Loan Loss Provisions and Bank Value in the United States: A Moderation Analysis of Economic Policy Uncertainty

-

and

and

Abstract

Macroeconomic conditions are often neglected in bank valuation models. We find that economic policy uncertainty significantly reduces bank value by using a panel data regression model with data on the US banks. Economic policy uncertainty also affects bank value through its moderating role in the relationship between loan loss provisions and bank value. The findings remain robust across various endogeneity and robustness tests. This moderating role is particularly significant for small and medium-sized banks, banks with higher levels of non-performing loans, and during the financial crisis period. This study contributes to the understanding of a macroeconomic determinant shaping bank valuation models. The moderation analysis offers new insights into economic policy uncertainty that appears to mitigate the impact of loan loss provisions on bank value by advocating stronger risk governance practices when economic conditions are challenging. Policymakers should address the uncertainties stemming from economic policies to bolster the financial stability of banks.

1 Introduction

Ambiguity in economic policy, such as monetary policy and fiscal policy, might occur due to economic recession or political polarization (Azzimonti, 2018; Kaviani et al., 2020; McCarty et al., 1997). Increasing political polarization between two major parties in the United States in the past has led to a high level of uncertainty in economic policies, particularly in government spending (Ng et al., 2020). Economic policy uncertainty has received considerable attention in research, particularly in the banking sector (Ashraf & Shen, 2019; Bordo et al., 2016; Danisman et al., 2021; Hu & Gong, 2019; Karadima & Louri, 2021; Ng et al., 2020; Nguyen et al., 2020; Phan et al., 2021; Tran et al., 2021). It was argued that economic policy uncertainty impacts loan loss provisions (Danisman et al., 2021; Ng et al., 2020), loan rates (Ashraf & Shen, 2019), the financial stability of banks (Phan et al., 2021), loan growth (Hu & Gong, 2019; Nguyen et al., 2020), and various bank businesses (Tran et al., 2021). All these impacts lead to negative consequences on bank earnings and value. However, the impact of economic policy uncertainty on bank value remains unexplored. The impact of economic policy uncertainty on bank value should be critically addressed to avoid valuation bias in financial analysis.

Past researchers found that banks tend to raise loan loss provisions when there is much uncertainty about economic policy (Danisman et al., 2021; Ng et al., 2020; Tran et al., 2021). Rising loan loss provisions may impact bank value. Even though the research study on loan loss provisions and bank value is scarce, some research provides the support to justify their potential negative relationship (Elnahass et al., 2014; Laeven & Majnoni, 2003; Lai, 2024; Ng et al., 2020). A negative signal would be sent to the financial market if banks decide to increase loan loss provisions, as banks might experience higher financial risks and challenges in the future that affect their profitability. With this, the market tends to lower the expected value of the banks. Consequently, high loan loss provisions will negatively affect the stock price of the banks and bank value. Ashraf and Shen (2019) warned that high economic policy uncertainty will increase the default risk on bank loans. Borrowers are likely to default on their loans and the value of the collateral underlying the loans is greatly reduced. This drives a bigger drop in bank value because banks are likely to increase loan loss provisions to reduce the impact of economic policy uncertainty on loan losses. On the other hand, economic policy uncertainty might weaken the negative relationship between loan loss provisions and bank value. Banks facing heightened levels of economic policy uncertainty might undertake more strategic and proactive risk governance actions to counteract the negative influence of higher loan loss provisions on bank value. Banks could enhance their balance sheet and their value by strategically managing their loan loss provisions. Therefore, the impact of loan loss provisions as risk signals on bank value could be weakened with banks’ strategic risk management response to economic policy uncertainty. The complexity of this relationship should be studied to reveal the moderating impact of economic policy uncertainty. However, there is an absence of studies investigating the potential moderating role of economic policy uncertainty on the relationship between loan loss provisions and bank value. The lack of attention to this potential moderating impact leaves a gap in knowledge concerning the influence of loan loss provisions on bank value from a macroeconomic perspective.

Although these considerations apply to the banking sector in general, the US banking sector, the focus of this study, has a special context. There is a high rise in uncertainty in economic policies in the United States due to the significant changing trend of regulation, taxes, government spending, and political polarization (Baker et al., 2014). As the largest economy in the world, the United States exerts significant influence on the financial markets globally. Policy changes and economic shocks in the US often propagate through interconnected financial markets, affecting international banking operations and investor sentiment. A clear example is the 2008 Global Financial Crisis triggered by subprime mortgage lending that caused severe repercussions to global financial markets. The US has a well‐established and sophisticated regulatory framework and a diversity of banking institutions that give rise to wide variations in bank values. It has the most stringent and extensive financial regulation for monitoring banks (Labonte, 2017), influencing banks’ accrual decisions, particularly loan loss provisions, and there is a strong positive correlation between loan loss provisions and the uncertainty of US economic policy (Danisman et al., 2021). The US banking sector relies more heavily on capital markets for financing than that of most other countries (Adrian et al., 2024; Beck et al., 2000). This feature increases exposure to market risks and results in a greater interconnectedness between economic policy uncertainty and financial institutions. Consequently, examining US banks offers a benchmark reference that can inform policy decisions and risk management strategies both within the United States and internationally.

The key objectives of this study are to study the impact of economic policy uncertainty on bank value and its moderation effect on the association between loan loss provisions and bank value. We sampled 606 publicly listed banks in the United States and employed panel data regression analysis. The findings show that economic policy uncertainty significantly impacts bank value and weakens the negative relationship between loan loss provisions and bank value. Further analyses indicate that the moderation effect is more pronounced for small- and medium-sized banks, banks with high non-performing loans, and in periods of financial crisis. With these significant findings, this article brings key contributions with a new bank valuation perspective. While prior research focuses on the direct effects of economic policy uncertainty on a bank’s stock performance or risk exposure, there has been limited attention on how it may affect the linkage between a bank’s loan loss provisions and its value. As is discussed below, challenging economic conditions elicit strategic responses from the banking sector. The market perception formed from the signals agents received from these responses will then affect the linkage between loan loss provisions and bank value. This study offers a more nuanced understanding of the results of these effects and provides a novel lens for policymakers, investors, and bank managers seeking to navigate periods of heightened economic uncertainty.

The next section reviews the literature to develop two hypotheses for this study. The measurement of the variables and the specification of the baseline model are explained in Section 3. Section 4 describes the data and their descriptive statistics. The results and discussion are reported in Section 5, followed by the endogeneity checks. We show some additional analyses of the moderating impact of economic policy uncertainty in different circumstances in Section 5.2. The last section concludes the study.

2 Development of Hypotheses

In this section, we hypothesize the connection between economic policy uncertainty and bank value using evidence from the literature. Also, we provide the basis for the moderating role of economic policy uncertainty in the connection between loan loss provisions and bank value.

2.1 Economic Policy Uncertainty and Bank Value

A growing body of past literature has investigated the impact of economic policy uncertainty on banks, examining issues such as bank stability, liquidity management, stock market valuations, and lending decisions (Arouri et al., 2016; Berger et al., 2022; Danisman & Tarazi, 2024; Nguyen et al., 2020; Tran, 2020). Danisman and Tarazi (2024) demonstrated that economic policy uncertainty can affect bank stability, and highlighted the importance of capital adequacy and liquidity in mitigating uncertainty‐induced risks. Berger et al. (2022) found that heightened economic policy uncertainty prompts banks to hoard liquidity. This action would likely constrain lending activities and harm the profitability of banks. Also, prior research has shown that economic policy uncertainty negatively affects bank profitability (Bordo et al., 2016; Tran, 2020) and suppresses stock valuations in the financial sector (Arouri et al., 2016). Additionally, increased economic policy uncertainty can reduce the credit growth of banks as institutions adopt a more cautious credit supply to shield themselves from economic uncertainty (Nguyen et al., 2020).

To comprehensively understand the impact of economic policy uncertainty on banks, we examine various dimensions of uncertainty as detailed in the framework developed by Baker et al. (2016). They categorized 11 areas of concern in economic policies, which are fiscal policy, monetary policy, health care, taxes, national security, government spending, financial regulation, entitlement programs, regulation, trade policy, and sovereign debt and currency crises. Among these areas, the primary uncertainty often stems from the monetary policy (Creal & Wu, 2017; Kurov & Stan, 2018). Uncertainty in monetary policy could seriously affect the capital structure of firms (Jiang et al., 2022). Firms tend to reduce capital expenditure and lending due to uncertain monetary policy, particularly during financial crises (Kahle & Stulz, 2013). The loan growth and mortgage business of banks would be negatively affected, harming bank earnings and value, as banks often reduce the approvals of large mortgage loans when economic policy is uncertain (Kara & Yook, 2023).

