the end of the year (Kasprowicz et al., 2023), however, the literature shows investment decisions encompass uncertainty (Jing et al., 2023).

There are two common interpretations for the term “uncertainty”: in the field of operations research, this term is synonymous with ambiguity, indeterminacy, imprecision, etc., in data. That’s why (as we will see in the literature review) whenever uncertainty is mentioned, fuzzy sets and their extensions are discussed (Chrysafis & Papadopoulos, 2021; Deiva Ganesh & Kalpana, 2023; El-Morsy, 2023). Conversely, from an economic perspective, uncertainty has nothing to do with numerical representation (Sakai, 2019). Uncertainty is radically distinct from the familiar notion of risk, too. According to Knight, there are two kinds of uncertainties – measurable and non-measurable (or unmeasurable). Measurable uncertainty is not, in effect, an uncertainty at all; instead, it should be called “risk” properly. By contrast, non-measurable uncertainty is what he may call “true” uncertainty (Sakai, 2019). We have to make decisions based on imperfect estimates or judgments. We are now subject to non-measurable uncertainty. Any type of investment (physical or financial) may be fraught with random events, such as natural disasters or economic instability, that can hinder the expected return on investment (Delbari et al., 2022; Gaspars-Wieloch, 2019; Hosseini et al., 2023). In such situations, due to the irreversibility of real investment projects, decision-makers become cautious about investing when uncertainty shocks hit (Guceri & Albinowski, 2021).

Conversely, uncertainty is divided into internal and external categories. External uncertainties arise from the organization’s external environment and may relate to, for example, fluctuating economic conditions, changing customer demands/demographic changes, or emerging competitors/substitute products. This source of uncertainty is typically correlated with the economic environment (Delaney, 2021). Faced with a negative shock, individuals are affected by an emotion (fear) that alters their willingness to take risks in both financial and nonfinancial domains (Guiso et al., 2018). Many theories can explain changes in individual risk aversion: changes in wealth, changes in the outside environment, a significant shock on the expected distribution of returns, etc.; among them, a major shock can affect the emotions of investors and alter their decisions about their willingness to take risks because it changes their perceived utility loss of bad outcomes (Guiso et al., 2018). However, some studies base their analyses on the assumption of risk-neutral decision-makers (where all uncertainty can be perfectly hedged away) and develop models in which they assume that once the investment option is exercised, the payoff is received as a fixed lump sum and the investment problem immediately ends. These assumptions are irrelevant to most real-world investments (Delaney, 2021).

Practically, traditional valuation methods, such as NPV, do not account for uncertainty in calculating the expected return on investment (Dusseault & Pasquier, 2021). In response to this limitation, researchers have focused on sensitivity analysis, scenario analysis, simulation approaches, and real options analysis (ROA). In sensitivity analysis, after determining the problem solution, specific changes are examined in the parameters, such as the weights of the indicators (Ismail et al., 2023). In scenario analysis, due to computational constraints, human capacity, etc., a small number of scenarios (three or four) are considered (Bahrampour et al., 2022). In the simulation approach, the main objective is to find the optimal response in future scenarios, considering expected benefits, returns, and the level of risk (Tsvetkov & Bozmarova, 2023). In the ROA approach, specific investment opportunities are defined as “real options” (Li et al., 2024), and some types of them such as an (a) option to defer, (b) option to abandon/exit, (c) option to exchange, (d) option to grow/scale up, (e) option to contract/scale down, (f) option to switch, and (g) compound options are examined (Chi & Huang, 2023). In this study, we intend to approach the issue differently. The focus of this research is on uncertain conditions where changes in macroeconomic, political, and other indicators can influence decision outcomes (Imeni & Edalatpanah, 2023).

Accurate prediction of economic and financial factors is essential in investment decision-making. A decision that may seem appropriate in the present may no longer be suitable over time due to changes in influential variables (Faghihmaleki et al., 2023). Complete information is unavailable in such conditions, and risks and unknown areas may exist. In these situations, decision-makers can use the robustness analysis (RA) to evaluate different responses to various probabilities (Mohammad Ganji Nik et al., 2023). Unlike probability and certainty-based approaches, this approach seeks solutions that perform well against fluctuations and uncertainties (Sorourkhah, 2024). In RA, ranges are considered for different variable values instead of focusing on a specific value for each variable. Then, the effect of changes in these ranges on the examined result is examined. This approach allows decision-makers to make the best decisions despite changes and fluctuations, preserving desirable performance (Edalatpanah, 2022). Using RA, it is possible to simultaneously deal with different risks and probabilities, making decisions that resist these changes. This method assures decision-makers that decisions will remain stable and effective even in uncertain conditions, ensuring good performance over time (Mehregan et al., 2022).

Additionally, the constantly changing environment, coupled with severe challenges in predicting the future, has made decision-making in this regard more complex than ever (Xu et al., 2023). The unpredictability in this dynamic environment is much greater and more thought-provoking in Iran compared to stable economies (Mehrabi et al., 2023). A glance at some economic indicators in this country (such as inflation rates, exchange rates, interest rates, etc.) over the past few years effortlessly reveals the challenging and environment-dependent nature of investment project selection based on current net worth. Therefore, considering the uncertainty of the future in the examined issue is essential (Hamidavi Nasab et al., 2023). Accordingly, this research examines the problem of selecting an appropriate investment plan in such a context. In this research, to choose a suitable investment project based on the NPV model in conditions of future uncertainty, investment plans are first determined, alternative future scenarios are defined, and the robustness scores of options (investment plans) are calculated. The research background will be reviewed in the next section, and any existing research gaps will be highlighted. Following that, the proposed approach will be introduced and then implemented in a case study. Finally, the results will be discussed, research limitations will be addressed, and directions for future research will be suggested.

2 Literature Review

The current business environment, filled with uncertainty, has posed a significant challenge to the economic evaluation of projects. Over the past few years, researchers have made various efforts to address this issue. Some of these efforts highlighted the application of the NPV method in practice, while others aimed to optimize the NPV value through mathematical modelling. Other researchers focused on the problem of uncertainty in the economic evaluation of investment projects by applying ROA. Others used simulation approaches to tackle this problem, while another group of researchers employed scenario-based approaches to confront uncertainty.

A research paper proposed a comprehensive inventory model that considers the dynamic nature of demand for deteriorating items and incorporates the impact of inflation on the time value of money, all within the context of an imperfect production and screening process. The incorporation of an imperfect production process further enhances the model’s practical applicability by addressing real-world scenarios where production may not always be flawless. The study employs mathematical modelling and optimization techniques to derive optimal ordering policies that balance the conflicting objectives of minimizing costs. Sensitivity analyses are conducted to assess the robustness of the proposed model under varying parameters, providing valuable insights for decision-makers (Padiyar et al., 2024). A study considered the incorporation of the time value of money into the depreciation equation. The conventional straight-line depreciation equation was modified by incorporating the time value concept of money into the equation. A petroleum economic model was developed using a spreadsheet approach. The model was used to evaluate the impact of the modified straight-line depreciation model on the profitability of petroleum investments. Two petroleum investment scenarios were considered. Scenario 1 had the conventional depreciation model. Scenario 2 had the modified depreciation model for comparative analysis. The effect of the conventional and modified depreciation model on the profitability of the investment was evaluated. This allowed the contractor to mitigate the effect of risk associated with the value of the asset over time due to inflation (Ogolo et al., 2023). To design and evaluate a type of rooftop system considering economic feasibility, energy costs, and carbon dioxide offset, a researcher utilized the NPV model. The results indicated that this project would be valuable for investment due to its short payback period, significantly positive NPV, and confirmed internal rate of return (IRR) (Mongkoldhumrongkul, 2023). A study applied the NPV in public–private partnership (PPP) projects, where the government collaborates with the private sector in providing projects/services, with the private sector accepting the financial burden and sharing risks with the government. This research investigates various types of PPP projects in Egypt, including a rest area, a garage, and an airport (Kamel et al., 2022). A study was conducted to evaluate energy retrofitting projects for building resilience. The researchers believed that due to increased social awareness and environmental concerns, homeowners might prefer to invest in more cost-effective solutions rather than low-cost ones. To assess the economic viability of projects, they completed the life cycle cost method with the NPV method. They determined the best retrofitting project by executing two criteria: reducing primary energy consumption and increasing NPV benefits compared to the current state (Bragolusi & D’Alpaos, 2022).

