Credit for the Poor, Investments for the Rich? Different Strategies for Investing and Saving Money in Medieval Tirol

-

Stephan Nicolussi-Köhler

Stephan Nicolussi-Köhler is Assistant Professor of Medieval History and Auxiliary Sciences at the Department of History and European Ethnology at the University of Innsbruck. His research interests include Mediterranean trade and medieval capital markets, with a focus on small-scale lending and pawnbroking. His publications include:S. Nicolussi-Köhler , Marseille, Montpellier und das Mittelmeer. Die Entstehung des südfranzösischen Fernhandels im 12. und 13. Jahrhundert, Pariser Historische Schriften 121, Heidelberg 2021 (https://doi.org/10.17885/heiup.833 ) andS. Nicolussi-Köhler (Ed.) , Change and Transformation of premodern Credit Markets. The Importance of small-scale Credits, Heidelberg 2021 (https://doi.org/10.11588/heibooks.593).

Abstract

This paper provides an overview of the various financial resources that existed in medieval Tirol to meet financial needs, using notary registers and court records from the 14th century as sources. These provide ample evidence of an active capital and land market in rural areas, which offered various ways of saving and investing money. Saving and investment behaviour was crucial for coping with external adversities such as harvest failure, but also with life events (marriage, bringing up children, retirement), and households sought to manage these risks. The results show that the poor and the rich behaved differently when it comes to investing and saving, and that their behaviour was strongly influenced by access to different financial instruments.

The aim of this paper is to discuss the economic functioning of rural capital and land markets for the purposes of saving and investing money, or for acquiring cash in Tirol in the late 14th century. When historians study premodern financial history, they usually apply a perspective focusing on early public credit, trade credit credit, highly urbanised areas, or the economic elite of the society. [1] Rural areas and the economic activities of the lower social classes have been less studied to date. [2] Recent studies emphasised the importance of informal financial practices, such as the transfer of assets or money within households or families. [3] Both participation in the land and capital markets and the mobilisation of financial resources within the family or household played an important role in the economic life of individuals in order to manage risks or save for the future. The most important means of accumulating and transferring capital were probably marriage and inheritance. [4] Although of great importance, both the practices of saving and investing in capital and land markets, as well as the accumulation of capital through inheritance and marriage matters in late medieval societies are understudied. This is partly due to the difficult situation regarding the conservation of sources on these practices. [5]

Academic interest in commercialisation and the growing system of credit dependency in the 13th century has fuelled the debate about an increasing differentiation between the peasant and non-landowning classes. [6] An important feature of this new wave of research on financial markets is the interest in cash flow management, as well as a wish to improve our knowledge about household financial behaviour. [7] The practices of medieval households in managing their financial assets have been the subject to speculation rather than empirical study. At the same time, informal practices often go unnoticed, thus allowing a distortion of the entire picture.

This raises the question of how households in fragile economies that were heavily influenced by exogenous factors actually made a living and how financial resources were managed. Based on a collection of various notarial registers from the second half of 14th century in Tirol, this article examines how certain groups – mostly wealthier sections of the rural and urban population – used different practices to save, invest and raise capital. Section 1 describes the regional context, which then leads to a discussion of the sources and data in Section 3 addresses why medieval households would have needed to invest and save. Section 4 turns to the different assets and tools available for saving or investing money. The following Section 5 presents the findings and general trends, while Section 6 contains conclusions that can be drawn from the analysis.

1 Regional Context

Tirol is located in the Eastern Alps. In medieval times the County of Tirol was part of the Holy Roman Empire. In the 13th century, Count Meinhard II of Gorizia (1258–1295) combined the titles to the lands to the south and north of the Brenner Pass to create the County of Tirol. For the sake of brevity, the terms northern Tirol and southern Tirol are used to refer to the areas that roughly correspond to the present-day regions of Trentino-Alto Adige/Südtirol and the Austrian state of Tirol.

Agricultural practice in Tirol included animal husbandry on high alpine meadows, mixed agriculture with cereal cultivation and dairy production at lower altitudes, and, especially on the south side of the Alps, viticulture. Agricultural output differed both in the form of cultivation and in the labour intensity depending on the location and quality of land. Overall, a growing agricultural specialisation with a rising market dependency from the 14th century onwards can be seen.

Urbanisation in Tirol was low compared to the European average. However, there were several village-rural market systems that connected city-like settlements with their surroundings, and peasants could sell their produce at such markets. In several cities such as Meran, Bozen or Glurns, there were regular fairs. The Pentecost and Martini fairs in Meran, that took place in the spring and in the fall, were of interregional importance and a popular payment date for credit transactions. [8]

Even the rural regions of Tirol were, at least in part, penetrated early on by the written administrative practices of the public notary’s office and monetary economy. [9] The County of Tirol was characterised by the politics of Meinhard II, who disempowered the local nobility and created a strong principality between 1258 and 1295. The dominant position of the sovereign continued into the 14th century and beyond. Serfdom disappeared nearly everywhere in the county during the reign of Meinhard II. Likewise, the manorial and lordly restrictions on exchange of land largely vanished and the peasantry enjoyed favourable property rights with the dissemination of hereditary tenure (Erbleihe). Insecure tenurial rights (Freistift), where the tenant’s land could be withdrawn anytime, continued to exist mostly in areas of enclosed manorial estates such as ecclesiastical institutions. [10] The widespread right of hereditary tenure enabled the peasants to bequeath their farms, to sell, mortgage or divide their leaseholds with consent of their lord. Land could also be sub-leased, provided that the owner was informed. [11] Land sales, including sales by peasants, are recorded on a large scale as early as the 13th century. Urban investments of burgher or municipal institutions in rural landholding were widespread, as has been shown for the city of Bozen. Thus, factor markets for the exchange of land and capital emerged early in Tirol. [12] Demesne lordship (Gutsherrschaft) was declining in general in late medieval Tirol but as recent research on eastern Switzerland has shown, landlords continued to interfere in the organisation of their estates to some extent. [13]

In Tirol there was a lower class of peasants in addition to the peasants who owned full estates. These latter were called Söllleute (cottagers) if they owned small plots of land or Inwohner (lodgers) if they were landless co-habitants in peasant or sub-peasant households. They earned their living mainly as craftsmen, servants, day-labourers, forest labourers or miners. [14] Even cottagers had only limited access to common goods such as forest or pasture. [15] No specific demographic data on the late Middle Ages exists, but research on early modern Tirol has shown that in certain districts of northern Tirol, up to 25 percent of the overall population belonged to the group of landless households or households with only small land ownership. [16] Already in this sub-peasant strata, there was an active land market: even the smallest plots of land were sold or mortgaged in late medieval Tirol. [17]

Overall, despite a low rate of urbanisation and a high dependence on agriculture, there were many opportunities for farmers to acquire financial assets or capital. Since peasants had limited property rights over the land they cultivated, they could mortgage it to obtain credit. In the southern part of Tirol, sharecropping contracts were a source of working capital, so the situation was similar to that in northern Italy. [18] However, the specific situation in Tirol differed from neighbouring regions: in Tirol, there was no opportunity for funded debt, as in Italy or northern or western Europe. There was also no large homogeneous institutional framework to facilitate the flow of capital throughout society. Instead, perpetual rents were sold on a private basis. Capital markets were organised to mediate problems of asymmetric information, for example through the use of public notaries.

