Financial Markets and Land Redistribution in 19th Century East Prussia

-

Kirsten Wandschneider

Kirsten Wandschneider is Assistant Professor of Economics and Economic and Social History at the University of Vienna. Her research focuses on the development of financial markets and institutions, and on macroeconomic policy, especially in Europe. Among other outlets her work has been published in the

Journal of Economic History , theJournal of International Economics ,Cliometrica andWorld Economy .

Abstract

How did the emerging market for land in the 19th century influence land distribution in East Prussia? And how did land markets respond to the emergence of financial institutions that relied on land as collateral but also affected the ease and speed of land transfer?

Focusing on the example of a specific financial institution – the East Prussian Landschaft – this paper empirically tests the hypothesis that the Landschaft credit institutes, through their provision of privileged credit, enabled noble estates to expand their landholdings. It also tests whether the existence of Landschaft-credit helped noble estates to remain in the hands of nobles and halted estate sales to the emerging bourgeoisie. The analysis combines several datasets on East Prussian landed estates in 1796, 1834 and 1882 and matches these with borrowing records of the East Prussian Landschaft from 1823 and 1829. The study finds that access to Landschaft-credit correlates positively with estate size over the 19th century, suggesting that the Landschaft credit institutes did play a role in ownership concentration. The results regarding the transfer of estates from the nobility to the bourgeoisie show a weaker link between Landschaft-credit and ownership status of estate holders.

1 Introduction

The history of Prussia is closely intertwined with the influence of the Junkers – a large landholding class of Prussian nobility, which dominated public and economic life. Subdivided into large estates, Junkers controlled a large share of Prussian arable land, and they maintained local control including jurisdiction and policing. This system of land tenure supported the Junker dominance and manifested unequal land distribution. Prussian land inequality has been identified as a contributing factor to the slow progress of German industrialization. Ownership concentration of land also contributed to political concentration, blocking democratization, and delaying the expansion of education. [1] Many studies that focus on the effects of land distribution, take land distribution as given and consider it exogenously determined by geographical factors such as hilliness and climate, which determine land use and crop choice. But for Prussia, the initial land distribution began to change in the early 19th century, as restrictions on land sales were lifted and peasants, who had been granted personal freedom after the October Edict of 1807, slowly emancipated themselves from their landlords. [2]

The current paper focuses on the question of how the emerging market for land in the 19th century influenced land distribution in East Prussia: Did land sales lead to a concentration of land in the hands of noble landholders, or did they re-distribute land more equally? How did land markets respond to emerging financial institutions that relied on land as collateral but also affected the ease and speed of land transfer?

Analysing the creation and operation of a specific financial institution – the Prussian “Landschaft” – this study offers a unique view of the effect of financial markets on estate transfers and landholding patterns, thereby emphasizing an institutional channel through which emerging financial markets shaped Prussian economic history.

Landschaften were founded by Frederick the Great following the 7-Years War in the 1770s. They were mandatory cooperative credit institutions, which, backed by the land of the noble estates in a certain region, issued covered bearer bonds (Pfandbriefe) to extend credit to the estates. Initially only available to designated noble estates, Landschaften enabled the Junker to borrow against their estates and thus provided access to privileged funds for the upper class. These funds could be used to improve the estates, but also to acquire additional land which again could serve as collateral for new loans. As loans were transferable, the Landschaften facilitated the sale of estates from one owner to the next, since they reduced the requirements for cash payments. [3]

While the overall economic importance of the institution of the Landschaft has often been downplayed, previous literature on the Landschaften has noted that especially large and wealthy estates used the credit provided by this institution in order to expand their landholdings at the expense of the free farmers. Estate holders could take out Pfandbriefe on their existing estate and use the proceeds to purchase additional landholdings. Through the purchase, this newly acquired land was incorporated into the Landschaft and could thus expand the credit base of estates. [4] Some authors have gone as far as characterizing the Landschaft as possibly the most important institution of Frederick II’s so-called Adelsschutz, the explicit policy of protecting the dominance of the first estate. [5] Frederiksen points out that King Frederick II himself claimed in his memoirs that the creation of the Silesian Landschaft “saved 400 of the best families of the province of Silesia from ruin.” [6] Yet, the potential mechanism by which the Landschaft supported the expansion of noble estates at the expense of free farmers, has yet to be empirically tested.