Two researchers aimed to address the uncertainty in investment decisions in the transportation industry by utilizing fuzzy set theories. They believed the fuzzy set theory could represent uncertainty and ambiguity in decision-making problems. This study aimed to evaluate ship investment using NPV, Profitability Index, and Payback Period under a Type-2 fuzzy environment. Additionally, two methods, Type-2 Fuzzy Payback Period (IT2FPP) and Type-2 Fuzzy Profitability Index (IT2FPI), were developed in this research (Akan & Bayar, 2022). In a study, the use of the detached net present value (DNPV) fuzzy phase has been proposed. Risk assessment through fuzzy mathematics analysis of pepper farms for 2016 and 2017 has been conducted. The use of DNPV eliminates the risk insurance rate. It enables increased precision and quantification of risks, separating significant risks such as price fluctuations, temporary and specific events, or salinity (Brotons-Martínez et al., 2022). Researchers argued that classic methods (NPV and IRR) have limitations when understanding relevant features for decision-making in high-risk investments, such as uncertainty in cash flows and risk quantification. An alternative to these methods is a technique known as DNPV. This technique separates project-related risks from the monetary value over time. This evaluation method was applied to Colombia’s self-sustaining solar photovoltaic energy project. In this study, the results obtained through DNPV were 2.3 times the value obtained using NPV. Therefore, many renewable energy projects may be undervalued, as traditional methods mistakenly associate a high insurance rate, often related to project financing resources, instead of demonstrating the inherent risk component (Martínez-Ruiz et al., 2021). The authors addressed change requests throughout the project lifecycle by employing fuzzy numbers, fuzzy probability moments, and a combined fuzzy estimator (fuzzy statistics) to introduce a probabilistic fuzzy version of the expanded net present value (FPeNPV) method. This approach comprises two fuzzy components: fuzzy probabilistic NPV and fuzzy option insurance. The algorithm leads to calculating FPeNPV through nine main stages, allowing the government to adapt to changes in internal and external environments (Chrysafis & Papadopoulos, 2021). Two researchers stated hybrid ground-source heat pump systems can heat and cool buildings by exchanging heat with geologically warm and cold materials. However, their size is complex, and due to uncertainty that distorts essential design parameters, their financial profitability during the design phase is challenging. They demonstrated how NPV at risk, a financial indicator inspired by a criterion used in the financial sector, could create the effects of uncertainties during the design phase. The results showed that this financial indicator, while yielding a higher calculated value than the NPV, leads to shorter payback periods, significantly reduces unforeseen financial risks, and does not require further sensitivity analysis (Dusseault & Pasquier, 2021).

Employing the ROA model, researchers have analysed the dynamics of the post-pandemic business landscape, employing the concepts of liability options and societal norms. Their analysis suggested that measures such as social distancing or regulatory directives, which affect business profitability, will give rise to two distinct operational paradigms: liability or property risk management strategies. The choice between these paradigms hinges on how a company’s projected revenues and resultant social costs compare to established societal norms. Accordingly, firms will operate under one of these frameworks based on their unique attributes and the degree of uncertainty they confront. In both scenarios, businesses will experience a reduction in profits commensurate with the social costs surpassing the established norm (Scandizzo & Knudsen, 2024). A comparison analysis was conducted in a study to analyse a ship investment problem using NPV and ROA empirically. This study aimed to suggest improvement measures through a real option valuation methodology for ship investment that could factor in uncertainty. This analysis was conducted through the option to defer for 2 years and the option to expand, placing additional orders for eight vessels depending on market conditions within 2 years after the initial order of eight vessels. As a result of the comparative analysis, it was confirmed that the real option showed a higher value of ship investment than the traditional valuation and affected investment decision-making since it considered uncertainty in the event of ship investment (Kim et al., 2024). A study utilized ROA to determine the most advantageous time for energy companies to retire their power plants and forecast the future trend of renewable energy waste from a bottom-up approach. The findings indicated that the optimal retirement period for the four segmented categories falls between 16 and 23 years. Delayed investments resulted in earlier decommissioning times and diminished project returns. Additionally, wind projects generated greater revenue than PV projects of equal size, with the disparity consistently increasing (Chen et al., 2024). A study was conducted to determine if a model demonstrates better valuation to analyse various models for evaluating investment projects in a company. Four valuation models were applied to a marine seaweed production and marketing company, including three classic models (NPV, IRR, and return on investment) and a newer model (ROA). The results showed that the ROA model, considering the flexibility provided by the expansion option in calculations, estimates a higher added value (Pérez-Vas et al., 2021).

Some argue that increasing the analysis of one-sided effects, as quantified through quantitative simulation, can create a balance between impact and anti-competitive efficiencies, improving the integration examination process. Complex economic models impose a compressed structure on the analytical process, neglecting the likelihood of various effects occurring and focusing solely on an approximate estimation of the price effect of integration. They suggested that addressing this issue through an adjusted NPV model with simple risk could provide a more comprehensive examination of the integration’s impact on a consumer welfare price index (Simons & Coate, 2022). Researchers estimated the economic value of improving carbon planning and the carbon trading market using the NPV approach. This study simulated the spatial distribution of carbon sequestration in 2030 and 2050 using the Land Use Simulation (PLUS) and NPV simulation models. Under two discount rates, this model calculated the carbon value in 2012, 2016, 2020, 2030, and 2050 (Ma et al., 2022). Some researchers have suggested combining NPV with related financial figures in a binary tree. This approach allows for evolving and adjusting to different world states at any given moment. Modelling cash flows in a binary tree requires a variable part based on relationships with a precisely defined random variable and a constant component at a specific moment (Arnold et al., 2022). A study considered input variables such as NPV, IRR, project payback period, ARR, and capital return index. The output variable determined the probability of project acceptance, effectiveness, and associated risks during implementation. Triangular and trapezoidal fuzzy numbers were suggested as linguistic terms. The authors used a fuzzy logic approach to assess the efficiency of investment projects based on production laws. This approach simplifies the evaluation process of investment projects, particularly in cases where influential factors (evaluation criteria) are not mathematically related to a single formality and their number is sufficiently large for calculations (Lavrynenko et al., 2020). A paper described a potential change in the NPV, allowing projects to be evaluated under uncertainty with unknown probabilities (primarily understood as frequency). Cash flows are usually uncertain as project revenues and costs are related to the future. Moreover, the probabilities of specific scenarios may be uncertain due to various unknown factors (such as diversity of definitions for probability, lack of historical data, and insufficient knowledge about possible states of nature). The proposed approach is based on a combination of Hurwicz and Bayes decision rules and is supported by a sensitivity analysis. It utilizes scenario programming and considers the decision-maker’s attitude towards a specific decision problem (measured with pessimistic and optimistic coefficients). This method can even be applied to the asymmetric distribution of net cash flows in particular periods, as it considers the frequency of each value (Gaspars-Wieloch, 2019). A study proposed a method for calculating the NPV of financial processes by considering the variance and correlation of uncertain parameters. It introduced a robust approach to NPV computation, which involved formulating the mathematical framework for robust NPV calculation. Uncertain parameter changes were assumed to occur within a closed and convex region referred to as the uncertainty region. The size and shape of this region were determined based on historical data and the investor’s risk preferences. The robust NPV calculation was implemented in a C++ programming environment, and its effectiveness was evaluated through numerical examples. Simulation of 10,000 random scenarios of uncertain parameters illustrated that while the traditional NPV computation method often fails to provide reliable decisions in certain situations, the robust approach consistently avoids such failures (Hanafizadeh & Latif, 2011).

A multi-criteria decision-making approach was utilized in a study to assess and select projects. NPV, investment size, payback period, cost-benefit analysis, and time to break even were used to select and evaluate projects. The fuzzy analytic hierarchy process was employed in the hierarchical analysis process. In contrast, fuzzy TOPSIS was used to determine the overall weights for each of the five investment options (Vijayakumar et al., 2022). Researchers argued that a downhole coaxial heat exchanger geothermal system must have an economical horizontal cross-sectional length to evaluate heat extraction performance. They created an economic evaluation model with a horizontal well based on NPV to identify the optimal length. The results showed that the project can only be profitable when the horizontal well is between 0 and 4,009 m, with an optimal economical length of 1,466 m. Two researchers, recognizing the need for substantial investments in green energy projects, suggested using the NPV method. They highlighted a research gap and demonstrated, based on data from Poland, Romania, Hungary, Croatia, the United States, etc., that the discount rate variable affects the time value of money. Therefore, they concluded that redefining the NPV formula is necessary. They claimed that this research contributes to the capital budgeting process, and a modified NPV formula can provide optimal results, reducing financial risks in companies (Dobrowolski & Drozdowski, 2022). A study aimed to assess the feasibility of landfill waste burial projects by incorporating their environmental values into project evaluations. Simultaneously, three policy-related methods (non-market valuation, benefits transfer, and cost-benefit analysis) were employed in two study areas. Positive NPV empirical evidence was presented for the landfill waste burial project feasibility study. The findings indicated that including environmental values in project evaluations increases the chances of implementing sanitary landfills and offers a new approach to addressing environmental concerns in developing countries (Nik Ab Rahim et al., 2021). Another study examined an energy efficiency project using the NPV method. This research aimed to improve energy utilization in the studied industrial plant. Choosing which turbine to purchase for the energy efficiency project is a complex decision-making problem. For this purpose, a financial analysis through NPV using standard steam system behaviour information was proposed (Cordi et al., 2020). A research study was conducted to evaluate the investment in purchasing CT scan machines in a government hospital, assessing the feasibility of the investment from financial aspects. The capital budgeting technique used in this research included the payback period and NPV (Setiadi et al., 2020).