2 Source Material and Data

The sources for this paper are primarily notary registers and court records from the late 14th century. The former institution, the public notary, had become widespread across southern Tirol since the 12th century, and notaries were active both in the bigger towns of Bozen, Glurns or Meran and in smaller settlements in the countryside such as Laas, Forst or Lana. [19] They recorded legal transactions in an abbreviated form in registers (imbreviatura). Ample notary registers exist for medieval southern Tirol, most of them recorded in Meran or Bozen. Drawing on a set of several notary registers of the second half of the 14th century (created by the following notaries: Konrad of Alerheim (1357), Jacob of Laas (1391, 1398, 1400) and Christanus de Eppiano (1406–1407)) and the oldest existing court records of Meran (1388–1391), this paper describes the use of different investment and saving strategies in the last two decades of 14th century southern Tirol. [20]

The notaries recorded individual acts of all kinds, from the sale of land to dowry contracts, in their registers, which facilitated the subsequent verification of legal acts and made it possible to issue a complete contract (instrumentum) for a fee at the request of the contracting parties. [21] Transactions of low value were all the more affected by this, as the transaction costs were proportionally much higher. [22] Here, we must note the currency used in Tirol at this time, which were the Veronese or Berner denarii (den.). These will be referred to throughout this text. Smaller denominations were marca (mr.), librae (lb.), grossi (gr.) and solidi (sol.). [23]

As Table 1 shows, the majority of all legal contracts was connected to credit, debts or transfer of property or rights. The selected registers probably do not cover the full variety of different forms of saving and investment. However, the cases illustrate the diversity of saving instruments and investment opportunities and show that certain aspects, such as the use of loans and pledges to pay dowries, were quite stable over time.

Notarial acts in southern Tirol (1357 to 1391).

| Konrad of Alerheim (1357) | Jakob of Laas (1390–1392) | Cristanus de Eppiano (1406/1407) | Court protocols of Meran (1388–1391) | |||||

|---|---|---|---|---|---|---|---|---|

| Total number | Share in % | Total number | Share in % | Total number | Share in % | Total number | Share in % | |

| Acts relating primarily to credit and debt | 76 | 30 | 45 | 47 | 109 | 53 | 153 | 39 |

| Acts relating primarily to transfers or investments | 113 | 44 | 25 | 26 | 55 | 27 | 89 | 23 |

| Acts relating to other rights and obligations | 56 | 22 | 9 | 10 | 38 | 19 | 18 | 5 |

| Court-related activity | 9 | 4 | 5 | 5 | 3 | 1 | 106 | 27 |

| Other | 0 | 0 | 11 | 12 | 0 | 0 | 29 | 7 |

| Overall Contracts | 168 | 95 | 205 | 395 | ||||

Sources: StA Meran, NI 3; NI 22; NI 30; GP 1.

For the period from 1388 to 1391, court protocols of the assemblies of the court meetings (eleichtaidinge) exist, which took place in court places in the countryside (Dingstätten) and in the city court (stadtrecht and dorfrecht) of Meran and in the court district of the so-called Landgericht (Meran und Burggrafenamt). [24] The court books recorded criminal assaults and civil law matters, such as legal changes concerning property and assets. Although the protocols cover only the period from July 1388 to April 1391, they are a unique source for small-scale transactions that would not be recorded by a public notary.

The different sources allow an understanding of the investment strategies used by households. A few examples of contracts recorded by a notary (in town) shall illustrate this. On 11th May 1391, Ulricus, son of the deceased Jaennlinus de Turnell, and his wife Brigida sold a rent consisting of payment in grain (rye and barley) for six mr. (or 720 gr.). The rent was redeemable for five years. [25] Just six days later, on 17th May 1391, the same couple acquired a rent in kind, consisting of cheese, grain (wheat) and small animals, for five mr. Interestingly, this rent came from the farmstead of said Ulricus (de curia predicti Uelrici de Turnell), which effectively freed him from this rent obligation. The rent was once again redeemable for five years. [26] In this case, the sale of the first rent was used for a strategic investment and enabled Ulricus and Brigida de Turnell to restructure debt (or rent in this case). As the payments were in kind, the reason could have been a change in the price or availability of the goods (cheese instead of cereals), or the exchange of a rent with a higher interest rate for one with a slightly lower interest rate.

Another example of household investment strategies is a marriage arrangement recorded by a notary (in town). In January 1398, a contract was drawn up between Katherina and Johannes rotificis (wheelwright) to settle the arrangement of an existing marriage contract between their underage children from previous marriages (Michael, son of Katherina, and Cristina, daughter of Johannes). The main concern was about the management of a farmstead (Camplung guot). It was the accumulated debt of the bride’s father Johannes that threatened the continued cultivation of the estate. [27] In order to ensure the economic viability of the estate, he transferred the farm to the next generation. The contract stipulated, among other things, that Katherina was allowed to stay on the farm and that she should receive a limited amount of firewood. In return, she had to assume the farm’s debts of 43 Mr. and 4 lb. (equal to 5,205 gr.) and take care of the farm until the children came of age. Besides, she was to receive one third of the mobile property of the manor, but she was liable if the value of the remaining household property decreased. When the children reached the age of majority, she had to hand over the farm. In this case, the farm was transferred to the next generation and a retirement plan was made for Katherina. This example shows how assuming someone else’s debts, transferring property to the children or arranging payments, were essential parts of the household economy. And although it is not spelled out in the contract, it seems obvious that in this way the debts could be repaid and the farm could remain in family ownership.

These two examples illustrate the richness of the source material, which enables us to reconstruct stipulations, financial strategies and contracts across two generations or to reveal the strategy behind investments.

Loan and investment amounts ranged from buying a small plot of land worth 24 gr. to credits of up to thousands of gr., as in the latter case mentioned above. These amounts can be compared to the wages of labourers at this time. At the end of the 14th century, the average annual income of a skilled labourer was about 1,920 to 2,880 gr. per year (for a master labourer), while an unskilled day labourer earned 960 gr. per year, calculating with approximately 240 working days a year. However, it must be noted, most labourers had other sources of income besides wages, such as gardening or farming, or they owned their own livestock.

Selected prices and wages in Tirol c. 1390 to 1410 (in grossi).

| Item | Price |

|---|---|

| Cow | 84-120 gr. |

| Pig | 58 gr. |

| Rye (per modius, c. 170 litre) | 30 gr. |

| Barley (per modius, c. 170 litre) | 24 gr. |

| Wine (per carrada, c. 622 litre) | 180 gr. |

| Salt (per carrada, c. 622 litre) | 24 gr. |

| Labourer | Daily wage |

| Mason | 7 gr. (for labour and food) |

| Carpenter | 8 gr. (for labour and food) |

| Master stonecutter | 10-12 gr. (and additionally wine) |

| Unskilled day labourer | 3-4 gr. |

Note: Wine prices varied from 126 to 240 gr. Sources: L. Thaler, Wertewandel im spätmittelalterlichen Tirol. Maßeinheiten, Münzgewicht, Wechselkurse und Preise zwischen 1290 und 1500, in: Geschichte und Region 29/2, 2020, pp. 38-61; Nicolussi-Köhler, Between City and Countryside; J. Ladurner, Über die Münze und das Münzwesen in Tirol vom 13. Jahrhundert bis zum Ableben Kaiser Maximilians, 1519, in: Archiv für Geschichte und Alterthumskunde Tirols 5, 1868, pp. 1-102, 275-308, here pp. 89-92.

3 The Need for Saving and Investing Money and Managing Liquidity

It has long been known that consumer and commercial loans, including the acquisition of working capital, have made up the largest part of the credit economy and are closely connected to strategies of saving and investing money. [28] Very often we do not have information about what preceded the decisions to become active on the financial market, however, there were various reasons for the need to save and invest money. Some of these stemmed from internal factors, such as lifecycle events or investments in one’s business; others were external, such as extraordinary taxation or harvest failures. The need for financial resources to overcome adversity was great: the main challenges were famines, harvest failures, wars or extraordinary taxation. [29]

Cautious estimates based on medieval estate registers (Urbare) of the monastery of Stams in Tirol indicate an average levy burden (ground tax and tithe) of peasant holdings amounting to about 22 percent of the grain yield (see Tab. 3.). After deducting the cost of the grain for sowing (approximately 20 to 25 percent), this leaves roughly 58 percent of the yield to the peasant family. With this they had to cover extraordinary payments, wage labourers and their own livelihood, as well as care for their livestock. Additional expenses for events like marriages or extraordinary taxes had to be paid from the remaining surplus. [30] Even considering a large variation in the estimate, a harvest decline of one third, as happened frequently, would have been enough to cause difficulties for the peasant households. [31]

Expenses and levies of agricultural peasant households in Tirol (1381).

| Expenses and levies | Amount of agricultural production |

|---|---|

| Ground tax | c. 12 percent |

| Tithe | c. 10 percent |

| Seeds for the next sowing | c. 20-25 percent |

| Total | c. 42-47 percent |

| Livelihood of the family | |

| Fodder for the livestock | |

| Wage for labourers | c. 53-58 percent |

| Extraordinary payments (taxes, etc.). | |

| Lifecycle events (marriages, dowry payments, etc.) |

Source: The calculation is based on examples of peasant farmer households taken from an urbar of the monastery of Stams, see: StiA Stams, Urbar III/1.