An uncertain tax policy may cause firms to have difficulties deciding their optimal amount of debt, as it will increase the chance of default and the financial risk (Tosun & Yildiz, 2020). Firms could not estimate their cash flow in the future if tax policy remains unclear. The trade-off theory of Fama and French (2002) on capital structure implies that firms could take on a higher level of debt under a higher interest tax shield scheme. As a result, firms might adjust their leverage target by taking on more debt, subject to the tax policy. However, the uncertainty of tax policy limits firms’ risk-taking behavior, causing them to take on lesser loan debt, resulting in lower loan growth for banks. Guceri and Albinowski (2021) compared two groups of firms in situations of low and high uncertainty in tax policy and found that investment behavior is slower when levels of uncertainty in tax policy are high. Bloom et al. (2007) provided consistent results that firms evaluate their investment decisions with consideration of tax conditions. Banks would experience lower demand for loans as most firms would choose to control their optimal debt level and investment decisions due to uncertain tax policy, and this hurts bank earnings.

Fiscal policy stability is an essential factor in mitigating innovation investments and operational risks. Wen et al. (2022) highlighted that a fall in government spending and the uncertainty in fiscal policy would negatively influence firms’ investment in innovation, particularly in the new energy industry. A high level of fiscal policy uncertainty increases operational risks and dampens investment in innovation. Banks would have fewer businesses to lend to and approvals to provide to firms if fiscal policy were uncertain. Fernández-Villaverde et al. (2015) demonstrated that the volatility in government spending has a significant negative impact on firms’ investment, as the government budget contains key subsidies for business investment. A contraction in economic activities due to uncertainty in fiscal policy and government spending hurts the earnings and value of banks.

Regulation, particularly financial regulation policy uncertainty, may also add to banks’ regulatory burden. The Patriot Act of 2001 and the Dodd-Frank Act in the US are examples of major regulations that have had a negative impact on small banks in the US, as the regulatory changes cause high compliance costs to fulfil the heavy regulatory legislation (Cyree, 2016). According to Dolar and Shughart (2007), the Patriot Act’s implementation increased compliance costs by 44.7% on average. The act aims to reduce the likelihood of money laundering, thus imposing more compliance obligations and costs on banks. Killins et al. (2020) complemented the findings of Cyree (2016) that the financial regulation policy uncertainty has affected bank profitability in terms of ROA and ROE. Furthermore, as stated in Basel III in 2013, banks are requested to strengthen their capital requirements by 2022 in order to mitigate the potential capital adequacy risk. Banks must ensure their total Tier I and Tier II capital achieves at least 10.5% of risk-weighted assets. Thus, banks have to retain more earnings to meet the required capital under the Basel III rules. Therefore, an uncertain future financial regulation policy might impose more financial constraints and incur more compliance costs for banks.

Trade policy uncertainty has gained prominence as a result of the US-China trade war, the US withdrawal from the Trans-Pacific Partnership (TPP), and increased tariffs on aluminum and steel imports into the United States (Baker et al., 2019). The US actual tariff on China’s exports has increased from 3.1% in January 2018 to 19.3% in June 2022, whereas China’s tariff on US exports has also risen from 8% in January 2018 to 21.2% in June 2022 (Bown, 2022). Handley and Limão (2022) concluded that the growing trade policy uncertainty has greatly influenced the earnings of firms in different industries. Caldara et al. (2020) and Handley (2014) provided evidence that trade policy uncertainty caused negative impacts on company investment decisions due to unclear tariff rates for commercial exports. The uncertainty also delays exporters’ access to new potential markets and reduces their responsiveness to tariff reductions (Handley, 2014). Additionally, industries with greater exposure to trade policy uncertainty had a greater decline in stock price when the uncertainty started, as well as more erratic returns around important policy dates (Bianconi et al., 2021). Due to the reduction in investment and export activities, the large earnings drop, and the decline in stock prices for affected firms, it is reasonable to forecast that a lot of affected firms would experience financial difficulties, causing lower financial stability and loan solvency. Banks would be equally affected when trade policy uncertainty is high in terms of loan growth and potential higher loan losses or non-performing loans.

Past studies explained the mechanism of the impact of currency crises and sovereign debt uncertainty on banks (Bordo & Meissner, 2016; Calvo et al., 2003; Glick & Hutchison, 2013). The currency crisis would cause a banking crisis if banks retained substantial amounts of unhedged foreign liabilities (Glick & Hutchison, 2013). The foreign liabilities would immediately become a heavy financial burden after a serious currency shock. Calvo et al. (2003) found that the financial crisis was associated with the currency crisis in Argentina in 2001. When the financial stability of the Argentine government became weaker, international investors chose to withdraw their capital from Argentina, resulting in a bank run that turned into a currency crisis. Consequently, the Argentine government failed to pay the growing sovereign debt. Bordo and Meissner (2016) highlighted that if a currency crisis occurs, the government will probably increase taxes in its own currency and charge more tax on the firms that have higher export earnings in foreign currency to cover its sovereign debt. In turn, it hurts the economy and raises the possibility of a sovereign default. The balance sheet of the banks would become impaired if they provided large loans during any currency crisis.

In summary, we present evidence from the literature that uncertainty in various domains of economic policies could affect the earnings and loan growth of banks. Thus, economic policy uncertainty may impact bank value as hypothesized below.

H1: Bank value has an inverse relationship with economic policy uncertainty.

2.2 Moderating Impact of Economic Policy Uncertainty

This section explains the moderating role of economic policy uncertainty in the relationship between loan loss provisions and bank value that is relatively unexplored in the literature. First, we discuss the connection between loan loss provisions and bank value that is also under-researched. Loan loss provisions are the largest accrual in banks compared to bonuses and salaries. Walter (1991) is the earliest researcher studying the influence of loan loss provisions on banks. He reported that large loan losses had been written off by the US banks in 1990, resulting in huge fluctuations in bank earnings. At that time, the Federal Reserve began to enforce and implement the practice of loan loss provisions, aimed at covering potential loan losses. If a loan has been past due for more than 180 days, banks may choose to write it off, and the loss could be covered by loan loss reserves. Loan loss provisions are reported quarterly in the income statement and are added to or subtracted from loan loss reserves in the balance sheet. Recent research found that the key objective of allocating loan loss provisions quarterly is to smooth the earnings of banks to cover the potential losses in loans and investments (Balla et al., 2012; Wall & Koch, 2000). This will enhance the financial stability of banks during economic recessions and reduce the procyclicality of bank earnings. However, discretionary loan loss provisioning would affect bank profitability, as explained by Walter (1991) and Laeven and Majnoni (2003). They conducted cross-country empirical research and discovered that loan loss provisions had a substantial impact on bank profit before taxes. Their results demonstrated a negative correlation between loan loss provisions and bank profitability, suggesting that banks would retain more funds as loan loss provisions in the midst of a recession. In addition, they stressed that most banks were too slow to establish appropriate loan loss reserves during economic crises, which exacerbated the negative effects on bank profitability. On the income statement, the amount of loan loss provisions will reduce bank earnings. As a result, the reported earnings of banks would have an impact on their stock prices (Balla et al., 2012; Docking et al., 2000). Financial markets are sensitive and vulnerable to changes in bank earnings, and their reactions will affect the stock prices of the banks negatively. Consequently, banks are valued lower. Therefore, higher loan loss provisioning might lead to a lower bank value.

This negative relationship between loan loss provisions and bank value may be affected by economic policy uncertainty through the following theoretical channels. Drawing on the “Big Bath” accounting theory, managers may capitalize on periods of heightened uncertainty to substantially increase loan loss provisions, effectively blaming economic policy uncertainty for performance setbacks (Danisman et al., 2021; Ng et al., 2020). This tactic can exacerbate the negative association between loan loss provisions and bank value, since suddenly larger provisions send a pessimistic signal to investors about the potential poor asset quality and future prospects. Under such conditions, bank management teams that are less prudent might adopt conservative or opportunistic provisioning decisions, further reinforcing the negative impact on bank value (Ng et al., 2020). Consistent with these findings, Ng et al. (2020) reported that loan loss provisions can rise by approximately 12.07% when the Economic Policy Uncertainty index increases by one standard deviation, suggesting that policy uncertainty can intensify provisioning and amplify negative market reactions. Therefore, the negative relationship between loan loss provisions and bank value may be strengthened when the degree of economic policy uncertainty is high.

On the other hand, economic policy uncertainty may weaken the negative relationship between loan loss provisions and bank value by fostering more prudent risk management. From a precautionary standpoint, banks anticipating volatile policy environments may strategically maintain higher levels of loan loss provisions to safeguard against potential loan defaults (Danisman et al., 2021). This approach can reassure stakeholders that the bank is proactively managing heightened risks, thus mitigating the negative effect of provisions on bank value. Moreover, banks might mitigate the bad news of economic conditions by reducing loan loss provisions during periods when economic policy uncertainty is high (Beatty et al., 2002; Cohen et al., 2014). Investors could interpret these adjustments as cautious optimism, further dampening any negative market response to banks. As a result, reduced loan loss provisions under uncertain conditions may ultimately signal stronger underlying fundamentals of banks, thereby weakening the overall impact of loan loss provisions on bank value.