Upon reviewing the research background, it is evident that researchers have mainly focused on using sensitivity analysis, scenario analysis, simulation, and ROA approaches to address uncertainty-related issues. These techniques have proven effective in handling uncertainty and have been extensively researched in the literature. However, the proposed method in the present study offers a unique perspective on investment decision-making by focusing on robustness and effectiveness in uncertain conditions, considering ranges of variable values, and seeking solutions that perform well against fluctuations and uncertainties. While the other methods provide valuable insights, they may not offer the same level of robustness and stability in decision-making under uncertainty. The contributions of the study are as follows:

Integration of NPV Model with RA: The study proposes a novel approach that integrates NPV with RA to address the challenge of prioritizing investment plans in conditions of future uncertainty. This integration offers an algorithm for evaluating investment projects while considering the impact of uncertain variables.

Addressing Real-World Uncertainty: The proposed approach acknowledges the presence of uncertainty in investment decision-making. From a distinct viewpoint, the study provides a practical framework for decision-makers to assess investment options in dynamic and uncertain environments.

Methodological Advancement: The study contributes to methodological advancement in investment decision-making by introducing RA as a tool for evaluating investment projects. This approach goes beyond other methods by focusing on stability and effectiveness in uncertain conditions.

Practical Implications for Decision-Makers: The proposed approach offers practical implications for decision-makers by providing a framework to evaluate investment projects that can withstand changes and fluctuations in the external environment. By considering ranges of variable values and assessing the impact of uncertainty on decision outcomes, decision-makers can make more informed and resilient investment decisions.

Case Study Implementation: The study plans to implement the proposed approach in a case study, which will provide empirical evidence of its effectiveness in real-world investment scenarios. This empirical validation will enhance the credibility and applicability of the proposed method.

3 Methodology

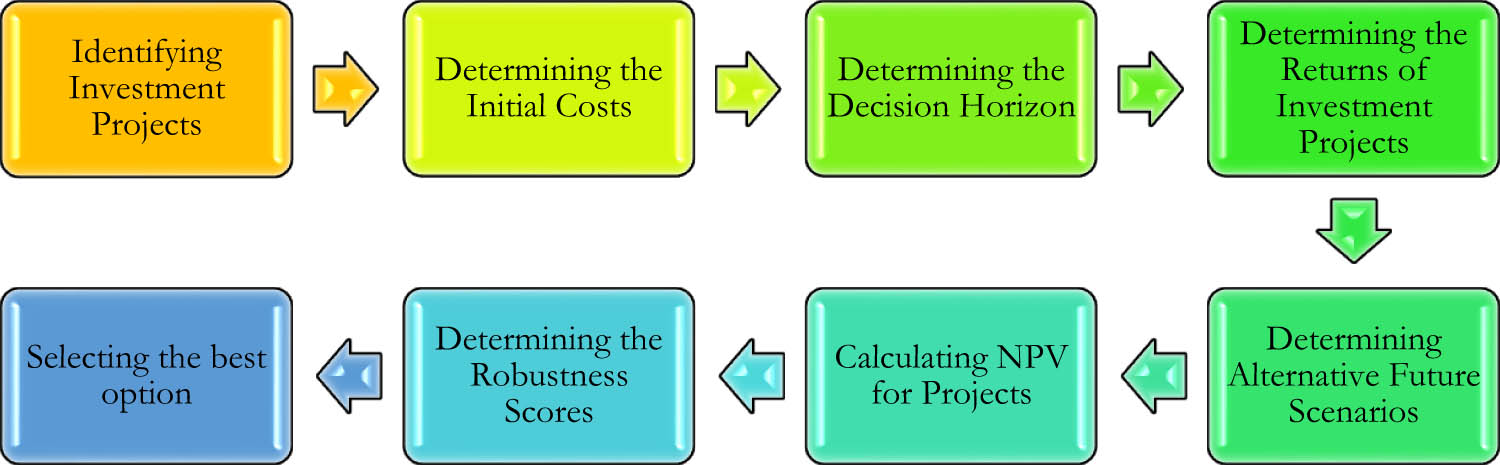

The current research problem pertains to prioritizing investment projects under uncertainty. The most commonly used approach in this area is the NPV method, which selects the best ones by considering the present value of the differences between incomes and costs of various projects. Despite its various advantages, this approach lacks the ability to consider changes. Based on this, we believe that combining the RA approach with the aforementioned method can enhance decision-making certainty. Eight steps outlined in Figure 1 must be followed to implement the proposed algorithm:

Step 1 – Identifying Decision Options/Investment Projects (d i , i = 1, 2, …, n)

In this step, the responsibility of selecting investment projects lies with the problem owner. These projects may vary, have different durations, and their lifetimes may not be uniform.

Step 2 – Determining the Initial Cost of Investment Projects (C 0i , i = 1, 2, …, n)

In this step, it is necessary to specify the capital required to launch each decision option. Costs can be certain or estimated. Estimating the costs associated with investment projects is the responsibility of the problem owner, and this study gathered these costs with the assistance of consultants and experts in the field.

Step 3 – Determining the Decision Horizon (T j , j = 1, 2, …, t)

According to the RA approach, which requires a specified horizon, we determine the timeframe in which investment projects are evaluated in this step. Based on the problem owner’s perspective, this timeframe can be set at 1, 3, 5, 10 years, etc. In this research, a 5-year horizon is considered, and accordingly, the returns from investment projects within these 5 years are examined.

Step 4 – Determining the Returns of Investment Projects (C ij , i = 1, 2, …, n and j = 1, 2, …, t)

This step estimates returns from each investment project over the specified timeframe. These estimates can be intuitive or obtained using predictive models. In this study, the problem owner provides intuitive estimates with the assistance of experts in the field. Estimates will be made in optimistic

Step 5 – Determining Alternative Future Scenarios (Sn p , p = 1, 2, …, m)

In this step, future scenarios are defined. Various indicators can be used depending on the problem under investigation and its specific characteristics. The most influential macro indicators, political, economic, and social factors, are typically employed in RA literature (Joorbonyan et al., 2024). Conversely, in the literature on investment project selection, as demonstrated in the research background, the interest rate is considered reliable. In this study, with the consultation of the problem owner, the interest rate (k) will be used to define future scenarios. It is worth noting that different interest rates are determined based on the views of technical experts and references to library resources.

Step 6 – Calculating NPVs for Projects in Different Scenarios (NPV ip , i = 1, 2, …, n and p = 1, 2, …, m)

In this step, the NPV index for investment projects is calculated in optimistic

(1)where C i0 represents the initial investment cost of project i at present, C it indicates the returns from project i in year t, and k is the interest rate.

Considering that the initial costs of investment projects differ from each other, the net present value ratio (NPVR) is used according to equation (2) (Alishahi et al., 2011):

(2)where PV i

(3)Step 7 – Determining the Robustness Scores (R ip , i = 1, 2, …, n and p = 1, 2, …, m)

The proposed algorithm process.

In Step 7, after determining the NPVR index of investment projects in optimistic, pessimistic, and probable scenarios using equation (2), we form the robustness matrix, in which positive NPVR elements are considered as 1 (one); otherwise, they are considered as 0 (zero).

Step 8 – Selecting the Best Option/Project (Max ΣR i , i = 1, 2, …, n)

Finally, using equation (5), we calculate the robustness score of decision options:

The option that achieves the highest robustness score (across optimistic, pessimistic, and probable scenarios) is considered superior.

4 Case Study

This research explicitly addresses the problem of selecting the most suitable investment project among several options in Tonekabon, Iran. A decision-maker (problem owner) will choose the most appropriate investment plan from seven options: cafe, restaurant, eco-lodge, water recreation, vitamin store, fast food, and traditional restaurant. The problem owner decided to use the NPV model for decision-making. Considering the existing uncertainty in the business environment, especially in the current situation in Iran, there was a need to incorporate this issue into the analysis.

The study’s considerations include the following assumptions:

Opting for one project precludes considering others.

Investment occurs once and at the outset of the period; there’s no reinvestment.

Sufficient capital for project implementation is assumed, with no constraints on the problem owner.

The problem owner provides precise estimations of the capital required for each project.

All investment projects adhere to a consistent evaluation horizon.

Optimistic, probable, and pessimistic estimates regarding returns determined by the problem owner implicitly and subjectively incorporate factors like inflation rates, exchange rates, and taxes.

All future scenarios are weighted equally in terms of their probability of occurrence.

Operational efficiency measures, such as cost controls or productivity enhancements, remain consistent across all projects.

In the following, a combination of the NPV model and RA, as outlined in the previous section, was implemented as follows:

Steps 1 and 2:

In the first step of the approach, the problem owner introduced the seven investment projects, among which they were undecided. In the next step, the cost required for each of these projects was provided. The results of the initial two stages of the proposed approach are shown in Table 1.

Step 3:

The previous section mentioned that determining the required horizon is necessary in applying the RA approach (in the NPV model, there is no such requirement). Therefore, with the agreement of the decision-maker, the horizon for evaluating the projects was set at 5 years.