Having difficulties in paying rents on time happened quite often. In the local courts, arrears of rent payments (versezzen zins) were claimed regularly. [32] In November 1357, Ludwicus and his wife Agnes of Meran promised to pay their landlord, the knight Bertholdus, 30 lb. for rent arrears (occasione retenti census nondum sibi dare) in wine during the next vintage season. [33] Larger rent arrears were paid in instalments. On 26th May 1400, Georius textor (a weaver) und his wife Diemundis promised to pay rent to two brothers, Ambrosius and Bartholomeus (amounting to 11 mr. 8 lb. and 6 gr.), that was to be paid to the lord of Starkenberg (pro censu de domino de Starkenberg). [34] Georius and Diemundis were probably subtenants of the two brothers who themselves owed the rent to the Lord of Starkenberg. The debtors were to pay 30 lb. annually at the fair of Saint Martin until the debt was repaid. They also had to pledge a plot of land and a pasture as security. The debt obligation was registered before a notary.

Recent research has highlighted the existence of factor markets and commercial dealings in medieval Tirol. [35] Signs of rural commercialisation, such as the monetisation of rents, the increasing incidence of wage labour or higher levels of market activity, can be observed in Tirol from the 13th century onwards. [36] In a society that had been forced into a great deal of market involvement, such as 14th century Tirol or southwestern Germany, access to capital could decide economic survival. [37] This was not least because of what Shami Ghosh called a growing social dependence on the market: more people relied on monetary assets for social reproduction – that is, to maintain their social status – through consumption, dowry payments or inheritance. Peasants needed money to maintain access to their holdings, in order to pay both rents and taxes, to pay off debts for inheriting the land or to make settlements between generations. [38] This was also the case for medieval and early modern Tirol. [39]

The family or lifecycle also involved systematic constellations like marriage, life with or without children or retirement, that involved specific transactions. [40] For example, in the event of marriage, financial matters (dowry payments, morning gift) had to be settled in cash or, more frequently, by pledging property. Here, the different assets that each of the spouses brought into marriage were documented and safeguarded. It was common practice in Tirol that the husband secured both the morning gift (donatio ante nuptias, morgengabe) as well as the dowry of his wife (dos, haimsteuer) by providing some property as security. [41] The dowry and the morning gift formed separate estates and as such were to be managed separately by the household. In most cases, these sums were not to be paid in cash but were placed as mortgages on properties. [42] However, they had to be paid out in the event of a claim or the death of one of the spouses. Several cases put forth before the courts in the district of Meran prove that dowry and morning gift payments were actually demanded and had to be paid out. [43] In other cases, wives agreed in their wills to waive payments of the morning gift. [44]

These special assets brought into a marriage were also invested and used to generate income. In a contract from January 1357 between Chuenradus dictus Zobel and his wife Cylie, it was agreed that the dowry and morning gift were to be safeguarded as a pledge by Chuenradus and would be paid out in full and undiminished if required. As usual, a special clause in the contract indicated that the interim usufruct, which Cylie or her heirs would receive as capital in the meantime, were not to be deducted from the total sum. [45] Consequently, the marital assets were invested in land or profitable businesses.

Other lifecycle phases include, for example, income losses in households during periods when young children are being brought up or when providing care for the elderly. It has been shown in quantitative research that rural family farm households reacted to the presence of young children or non-working elderly and tried to compensate for these cost and human capital burdens with additional resources (land, capital) or extra labour. [46] As the farms were very labour-intensive, these temporary losses of work had to be compensated for. Studies on the later period suggest that the actual practices depended, among other things, on the respective inheritance law (division of property (Realteilung) or impartible succession (Anerbenrecht)). [47] In any case, financial resources would have been needed to compensate for the loss of labour force by paying wage labourers or saving for retirement.

If no one was there to compensate for the labour, things could end badly for the household. This was the case in February 1389 when the landlord Ludwig auz der Awen claimed rent arrears from one of his tenants, a woman called Grumserin. [48] Said woman was living off a manor called ze Grumse. In the summer of 1388, she was already in financial difficulties when several people claimed unpaid debts from her before the court. [49] Six months later, she was called to court again. There it was decided that she should consult with her and her children’s relatives and appoint a guardian (gerhab) for her underage child. The guardian should help her to run the farm and help to pay the rent. The final decision of the court, that was to have taken place two weeks later, is unfortunately not documented. In the meantime, the Grumserin was expected to do as she was instructed and was allowed to obtain necessary foodstuffs from the farm on condition that she did not diminish the farm’s value. There is no mention of a husband, who was either dead or had left the household, leaving the family with little means to maintain the homestead. In this case, a network of relatives or friends was necessary to support the family and help them to pay off debts and provide for their livelihood.

Other major costs were connected to the education and training of children. On 26th February 1357, Chuenradus, who was the cleric (pastor) in Latsch, received the sum of 53 lb. (636 gr.) on behalf of the underage children of the deceased Hainricus dicti Chrophlun from the widow. [50] The children were apparently Hainrich’s children from a previous marriage and Stine was their stepmother – at least she is not referred to as the children’s mother in the contract that was drawn up with the cleric. He, as a good friend of the children (melior amicus predictorum puerorum), pledged a rent of 5.5 modios of rye to Stine for the money received. [51] The rent stemmed from a field that was cultivated by a certain Ulricus and could be redeemed every year at Christmas by the boys or their procurators. The contract states rather vaguely that the pledge of the rent was made to the benefit of the upbringing and education of the children. [52] The children’s upbringing was thus associated with considerable costs.

Inheriting land or taking over a farmstead was also connected to financial burdens. A series of legal contracts from Meran registered by the notary Cristanus de Eppiano from April 1406 enables a glimpse into these practices. On 24th April 1406, Hainricus in Grübe, a farmer, decided to retire and settle his affairs. [53] He cultivated half a manor (media curia), the Prünsthof in Telle (in the parish of Schenna, some 15 km away from Meran). With the consent of his sons Chunrad, Iacob and Iaklin, he bequeathed his rights over half of the farmstead with all associated land and rights to another son, Ulric. In return, Ulric had to pay out his brothers by paying each of them ten lb. to redeem their inheritance rights. His father was to receive four staria of rye, one starium of wheat and one starium of barley annually as long as he would live. [54] The next entry made on the same date in the notary register is a contract of sale. Here, the brothers Ulric, Iacob and Iaklin sold their rights to the other part of the farmstead in Telle, to their brother Chunrad for 30 lb. [55] Chunrad was to possess half of the manor with all its possessions freely, on condition that he respected and paid the landlord’s levies (census domini). Finally, a third contract was recorded by the notary that safeguarded the payment of the sale. [56] Chunrad promised to pay his brothers Iacob and Iaklin 20 lb. for the aforementioned farmstead. Iacob was to receive his ten lb. within five years from the coming Pentecost, while Iaklin was to receive his share of ten lb. only after six years. No payment had to be made to the third brother Ulric because his share was offset against the inheritance of the other half of the manor.