With the above arguments, a higher level of economic policy uncertainty might strengthen or weaken the relationship between loan loss provisions and bank value. This duality in possible outcomes motivates the present study to explore the moderating effect of economic policy uncertainty on the loan loss provisions–bank value relationship. By doing this, our study extends the literature on prudential bank management and bank valuation on the grounds that higher uncertainty could either exacerbate or buffer the impact of loan loss provisions. This focus enriches our understanding of the connection between macro‐level policy uncertainty and micro‐level provisioning in banking. The proposed hypothesis is:

H2: The relationship between loan loss provisions and bank value is moderated by the level of economic policy uncertainty.

3 Measurement of Variables and Specification of the Baseline Model

This section explains the proxies used to measure bank value and economic policy uncertainty. The specification of the baseline model and the control variables included in the model are described.

3.1 Dependent Variable

We select Tobin’s Q ratio as the proxy to represent bank value, the dependent variable. Tobin’s Q ratio was established by Tobin and Brainard (1976). It is a ratio between the assets of a company’s market value and their replacement cost. The formula for Tobin’s Q ratio (tobinq) is listed as follows:

A company with a ratio of more than 1 is interpreted as overvalued, but it could also signify that the company gained market confidence in its future prospects. Conversely, the market might not have a high level of confidence in the company if the ratio is less than 1. Tobin’s Q ratio was commonly used to value non-bank firms in terms of company performance (Wernerfelt & Montgomery, 1988), company structure and valuation (Cho, 1998; Demsetz & Villalonga, 2001), and mergers and requisitions in the United States (Servaes, 1991). Also, Tobin’s Q ratio is prevalent and influential in its use as a proxy of bank value to study bank governance (Caprio et al., 2007), board size (Adams & Mehran, 2012; Belkhir, 2009), bank performance during financial crises (Huizinga & Laeven, 2012; Jones et al., 2011; Peni & Vähämaa, 2012), bank risk (González, 2005), stock performance (Sawada, 2013), and bank size and valuation (Minton et al., 2017). Previous studies (Bordo et al., 2016; Tran, 2020) have examined how economic policy uncertainty affects a bank’s profitability or stock price. However, the use of Tobin’s Q ratio as a measure of bank value provides a distinct perspective. Tobin’s Q ratio not only reflects market-based valuations but also includes the replacement cost of assets, thus capturing a more comprehensive view of bank performance. It accounts for investor confidence in a bank’s future prospects, which may not be fully reflected in traditional profitability or stock price measures. The use of Tobin’s Q ratio is a valuable addition to the existing literature on bank value.

3.2 Measure of Economic Policy Uncertainty

Baker et al. (2016) developed the Economic Policy Uncertainty (EPU) index, which is the recognized benchmark indicator for measuring the uncertainty of economic policies. They constructed the yearly EPU index for various countries by quantifying three components: the newspaper-based component, Congressional Budget Office reports, and forecasters’ predictions. The newspaper-based component is measured based on the search results from the 10 largest newspapers in the United States, including the Wall Street Journal, the Washington Post, and the New York Times. The US tax provisions that are about to expire are reported by the Congressional Budget Office. The forecasters’ predictions include different forecasts on local and federal expenses and the Consumer Price Index. The insightful perspective on policy uncertainty conveyed by the EPU index enables us to investigate the sensitivity and influence of economic policy uncertainty on bank value and the relationship between loan loss provisions and bank value.

3.3 Specification of the Baseline Model

The baseline model consists of Tobin’s Q ratio as the dependent variable, and the EPU index and loan loss provisions as the key independent variables. Following past studies, other bank-related variables that are highly relevant to bank earnings and value are also included in the model. They are return on assets (Caprio et al., 2007), total assets (Dang et al., 2018; Himmelberg & Hubbard, 2000; Linck et al., 2008), loan-to-deposit ratio (Sloman et al., 2018), net interest income to earning assets ratio (Fang et al., 2014), deposit growth (Damodaran, 2008), loan growth (Bernanke et al., 1996; Niu, 2016), and capital adequacy ratio (Basel Committee on Banking Supervision, 2017). The baseline model (2) below is employed to test H1 and H2:

where

3.4 Further Analyses and Assessing Endogeneity

Equation (2) is estimated using the full sample. The results may vary according to heterogeneity in the banking environment and bank characteristics. We extend the empirical analyses to explore how economic policy uncertainty affects bank value under three distinct conditions: periods of financial crisis, varying levels of bank prudence, and differences in bank size. Equation (2) is estimated for these additional analyses to capture the impact of economic policy uncertainty under different banking environments and bank characteristics.

In all these analyses, shocks that affect bank value could potentially cause changes to economic policy uncertainty. Bias due to the omission of macroeconomic variables related to such shocks from the estimation could also cause a correlation between economic policy uncertainty and the error term of equation (2). These possibilities raise concerns about the endogeneity problem. Three sets of estimations are conducted to examine if the findings remain robust and not affected by endogeneity.

Hailemariam et al. (2019), Kang et al. (2017), and Kang and Ratti (2013) empirically found a significant causal impact of the crude oil price on economic policy uncertainty. From a banking perspective, shifts in energy prices can influence the credit risks faced by banks, especially if their clients rely heavily on energy inputs. Rapid changes in energy costs may harm firms’ profitability and loan repayment capacity. This hurts not only bank profitability but also induces higher economic policy uncertainty as regulators would alter policy to maintain financial stability. Variables representing exogenous energy price shocks are used to model the sources of variation in economic policy uncertainty due to energy price shocks. Equation (2) is then re-estimated with these shocks isolated.

In addition to energy price shocks, political tension, disagreements and conflict in the US might also contribute to economic policy uncertainty. Variables that measure these political dimensions can be used to estimate the exogenous variations in economic policy uncertainty. Using them as instrumental variables, the two-stage least squares (2SLS) is applied to re-estimate equation (2) to address the endogeneity issue. This accounts for the possibility that economic policy uncertainty does not arise solely from within the financial system, but it could be triggered by external events.

The reverse causality between economic policy uncertainty and bank value is an additional endogeneity concern. Financial market shocks related to the banking sector could lead to changes in the financial regulation and monetary policy which are two major domains of the economic policy concerns. The effects of this concern on the results are examined by using the dynamic panel generalized method-of-moments (GMM) method to estimate equation (2) so that reverse causality is taken into consideration.

4 The Data

4.1 Data Collection and Processing

In this study, we apply panel data regression to the time series data of 608 publicly listed banks in the United States extracted from the Thomson Reuters database. The database provides information on 660 publicly listed US banks. The final inclusion of the 608 banks is based on complete information available to compute Tobin’s Q ratio. The loan loss provisions were calculated using the Incurred Loss Model until it was replaced by the Expected Loss Model beginning January 1, 2018 (BIS, 2017; IASB, 2014). The data period 2000–2017 is chosen to isolate the effect of the new model, which may lead to a volatile adjustment of loan loss provisions. All data and regressions are processed using the STATA 16.1 SE software. The upper and lower 1% of data points for all the variables were subjected to winsorization to mitigate the effects of outliers (Ghosh & Vogt, 2012; Kwak & Kim, 2017). Data winsorization is commonly conducted in finance research (Adams et al., 2019).

4.2 Descriptive Statistics

Table 1 presents the summary statistics for all the variables. The statistics of Tobin’s Q ratio indicate that 50% of the data have a higher bank value ranging from 1.021 to 1.783, and another 50% have a lower bank value ranging from 0.802 to 1.021 with a shorter range. In other words, most of the US banks have a relatively high bank value. The average value of the loan loss provision ratio of US banks is 0.565% of total loans. Although the EPU index has the largest standard deviation compared to Tobin’s Q ratio and loan loss provision ratio, the loan loss provision ratio displays the largest dispersion when measured by the coefficient of variation. According to the correlation matrix in Table 2, Tobin’s Q ratio exhibits a negative association with both the EPU index and the loan loss provision ratio, indicating a higher value of either will lead to a lower bank value. However, the EPU index has a positive correlation with the loan loss provision ratio. This result concurs with the finding that higher loan loss provisioning by banks is associated with higher economic policy uncertainty (Ng et al., 2020).

Summary statistics of variables

| Variable | Obs | Mean | Std. dev. | Median | Min | Max |

|---|---|---|---|---|---|---|

| tobinq | 7,594 | 1.031 | 0.073 | 1.021 | 0.802 | 1.783 |

| EPU | 11,552 | 130.573 | 19.058 | 138.523 | 96.553 | 152.671 |

| llpratio | 7,717 | 0.565 | 6.822 | 0.247 | −47.659 | 583.947 |

| roa | 6,874 | 1.052 | 0.958 | 1.11 | −4.46 | 8.11 |

| lntassets | 8,388 | 14.032 | 1.651 | 13.747 | 10.484 | 21.033 |

| loandeposit | 7,737 | 160.673 | 3115.949 | 89.035 | 0.098 | 150266.67 |

| interestincome | 7,975 | 3.752 | 0.97 | 3.65 | 0.64 | 16.04 |

| depositgrowth | 7,724 | 10.348 | 17.769 | 6.422 | −40.162 | 119.062 |

| loangrowth | 6,873 | 10.301 | 15.801 | 6.5 | −14.5 | 91.21 |

| car | 6,474 | 15.538 | 5.463 | 14.12 | 7.98 | 47.01 |

Note: Appendix 1 shows the definitions of the variables. Obs refers to the number of observations.