Step 4:

Investment projects and initial costs

| Row | Project | Cost (in 1,000 currency units) |

|---|---|---|

| 1 | Cafe | 2,200 |

| 2 | Restaurant | 2,700 |

| 3 | Eco-lodge | 4,300 |

| 4 | Water recreation | 1,000 |

| 5 | Vitamin store | 1,300 |

| 6 | Fast food | 2,500 |

| 7 | Traditional restaurant | 1,800 |

In this step, it is necessary to determine the returns from the investment projects. The decision-maker, with the assistance of consultants and experts in the field, estimated the returns of the projects at this stage. Given the intuitive nature of the estimates, we asked the decision-maker to provide the estimates in optimistic, pessimistic, and probable scenarios. These estimates are presented in Tables 2–4, respectively.

Step 5:

To define future scenarios, the most critical variable that could significantly impact the analysis results (i.e., the interest rate) was considered in this research. We examined the country’s primary source of economic trends to determine potential interest rates.

In a survey conducted by “Farda-e-Eghtesad[1]” with 230 economic analysts and experts, the question was raised about the expected interest rate in the year 1402 (the Iranian calendar, which corresponds to the year 2023–2024). The comprehensive results of this survey showed that approximately 54% of the participants expected the deposit and bond interest rates in the year 1402 to be between 22 and 26%, while 28% predicted interest rates between 26 and 30%. About 18% also anticipated these rates would fall between 18 and 22%.

Based on this, we considered interest rates in this study in seven scenarios: 18, 20, 22, 24, 26, 28, and 30%. Therefore, we have seven scenarios in each optimistic, pessimistic, and probable scenario, resulting in 21 alternative future scenarios.

Step 6:

Returns in optimistic scenarios

| Row | Project | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

|---|---|---|---|---|---|---|

| 1 | Cafe | 0 | 900 | 1,200 | 1,400 | 1,580 |

| 2 | Restaurant | 0 | 940 | 1,410 | 1,720 | 2,320 |

| 3 | Eco-lodge | 450 | 1,180 | 2,500 | 3,100 | 3,500 |

| 4 | Water recreation | 410 | 520 | 570 | 550 | 550 |

| 5 | Vitamin store | 100 | 420 | 570 | 810 | 1,550 |

| 6 | Fast food | 250 | 900 | 1,350 | 1,750 | 2,100 |

| 7 | Traditional restaurant | 280 | 830 | 1,240 | 1,610 | 1,600 |

Returns in pessimistic scenarios

| Row | Project | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

|---|---|---|---|---|---|---|

| 1 | Cafe | −230 | 510 | 790 | 980 | 1,230 |

| 2 | Restaurant | −150 | 710 | 1,160 | 1,490 | 1,990 |

| 3 | Eco-lodge | 210 | 840 | 1,710 | 2,680 | 3,050 |

| 4 | Water recreation | 320 | 450 | 500 | 410 | 375 |

| 5 | Vitamin store | 0 | 385 | 525 | 730 | 1,150 |

| 6 | Fast food | 110 | 670 | 1,120 | 1,240 | 1,390 |

| 7 | Traditional restaurant | 170 | 490 | 790 | 1,080 | 1,300 |

Returns in probable scenarios

| Row | Project | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

|---|---|---|---|---|---|---|

| 1 | Cafe | −50 | 820 | 1,050 | 1,220 | 1,470 |

| 2 | Restaurant | −100 | 900 | 1,380 | 1,690 | 2,100 |

| 3 | Eco-lodge | 370 | 1,100 | 2,250 | 3,050 | 3,490 |

| 4 | Water recreation | 350 | 480 | 510 | 420 | 390 |

| 5 | Vitamin store | 50 | 400 | 550 | 800 | 1,500 |

| 6 | Fast food | 220 | 870 | 1,310 | 1,600 | 2,100 |

| 7 | Traditional restaurant | 250 | 710 | 1,180 | 1,610 | 1,500 |

In this step, using equation (2), the NPVR values for various projects were calculated in optimistic, pessimistic, and probable scenarios. Table 5 displays the NPVR indices in the optimistic scenario, respectively.

Projects’ NPVRs in optimistic scenarios

| Row | Project | 18% | 20% | 22% | 24% | 26% | 28% | 30% |

|---|---|---|---|---|---|---|---|---|

| 1 | Cafe | 0.21 | 0.15 | 0.10 | 0.05 | 0.01 | −0.03 | −0.07 |

| 2 | Restaurant | 0.21 | 0.15 | 0.10 | 0.05 | 0.00 | −0.04 | −0.08 |

| 3 | Eco-lodge | 0.27 | 0.21 | 0.16 | 0.11 | 0.07 | 0.02 | −0.02 |

| 4 | Water recreation | 0.37 | 0.20 | 0.16 | 0.12 | 0.08 | 0.05 | 0.01 |

| 5 | Vitamin store | 0.29 | 0.23 | 0.17 | 0.12 | 0.08 | 0.03 | −0.01 |

| 6 | Fast food | 0.29 | 0.23 | 0.18 | 0.13 | 0.08 | 0.04 | 0.01 |

| 7 | Restaurant | 0.42 | 0.37 | 0.32 | 0.27 | 0.23 | 0.19 | 0.15 |

Table 6 presents the NPVR indices in the pessimistic scenario.

Projects’ NPVRs in pessimistic scenarios

| Row | Project | 18% | 20% | 22% | 24% | 26% | 28% | 30% |

|---|---|---|---|---|---|---|---|---|

| 1 | Cafe | −0.30 | −0.36 | −0.42 | −0.48 | −0.53 | −0.57 | −0.61 |

| 2 | Restaurant | 0.01 | −0.05 | −0.11 | −0.16 | −0.21 | −0.26 | −0.30 |

| 3 | Eco-lodge | 0.05 | −0.01 | −0.06 | −0.11 | −0.16 | −0.20 | −0.24 |

| 4 | Water recreation | 0.22 | 0.01 | −0.03 | −0.07 | −0.10 | −0.14 | −0.17 |

| 5 | Vitamin store | 0.12 | 0.06 | 0.00 | −0.05 | −0.10 | −0.14 | −0.18 |

| 6 | Fast food | 0.00 | −0.06 | −0.11 | −0.16 | −0.20 | −0.24 | −0.28 |

| 7 | Restaurant | 0.14 | 0.09 | 0.03 | −0.01 | −0.06 | −0.10 | −0.14 |

Table 7 presents the NPVR indices in the probable scenario.

Step 7:

Projects’ NPVRs in probable scenarios

| Row | Project | 18% | 20% | 22% | 24% | 26% | 28% | 30% |

|---|---|---|---|---|---|---|---|---|

| 1 | Cafe | 0.10 | 0.05 | −0.01 | −0.06 | −0.10 | −0.14 | −0.18 |

| 2 | Restaurant | 0.15 | 0.09 | 0.04 | −0.01 | −0.06 | −0.10 | −0.14 |

| 3 | Eco-lodge | 0.23 | 0.17 | 0.12 | 0.07 | 0.02 | −0.02 | −0.06 |

| 4 | Water recreation | 0.25 | 0.06 | 0.02 | −0.02 | −0.06 | −0.09 | −0.12 |

| 5 | Vitamin store | 0.25 | 0.19 | 0.13 | 0.08 | 0.03 | −0.01 | −0.05 |

| 6 | Fast food | 0.29 | 0.23 | 0.18 | 0.13 | 0.08 | 0.04 | 0.00 |

| 7 | Restaurant | 0.38 | 0.33 | 0.28 | 0.23 | 0.19 | 0.15 | 0.11 |

Based on the NPVRs obtained in the previous step, we form the robustness matrices in this step, considering 1 for positive elements and 0 for negative elements. Considering Table 5, the robustness scores of investment projects in the optimistic scenario are presented in Table 8:

Projects’ robustness scores in optimistic scenarios

| Row | Project | 18% | 20% | 22% | 24% | 26% | 28% | 30% | Robustness |

|---|---|---|---|---|---|---|---|---|---|

| 1 | Cafe | 1 | 1 | 1 | 1 | 1 | 0 | 0 | 5 |

| 2 | Restaurant | 1 | 1 | 1 | 1 | 1 | 0 | 0 | 5 |

| 3 | Eco-lodge | 1 | 1 | 1 | 1 | 1 | 1 | 0 | 6 |

| 4 | Water recreation | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 7 |

| 5 | Vitamin store | 1 | 1 | 1 | 1 | 1 | 1 | 0 | 6 |

| 6 | Fast food | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 7 |

| 7 | Restaurant | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 7 |

Figure 2 illustrates the robustness scores of investment projects in the optimistic scenarios.

The robustness scores of investment projects in the optimistic scenarios.

As evident in Figure 2, in the optimistic state, the superior investment projects are those related to water recreation, fast food, and restaurants.

In the same manner, considering Table 6, the robustness scores of investment projects in the pessimistic scenarios are shown in Table 9.