This example shows how much money was needed to settle the inheritance affairs for a single farmstead: the father had to be taken care of and the two yielding brothers that did not receive any property, Iacob and Iaklin, had to be paid out. The payment of the modest sum of 20 lb. (approximately 30 day’s wages of a skilled craftsman) was stretched over a period of more than six years. Given that each of the four brothers’ share of half the manor was worth ten lb., the total value of the estate can be estimated at around 80 lb. Volker Stamm has pointed out that a rent-price relation of 1 to 10 for agricultural goods seems to have been the norm in medieval Tirol. [57] In this case, the Prünsthof would be economically able to pay a rent of eight lb. (not to be confused with the overall agricultural output). Chunrad had to pay out the yielding heirs with the production of only half of the manor and thus a payment period of around six years seems realistic.

Some of the consumption went beyond covering more basic needs and involved luxury spending – this was mainly the case for higher social classes. A vivid example of the consumption of the upper classes can be found in a charter from 1421. In April of that year, Alphart Goldecker, as guardian (gerhab) for two boys, Balthisar and Sigmund, settled a debt of their deceased brother Caspar in Meran. [58] The latter owed Jacob dem Pfisel of Bozen 8 mr. 2 lb. and 9 gr. for drapery. Another item of debt was the material for an extravagantly designed wedding dress, consisting of drapery and a fur coat (ayn vehrueckeine kürsen, daraus man ir yetzund gemacht hat ir prautgewant) of the boys’ sister Agnes. Altogether the debt totalled 22.5 mr. For this sum, the guardian gave the creditor a perpetual rent of 15 lb., stemming from one manor that was owned by the boys. Social distinction through clothing (fur on the dress) and the large sums of money involved illustrate that the upper classes already indulged in conspicuous consumption.

Apart from such social and economic pressures, wealthy peasants, burghers and minor nobles in Tirol invested their capital in leases, vineyards or houses that provided them with a regular income that far exceeded their economic needs. [59] Funds were needed to take over inherited properties and to cover related costs. There was even an active pursuit of profit in certain upper-class peasant families. The subsistence and non-subsistence consumption of peasants resulted in the need to acquire or save money, which again was spent to acquire foodstuff or artisanal products. [60] Thus, the consumption of large parts of the population was of great economic importance.

4 Financial Instruments Available for Saving, Investing and Acquiring Cash

In this section, the different tools available in medieval Tirol for saving, investing and acquiring money are described. Saving here means keeping money safe, so that it is available when needed, which usually involves little risk. Investing does involve risk, but also the potential for higher returns. Investing is usually associated with a long-term horizon, such as preparing for retirement. In both instances, the ability to convert money into cash – and thus maintain liquidity – is important.

Wealth was the decisive factor in deciding how someone saved or invested money. This is due to two reasons: Firstly, poor and rich households had different demands. The major concern of the poor was not to save for the future, but to maintain cash flow in the present. [61] Therefore, poor households resorted to different methods and most of all wanted liquidity, that is the possibility of converting their assets back into cash at low cost and short notice. [62] Secondly, land-poor households were to a large extent excluded from the formal credit market since they lacked security which could be mortgaged in exchange for credit. [63] In contrast, wealthier households had easy access to credit by mortgaging their property.

Before the emergence of insurance and modern capital markets, households had to resort to other ways to ensure a flow of capital or to save money for hardships. [64] For example peasant households depended upon internal transfers, having to resort more often to financial services within their social networks consisting of neighbours or relatives, where money was lent (with or without interest). [65] Although this sector of the medieval economy is difficult to reconstruct, an analysis of the court records of Meran (1388–1391) suggests that there was a lively informal small-scale credit market, the majority of which was conducted orally. [66] This need for informal credit must be understood against the backdrop of slim profit margins in agriculture, seasonal working patterns creating a volatile household income over the year, or the payment of wages in kind. [67] Payments in kind increased the need to raise cash from other sources to pay monetised levies such as taxes. Table 4 provides a schematic depiction of the assets and financial instruments used for acquiring cash or saving money recorded by the selected notaries. Borrowing within family or neighbourhood circles was not recorded by them, so the list is not exhaustive. Not all methods were suitable for saving or investing money or providing needy people with cash and vice versa. The choice of financial instrument depended on the specific need, the age or lifecycle status of those involved, the risk affinity and personal preferences of the people living in the household, as well as on the overall economic conditions. It can also be assumed that people (then as now) used a variety of financial instruments, some of which were riskier, others less risky, some very liquid and others less liquid.

Financial Instruments and their advantages for investment and loan purposes in medieval Tirol.

| Financial instrument Saving Cash | Prerequisites None | Liquidity requirements High | Investment None | Credit None | Costs/Return (in percent) (-5) | Disadvantages Inflation |

|---|---|---|---|---|---|---|

| Pawnbroking | None | High | None | Yes | 1.6 (per week) | High interest |

| Crops (selling on credit) | Access to agricultural land | Medium | None | Yes | None | Volatile prices |

| Annuities and Rents | Collateral (Real Estate) | Medium | Yes | Yes | 7-10 (per year) | Collateral needed |

| Real Estate | Real Estate | Low | Yes | Yes | 4-5 (per year) | Low liquidity |

| Sharecropping | None | Low | Yes | Yes | None | Labour force is tied down |

Source: StA Meran, NI 3; NI 22; NI 23; NI 30; GP 1.

In Tirol, markets for land and capital had already emerged in the 13th century, so people had experience with this sort of investing and trading. Data from 13th century Tirol suggests that the volume of markets for capital and real estate was already quite sizable; in Bozen at least 10 percent of the available assets flowed annually into the property and land market. [68] This means that there were ample possibilities for households to invest in the market and to adjust their portfolios to their specific needs. People could choose to be more or less marketoriented and resort to the financial strategy of their choice. The rest of this section will focus on analysing the variety of financial instruments used in Medieval Tirol.

4.1 Saving Cash

The easiest way of saving money was hoarding coins as cash. By the 14th century, the monetary economy was widely spread in Tirol, and coins became steadily more abundant and accepted in the countryside. [69] However, hoarding could be risky, money could be stolen and in times of inflation, saving cash could result in losses. [70] Mentions of cash savings are rare and we are usually only informed about cash hoarding in connection with specific events (marriage, drawing up of testaments, death). In the will of the baker Chunradus dictus Scholentrit of Meran, it was emphasised that he had not inherited anything from his parents but had earned everything he owned himself together with his wife. [71] He bequeathed several items to his son and organised the financial affairs in the event of the latter’s death during his minority. The testament states that Chunradus kept large amounts of cash, namely 106 ducats (gold coins) and 14 mr. in other coins (totalling 6,026 gr.), as well as four barrels of wine (carradas) in his house and cellar. [72] This was an enormous sum, equivalent to more than 753 days’ wages for a skilled labourer. This case illustrates the practice of saving cash, but also of using objects as storage of value. [73]

It is hard to say how much cash on average was stored in households in medieval Tirol. Various sources suggest that loans, artisanal products and rents were paid with coins, but the medieval economy worked on credit to a large extent. When households bought on a scale too small for the use of coins, when grain for nutrition or sowing was needed in advance of harvests, or when payments for a dowry were to be prepared, credit was the solution. [74] When there were no cash savings, possessions could be converted into liquid funds by pawnbroking.