Matrix of correlations

| Variable | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) |

|---|---|---|---|---|---|---|---|---|---|---|

| (1) tobinq | 1.000 | |||||||||

| (2) EPU | −0.277* | 1.000 | ||||||||

| (3) llpratio | −0.028* | 0.021 | 1.000 | |||||||

| (4) roa | 0.350* | −0.177* | −0.065* | 1.000 | ||||||

| (5) lntassets | 0.140* | 0.223* | 0.036* | 0.151* | 1.000 | |||||

| (6) loandeposit | −0.068* | −0.028* | 0.001 | 0.153* | 0.049* | 1.000 | ||||

| (7) interestincome | 0.137* | −0.132* | −0.006 | 0.311* | −0.079* | −0.026* | 1.000 | |||

| (8) depositgrowth | 0.095* | −0.060* | −0.004 | 0.062* | 0.038* | 0.034* | 0.095* | 1.000 | ||

| (9) loangrowth | 0.152* | −0.135* | −0.016 | 0.088* | −0.012 | 0.029* | 0.104* | 0.881* | 1.000 | |

| (10) car | −0.005 | 0.062* | −0.001 | 0.053* | −0.160* | −0.073* | −0.026* | −0.095* | −0.075* | 1.000 |

Note: Pairwise deletion for the correlation matrix is used. Refer to Appendix 1 for the definitions of the variables. The statistical significance at the 10% level of significance is indicated by *.

5 Results and Discussions

5.1 Estimation Results

The estimation results are reported in Table 3.[1] There is no serious multicollinearity issue in the baseline model (Table 4). All the variance inflation factors (VIFs) are less than the acceptable level of 10 (Alin, 2010; Gujarati et al., 2012), and the average VIF is 2.20. Model (1) in Table 3 shows that there is a significant negative relationship between economic policy uncertainty and bank value. A one-unit increase in the EPU index is associated with a 0.0157-unit decrease in Tobin’s Q ratio. With the addition of the interaction term in Model (2), the results that bank value drops when uncertainty in economic policies is higher remain the same. These results support H1 that bank value is negatively associated with increased economic policy uncertainty. This finding is consistent with the literature that provides support for the negative effect of economic policy uncertainty on bank value. Pastor and Veronesi (2012) concluded that policy uncertainty heightens risk aversion among investors, thereby reducing stock prices in the banking sector. Similarly, Bernanke (1983) noted that uncertainty has the potential to discourage investment and economic activity, particularly for financial institutions that depend on a stable economic environment. Tran (2020) found that higher economic policy uncertainty levels reduce bank lending, decrease bank profitability, and lower bank stock returns.

Estimation results: Moderation by economic policy uncertainty

| Variable | (1) | (2) |

|---|---|---|

| Baseline | Moderation by economic policy uncertainty | |

| EPU | −0.00157*** | −0.00173*** |

| (0.00005) | (0.00007) | |

| EPUxllpratio | 0.00036*** | |

| (0.00009) | ||

| llpratio | −0.00292** | −0.05478*** |

| (0.00117) | (0.01267) | |

| roa | 0.02102*** | 0.02017*** |

| (0.00158) | (0.00157) | |

| lntassets | 0.00698*** | 0.00726*** |

| (0.0006) | (0.0006) | |

| loandeposit | −0.00044*** | −0.00043*** |

| (0.00005) | (0.00005) | |

| interestincome | 0.00692*** | 0.00668*** |

| (0.0013) | (0.0013) | |

| depositgrowth | −0.00021 | −0.0002 |

| (0.0002) | (0.0002) | |

| loangrowth | 0.00047** | 0.00047** |

| (0.00022) | (0.00022) | |

| car | −0.00019 | −0.0002 |

| (0.00023) | (0.00023) | |

| Constant | 1.13866*** | 1.15876*** |

| (0.01343) | (0.01423) | |

| No. of observations | 5,091 | 5,091 |

| Adjusted R 2 | 0.3196 | 0.2069 |

| Bank clustered | Yes | Yes |

| Year clustered | Yes | Yes |

Note: Tobin’s Q ratio is the dependent variable. Refer to Appendix 1 for the definitions of the other variables. These are the OLS estimation results from pooled panel data regression models with double-clustered standard errors reported in parentheses.

The statistical significance at the 1 and 5% levels is indicated by *** and **, respectively.

Multicollinearity check

| Variable | VIF | 1/VIF |

|---|---|---|

| loangrowth | 5.83 | 0.171529 |

| depositgrowth | 5.71 | 0.175246 |

| roa | 1.44 | 0.693366 |

| llpratio | 1.25 | 0.800411 |

| lntassets | 1.22 | 0.822719 |

| EPU | 1.19 | 0.842003 |

| interestincome | 1.18 | 0.844466 |

| car | 1.08 | 0.926125 |

| loandeposit | 1.06 | 0.945773 |

| Mean VIF | 2.20 |

In terms of the moderation effect, the positive sign of the coefficient of EPU × llpratio in Model (2) in Table 3 indicates that economic policy uncertainty positively moderates the relationship between loan loss provisions and bank value. The marginal effect of loan loss provisions on bank value is given by δ(tobinq)/δ(llpratio) = −0.05478 + 0.0036EPU. In other words, a high EPU index smooths over the negative influence of loan loss provisions on bank value. Zhang et al. (2022) provided the explanation that economic policy uncertainty has less impact on banks with sound risk governance. Thus, high economic policy uncertainty might trigger more proactive risk governance by banks to mitigate the harm to their profitability and the negative impact of loan loss provisions on bank value. Banks could systematically manage the risks of economic policy uncertainty by applying the optimal loan loss provisions to safeguard their financial stability and promote sustainable business growth.