This paper aims to fill this gap. Focusing on the example of East Prussia, it empirically tests the hypothesis that Landschaften, through their provision of privileged credit, enabled noble estates to expand their landholdings. It also tests whether the existence of Landschafts-credit helped noble estates to remain in the hands of nobles and halted estate sales to the emerging bourgeoisie. The empirical analysis combines several datasets on East Prussian landed estates in 1796, 1834 and 1882 and matches these with borrowing records of the East Prussian Landschaft from 1823 and 1829 to identify which estates took advantage of the privileged credit provided by the Landschaft. The study finds that access to Landschaft-credit correlates positively with estate size over the 19th century. There is weaker evidence that Landschaften influenced the ownership patterns of estate holdings and limited the transfer of estates from the nobility to the bourgeoisie.

The paper underscores the importance of the Landschaften for Prussian economic development. It also contributes to our understanding of Prussian landholding patterns and emphasizes a financial channel that can reinforce entrenched ownership patterns, thereby exacerbating the negative effect of land inequality. Considering the effect of the Landschaften, which were a financial institution specifically designed to support the Prussian nobility, highlights that, at least in the case of Prussia, land distribution in the 19th century cannot be viewed as exogenous, but as an outcome of the institutions in place.

2 Historical Context

The end of the Seven Years War coincided with a global liquidity crisis. [7] This crisis also affected Prussian Junker estates, who found themselves in financial difficulty. A run-up in estate prices prior to the war was met by falling grain and land prices. Many estate holders were heavily mortgaged and owed more than the value of their estate. Creditors started calling back loans, at a time when landholders lacked the financial means to meet these demands. [8]

A three-year moratorium on all debts called by Frederick the Great on August 1st 1765 was designed to provide relief, but only exacerbated the situation as creditors, uncertain about the protection of their investments, withdrew from the market. The creation of the Landschaften followed at the heels of this moratorium and filled a void in the credit market that re-started the flow of credit towards the estates.

Landschaften were created top-down by Frederick the Great, with the specific aim of supporting the landed gentry. But the idea for their design came from a Berlin merchant, Diederich Ernst Bühring, who had spent time in Bremen and Amsterdam. [9] In 1767, Bühring proposed a general mortgage institute for Prussia that would lend on the collateral of all Prussian estates and issue 4 percent bearer bonds. Borrowers would pay a rate of 4.5-5 percent, the interest differential covering administrative costs. Similar to Bühring’s original plan, in 1768 the new minister of finance, Johann Heinrich Casimir von Carmer presented Frederick II with a proposal for a Landschaft. Rather than setting up a centralized Landschaft, a decentralized system of regional Landschaften, corresponding to the old Prussian Provinces was adopted. As the first Landschaft, Frederick II signed a Cabinet Ordre setting up the Silesian Landschaft in 1769. The Silesian Landschaft was ratified by the general assembly of the Silesian nobility in 1770 and in December of the same year the first Pfandbriefe were issued. [10] Other Landschaften followed in the Kur- and Neumark (1777), Pomerania (1781), Westprussia (1787) and East Prussia (1788), as well as throughout the 19th century in other parts of Prussia. [11]

Landschaften did not loan out their own capital, but acted as pure intermediators between borrowers and lenders. To obtain a loan, borrowers would submit a loan application to the Landschaft, the Landschaft would assess the estate, and based on this assessment issue Pfandbriefe up to about half of the value of the estate. Then the landholder could either sell the Pfandbriefe directly in the open market, or, after a 6-month waiting period, cash them in with the Landschaft. The Landschaft would re-sell these Pfandbriefe in the market to urban and sometimes even international investors. The corresponding cash inflows constituted the lending capital of the Landschaft. In addition to intermediating the original issue, the Landschaft would facilitate interest payments: borrowers would pay interest to the Landschaft in 6-month intervals every June and December, while lenders could collect the interest payments directly from the Landschaft, either at their Berlin headquarters or at one of the regional subsidiary offices. Typically, the Landschaft would retain a 1 percent interest differential to cover administrative costs.

Pfandbriefe were jointly secured by the estate they had been issued for, as well as the institution and the combined assets of the Landschaft, backed by the value of all estates situated within the geographic bounds of the Landschaft. [12] The East Prussian Landschaft thus relied on a system of joint liability (Generalgarantie) whereby the Pfandbriefe issued by the Landschaft were secured by the value of all noble estates situated in East Prussia, whether the owners had taken on a Landschafts loan or not. Pfandbriefe carried additional security as they were always registered in the first privileged debt position (Prinzip der ersten Hypothek), taking preference over other loans in the event of a liquidation. [13] Initially, Landschaft loans were not amortized, thus provided long-term credit at comparatively low rates.