4.2 Pawnbroking

Pawnbroking was an easy way to obtain cash at short notice. All households owned something that could be pledged, such as precious objects, clothing or linens, working tools or livestock. Money could be acquired both by pledging objects as collateral for future payments to the business partner or by using the services of professional pawnbrokers. In the latter case, these were the operators of pawnbroking houses, so-called casanas that existed in several villages and cities in the County of Tirol. [75] These institutions were leased out by the sovereign against an annual leasehold. In return, the pawnbrokers or money lenders were allowed to grant interest-bearing loans against pledges. These professional moneylenders offered credit but charged up to two den. per pound and week (=240 den.), which is equal to 1.6 percent per week (or 86.6 percent per annum). [76] However, the calculation of the interest rate on a weekly basis hints at a rather short runtime, probably between three and six months. [77] The casanas accepted all kinds of pawns, from textiles to wine, and in one exceptional case even a house was pawned. [78] Unlike in other parts of Europe, the moneylenders did not accept deposits from customers and therefore did not function as savings banks. [79] Thus, they seem to have been mostly credit institutions. The clients of the casanas were not the poorest part of the population but rather people of the urban middle class like artisans and merchants. [80]

Although the comital casanas had the absolute monopoly of lending against interest in their cities, as was confirmed to them in various official statements of privilege, pawnbroking was a widespread practice. Besides the option to resort to the services of professional moneylenders, there was also the possibility to obtain credit through the pledging of goods. Such non-professional pawnbroking, that is pawnbroking without charging (visible) interest, was omnipresent in medieval Tirol. [81]

The practice of pawnbroking in Meran is of special interest here: besides private moneylending secured with pledged items, there was also the possibility to deposit pawns as security in court. If the debtor failed to repay the loan, the creditor could claim the pledged goods in court. The city of Meran was seat of the provincial and urban court (Land- und Stadtgericht) of the provincial district (the so-called Burggrafenamt). [82] It was common practice to pledge items as collateral in court for loans or deferred payments. [83] In Meran and also in some other cities in the 14th century, there existed the office of veilträger, who was responsible for the correct selling of pawned items. [84] His main purpose was to prevent the unauthorised seizure of goods at the market or at court. He was responsible for the seizure, he took care of the pledged items (which could even include animals), organised the auctioning of the goods and ensured payment to all parties involved. In 1337, an addendum to the city book (Stadtbuch) of Meran specified the rules governing the exercise of this office. Although the veilträger per se did not grant any loans and therefore did not charge any interest, he was entitled to remuneration for his services. The veilträger was allowed to keep a certain amount of money from the auctioned items for himself.

The court protocols and the city book inform us about this practice in more detail: In a first step, several respectable citizens of Meran estimated the value of the pledged items. [85] Then, the pawns could either be released within a certain time by the debtor or, if not, were publicly auctioned. In both cases, the veilträger was rewarded. People pledged all kinds of items including foodstuffs, wine or textiles. The statutes mention the following animals being pawned: horses, stallions, cows, oxen, sheep, goats or pigs. The service charged depended on the type of the pledge and if the item was auctioned or released by the debtor. The transaction costs were on average between 8 and 16 percent, as the lump sums for goods worth more or less than one mr. show. The animals, here so-called eating pledges (ezzendiu pfand), probably caused higher transaction costs because they had to be fed and cared for. Depending on the principal and the items pledged, the transaction costs were between 10 gr. and 60 gr. In general, pawnbroking provided easy access to liquidity against the risk of losing necessary items if they could not be redeemed. [86]

4.3 Selling Crops Before Harvest and Using Crops as Means Of Payment

As recently has been pointed out by Mathieu Arnoux, in a society where crops were an essential part of value and exchange, they have to be included in economic considerations. [87] Besides the circulation of money and monetary exchange, crops were important in two different ways to promote economic exchange: Firstly, they could be bought, sold or traded in form of annuities (see below), and secondly, harvested crops like grain or wine could be used as a means of payment, sometimes at a fixed price even before the harvest was brought in. [88]

Payment with wine due during the upcoming harvest enabled peasants to have easy access to credit for consumption and investments, as numerous cases show. On 8th January 1400, Petrus de Vial from Kaltern promised a certain Egno Carpentarius and his wife seven mr. for salt and grain. He promised to pay with five carrada of wine during the upcoming harvest from his vineyard called Wolfernai. If the delivered wine should be worth more than the seven mr., the creditors would refund the surplus. In the event that the wine would be worth less, the debtor must deliver good wine up to the value of the shortfall. Should there not be enough wine at Wolfernai, Petrus would be obliged to supply wine from other estates, provided its good quality. If, for any reason, no wine should grow at all, the debtor would be obliged to refund the total amount without delay or damage. [89] Other examples of this practice were recorded in the same year. On 20th November 1400, Jacob Rauch and his wife bought drapery for 10 mr. and 8 lb. on credit and promised to pay for it at the next Candlemas in Imst with good wine instead of cash (“cum bono vino kaufmansguͦt an beraiter phening stat”). [90] Each contracting party could appoint two arbitrators to determine the quality and price of the wine. In the event of disagreement over the price, a fifth arbitrator should be called in. In another contract from 8th December 1400, Hainricus Kastraͤunel promised to pay Jodocus Segger the sum of 13 lb. for grain, to be paid in wine from the upcoming harvest. [91] Again, the price was to be decided by two men, one appointed by each of the contracting parties. On 6th December 1406, Nicolaus dictus Wett de Sancto Antonio from Kaltern promised to pay the notary Thomas the price for 20 staria of rye and for 18 cheeses. The goods were to be paid in wine during the next vintage for the usual price (“vinum secundum commune cursum in Caldario ut emitur et venditur”). [92] Similar cases are recorded for the village of Laas in 1391. [93]

The practice of paying in wine was widespread. [94] Selling their produce before the harvest enabled the peasants access to money that could be used for further investments or to obtain necessary goods such as grain or salt. [95] These contracts guaranteed fair prices for both parties at the usual market value. The wine was sold during the grape harvest, when supply was at its highest, and it was sold on the market or in the presence of specially designated intermediaries, ensuring conformity of the quality and price of the product. [96] The very precise framework in which the price of the produce was calculated suggests there was a functioning product market in Tirol where supply, demand and quality determined the price. This is confirmed by the city charter of Meran from 1317, which stipulated that the quality and price of wine sold in the city was to be estimated by four citizens. Grain was also to be sold exclusively at the Meran corn market. [97] This way, information asymmetry concerning quality and prices was reduced. Contracts where wine or grain were sold at the ceiling price before the harvest can be interpreted as short-term credit contracts of a speculative nature. [98] It is striking that in many of the contracts, foodstuff (rye, salt, cheese) was bought on credit. This indicates that selling crops before the harvest was a common way to obtain liquidity to buy food during the wintertime.

4.4 Annuities and Rents

The selling of annuities and rents (renten) was the most widely used credit instrument in rural areas. [99] Buying annuities was a profitable investment and by the 13th and 14th centuries, a considerable part of Tirolean society was active on the land and capital market. [100] Rising prices for agricultural produce and advances in productivity in the early 14th century, albeit at a low level, created the economic preconditions for the sale of annuities. [101]

Anyone who owned arable agricultural land or town property could extract regular income in kind or money from it, or sell it. As annuities were a purchase and not a loan (or titulus mutui) in the legal sense, the interest on these loan transactions was also unproblematic under usury law. With the purchase of an annuity, the buyer (creditor) acquired the right to receive an annuity (redditus, fictum), which was to be paid regularly in a fixed amount (in cash or in kind) for a certain purchase price and which was placed on a property as an encumbrance. Since annuities were created as a burden in rem on real estate, the peasants’ power of disposal over the land was a legal prerequisite for the sale of annuities. These rights were open to the owners and by the 14th century, the peasants had also acquired the corresponding rights to the hereditary estates (Erbleihegüter) in Tirol. [102] The majority of interest rates were between 4 and 15 percent per annum (much lower than for cash loans). The usual purchase price of an annuity was about ten times the annual payment. [103]

The annuities sold were in most cases redeemable. This was indicated by an addendum at the end of the contract or in an extra entry, depending on the habits of the notary, where it was stated that the seller (debtor) received a contract (carta redimendi, carta revendicionis) that granted the seller and his heirs a right of repurchase. This could be perpetual or limited in time. The limited runtime was usually between one and six years. Sometimes it was contracted that the rent could not be redeemed before a certain date. [104] This was probably done to guarantee the buyer a certain minimum income from the transaction. However, in most cases, the annuity could be redeemed during one of the regular dates of payment for levies (usually Candlemas, vintage time, Michaelmas, Martinmas, Galli or Andrei) or during one of the annual fairs of Meran (Pentecost or Martinmas). Whether the debtor received limited or perpetual rights of redemption seems not to have influenced the interest rate. [105] The annuities sold consisted of payments in coin or in kind, where wine and grain were the most important products. As has been shown above, payments in kind were highly regulated, which made the marketing of rent payments in kind uncomplicated and widespread. The preference for annuities of a specific size indicates that there was a well-structured market for annuities that enabled buyers to easily evaluate the financial instruments. [106]

The rent payment could stem either from the property cultivated by the seller himself or from another right of income owned by the seller, e.g. a plot of land possessed by the seller but leased out to another person. In the latter case, the person cultivating the land had to pay his rent to the owner of the rent or annuity. It must be pointed out that the levies for hereditary leases were fixed and could not be increased unilaterally by the landlord. Therefore, landowners could not generate more levies (or new annuities) from already leased out properties. [107] However, it was possible for tenant farmers with hereditary tenure (Erbleihe), who were perhaps in acute financial need, to create additional annuities in order to sell them immediately. Below are some examples of typical rent or annuity transactions.