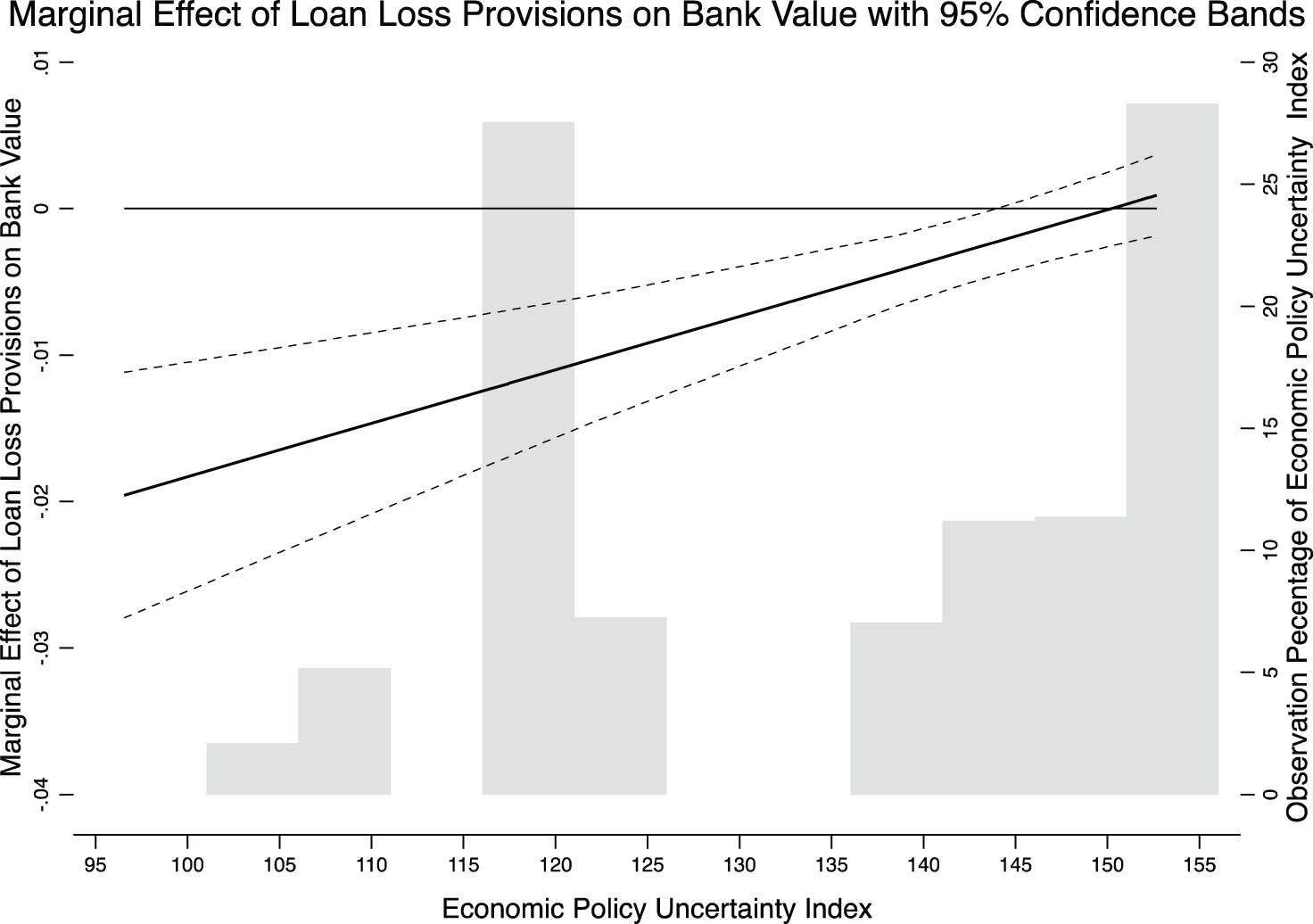

A further analysis of the marginal effects of loan loss provisions on bank value at different levels of the EPU index is conducted following the method suggested by Kingsley et al. (2017). Figure 1 illustrates that these effects significantly differ from zero across the EPU index range of 96.553 to 143.72, as delineated by the 95% confidence interval. The index value of 143.72 marks the upper boundary where the marginal effect reaches zero, suggesting that the moderating effect of the index is capped at this value. This result highlights a threshold effect at the upper limit of the EPU index. This threshold effect underscores how the moderating role of economic policy uncertainty operates within a specific range. Once the EPU index surpasses a critical boundary, its weakening influence on the loan loss provisions-bank value negative relationship is no longer significant. This finding offers an intuitive understanding of the threshold effect, demonstrating that economic policy uncertainty exerts a meaningful influence on bank value up to a point of the EPU index. Beyond this point, the interaction effects between economic policy uncertainty and loan loss provisions are not relevant for improving bank value. This implies that excessive policy uncertainties advocate for alternative credit risk management strategies.

Marginal effect of loan loss provisions on bank value.

In terms of the other independent variables, according to the estimation results in Model (1) and Model (2) in Table 3, the significance of llpratio indicates a negative relationship between the loan loss provisions and bank value. A one-percentage point increase in the loan loss provisions ratio is associated with a 0.05478-unit decrease in Tobin’s Q ratio in Model (2). Accounting-wise, an increase in loan loss provisions would reduce bank earnings in their income statements and balance sheets. When banks have higher financial distress or pressure during an economic recession or financial crisis, they usually increase the loan loss provisions to cover the potential loan losses. High loan loss provisions, according to Balla et al. (2012), Docking et al. (2000), and Laeven and Majnoni (2003), have a negative impact on bank profitability and stock prices. Also, high loan loss provisions provide negative signals to the market that banks might experience a challenging economic environment, affecting their future financial performance and bank value (Elnahass et al., 2014; Ng et al., 2020). All bank-related variables except the capital adequacy ratio and deposit growth are statistically significant in determining Tobin’s Q ratio. The return on assets (roa) has a similar characteristic to the net interest income to earning assets ratio (interestincome), as both variables measure bank profitability and are significantly positive. According to Model (2), a one-percentage point increase in the return on assets yields a 0.02017-unit rise in Tobin’s Q ratio, while the same increment in the net interest income to earning assets ratio corresponds to a 0.00668-unit increase. These results are supported by past studies that profitability is one of the most important indicators determining the value of a company (Ghosh, 2015; Huang et al., 2020), particularly for banks (Caprio et al., 2007; Fang et al., 2014). High bank profits indicate that high earnings are obtained from loans and investments. Loan growth (loangrowth) is significantly positive. A one-percentage point increase in the loan growth is associated with a 0.00047-unit increase in Tobin’s Q ratio in Model (2). It is consistent with the Theory of Financial Intermediation (Pyle, 1971) and the Production Theory (Sealey & Lindley, 1977) that the transformation from deposits to loans results in earning assets that generate market value. The same result is also found in past studies that show a strong connection between loan growth and bank value (Bernanke et al., 1996; Niu, 2016). However, the deposit growth (depositgrowth) is not significant because loans are generally the value driver for the banks.

Total assets (lntassets) is another significant variable with a positive coefficient that is supported in many valuation studies (Dang et al., 2018; Himmelberg & Hubbard, 2000; Linck et al., 2008). A company’s large total assets indicate its ability to source funds, a larger board size, stable financial performance, and more skilled staff. Banks with large total assets could generate more earnings and financial stability. The findings of Sloman et al. (2018) provide justification for the significantly negative loan-to-deposit ratio (loandeposit) found in Model (2). They highlight the concern of the liquidity risk to banks, as a high ratio of loans to deposits at a bank could raise alarm about fund shortages to cover potential risks and losses. Keeton (1999) also pointed out the issue of high liquidity risk, as higher loans may have a higher risk of non-performing loans. Capital adequacy ratio is commonly regarded as a measure of fund adequacy to secure financial stability. According to the Basel rule, all banks have to comply with the minimum requirement of 10.5% risk-bearing assets covered by their total Tier 1 and Tier 2 funds (Basel Committee on Banking Supervision, 2017). The statistics in Table 1 show that most of the banks comply with the regulation of the capital adequacy ratio, with an average of 15% and a low standard deviation. Thus, it explains the insignificance of the capital adequacy ratio (car) in our regression result.

Table 5 shows that 9 out of 11 of the sub-EPU indexes are negatively related to bank value, providing support to H1 in general. To further understand this relationship, we discuss the specific influences of some significantly negative sub-indexes on bank value. Monetary policy uncertainty concerns ambiguity about central bank decisions related to interest rates, inflation targeting, and money supply growth. Bordo et al. (2016) asserted that monetary policy uncertainty increases the risk premium demanded by investors, and this in turn raises the cost of capital for banks. Additionally, it introduces volatility in interest rates, which impacts banks’ net interest margins. Our findings are consistent with this perspective, indicating that heightened monetary policy uncertainty is associated with lower market valuations for banks. Fiscal policy uncertainty refers to the unpredictability of government spending, taxation, and budget deficits. Gulen and Ion (2016) argued that fiscal policy uncertainty affects firms’ investment and spending decisions and indirectly affects banks. Consequently, there is a hesitancy to undertake investments or engage in increased spending that likely results in lower profitability and, in turn, lower bank value. Our results support this view that banks are negatively impacted by ambiguous fiscal policies that limit strategic planning and operational efficiency. Regulatory policy uncertainty captures unpredictability in banking regulations such as capital and liquidity requirements or compliance costs. Li et al. (2014) contended that regulatory uncertainty resulting from frequent changes or vague regulatory guidance can cause operational challenges for banks that change their risk-taking behavior and increase compliance costs. The results of this study align with this point, demonstrating that bank value is lower under conditions in which regulation is unclear, as investors perceive greater risk and potential costs involved in compliance.

Sub-EPU indexes and bank value

| Variable | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Monetary policy | Fiscal policy | Taxes | Government spending | Health care | National security | Entitlement programs | Regulation | Financial regulation | Trade policy | Sovereign debt & currency crises | ||

| llpratio | −0.00094 | −0.00702*** | −0.00735*** | −0.00504*** | −0.01137*** | −0.00107 | −0.00861*** | −0.01556*** | −0.00611*** | −0.00544*** | −0.00386*** | |

| (0.00215) | (0.00195) | (0.00206) | (0.00131) | (0.00233) | (0.0027) | (0.0019) | (0.00229) | (0.00118) | (0.00201) | (0.00123) | ||

| EPU | ||||||||||||

| EPUxllpratio | ||||||||||||

| MP | −0.00024*** | |||||||||||

| (0.00005) | ||||||||||||

| MPxllpratio | −0.00002 | |||||||||||

| (0.00004) | ||||||||||||

| FP | −0.00043*** | |||||||||||

| (0.00002) | ||||||||||||

| FPxllpratio | 0.00005*** | |||||||||||

| (0.00002) | ||||||||||||

| TX | −0.0004*** | |||||||||||

| (0.00002) | ||||||||||||

| TXxllpratio | 0.00005*** | |||||||||||

| (0.00002) | ||||||||||||

| GS | −0.00031*** | |||||||||||

| (0.00001) | ||||||||||||

| GSxllpratio | 0.00004*** | |||||||||||

| (0.00001) | ||||||||||||

| HC | −0.00032*** | |||||||||||

| (0.00001) | ||||||||||||

| HCxllpratio | 0.00005*** | |||||||||||

| (0.00001) | ||||||||||||

| NS | 0.00014*** | |||||||||||

| (0.00003) | ||||||||||||

| NSxllpratio | −0.00002 | |||||||||||

| (0.00004) | ||||||||||||

| EP | −0.00036*** | |||||||||||

| (0.00001) | ||||||||||||

| EPxllpratio | 0.00005*** | |||||||||||

| (0.00001) | ||||||||||||

| RG | −0.00061*** | |||||||||||

| (0.00002) | ||||||||||||

| RGxllpratio | 0.00012*** | |||||||||||

| (0.00002) | ||||||||||||

| FR | −0.0003*** | |||||||||||

| (0.00001) | ||||||||||||

| FRxllpratio | 0.00005*** | |||||||||||

| (0.00001) | ||||||||||||

| TP | 0.00005* | |||||||||||

| (0.00002) | ||||||||||||

| TPxllpratio | 0.00002* | |||||||||||

| (0.00001) | ||||||||||||

| CC | −0.00019*** | |||||||||||

| (0.00001) | ||||||||||||

| CCxllpratio | 0.00003*** | |||||||||||

| (0.00001) | ||||||||||||

| No. of observations | 5,091 | 5,091 | 5,091 | 5,091 | 5,091 | 5,091 | 5,091 | 5,091 | 5,091 | 5,091 | 5,091 | |

| Adjusted R 2 | 0.20696 | 0.28838 | 0.27954 | 0.29153 | 0.30074 | 0.20626 | 0.29659 | 0.32809 | 0.29877 | 0.20103 | 0.2909 | |

| Bank clustered | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | |

| Year clustered | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

Note: The estimation results of the control variables are not reported to conserve space. Tobin’s Q ratio is the dependent variable. MP, monetary policy; FP, fiscal policy; TX, taxes; GS, government spending; HC, health care; NS, national security; EP, entitlement programs; RG, regulation; FR, financial regulation; TP, trade policy; CC, currency crises. Refer to Appendix 1 for the definitions of the other variables. These are the OLS estimation results from pooled panel data regression models with double-clustered standard errors reported in parentheses.