Projects’ robustness scores in pessimistic scenarios

| Row | Project | 18% | 20% | 22% | 24% | 26% | 28% | 30% | Robustness |

|---|---|---|---|---|---|---|---|---|---|

| 1 | Cafe | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 2 | Restaurant | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 3 | Eco-lodge | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 4 | Water recreation | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 2 |

| 5 | Vitamin store | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 3 |

| 6 | Fast food | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| 7 | Restaurant | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 3 |

Figure 3 illustrates the robustness scores of investment projects in the pessimistic scenarios.

The robustness scores of investment projects in the pessimistic scenarios.

As shown in Figure 3, in the pessimistic state, the superior investment projects are vitamin stores and restaurants.

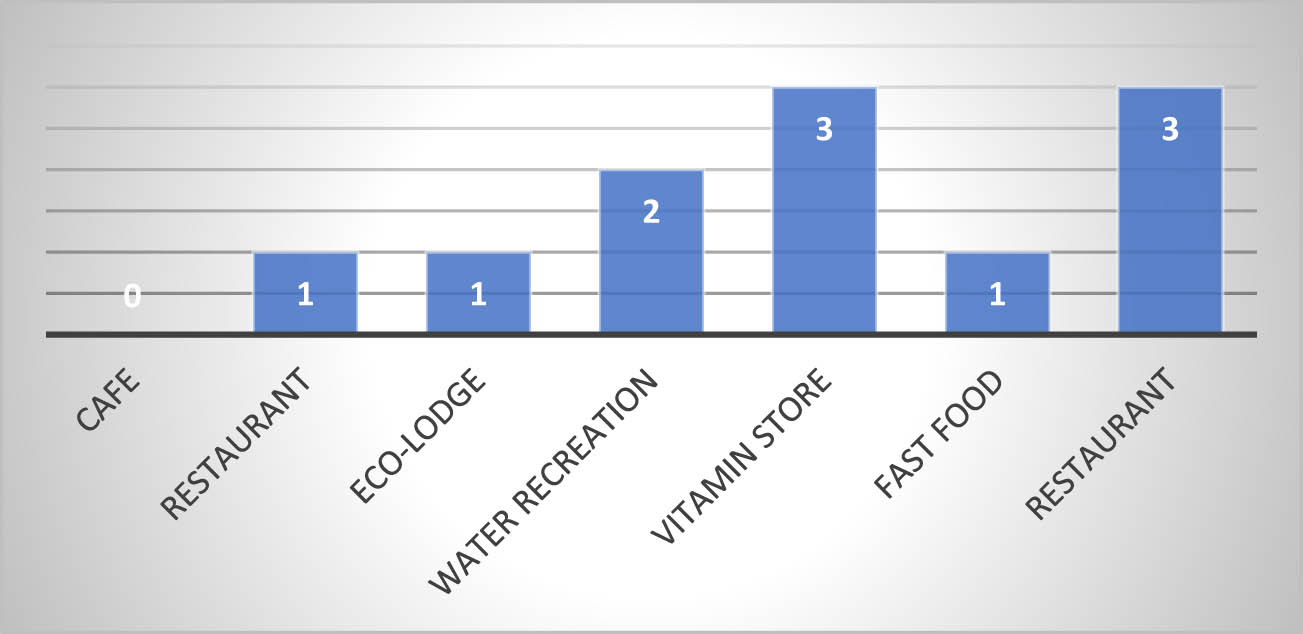

In the same manner, considering Table 7, the robustness scores of investment projects in the probable scenario are shown in Table 10.

Projects’ robustness scores in probable scenarios

| Row | Project | 18% | 20% | 22% | 24% | 26% | 28% | 30% | Robustness |

|---|---|---|---|---|---|---|---|---|---|

| 1 | Cafe | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 2 |

| 2 | Restaurant | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 3 |

| 3 | Eco-lodge | 1 | 1 | 1 | 1 | 1 | 0 | 0 | 5 |

| 4 | Water recreation | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 3 |

| 5 | Vitamin store | 1 | 1 | 1 | 1 | 1 | 0 | 0 | 5 |

| 6 | Fast food | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 7 |

| 7 | Restaurant | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 7 |

Figure 4 illustrates the robustness scores of investment projects in the probable scenarios.

The robustness scores of investment projects in the probable scenarios.

According to Figure 4, the restaurant and fast-food projects are superior investments in the probable scenario.

Step 8:

In the final step, the investment project that obtains the highest robustness score across 21 future scenarios (seven different interest rates and three states: optimistic, pessimistic, and probable) is selected as the superior plan. The results of the above analysis are illustrated in Figure 5.

The overall robustness scores of investment projects.

Considering Figure 5, it becomes evident that the restaurant project, with a robustness score of 17 in a total of 21 future scenarios, is the top investment project. Following that, the fast-food and vitamin projects, with robustness scores of 15 and 14, respectively, secure the following positions. It is also apparent that the café investment project, with a robustness score of 7, is the least suitable investment option.

5 Conclusion

One of the most challenging decision-making areas that has been the focus of researchers for years is the problem of choosing an appropriate investment project among various options (Bao & Pouresmaeil Motlagh, 2024). Despite various methods for evaluating investment projects, one of the essential and widely used tools in this field is the concept of NPV (Fakher, 2021). In practice, traditional valuation methods, such as NPV, do not account for uncertainty in assessing alternatives (Nozarpour et al., 2023). Furthermore, although possessing positive attributes, the methods or approaches that have garnered expert attention in addressing this deficiency have not scrutinized the aspect of uncertainty in a manner akin to that explored in this research. The focal point of this research is how, in uncertain conditions where changes in macroeconomic and political indicators can influence decision outcomes, one can evaluate options using the NPV index within the framework of alternative future scenarios.

We suggested a hybrid NPV-RA algorithm to enhance confidence in investment decision-making. The research focused on selecting the most suitable investment project among several options in Tonekabon, Iran. The decision-maker introduced seven investment projects, and their costs and returns were determined in optimistic, pessimistic, and probable states. The most critical variable, the interest rate, was considered in seven different scenarios based on the survey results from a reliable economic trends media outlet. Next, the NPVRs for all projects were calculated under optimistic, pessimistic, and probable states with varying interest rates. Based on the obtained NPVRs, robustness matrices were constructed. Finally, with a robustness score of 17, the restaurant project was identified as the best investment project across 21 future scenarios, and the cafe project was identified as the least suitable, with a robustness score of 7.

The proposed method differs in several ways from sensitivity analysis, scenario analysis, simulation methods, and ROA. The most significant difference lies in the type of response the discussed approaches provide. While other approaches seek to provide an optimal answer, NPV-RA seeks a response that will maintain its performance in the event of different scenarios in the future and focuses on evaluating different responses to various probabilities. RA seeks solutions that perform well against environmental fluctuations and uncertainties rather than pinpointing specific variables or scenarios. RA considers uncertainty by examining ranges of different variable values rather than focusing on specific values or scenarios. It seeks to make stable and effective decisions even in uncertain conditions, ensuring good performance over time. Other methods may address uncertainty somewhat, but RA specifically aims to deal with uncertainty by preserving desirable performance despite changes and fluctuations. While sensitivity analysis, scenario analysis, simulation, and ROA methods provide insights into how specific variables, scenarios, or options affect investment decisions, RA takes a broader approach by simultaneously dealing with different risks and probabilities. Considering various uncertainties, it assures decision-makers that decisions will remain stable and effective. Moreover, it is worth mentioning that the NPV-RA approach differs from robust NPV. While RA falls into the category of soft operations research (Soft OR), robust NPV belongs to hard operations research (Hard OR), which seeks optimal answers.

However, the present study has limitations that must be considered in future studies. While applying the proposed approach is recommended in other cases, fields, and countries, the generalizability of its results is questionable for several reasons. The assumptions made in this study, especially assumptions 2, 4, 5, 6, and 8, may not align with some real-world scenarios. Therefore, it is advisable to investigate the problem by altering these assumptions in future research. For example, if investments occur multiple times or there are reinvestments, the model may incorporate cash flows for each investment period separately by adjusting the cash flow timeline and discounting each cash flow appropriately based on when it occurs. If precise estimations are not available, the model may include a range of potential capital requirements and use a probabilistic/hesitant fuzzy approach to account for the uncertainty. If investments occur multiple times or there are reinvestments, precise estimations are not available, or projects have different evaluation horizons, compound interest can be applied.

Although most companies all over the world prefer NPV rather than IRR, the usage of NPV or IRR can be different on a country-by-country basis (Wang, 2021). Some believe that ranking the investment project using IRR and rejecting marginal projects offers several preponderances over an NPV criterion with cash flow adjustments (Yan & Zhang, 2022). Additionally, depending on an investor’s risk profile, they may prefer a project with a higher IRR in several scenarios to a lower one in a higher number of scenarios. Therefore, using the IRR approach alongside NPV, comparing the results, and providing further analysis could be considered in future studies.