On 6th May 1372, Jaeclinus and his wife, Elspeta, received a vineyard called ze spitz from Laurencius Treipgazzer as hereditary leasehold for an annual rent of two urns of wine. [108] In another contract, the married couple sold a perpetual rent of four urns of wine, payable from the vineyard ze spitz, for 8 mr. to Laurencius Treipgazzer. [109] A total rent of six urns of wine was imposed on the vineyard. The rent could be redeemed within four years for the aforementioned price.

The leaseholders of hereditary tenures were free to create new annuities from the land they cultivated. Annuities were also transferable and could be sold and resold, so liquidity was reasonable. They could also be used as collateral for obtaining credit. [110] One of the dangers of investing in annuities was that they would suffer from inflation. For this reason, some contracts specified which coins were acceptable at which exchange rate for the redemption of the annuity. [111]

There were some limits on how many annuities could be created. In one contract from 10th March 1398, a certain Paulus sold an annuity of 17 lb. for 17 mr. to Johannes Ganthaler. The annuity was perpetually redeemable. Besides, it was stipulated in the contract that the debtor henceforth had no power to sell further annuities without the knowledge and consent of said buyer and his heirs. [112] This measure was probably intended to prevent the seller of the annuity from becoming over-indebted, which would reduce his ability to pay. While selling annuities was an easy way to gain credit, the burden of the annuities could quickly become oppressive due to changing economic developments.

For investors, annuities were attractive and open to anyone who had some capital available. They offered an annual income of around 10 percent of the principal sum and could be sold on a secondary market. Examples from the late 14th and early 15th century, such as Ursula Rittner, widow of the late notary Michel Rittner from Bozen, and her sister Elisabet, demonstrate that investors actively managed their assets. They usually owned real property that was cultivated by themselves, leased out some property against rents, and also owned annuities. [113] Investments in annuities granted a regular income that could be used for raising small children, [114] for donations to monasteries [115] or for the provision of daughters. [116] For example, Johannes dicti Rumetzer, judge of Meran, donated an annuity of 20 lb. to the nunnery in Stainach. In return, the prioress and her convent promised to accept his daughter, Dymlina, into the monastery. This ensured that the daughter would be able to live according to rank.

4.5 Real Estate

Real estate was the most obvious type of investment. Houses and agricultural lands were a safe investment, yielding an annual profit of between 5 to 10 percent. [117] Vineyards, manors or fields could either be cultivated or leased out. In the second case, the owner would avoid the labour-intensive cultivation and maintenance of the property and the related costs. Besides, property could act as a store of value and, if necessary, be mortgaged or used as collateral. This was very often the case when dowry payments or the morning gift were transferred to the spouse, and instead of a cash payment, both parties agreed that the payment was secured by real estate. Liquidity of real estate was not very high because if someone wanted to sell a plot of land, it was unlikely that a buyer would be found at short notice. This disadvantage could be minimised if the property was not sold directly but was provided as collateral for a loan. [118] It is important to point out that markets for land had become established by the later Middle Ages in Tirol, and by the end of the 14th century, people had ample experience in selling, buying and mortgaging land. [119] There was a strong institutional framework protecting the ownership rights and titles of both land owners and creditors. [120]

Ownership of even the smallest plots of arable land (meadows, vineyards, orchards, fields) enabled access to credit. Owning land was widespread, and the property structure was more flexible than the older historiography suggested. [121] In addition to full farmers, who owned entire manors and were allowed to participate in the common rights of the commune, there was the sub-peasant strata, which included farm hands or artisans, with ownership of small pieces of real estate. Very often, belonging to the landless group of farm hands was an age-dependent transitory stage. Those initially landless could acquire land through tenancy or other ways. [122] This is reflected in sources about the land and credit market.

Especially in the countryside, most contracts dealing with mortgaging, selling or pawning of real estate are connected to plots of land of rather low value. In the notary register of Jakob for the village of Laas for the year 1391, the median value of real estate sold or pledged was 315 gr. or roughly 40 daily wages of a skilled labourer (the mean being 521 gr., with a total sum of 26,034 gr.). [123] Many artisans or farmhands owned small plots of real estate. These properties were used as collateral for all kind of contracts, even small purchases. This was the case on 7th March 1357, when a certain dominus Prandlinus confessed that he owed 10 l. (120 gr.) to Ulinus, calciator (shoemaker), for shoes he had bought from him. For this he pledged a small field (agellum) to the shoemaker that could be redeemed every Michaelmas. [124]

Houses and property were, like today, a good investment for old age and retirement. There are several cases where a married couple handed over their estate to their heirs in return for the lifelong right to residence and support. [125] An interesting case is that of the shoemaker Hainricus and his wife Geysula. [126] The couple gave all of their property, which consisted of a house, two vineyards and two fields which they held as hereditary tenure, to another married couple, Hainricus and Agnes. All of them were liable to pay rents and belonged to the monastery of Wilten. The monastery as landlord agreed to the change of the leaseholders, and the new tenants, Hainricus and Agnes, promised to cultivate and maintain the property and to pay the rent. The senior couple was to receive food and appropriate clothing, and they should be treated according to their needs with piety and kindness by the younger tenants. The parties agreed to observe the terms and conditions, and conflicts were to be resolved before a court of arbitration. This ensured the older couple’s livelihood even after they were no longer able to work. Whether the two couples were related is not known. In another contract, Wolflin, as guardian of the children Clara and Henslinus, leased a house in Meran to Chuenrad and his wife Agnes for five years for an annual rent of eight mr. [127] It was also stipulated that if during these five years one of the owners (the landlords) should become engaged or if the new parents-in-law should want to live in the house, then the tenants must leave the house. In other words, the landlords could claim their personal needs. Here, the house was used both as an investment and later as a living space.

4.6 Sharecropping

Another investment tool available in medieval Tirol was sharecropping. Although not a typical financial instrument, this type of contract offered investment opportunities for people without assets or collateral. The rural capital market was tightly connected to the land market, and those who did not own real estate were left behind. [128] This meant that they had to resort to other credit intermediaries such as pawnbrokers, who often charged high interest rates.

An alternative way to obtain capital was through sharecropping, where landowners provided capital in the form of farmland, cash, seed or tools. [129] The tenants (or debtors) received working capital and in return paid the landowners back with their labour in the form of a share of the harvest. In Tirol, this type of contract was used almost exclusively in labour-intensive viticulture, where the tenants usually paid half the harvest (medium vinum, halber wein) as rent, in addition to other small levies. [130] This contract was both an investment (through the capital input of the investors or landowners) and a loan (through the acquisition of working capital, which was repaid by the creditors or tenants with labour input). [131] In many cases, the tenants received a levy-free piece of land for their own use next to the vineyards, from which they had to pay half of the yield. Landowners could thus use the contracts for improving some of their land. Below are some examples of sharecropping contracts.