The statistical significance at the 1 and 10% levels is indicated by *** and *, respectively.

The moderating effects of all the sub-EPU indexes are also positive, except for monetary policy (Model (1)) and national security (Model (6)). In the estimated model that included these two sub-indexes, the relationship between bank value and loan loss provisions is not significant, and therefore, the moderation is not relevant. Overall, the hypothesis H2 is supported. Regulation policy uncertainty notably has the highest moderating effect. The regulation policy consists of the regulations on bank supervision and financial reform. Banks would optimize their loan loss provisions to deal with anticipated loan losses in response to the uncertainty in heavy supervision policies to demonstrate their capability and their loan asset quality. Thus, the regulation policy uncertainty weakens the negative impact of loan loss provisions on bank value.

5.2 Further Analyses

The relationship between economic policy uncertainty and bank value may vary across different dimensions of bank heterogeneity. We extend our analyses of the impact of economic policy uncertainty by investigating its influence from the perspectives of a financial crisis, bank prudence, and bank size. These expanded analyses provide a thorough view of the impact of economic policy uncertainty on banks in various economic environments and bank conditions.

5.2.1 Subprime Mortgage Crisis

The subprime mortgage crisis in the years 2007–2009 provided an episode of exogenous shock to examine if the results reported earlier remain robust. The results from Table 6 show that the impact of economic policy uncertainty on bank value is significantly negative with a larger magnitude compared to the coefficient of the baseline model. The uncertainty during the crisis had affected bank value more than other times. The interaction term EPUxllpratio remains significantly positive for the crisis period. During the crisis, banks experienced unprecedented mortgage defaults. The Lehman Brothers experienced bank failure that resulted in bankruptcy. Thus, the economic policies related to the Housing and Economic Recovery Act of 2008 became important to the US banks after the economic recession. More financial acts and regulations have been implemented, such as the Emergency Economic Stabilization Act (EESA) in 2008 to bail out $700 billions of troubled assets. This explains the significance of the EPU index. After the crisis, loan loss provisions became extremely important to protect bank value from uncertainty in economic policies and to safeguard banks from potential financial disasters in the future.

The impact of economic policy uncertainty during the financial crisis

| Variable | (1) | (2) |

|---|---|---|

| Baseline | Subprime crisis | |

| EPU | −0.00173*** | −0.00214*** |

| (0.00007) | (0.00027) | |

| EPUxllpratio | 0.00036*** | 0.00037** |

| (0.00009) | (0.00017) | |

| llpratio | −0.05478*** | −0.05344** |

| (0.01267) | (0.02301) | |

| roa | 0.02017*** | 0.01226*** |

| (0.00157) | (0.00212) | |

| lntassets | 0.00726*** | 0.00444*** |

| (0.0006) | (0.0013) | |

| loandeposit | −0.00043*** | −0.00046*** |

| (0.00005) | (0.00013) | |

| interestincome | 0.00668*** | 0.00341 |

| (0.0013) | (0.00344) | |

| depositgrowth | −0.0002 | −0.00026 |

| (0.0002) | (0.00032) | |

| loangrowth | 0.00047** | −0.00005 |

| (0.00022) | (0.00036) | |

| car | −0.0002 | 0.00062 |

| (0.00023) | (0.00054) | |

| Constant | 1.15876*** | 1.24181*** |

| (0.01423) | (0.04445) | |

| No. of observations | 5,091 | 1,094 |

| Adjusted R 2 | 0.31943 | 0.21481 |

| Bank clustered | Yes | Yes |

| Year clustered | Yes | Yes |

Note: Tobin’s Q ratio is the dependent variable. Refer to Appendix 1 for the definitions of the other variables. These are the OLS estimation results from pooled panel data regression models with double-clustered standard errors reported in parentheses.

The statistical significance at the 1 and 5% levels is indicated by *** and **, respectively.

5.2.2 Heterogeneity in Bank Characteristics

This section investigates if the findings are different according to bank prudence and bank size. Bank prudence is a multi-dimensional concept and may not be easy to measure. In this article, we limit the analysis to two dimensions whereby high-prudent banks are defined as those with a higher capital adequacy ratio and lower non-performing loans. These banks are prudent in their cash flow management and have higher financial stability. Referring to Estrella et al. (2000) and Jokipii and Milne (2011), the capital adequacy ratio is frequently employed as an indicator of bank prudence. Their findings suggest that banks with stronger capital buffers implement more effective risk management, thereby reducing their probability of failure. Non-performing loans also serve as an equally important indicator in assessing the bank prudence. For instance, Salas and Saurina (2002) show that financial institutions with lower non-performing loans tend to adhere to more rigorous underwriting standards and are less prone to default risk, indicating more prudent management practices. Similarly, Bikker and Vervliet (2018) found that higher non-performing loan levels signal inadequate credit risk controls, which can erode the financial stability of a bank.

According to the estimation results from Table 7, the relationship between economic policy uncertainty and bank value is significant for all banks, regardless of their prudence and size. The moderating impact of economic policy uncertainty is significant for banks with higher non-performing loans. We contended that a high economic policy uncertainty environment would call for more attention from the management of the banks with higher non-performing loans in determining the appropriate loan loss provisioning strategy to mitigate the impact of the uncertainty to protect financial stability. Under the dual stress of high economic policy uncertainty and non-performing loans, bank management will be more progressive in risk management than banks with less pressure on non-performing loans. Banks with a low or high capital adequacy ratio show no statistical difference pertaining to the moderating impact of economic policy uncertainty. The majority of the banks constantly adhere to the Basel standards regarding capital adequacy, and therefore, the ratio does not affect the moderating effect of economic policy uncertainty. The moderating impact of economic policy uncertainty is more pronounced for small and medium-sized banks compared to large banks, as the EPU × llpratio variable is significant for small and medium-sized banks but not for large banks. The small and medium-sized banks have fewer assets and monetary resources compared to the large banks. Consequently, when high economic policy uncertainty occurs, they face more financial constraints and have to rely on a better risk management strategy. The actions of the smaller-sized banks in times of challenging economic conditions to deal with the uncertainties within the constraint of their resources may be perceived by the market as a precautionary risk management approach to mitigate the negative valuation effects of loan loss provisions.

Moderating role of economic policy uncertainty: Bank prudence and size

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

|---|---|---|---|---|---|---|---|

| Lower NPL ratio | Higher NPL ratio | Lower CAR | Higher CAR | Small banks | Medium banks | Large banks | |

| EPU | −0.00136*** | −0.00134*** | −0.00133*** | −0.00193*** | −0.00186*** | −0.00187*** | −0.00182*** |

| (0.00013) | (0.00009) | (0.00009) | (0.00009) | (0.00008) | (0.00012) | (0.00024) | |

| EPUxllpratio | 0.00042 | 0.0002*** | 0.00037*** | 0.00043*** | 0.00033*** | 0.00047** | 0.00026 |

| (0.00043) | (0.00008) | (0.00012) | (0.00012) | (0.00011) | (0.00021) | (0.00018) | |

| llpratio | −0.05881 | −0.03116*** | −0.05537*** | −0.06309*** | −0.04789*** | −0.0763** | −0.0384 |

| (0.0603) | (0.0109) | (0.0174) | (0.01682) | (0.01528) | (0.03091) | (0.02536) | |

| roa | 0.03111*** | 0.01451*** | 0.02076*** | 0.02383*** | 0.01496*** | 0.01764*** | 0.03209*** |

| (0.00447) | (0.00139) | (0.00246) | (0.00212) | (0.00267) | (0.00227) | (0.00426) | |

| lntassets | 0.01034*** | 0.00419*** | 0.00705*** | 0.00809*** | 0.0061** | 0.0147*** | −0.00804*** |

| (0.00123) | (0.00064) | (0.00084) | (0.00086) | (0.00293) | (0.00187) | (0.00162) | |