The study was conducted in a city in Iran where, unfortunately, ecological issues are not given the deserved attention by decision-makers or local authorities. This negligence is in contrast to other countries, especially developed ones, where considering this indicator will play a significant role in evaluating investment options (Alkaraan et al., 2023). Another drawback of the proposed approach is that all future scenarios have been considered with equal weights, whereas future research could consider the probability of occurrence for scenarios by using the analytic hierarchy process, analytic network process, etc. (Sharma et al., 2019). Finally, the RA approach is conservative and aimed at reducing risk in changing conditions, making avoiding losses the basis for selecting the best option. In contrast, the antifragility analysis approach aims to select an option that maximizes the benefit for the problem owner (Li et al., 2023). Combining antifragility analysis with NPV could be of interest to researchers in future studies.

Acknowledgement

We appreciate all seven reviewers for their insightful feedback and valuable suggestions, which have significantly improved the quality of this manuscript.

-

Funding information: Authors state no funding involved.

-

Author contributions: All authors have accepted responsibility for the entire content of this manuscript and consented to its submission to the journal, reviewed all the results and approved the final version of the manuscript. AS and SS contributed to the conception and design of the study. AS was responsible for methodology, data curation, investigation, and writing the original draft. SS conducted the formal analysis, developed the necessary software, and validated the results. Both authors reviewed and edited the manuscript to reach its final form. All authors have read and approved the final manuscript.

-

Conflict of interest: Authors state no conflict of interest.

-

Data availability statement: All relevant data and materials are available within the text of the manuscript.

-

Article note: As part of the open assessment, reviews and the original submission are available as supplementary files on our website.

References

Akan, E., & Bayar, S. (2022). An evaluation of ship investment in interval type-2 fuzzy environment. Journal of the Operational Research Society, 73(8), 1768–1786. doi: 10.1080/01605682.2021.1944826.Search in Google Scholar

Alishahi, N., Zandi, F., & Mousavi, F. (2011). Combining real options and NPV methods for assessing IT investments. Alzahra University.Search in Google Scholar

Alkaraan, F., Elmarzouky, M., Hussainey, K., & Venkatesh, V. G. (2023). Sustainable strategic investment decision-making practices in UK companies: The influence of governance mechanisms on synergy between industry 4.0 and circular economy. Technological Forecasting and Social Change, 187, 122187. doi: 10.1016/j.techfore.2022.122187.Search in Google Scholar

Arnold, T., Crack, T. F., & Schwartz, A. (2022). Embedding a net present value analysis into a binomial tree with a real option analysis. Managerial and Decision Economics, 43(7), 2924–2934. doi: 10.1002/mde.3572.Search in Google Scholar

Bahrampour, P., Najafi, S. E., Hosseinzadeh Lotfi, F., & Edalatpanah, A. (2022). Development of scenario-based mathematical model for sustainable closed loop supply chain considering reliability of direct logistics elements. Journal of Quality Engineering and Production Optimization, 7(2), 232–266. doi: 10.22070/jqepo.2022.15643.1219.Search in Google Scholar

Balaei, S., Mohammadi, N., & Doroudi, H. (2023). Designing a hybrid model for the green supply chain in Gilan Steel Industry. International Journal of Research in Industrial Engineering, 12(1), 73–87. doi: 10.22105/riej.2022.298634.1327.Search in Google Scholar

Bao, Z., & Pouresmaeil Motlagh, B. (2024). How investment efficiency affects firms performance? Accounting and Auditing with Applications, 1(1), 17–26. https://www.journal-aaa.com/journal/article/view/19.Search in Google Scholar

Bragolusi, P., & D’Alpaos, C. (2022). The valuation of buildings energy retrofitting: A multiple-criteria approach to reconcile cost-benefit trade-offs and energy savings. Applied Energy, 310, 118431. doi: 10.1016/j.apenergy.2021.118431.Search in Google Scholar

Brealey, R., Myers, S., & Allen, F. (2020). Principles of corporate finance (13th ed.). McGraw-Hill Education.Search in Google Scholar

Brotons-Martínez, J. M., Galvez, A., Chavez-Rivera, R., & Lopez-Marín, J. (2022). The use of fuzzy decoupled net present value in pepper production. In M. del P. Rodríguez García, K. A. Cortez Alejandro, J. M. Merigó, A. Terceño-Gómez, M. T. Sorrosal Forradellas, & J. Kacprzyk (Eds.), Lecture notes in networks and systems: Vol. 384 LNNS (pp. 36–46). Springer International Publishing. doi: 10.1007/978-3-030-94485-8_3.Search in Google Scholar

Bugrov, O., & Bugrova, O. (2020). Control process development on the ground of project value dynamics laws. Technology Audit and Production Reserves, 2(4(52)), 11–19. doi: 10.15587/2706-5448.2020.200995.Search in Google Scholar

Chen, Z., Wang, F., Wang, T., He, R., Hu, J., Li, L., Luo, Y., Qin, Y., & Wang, D. (2024). A real options approach to renewable energy module end-of-life decisions under multiple uncertainties: Application to PV and wind in China. Renewable Energy, 226, 120389. doi: 10.1016/j.renene.2024.120389.Search in Google Scholar

Chi, T., & Huang, Y. (2023). The application of real option approach in international business research. In Oxford research encyclopedia of business and management. Oxford University Press. doi: 10.1093/acrefore/9780190224851.013.337.Search in Google Scholar

Chrysafis, K. A., & Papadopoulos, B. K. (2021). Decision making for project appraisal in uncertain environments: A fuzzy-possibilistic approach of the expanded NPV method. Symmetry, 13(1), 1–24. doi: 10.3390/sym13010027.Search in Google Scholar

Cordi, J. A., Rossit, D. A., Ajis, M., & Biondo, L. (2020). Towards the assessment of the efficiency and sustainability of energy-based Investment projects. 2020 International Conference on Decision Aid Sciences and Application (DASA) (pp. 464–468). doi: 10.1109/DASA51403.2020.9317155.Search in Google Scholar

Deiva Ganesh, A., & Kalpana, P. (2023). Factors influencing proactiveness in supply chain risk identification: A fuzzy-set qualitative comparative analysis. International Journal of Disaster Risk Reduction, 88, 1–12. doi: 10.1016/j.ijdrr.2023.103614.Search in Google Scholar

Delaney, L. (2021). A model of investment under uncertainty with time to build, market incompleteness and risk aversion. European Journal of Operational Research, 293(3), 1155–1167. doi: 10.1016/j.ejor.2020.12.052.Search in Google Scholar

Delbari, S. A., Davoodi, A., & Firozeh, N. (2022). Identifying and prioritizing international markets entry strategies in plastics industry using analytic hierarchy process. Journal of Decisions and Operations Research, 7(4), 550–568. doi: 10.22105/dmor.2021.270706.1309.Search in Google Scholar

Dobrowolski, Z., & Drozdowski, G. (2022). Does the net present value as a financial metric fit investment in green energy security? Energies, 15(1), 1–16. doi: 10.3390/en15010353.Search in Google Scholar

Dusseault, B., & Pasquier, P. (2021). Usage of the net present value-at-risk to design ground-coupled heat pump systems under uncertain scenarios. Renewable Energy, 173, 953–971. doi: 10.1016/j.renene.2021.03.065.Search in Google Scholar

Edalatpanah, S. A. (2022). Using hesitant fuzzy sets to solve the problem of choosing a strategy in uncertain conditions. Journal of Decisions and Operations Research, 7(2), 373–382. doi: 10.22105/dmor.2022.348658.1626.Search in Google Scholar

El-Morsy, S. (2023). Stock portfolio optimization using pythagorean fuzzy numbers. Journal of Operational and Strategic Analytics, 1(1), 8–13. doi: 10.56578/josa010102.Search in Google Scholar

Esmaeil Darjani, N., Assadzadeh, A., & Barghi Oskoei, M. M. (2023). Investigating behavioral economics in tax evasion decision making phenomenon: A tax crime scenario approach. Journal of Decisions and Operations Research, 8(3), 654–670. doi: 10.22105/dmor.2023.345401.1615.Search in Google Scholar

Faghihmaleki, H., Habibpour, F., & Anjam, A. R. (2023). Analyzing and enhancing the resilience of steel moment frame structures against progressive collapse. Journal of Operational and Strategic Analytics, 1(2), 90–105. doi: 10.56578/josa010206.Search in Google Scholar

Fakher, H. A. (2021). The role of environmental sustainability, foreign direct investment and trade openness in economic growth: With emphasis on the causal linkage. Big Data and Computing Visions, 1(2), 57–70. doi: 10.22105/bdcv.2021.142227.Search in Google Scholar

Gaspars-Wieloch, H. (2019). Project net present value estimation under uncertainty. Central European Journal of Operations Research, 27(1), 179–197. doi: 10.1007/s10100-017-0500-0.Search in Google Scholar

Ghahremani-Nahr, J., Nozari, H., & Sadeghi, M. E. (2022). Investment modeling to study the performance of dynamic networks of insurance companies in Iran. Modern Research in Performance Evaluation, 1(2), 67–79. https://www.journal-mrpe.ir/article_136608.html.Search in Google Scholar