On 6th March 1357, two landowners, Dyepoldus dictus Hael and dominus Bertholdus dictus Stofler (together with his wife), leased their co-owned manor called Schalayrhof as a hereditary leasehold to a woman, Grete, and her son-inlaw Hainricus. [132] The new tenants had to pay only one lb. (that is 12 gr.) rent for the first two years. In return, they had to plant two vineyards and build a winepress at their own expenses. In addition, they were obliged to carry out all regular farm work (tamping, tying, digging, cutting foliage, bringing in the grape harvest, pressing) at their own expense. At harvest time, they had to deliver half of the wine that would grow on the manor, and one yhre of the common wine for the provost of the landlords (that is, a labourer sent to supervise the grape harvest). [133] They must also feed the provost, a farm labourer, and a horse until the wine was harvested and pressed. The tenants gained working capital. In the first two years, they invested labour and then could start harvesting and selling wine on their own account. They themselves only had to provide the manpower for the labour-intensive activities. In another contract from 1357, a notary called Hainricus de Epyano leased out a vineyard as hereditary tenure to a certain Bertholdus and his wife Stine for an annual rent of seven lb. at the common conditions (that is for half of the yield, including costs for harvest and delivery of the grapes to the winepress). [134] They also promised to plant new vines as stipulated. Finally, the tenants received 30 lb. for improving the vineyard (pro melioracione). They received 30 lb. on condition that they could relinquish the estate to the landlord within eight years and repay the 30 lb. However, if they did not return the estates, they could retain the leasehold and were not obliged to repay the 30 lb. This favourable contract from 1357 might be connected to the events of the Black Death and a possible scarcity of labourers. Thus, the tenants acquired capital worth 30 lb. to make investments.

By signing sharecropping contracts, peasants were able to obtain working capital for the sole use of labour and manpower. However, due to the labourintensive work, they were unable to sell their labour outside their farms, thus also limiting their economic capacity. [135]

5 General Trends of Saving and Investing in Medieval Tirol

Practices of saving and investing in Tirol were complex, and households were in many ways economically and socially entangled. A recurring topic is the transfer of property and assets at certain stages of life, such as at weddings or as inheritances. Cash savings, labour input, credit and real estate were used in different combinations. Some more examples from the sources will be provided here to show just such complexities and combinations, as well as other common factors that affected financial transactions.

In July 1357, domina Luitgardis donated to her husband, Bertholdus, all of her goods and provided insight into her economic life. [136] She probably did this because of the support her husband provided during their marriage. The contract stated that she made the donation because Bertholdus brought into the marriage, besides several estates, ten mr. that he used to pay off her debts and to work her land, which he did reliably, according to the contract. Here, different financial instruments and assets (saving, real estate, input of additional labour force) were combined. While the sources often mention the dowry, the settling of debts or the donation at the end of a person’s life separately, the combination of different types of financial instruments seems to have been the norm rather than the exception.

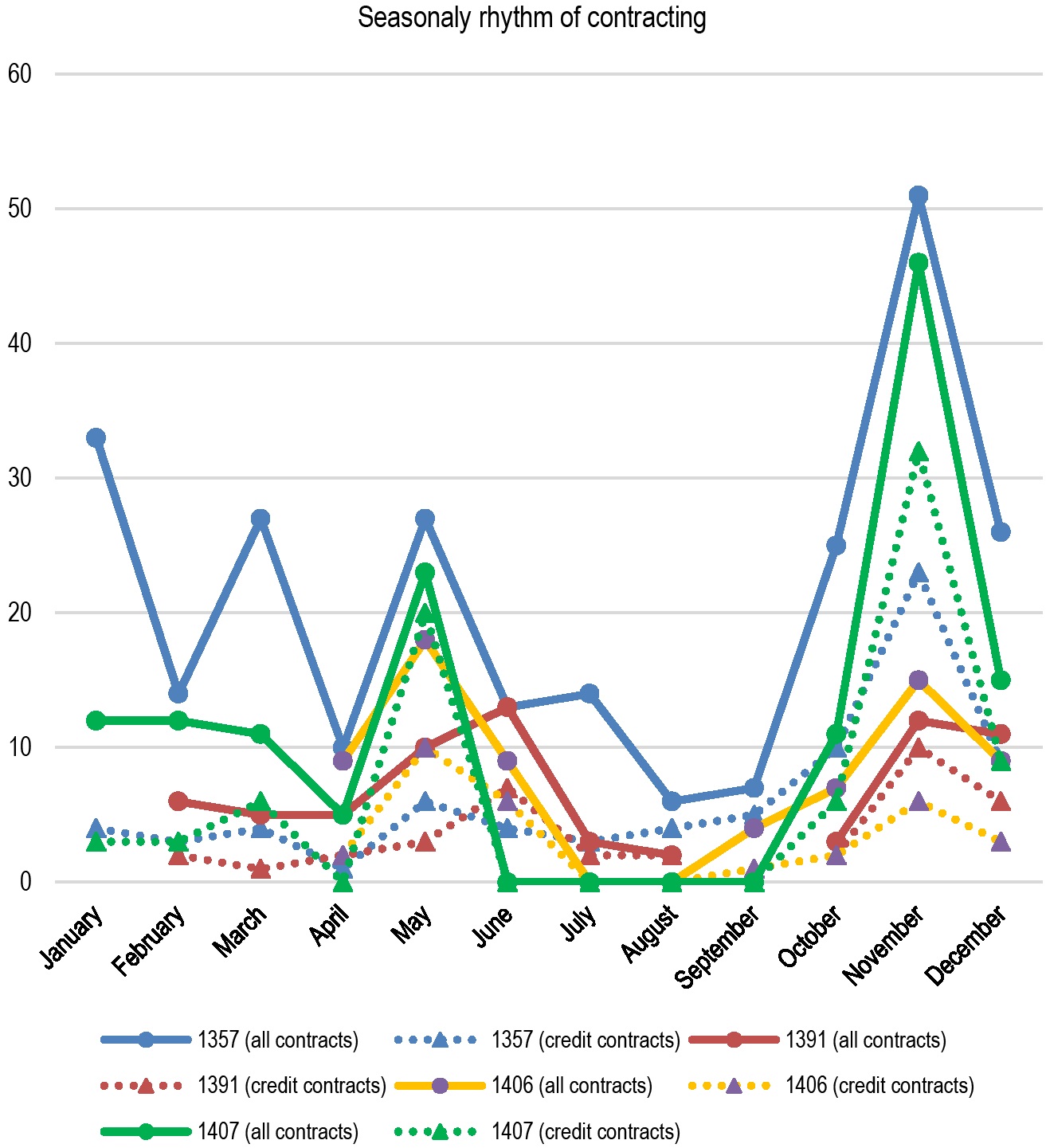

Another visible characteristic of economic behaviour was the impact of the seasonal rhythm of the financial market. Figure 1 shows the number of contracts and the respective number of credit transactions recorded by the notaries Konrad von Alerheim (1357), Jakob von Laas (1391) and Christianus de Eppiano (1406/07) per month and the result shows a strong correlation to the farming calendar.

Seasonality of financial contracts in Medieval Tirol as recorded by selected notaries per month (1357 to 1407). Source: StA Meran, NI 3 (1357); Ni 22 (1391); NI 30 (1406/07).

There was a strong seasonality of the credit market with two peaks: The early peak of credit activity during the first half of the year is due to investments in agriculture. [137] The rise in May is connected to the annual Pentecost fair of Meran, which took place during this month in the respective years. In the summer, credit activity declined and came nearly to standstill before it rose again during harvest and vintage time. In October and November, most of the rents had to be paid, and grain had to be bought to stock up for the winter and for sowing. This explains the second peak of credit activity during the calendar year. The fairs were important payment dates. In addition, at the Pentecost and Martini fairs, goods could be sold or bought, cash was exchanged, and merchants and moneylenders offered their financial services. [138] Crops and wine sold on credit before the harvest were to be delivered.

As can be seen, this rhythm of financial activity remained rather stable over several decades. This seasonality stems from the fact that most of those involved in the credit market worked in the region’s dominant economic activity, that is, agriculture. Peasants were the dominant borrowing group, and they imparted their seasonality on all lending groups. The heavy borrowing during October and November was possible because other groups, whose economic activities were not fully entangled with agriculture, were willing to engage in the rural capital market. [139] The rural and urban capital markets were closely connected and people from Meran invested in the countryside and vice versa.