| loandeposit | −0.0005*** | −0.00039*** | −0.00041*** | −0.00042*** | −0.00045*** | −0.00032*** | −0.00053*** |

| (0.0001) | (0.00006) | (0.00007) | (0.00006) | (0.00007) | (0.00007) | (0.00011) | |

| interestincome | 0.01158*** | 0.00384** | 0.01969*** | 0.00061 | 0.00657*** | 0.01131*** | 0.00733** |

| (0.00298) | (0.00165) | (0.00218) | (0.00167) | (0.00188) | (0.00218) | (0.00301) | |

| depositgrowth | 0.00027 | −0.00068*** | 0.00023 | −0.00034* | −0.00014 | −0.00005 | −0.0001 |

| (0.00041) | (0.00016) | (0.00039) | (0.0002) | (0.00035) | (0.00018) | (0.00033) | |

| loangrowth | −0.00031 | 0.0011*** | −0.00014 | 0.00073*** | 0.00042 | 0.00017 | 0.0002 |

| (0.00043) | (0.00019) | (0.00041) | (0.00021) | (0.00037) | (0.00021) | (0.00037) | |

| car | −0.00007 | −0.00027 | −0.00294*** | 0.00015 | −0.00037 | 0.00078** | −0.00132 |

| (0.00041) | (0.00026) | (0.00098) | (0.00028) | (0.00031) | (0.00037) | (0.00086) | |

| Constant | 1.05419*** | 1.1496*** | 1.09554*** | 1.18276*** | 1.19184*** | 1.04352*** | 1.4383*** |

| (0.02901) | (0.01775) | (0.02106) | (0.01812) | (0.04223) | (0.03284) | (0.04811) | |

| No. of observations | 2,253 | 2,678 | 2,537 | 2,546 | 2,334 | 2,142 | 615 |

| Adjusted R 2 | 0.27017 | 0.23489 | 0.34757 | 0.31334 | 0.28637 | 0.38460 | 0.43001 |

| Bank clustered | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year clustered | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

Note: Tobin’s Q ratio is the dependent variable. See Appendix 1 for the definitions of the other variables. Low NPL ratio denotes non-performing loans ratio is less than its median. High NPL ratio denotes non-performing loans ratio is more than its median. Low CAR denotes capital adequacy ratio is less than its median. High CAR denotes capital adequacy ratio is more than its median. Following Niu (2016), small banks are those with total assets less than or equal to $1 billion. Medium-sized banks are those with total assets from $1 billion to $10 billion. Large banks are those with total assets greater than $10 billion. These are the OLS estimation results from pooled panel data regression models with double-clustered standard errors reported in parentheses.

The statistical significance at the 1, 5, and 10% levels is indicated by ***, **, and *, respectively.

5.3 Endogeneity Checks

In this section, we check if the findings are affected by possible endogeneity and reverse causality.

5.3.1 Exogenous Energy Price Shock

As explained in Section 3.4, the credit risks faced by banks can be affected by energy price changes, especially banks that provide financing to energy companies. Volatile energy price changes may harm the profitability and loan repayment capacity of these companies. Excessive energy price fluctuations may prompt policy intervention from the authorities to maintain not only macroeconomic but also financial stability. The exogenous variable of energy price shocks is used to capture external drivers of economic policy uncertainty. The EPU index is first regressed on the prices of two energy sources, the crude oil price, and retail gasoline price, as in equation (3).

where

Re-estimation of equation (2) to address endogeneity concern due to energy price shock

| Variable | (1) | (2) |

|---|---|---|

| EPU | tobinq | |

| OIL | −63.45968*** | |

| (2.15718) | ||

| GASOLINE | 56.90313*** | |

| (3.32926) | ||

| resid_EPU | −0.00167*** | |

| (0.00007) | ||

| resid_EPUxllpratio | 0.00039*** | |

| (0.00008) | ||

| llpratio | −0.00751*** | |

| (0.00132) | ||

| roa | 0.02085*** | |

| (0.0015) | ||

| lntassets | 0.00603*** | |

| (0.00059) | ||

| interestincome | 0.00724*** | |

| (0.00127) | ||

| loandeposit | −0.00037*** | |

| (0.00005) | ||

| depositgrowth | −0.00027 | |

| (0.00021) | ||

| loangrowth | 0.00055** | |

| (0.00022) | ||

| car | −0.00035 | |

| (0.00024) | ||

| Constant | 132.34508*** | 0.94511*** |

| (0.17791) | (0.01274) | |

| No. of observations | 10,944 | 5,091 |

| Adjusted R 2 | 0.16985 | 0.28778 |

| Bank clustered | Yes | Yes |

| Year clustered | Yes | Yes |

Note: The dependent variables are EPU index in Model (1) and tobinq in Model (2), respectively. resid_EPU represents the residuals obtained from the regression of the EPU index on the change in the average monthly crude oil price and retail gasoline price. Refer to Appendix 1 for the definitions of the other variables. These are the OLS estimation results from pooled panel data regression models with double-clustered standard errors reported in parentheses.

The statistical significance at the 1 and 5% levels is indicated by *** and **, respectively.

5.3.2 The Shock from US Political Tension

Political tensions, disagreements, and conflicts between the two major political parties in the United States as well as their strength, might be another factor that affect economic policy uncertainty. We refer to the study of Ng et al. (2020) and employ three instrumental variables that reflect political tension in the United States. The instrumental variables are the Partisan Conflict Index by Azzimonti (2018), DW-NOMINATE scores by McCarty et al. (1997), and relative political strengths by Kaviani et al. (2020). The Partisan Conflict Index represents the extent of political disagreement among federal-level politicians in the United States. The index, calculated based on the number of policy disagreements reported in the newspapers, is sourced from the Federal Reserve Bank of Philadelphia. The natural logarithm of the index is computed in accordance with the literature. Next, the first dimension of the DW-NOMINATE scores is intended to record the legislators’ evolving ideologies towards government interference in the economy. The scores capture the political polarization between Democrats and Republicans in the US Senate. We calculate the difference between the mean scores in the first dimension of DW-NOMINATE of the legislators representing the two parties as the second instrumental variable. The scores are sourced from the Voteview: Congressional Roll-Call Votes Database constructed by Lewis et al. (2022). A greater disparity between the mean scores indicates greater polarization that will increase economic policy uncertainty. The last variable to measure political tension is the relative political strength between the Democrats and Republicans. It is computed based on the difference between the percentages of the legislative seats of the two parties in the US Senate. The data is downloaded from the Voteview: Congressional Roll-Call Votes Database according to the type of congressional party. A small difference in the percentages reflects a larger turnover in the economic policies, contributing to larger uncertainties. We name the three instrumental variables as CONFLICT, POLARIZATION, and STRENGTH, respectively.

In the 2SLS estimation, we first regress the EPU index on each of the instrumental variables representing political tension as well as the average monthly changes in crude oil price and the US retail gasoline price. All the instrumental variables are significant in explaining the EPU index in the first-stage estimation results. After that, the predicted value of the EPU index, denoted as EPU (Instrumented), is generated and used in the second stage regression specified in equation (2) to replace the EPU index. Table 9 shows the estimation results. The variable EPU (Instrumented) is significantly negative. The interaction term EPU (Instrumented)xllpratio is also significant. The magnitudes of the coefficients are analogous compared to the results for the baseline model, suggesting that the primary regression results are still robust after consideration of possible endogeneity. The weak identification test is conducted. The Cragg–Donald F-statistics in columns (2), (4), and (6) are 98.89, 101.84, and 123.77, respectively. They are well above the conventional threshold of 10, indicating that the instruments used are strongly correlated with the EPU index. In other words, the F‐statistics suggest strong predictive power for the first‐stage regressions. The validity of the instruments is also tested. The Hansen J test statistics in those same columns yield p‐values of 0.2748, 0.3277, and 0.5355, respectively, which are not statistically significant. This implies that we fail to reject the null hypothesis that the instruments are valid and uncorrelated with the error term in the structural equation. These diagnostics demonstrate that the chosen instruments exhibit both strength and validity, lending credibility to the 2SLS estimations.