Guceri, I., & Albinowski, M. (2021). Investment responses to tax policy under uncertainty. Journal of Financial Economics, 141(3), 1147–1170. doi: 10.1016/j.jfineco.2021.04.032.Search in Google Scholar

Guiso, L., Sapienza, P., & Zingales, L. (2018). Time varying risk aversion. Journal of Financial Economics, 128(3), 403–421. doi: 10.1016/j.jfineco.2018.02.007.Search in Google Scholar

Hamidavi Nasab, Y., Amiri, M., Keyghobadi, A., Fathi Hafshejani, K., & Zandhessami, H. (2023). Identifying effective factors of organizational resilience: A meta-synthesis study. International Journal of Research in Industrial Engineering, 12(2), 177–196. doi: 10.22105/riej.2023.375356.1352.Search in Google Scholar

Hanafizadeh, P., & Latif, V. (2011). Robust net present value. Mathematical and Computer Modelling, 54(1–2), 233–242. doi: 10.1016/j.mcm.2011.02.005.Search in Google Scholar

Hosseini, S. S., Mafee, H., & Fakhrhosseini, S. F. (2023). Prioritizing available Islamic finance ways, policies and strategies in Iranian commercial banks (case study of Ayandeh Bank). Innovation Management and Operational Strategies, 4(1), 38–62. doi: 10.22105/imos.2022.349478.1242.Search in Google Scholar

Imeni, M., & Edalatpanah, S. A. (2023). Resilience: Business sustainability based on risk management (pp. 199–213). Singapore: Springer. doi: 10.1007/978-981-19-9909-3_9.Search in Google Scholar

Ismail, J. N., Rodzi, Z., Hashim, H., Sulaiman, N. H., Al-Sharqi, F., Al-Quran, A., & Ahmad, A. G. (2023). Enhancing decision accuracy in dematel using bonferroni mean aggregation under pythagorean neutrosophic environment. Journal of Fuzzy Extension and Applications, 4(4), 281–298. doi: 10.22105/jfea.2023.422582.1318.Search in Google Scholar

Jing, D., Imeni, M., Edalatpanah, S. A., Alburaikan, A., & Khalifa, H. A. (2023). Optimal selection of stock portfolios using multi-criteria decision-making methods. Mathematics, 11(2), 1–21. doi: 10.3390/math11020415.Search in Google Scholar

Joorbonyan, Z., Sorourkhah, A., & Edalatpanah, S. A. (2024). Identifying and prioritizing appropriate strategies for customer loyalty in a mass environment (Case Study: Clothing House). Journal of Decisions and Operations Research, 9(1), 98–119. doi: 10.22105/dmor.2024.420185.1800.Search in Google Scholar

Kamel, M., Khallaf, R., & Nosaier, I. (2022). Net present value-time curve behaviour of public private partnership projects. International Journal of Construction Management, 23, 1–8. doi: 10.1080/15623599.2022.2025742.Search in Google Scholar

Kasprowicz, T., Starczyk-Kołbyk, A., & Wójcik, R. R. (2023). The randomized method of estimating the net present value of construction projects efficiency. International Journal of Construction Management, 23(12), 2126–2133. doi: 10.1080/15623599.2022.2045426.Search in Google Scholar

Kaviani, M., Kaviani, K., & Kaviani, M. (2023). Working capital management and profitability of banks: Evidence from the Iranian Capital Market. Transactions on Quantitative Finance and Beyond, 1(1), 29–34. https://journal-tqfb.com/journal/article/view/18.Search in Google Scholar

Kim, H., Park, S., Choi, S., & Kim, T. (2024). Ship investment valuation using real option analysis (ROA). Journal of Coastal Research, 116(sp1), 423–427. doi: 10.2112/JCR-SI116-086.1.Search in Google Scholar

Lavrynenko, S., Kondratenko, G., Sidenko, I., & Kondratenko, Y. (2020). Fuzzy logic approach for evaluating the effectiveness of investment projects. International Scientific and Technical Conference on Computer Sciences and Information Technologies, 2, 297–300. doi: 10.1109/CSIT49958.2020.9321880.Search in Google Scholar

Li, X., Zhang, Y., Sorourkhah, A., & Edalatpanah, S. A. (2023). Introducing antifragility analysis algorithm for assessing digitalization strategies of the agricultural economy in the small farming section. Journal of the Knowledge Economy, 14, 1–25. doi: 10.1007/s13132-023-01558-5.Search in Google Scholar

Li, Z., Yu, P., Xian, Y., & Fan, J. L. (2024). Investment benefit analysis of coal-to-hydrogen coupled CCS technology in China based on real option approach. Energy, 294, 130293. doi: 10.1016/j.energy.2024.130293.Search in Google Scholar

Loucks, D. P. (2022). Models for managing money (pp. 51–63). Cham: Springer. doi: 10.1007/978-3-030-93986-1_5.Search in Google Scholar

Ma, X., Li, J., Zhao, K., Wu, T., & Zhang, P. (2022). Simulation of spatial service range and value of carbon sink based on intelligent urban ecosystem management system and net present value models – An example from the qinling mountains. Forests, 13(3), 407. doi: 10.3390/f13030407.Search in Google Scholar

Martínez-Ruiz, Y., Manotas-Duque, D. F., & Ramírez-Malule, H. (2021). Evaluation of investment projects in photovoltaic solar energy using the dnpv methodology. International Journal of Energy Economics and Policy, 11(1), 180–185. doi: 10.32479/ijeep.10577.Search in Google Scholar

Mehrabi, M., Sorourkhah, A., & Edalatpanah, S. A. (2023). Decision-making regarding the granting of facilities to sepah bank loan applicants based on credit risk factors considering hesitant fuzzy sets. Financial and Banking Strategic Studies, 1(3), 153–166. https://www.journal-fbs.com/article_181500.html.Search in Google Scholar

Mehregan, M., Jafari, S., Azara, A., & Zahedi, S. (2022). Application of the methodological approach to strategic selection and robust analysis, case study: Deciding on the promotion of product sales. Innovation Management and Operational Strategies, 3(2), 113–129. doi: 10.22105/imos.2022.309117.1174.Search in Google Scholar

Mohammad Ganji Nik, M., Golarzi, G., Shafiei Nikabadi, M., & Fadaiei Eslam, M. (2023). Futures studies of factors affecting stock price fluctuations using scenario planning approach. Journal of Applied Research on Industrial Engineering, 10(4), 584–598. doi: 10.22105/jarie.2023.370729.1514.Search in Google Scholar

Mongkoldhumrongkul, K. (2023). Techno-economic analysis of photovoltaic rooftop system on car parking area in Rayong, Thailand. Energy Reports, 9, 202–212. doi: 10.1016/j.egyr.2022.10.421.Search in Google Scholar

Nik Ab Rahim, N. N. R., Othman, J., Hanim Mohd Salleh, N., & Chamhuri, N. (2021). A non-market valuation approach to environmental cost-benefit analysis for sanitary landfill project appraisal. Sustainability (Switzerland), 13(14), 7718. doi: 10.3390/su13147718.Search in Google Scholar

Nozarpour, Y., Davoodi, S. M. R., & Fadaee, M. (2023). Optimal multi-period portfolio selection with different investment horizons using uncertainty theory. Journal of Decisions and Operations Research, 8(1), 256–268. doi: 10.22105/dmor.2022.322209.1547.Search in Google Scholar

Ogolo, O., Iyalla, E., Tahir, S. M., Ileogbunam, E., Egede, F., & Obe, A. (2023, July 30). Modified straight-line depreciation model for upstream petroleum investment. In SPE Nigeria Annual International Conference and Exhibition. doi: 10.2118/217219-MS.Search in Google Scholar

Padiyar, S. V. S., Chandra Kuraie, V., Makholia, D., Singh, S. R., Singh, V., & Joshi, N. (2024). An imperfect production inventory model for instantaneous deteriorating items with preservation investment under inflation on time value of money. Contemporary Mathematics, 5, 1422–1446. doi: 10.37256/cm.5220243274.Search in Google Scholar

Patil, P. G., Elluru, V., & Shivashankar, S. (2023). A new approach to MCDM problems by fuzzy binary soft sets. Journal of Fuzzy Extension and Applications, 4, 207–216. doi: 10.22105/jfea.2023.390059.1257.Search in Google Scholar

Pérez-Vas, R., Puime Guillén, F., & Enríquez-Díaz, J. (2021). Valuation of a company producing and trading seaweed for human consumption: Classical methods vs. real options. International Journal of Environmental Research and Public Health, 18(10), 5262. doi: 10.3390/ijerph18105262.Search in Google Scholar

Sakai, Y. (2019). JM Keynes on probability versus FH Knight on uncertainty: Reflections on the miracle year of 1921. In Y. Sakai (Ed.), JM Keynes versus FH Knight: Risk, probability, and uncertainty (pp. 39–60). Springer.10.1007/978-981-13-8000-6_3Search in Google Scholar