The data shows that an increasing number of people were involved in the capital and land market. In many cases, households – these could include married couples with or without children, stepchildren, guardians, or other relatives – appear as groups of people in the transactions. This may be attributed to the makeup of landholdings that were owned mostly by groups of relatives. Shares in a sixth or a quarter of a property were not uncommon. Numerous contracts involved cessions, waivers and sales of inheritance rights to relatives. Groups of people who were not related to each other and who jointly acquired property as an investment by pooling their resources were only rarely mentioned in the sources. [140]

The majority of people appear only once in the selected sample, suggesting that for many people a capital or property transaction was a rare affair. However, some individuals such as Cristanus de Swinsteg from St. Leonhard were vividly engaged. Cristanus de Swinsteg owned property in Riffian and St. Leonhard (Passeier Valley). On 26th February 1357, he leased out a vineyard in Riffian and a manor in St. Leonhard. [141] On the same day, he sold an annuity of grain for 12 mr. (1,440 gr.) with the right to redeem it. In June of that year, he sold another redeemable annuity of 5 lb. stemming from a house in St. Martin (also in Passeier Valley). [142] Five months later, he bought a redeemable annuity consisting of one carrada of wine from Chuenradus dictus Traechke for 14 mr. (1,680 gr.) from a vineyard in Algund. [143] Cristanus also bought and sold annuities, depending on economic preferences. [144] He invested the profits from his agricultural activities to build a portfolio of annuities and agricultural land in Passeier Valley and the surrounding area (all within around 35 km from St. Leonhard where he apparently lived). In addition, he used his property to acquire loans by selling annuities from it. He reinvested the capital in other investments. In this single notarial register, Cristanus appears as an investor five times in one year. This example suggests that there was a vivid local land market. Cristanus both sold and bought annuities, making him a debtor and creditor at the same time. However, his economic position enabled him to redeem the annuities sold and he therefore only paid a manageable amount of interest in absolute terms. For him, real estate and annuities were a good investment tool. However, there were few cases of people like Cristanus de Swinsteg owning such large portfolios of property. The majority of people mentioned in the notarial records seem to have made only one or two transactions a year.

People with smaller economic means had to resort to selling annuities to obtain credit and were often unable to redeem them for a long time. As a result, these people were burdened with additional levies, which were difficult to pay due to the low profit margins in agriculture. Annuities also had the drawback that they could not be converted back into cash at short notice. For such purposes, other instruments such as pawnbroking or selling the harvest on credit were more suitable. Thus, households had to and could resort to many different options of saving, investing or acquiring money.

6 Conclusion

Although sources are scarce, the study of the notary registers and court records allows valuable insight into the investment and saving strategies of individuals and households in medieval Tirol. It is possible to draw four main conclusions from this analysis.

1. Evidence from the second half of the 14th century suggests that households used a combination of different financial tools for saving money or overcoming economic hardships. The question of purpose is essential because while some forms of investment were geared towards profit, others were better suited to bridge cash shortages or acquiring working capital. The use of different financial instruments was complementary and not mutually exclusive.

2. Family relations mattered, both for financial support as well as for financial obligations. On the one hand, the family was one of the first places to go for support and help. In addition, the pooling of economic resources within households enabled investment and social advancement, for example by allowing appropriate dowry payments to be made. On the other hand, family matters were strictly regulated, and financial obligations were carefully recorded. Older household members had to be cared for and children had to be raised and provided for. The claims of (co-)heirs had to be satisfied or their consent obtained from the estate administration. All such family matters were associated with financial burdens that needed to be addressed

3. The urban and rural land and capital markets appear to have been closely linked. Thanks to a standardised system of written documentation (by notaries), property titles, annuities and debts were easily transferable. Residents of rural areas also had access to common financial instruments, such as the sale of annuities. The annual fairs in cities like Meran, Bozen and Glurns, were important events for paying rents, bartering and exchanging money and thus bringing together the urban and rural population. However, the farming calendar also affected urban participants in financial markets.

4. Wealth mattered, both for investing capital, but also for obtaining credit. Wealthy households sought to diversify their portfolios by investing in various agricultural goods, houses and annuities. The assets could be used both as a source of income and as collateral on the credit market. Those who did not own real estate had to resort to other instruments. Raising working capital without personal wealth was difficult. In addition to the pledging of personal property, sharecropping enabled people to obtain capital, although this could be on unfavourable terms.

These findings suggest that the multitude of financial instruments available in medieval Tirol allowed different households to cope with a variety of everyday struggles. The available instruments were open to nearly everyone, but the financial outcome depended on the personal situation. Whereas annuities or sharecropping could be profitable investments (for the rich), they were often the only affordable credit option (for the poor). The combination of different financial instruments and strategies must be regarded as an important part in the financial history of the medieval period that enabled households to overcome adversities. These findings are particularly relevant because according to the literature, the medieval economy is characterised by an ever-increasing commercialisation.

As has been shown, even in the rural parts of a mountainous region such as Tirol, which was characterised by a high dependence on agriculture, economic activity was stimulated by the availability of various financial instruments. The overall picture is that even mountainous and agricultural regions (that are supposedly economically backward) were affected by commercialisation, but the specific development was not the same as that in urbanised regions. As Shami Gosh has pointed out, commercialisation took place at the same time in several regions of Europe, but the nature of the structural changes that took place differed. [145] The increasing commercialisation of the later Middle Ages can only be understood in a comparative context, looking at both urban and rural areas.

About the author

Stephan Nicolussi-Köhler is Assistant Professor of Medieval History and Auxiliary Sciences at the Department of History and European Ethnology at the University of Innsbruck. His research interests include Mediterranean trade and medieval capital markets, with a focus on small-scale lending and pawnbroking. His publications include: S. Nicolussi-Köhler, Marseille, Montpellier und das Mittelmeer. Die Entstehung des südfranzösischen Fernhandels im 12. und 13. Jahrhundert, Pariser Historische Schriften 121, Heidelberg 2021 (https://doi.org/10.17885/heiup.833) and S. Nicolussi-Köhler (Ed.), Change and Transformation of premodern Credit Markets. The Importance of small-scale Credits, Heidelberg 2021 (https://doi.org/10.11588/heibooks.593).

© 2025 Stephan Nicolussi-Köhler, published by De Gruyter

This work is licensed under the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Articles in the same Issue

- Frontmatter

- Nachruf auf Wolfram Fischer

- Special Issue Articles

- Investment and Saving Opportunities for Different Socio-Economic Groups in Medieval and Early Modern Europe

- Politics, Investments and Public Spending in Bologna (End of 13th – First Half of 14th Century)

- Financing Poor Relief in the Small Lower Rhine Town of Kalkar in the Late Middle Ages

- Credit for the Poor, Investments for the Rich? Different Strategies for Investing and Saving Money in Medieval Tirol

- Financing the Commune

- Investing in a New Financial Instrument: The First Buyers of Urban Debt in Catalonia (Mid. 14th Century)

- Set for Life: Old-Age Pensions Provided by Hospitals in Late-Medieval Amsterdam

- Credit Investments in Northern Italian States (17th–18th Centuries)

- Research Forum

- Food Crises in Germany, 1500–1871

Articles in the same Issue

- Frontmatter

- Nachruf auf Wolfram Fischer

- Special Issue Articles

- Investment and Saving Opportunities for Different Socio-Economic Groups in Medieval and Early Modern Europe

- Politics, Investments and Public Spending in Bologna (End of 13th – First Half of 14th Century)

- Financing Poor Relief in the Small Lower Rhine Town of Kalkar in the Late Middle Ages

- Credit for the Poor, Investments for the Rich? Different Strategies for Investing and Saving Money in Medieval Tirol

- Financing the Commune

- Investing in a New Financial Instrument: The First Buyers of Urban Debt in Catalonia (Mid. 14th Century)

- Set for Life: Old-Age Pensions Provided by Hospitals in Late-Medieval Amsterdam

- Credit Investments in Northern Italian States (17th–18th Centuries)

- Research Forum

- Food Crises in Germany, 1500–1871