Re-estimation of equation (2) with two-stage least squares

| Variable | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| EPU | tobinq | EPU | tobinq | EPU | tobinq | |

| CONFLICT | 49.32383*** | |||||

| (0.39736) | ||||||

| POLARIZATION | 389.14022*** | |||||

| (2.82605) | ||||||

| STRENGTH | 1.58541*** | |||||

| (0.0232) | ||||||

| OIL | −23.59323*** | −16.96035*** | −76.80764*** | |||

| (1.14141) | (.98367) | (1.95512) | ||||

| GASOLINE | 14.68383*** | 22.91931*** | 90.23349*** | |||

| (1.67198) | (1.45808) | (2.9269) | ||||

| EPU (Instrumented) | −0.00105*** | −0.00109*** | −0.00112*** | |||

| (0.00007) | (0.00007) | (0.00009) | ||||

| EPU (Instrumented)xllpratio | 0.00022*** | 0.00029*** | 0.00021*** | |||

| (0.00005) | (0.00006) | (0.00006) | ||||

| llpratio | −0.03703*** | −0.04586*** | −0.0298*** | |||

| (0.00863) | (0.00944) | (0.00906) | ||||

| roa | 0.02123*** | 0.02115*** | 0.02683*** | |||

| (0.00181) | (0.00181) | (0.00171) | ||||

| lntassets | 0.00618*** | 0.00605*** | 0.0035*** | |||

| (0.00066) | (0.00068) | (0.0006) | ||||

| interestincome | 0.00753*** | 0.00718*** | 0.00586*** | |||

| (0.0013) | (0.00127) | (0.00134) | ||||

| loandeposit | −0.00035*** | −0.00032*** | −0.00034*** | |||

| (0.00005) | (0.00005) | (0.00006) | ||||

| depositgrowth | −0.00041** | −0.00047** | −0.00024 | |||

| (0.0002) | (0.00021) | (0.00021) | ||||

| loangrowth | 0.00078*** | 0.00085*** | 0.0006*** | |||

| (0.00022) | (0.00022) | (0.00023) | ||||

| car | −0.00053** | −0.00058** | −0.00072*** | |||

| (0.00024) | (0.00025) | (0.00025) | ||||

| Constant | −100.83385*** | 1.0743*** | −183.64955*** | 1.08089*** | 119.65021*** | 1.12012*** |

| (1.87701) | (0.01339) | (2.33393) | (0.01346) | (0.2497) | (0.0164) | |

| No. of observations | 10,944 | 5,091 | 10,944 | 5,091 | 10,944 | 5,091 |

| Adjusted R 2 | 0.75439 | 0.24492 | 0.69012 | 0.23817 | 0.38364 | 0.22702 |

| Cragg–Donald F-statistic | 98.891 | 101.841 | 123.769 | |||

| Hansen J test (p-value) | 0.2748 | 0.3277 | 0.3535 | |||

| Bank clustered | Yes | Yes | Yes | Yes | Yes | Yes |

| Year clustered | Yes | Yes | Yes | Yes | Yes | Yes |

Note: The dependent variables are EPU index in Models (1), (3), and (5) and tobinq in Models (2), (4), and (6), respectively. CONFLICT is the natural logarithm of the Partisan Conflict Index. POLARIZATION is the difference between the mean scores in the first dimension of DW-NOMINATE for the legislators representing Democrats and Republicans. STRENGTH is the difference between the percentages of the US Senate legislative seats owned by the two major parties. Refer to Appendix 1 for the definitions of the other variables. These are the estimation results using 2SLS estimators with double-clustered standard errors reported in parentheses. The instrumental variables used in each of the models are the change in the average monthly crude oil price and retail gasoline price and the political tension variable. The predicted EPU index is denoted as EPU (Instrumented).

The statistical significance at the 1 and 5% levels is indicated by *** and **, respectively.

5.3.3 Dynamic Panel Generalized Method of Moments (GMM) Estimator

The reverse causality between economic policy uncertainty and bank value is an additional endogeneity concern. The dynamic panel generalized method-of-moments (GMM) method by Wintoki et al. (2012) recommends utilizing the lagged dependent variable of the bank value (Tobin’s Q ratio). The dynamic panel model is estimated using System GMM and the results are reported in Table 10. The result of the regression confirms the positive sign of the moderating effect of economic policy uncertainty and reaffirms its significance. This suggests that the earlier findings are not undermined by endogeneity.

System GMM estimator for the dynamic panel model

| System GMM | |

|---|---|

| L.tobinq | 0.65464*** |

| (0.04989) | |

| EPU | −0.00048*** |

| (0.00013) | |

| EPUxllpratio | 0.00036*** |

| (0.00012) | |

| llpratio | −0.05438*** |

| (0.01761) | |

| roa | 0.00736*** |

| (0.00237) | |

| lntassets | 0.00256*** |

| (0.00095) | |

| interestincome | 0.00373** |

| (0.00174) | |

| loandeposit | −0.00028*** |

| (0.00006) | |

| depositgrowth | 0.00027* |

| (0.00016) | |

| loangrowth | −0.00046** |

| (0.00019) | |

| car | −0.00068** |

| (0.00031) | |

| Constant | 0.3999*** |

| (0.0575) | |

| No. of observations | 4,945 |

| Arellano-Bond test | 0.726 |

Note: L. is the prefix of the lagged variables with time t − 1. Refer to Appendix 1 for the definitions of the other variables. The statistical significance at the 1, 5, and 10% levels is indicated by ***, **, and *, respectively.

6 Conclusion

This study provides empirical evidence that economic policy uncertainty significantly impacts bank value and moderates the relationship between loan loss provisions and bank value. The negative effect of economic policy uncertainty on bank value indicates that decreasing uncertainty through transparent, consistent, and certain economic policies would benefit the banking sector. Bank managers should develop strong risk management strategies to minimize the effects of economic policy uncertainty on bank value. Our panel data regression analyses, reinforced by endogeneity checks, consistently demonstrate that the negative impact of loan loss provisions on bank value is alleviated during times of economic policy uncertainty. This mitigation suggests that the standard negative impact associated with increased provisions is less pronounced when economic policy uncertainty is high, potentially due to strategic adaptations by banks in their risk management practices. There is a threshold to this mitigation effect. It does not occur when economic policy uncertainty is exceedingly high.

This study provides two key contributions. It represents new attempts to introduce the macroeconomic determinant through the EPU index to study the impact of economic policy uncertainty on bank value. Past studies have only focused on the use of traditional technical valuation analyses, which rely on internal banking variables. The traditional analyses neglect the impact of uncertainty in economic policies and might generate a valuation bias due to the limited interpretation of the microeconomic perspectives of banks. The next contribution of this research is its extension of the existing empirical findings previously outlined by Danisman et al. (2021), Ng et al. (2020), and Ozili (2022). Past studies have found evidence of the impact of uncertainty in economic policies on loan loss provisions, but the further influence on bank value has not been addressed yet. This study bridges the gap by advancing the understanding of the impact of loan loss provisions on bank value from the perspective of macroeconomic uncertainties. Our investigation of the moderating role of economic policy uncertainty on the loan loss provisions–bank value relationship represents a key novelty of this article. This dimension not only clarifies how uncertainty in economic policies might alter the effectiveness of provisioning strategies but also reinforces the importance of monitoring macroeconomic signals when assessing bank performance. By the moderation analysis, our findings contribute to ongoing debates on financial stability and regulatory oversight, particularly in times of heightened economic policy fluctuations.

The findings of this study lead to several implications. The main implication for research is that macroeconomic determinants should be considered in future research on valuation modelling for banks and other financial institutions. Due to the significant effect of economic policy uncertainty, bank valuation models, which are more susceptible to the point of view of a solely technical analysis must be revisited. To avoid serious valuation bias, the new macroeconomic perspective on valuing banks must be considered and incorporated into valuation modelling. The common cash flow model and dividend-based model might not be able to capture the dynamic changes of the challenging economic environment, which may greatly affect bank profitability and risk management. Revisiting the valuation theory for banks is needed as banks have unique business models compared to non-banks, particularly in financial governance and regulation. As a result, combining the microeconomic (internal banking performance and valuation), macroeconomic (policy uncertainties), and risk management (loan loss provisions) perspectives in valuing banks provides a more comprehensive view. As for the practical implication, during rising uncertainty in economic policies, bank managers could have a better instrument to quantify the impact of this uncertainty to make the appropriate discretionary loan loss provisioning to safeguard the bank value.

In terms of policy implications, policymakers could strengthen existing policies to guide banks to take more dynamic and proactive actions on loan loss provisioning due to economic policy uncertainty. Strengthening the risk governance of banks through loan loss provisioning could enhance the financial stability of banks during an economic recession or financial crisis. Small and medium-sized banks are more vulnerable to economic policy uncertainty and should be prioritized in policy implementation. This calls for rigorous supervisory frameworks. Regular stress testing exercises for banks could incorporate varying levels of economic policy uncertainty to identify which financial institutions are most susceptible. As a result, regulators and central banks could more effectively gauge the capital adequacy needs of banks to mitigate systemic risks. Moreover, our finding that small and medium‐sized banks are more vulnerable under high economic policy uncertainty suggests that targeted regulatory support should be given to them. It may help these banks to manage funding pressures and credit risk more effectively. By proactively adjusting supervisory policies in response to rising economic policy uncertainty, policymakers can lessen the likelihood of financial instability.

This study has the limitation of not considering the impact of economic policy uncertainty in other countries and geopolitical risks that may also affect the US banks. The recent bank collapse in the United States indicated the importance of depositors’ confidence and potential for contagion. The resilience of the banking sector of a country to withstand the negative consequences of these contagion effects depends on the institutional quality of the country. The implications of these factors on bank valuation could be considered in future studies.

Acknowledgements

This article reports part of the research conducted by the first author for his doctoral study at the Faculty of Business and Economics, University of Malaya. We are grateful to our colleagues at the faculty for their comments and suggestions on an earlier draft of this article. We thank two anonymous reviewers for their insightful comments that led to improvement in this article.

-