Sanam, Y., & Sartien, M. (2022). Feasibility analysis of investment in Pt. Sahabat Kasih Nusantara at South central timor regency. Proceedings of the International Conference on Applied Science and Technology on Social Science 2021 (ICAST-SS 2021) (Vol. 647, pp. 398–400). doi: 10.2991/assehr.k.220301.065.Search in Google Scholar

Scandizzo, P. L., & Knudsen, O. K. (2024). The new normalcy and the pandemic threat: A real option approach. Journal of Risk and Financial Management, 17(2), 72. doi: 10.3390/jrfm17020072.Search in Google Scholar

Seifollahi, N. (2023). Designing a national model for evaluating and financing industrial investment projects in Iranian towns and industrial areas. Innovation Management and Operational Strategies, 4(1), 82–99. doi: 10.22105/imos.2023.354103.1247.Search in Google Scholar

Setiadi, D., Anwar, S., & Surianti, S. (2020). Investments evaluation model case in Indonesian hospital. In 1st International Conference on Accounting, Management and Entrepreneurship (pp. 141–144). doi: 10.2991/aebmr.k.200305.035.Search in Google Scholar

Seyed Nezhad Fahim, S. R., & Gholami Gelsefid, F. (2023). The impact of internal and external driving forces and strategic decisions on supply chain risk management (case study: Automotive industry). Journal of Applied Research on Industrial Engineering, 10(3), 472–491. doi: 10.22105/jarie.2022.342727.1470.Search in Google Scholar

Shahbeyk, S., & Banihashemi, S. (2023). Loan portfolio performance evaluation by using stochastic recovery rate. Journal of Applied Research on Industrial Engineering, 11, 116–124. doi: 10.22105/jarie.2023.346023.1478.Search in Google Scholar

Sharma, V., Gidwani, B. D., Sharma, V., & Meena, M. L. (2019). Implementation model for cellular manufacturing system using AHP and ANP approach. Benchmarking: An International Journal, 26(5), 1605–1630. doi: 10.1108/BIJ-08-2018-0253.Search in Google Scholar

Shemshad, A., & Karim, R. G. (2023). The effect of managerial ability on the timeliness of financial reporting: The role of audit firm and company size. Journal of Operational and Strategic Analytics, 1(1), 34–41. doi: 10.56578/josa010105.Search in Google Scholar

Shou, T. (2022). A literature review on the net present value (NPV) valuation method. Proceedings of the 2022 2nd International Conference on Enterprise Management and Economic Development (ICEMED 2022) (Vol. 656, pp. 826–830). doi: 10.2991/aebmr.k.220603.135.Search in Google Scholar

Simons, J., & Coate, M. B. (2022). A net present value approach to merger analysis. SSRN Electronic Journal. doi: 10.2139/ssrn.4104499.Search in Google Scholar

Sorourkhah, A. (2024). A scenario-based alternative to conventional tools for choosing the strategy in turbulent environments. International Journal of Research in Industrial Engineering, 13(2), 224–236.Search in Google Scholar

Tsvetkov, T. G., & Bozmarova, A. R. (2023). Investment decisions reasoning to increase the organization’s cyber security using simulation models. 2023 International Scientific Conference on Computer Science (COMSCI) (pp. 1–6). doi: 10.1109/COMSCI59259.2023.10315820.Search in Google Scholar

Vijayakumar, S. R., Suresh, P., Sasikumar, K., Pasupathi, K., Yuvaraj, T., & Velmurugan, D. (2022). Evaluation and selection of projects using hybrid MCDM technique under fuzzy environment based on financial factors. Materials Today: Proceedings, 60, 1347–1352. doi: 10.1016/j.matpr.2021.10.138.Search in Google Scholar

Wang, Y. (2021). The development and usage of NPV and IRR and their comparison. In 2021 3rd International Conference on Economic Management and Cultural Industry (ICEMCI 2021). doi: 10.2991/assehr.k.211209.334.Search in Google Scholar

Xu, W., Edalatpanah, S. A., & Sorourkhah, A. (2023). Solving the problem of reducing the audiences’ favor toward an educational institution by using a combination of hard and soft operations research approaches. Mathematics, 11(18), 3815. doi: 10.3390/math11183815.Search in Google Scholar

Yan, R., & Zhang, Y. (2022). The introduction of NPV and IRR. In 2022 7th International Conference on Financial Innovation and Economic Development (ICFIED 2022). doi: 10.2991/aebmr.k.220307.241.Search in Google Scholar

© 2024 the author(s), published by De Gruyter

This work is licensed under the Creative Commons Attribution 4.0 International License.

Articles in the same Issue

- Regular Articles

- Political Turnover and Public Health Provision in Brazilian Municipalities

- Examining the Effects of Trade Liberalisation Using a Gravity Model Approach

- Operating Efficiency in the Capital-Intensive Semiconductor Industry: A Nonparametric Frontier Approach

- Does Health Insurance Boost Subjective Well-being? Examining the Link in China through a National Survey

- An Intelligent Approach for Predicting Stock Market Movements in Emerging Markets Using Optimized Technical Indicators and Neural Networks

- Analysis of the Effect of Digital Financial Inclusion in Promoting Inclusive Growth: Mechanism and Statistical Verification

- Effective Tax Rates and Firm Size under Turnover Tax: Evidence from a Natural Experiment on SMEs

- Re-investigating the Impact of Economic Growth, Energy Consumption, Financial Development, Institutional Quality, and Globalization on Environmental Degradation in OECD Countries

- A Compliance Return Method to Evaluate Different Approaches to Implementing Regulations: The Example of Food Hygiene Standards

- Panel Technical Efficiency of Korean Companies in the Energy Sector based on Digital Capabilities

- Time-varying Investment Dynamics in the USA

- Preferences, Institutions, and Policy Makers: The Case of the New Institutionalization of Science, Technology, and Innovation Governance in Colombia

- The Impact of Geographic Factors on Credit Risk: A Study of Chinese Commercial Banks

- The Heterogeneous Effect and Transmission Paths of Air Pollution on Housing Prices: Evidence from 30 Large- and Medium-Sized Cities in China

- Analysis of Demographic Variables Affecting Digital Citizenship in Turkey

- Green Finance, Environmental Regulations, and Green Technologies in China: Implications for Achieving Green Economic Recovery

- Coupled and Coordinated Development of Economic Growth and Green Sustainability in a Manufacturing Enterprise under the Context of Dual Carbon Goals: Carbon Peaking and Carbon Neutrality

- Revealing the New Nexus in Urban Unemployment Dynamics: The Relationship between Institutional Variables and Long-Term Unemployment in Colombia

- The Roles of the Terms of Trade and the Real Exchange Rate in the Current Account Balance

- Cleaner Production: Analysis of the Role and Path of Green Finance in Controlling Agricultural Nonpoint Source Pollution

- The Research on the Impact of Regional Trade Network Relationships on Value Chain Resilience in China’s Service Industry

- Social Support and Suicidal Ideation among Children of Cross-Border Married Couples

- Asymmetrical Monetary Relations and Involuntary Unemployment in a General Equilibrium Model

- Job Crafting among Airport Security: The Role of Organizational Support, Work Engagement and Social Courage

- Does the Adjustment of Industrial Structure Restrain the Income Gap between Urban and Rural Areas

- Optimizing Emergency Logistics Centre Locations: A Multi-Objective Robust Model

- Geopolitical Risks and Stock Market Volatility in the SAARC Region

- Trade Globalization, Overseas Investment, and Tax Revenue Growth in Sub-Saharan Africa

- Can Government Expenditure Improve the Efficiency of Institutional Elderly-Care Service? – Take Wuhan as an Example

- Media Tone and Earnings Management before the Earnings Announcement: Evidence from China

- Review Articles

- Economic Growth in the Age of Ubiquitous Threats: How Global Risks are Reshaping Growth Theory

- Efficiency Measurement in Healthcare: The Foundations, Variables, and Models – A Narrative Literature Review

- Rethinking the Theoretical Foundation of Economics I: The Multilevel Paradigm

- Financial Literacy as Part of Empowerment Education for Later Life: A Spectrum of Perspectives, Challenges and Implications for Individuals, Educators and Policymakers in the Modern Digital Economy

- Special Issue: Economic Implications of Management and Entrepreneurship - Part II

- Ethnic Entrepreneurship: A Qualitative Study on Entrepreneurial Tendency of Meskhetian Turks Living in the USA in the Context of the Interactive Model

- Bridging Brand Parity with Insights Regarding Consumer Behavior

- The Effect of Green Human Resources Management Practices on Corporate Sustainability from the Perspective of Employees

- Special Issue: Shapes of Performance Evaluation in Economics and Management Decision - Part II

- High-Quality Development of Sports Competition Performance Industry in Chengdu-Chongqing Region Based on Performance Evaluation Theory

- Analysis of Multi-Factor Dynamic Coupling and Government Intervention Level for Urbanization in China: Evidence from the Yangtze River Economic Belt