The Landschaften held advantages from an economic standpoint and filled an economic need that improved the functioning of the emerging mortgage credit market. Landschaften assisted the matching of lenders and borrowers, they reduced transaction costs by standing ready to extend credit to borrowers and by selling credit instruments to lenders, they verified collateral, and they pooled loans and standardized the debt instrument, thereby making it more attractive to a wider audience of lenders. The growth of credit after the creation of the Landschaften underscores that the credit market prior to the creation was characterized by a lemons problem, where funds were available in the market, but land on its own was not considered sufficient collateral for estate loans. Providing the operational infrastructure as well as the additional layers of security, Landschaften were able to overcome this and revive lending to the estates. [14]

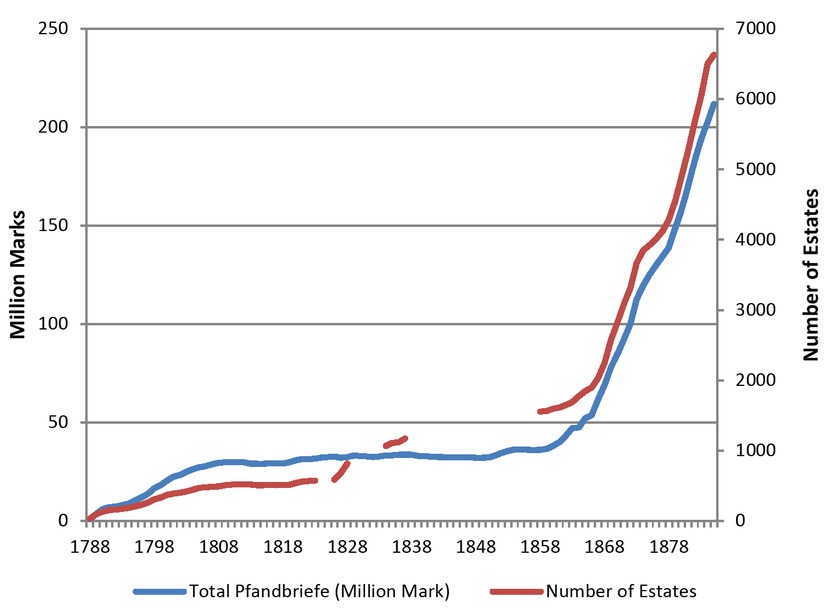

As can be seen in Figure 1, Pfandbriefe were a popular investment right from the start. For the East Prussian Landschaft, which will be the focus of the quantitative analysis in this paper, the number of estates that borrowed and with it the amount of Pfandbriefe issued rose steadily after its creation, reaching 12 million mark in total lending volume and 230 borrower estates already by 1796. The total lending volume rose to around 30 million mark throughout the first half of the 19th century, with some stalling around the time of the Napoleonic wars and the agricultural crises of the 1820s. It is striking that the lending of the Landschaften was not negatively affected by the liberation of the peasants in the wake of the Stein-Hardenberg reforms. As part of the reforms, the large landholders received farmland as compensation, which expanded the estates and added to the potential collateral. [15] The lending volume of the Landschaft further rose in the 1860s and 70s to over 200 million. This large increase in lending went along with a rise in the number of borrowing estates from around 1,000 in the 1830s to over 6,000 by 1885. The large rise can be explained by the changing focus of the East Prussian Landschaft after 1849: the Landschaft admitted free farmers, extending the borrowing privileges and enlarging the scope of the Landschaft. [16] The Landschaft continued to play an important role in agricultural credit markets into the early 20th century. By 1902, about one third of agricultural credit in East Prussia was provided by the Landschaft. [17]

Number of Estates and Total Lending Volume for the East Prussian Landschaft. Source: Leweck, Ostpreussische Landschaft: 1788-1913, Denkschrift zur Feier des 125-jährigen Bestehens der Ostpreusischen Landschaft, Königsberg 1913. (Lending volume is given in nominal values).

Based on data constraints, this paper compares estate outcomes for 1796, 1834 and 1882, since these are available from public records. These observation dates span almost a full century, which brought many political and economic changes for the estates, including the Stein-Hardenberg reforms, the 1848 revolutions and industrialization. The main analysis of this paper relies on the comparison of estates that borrowed from the Landschaft with those where the borrowing status cannot be assumed, at these different points in time. Therefore, other historical events, while critical for the overall development of the estates, do not affect the question of the impact of the Landschaften.

Estate level borrowing records from the East Prussian Landschaft are used to identify the estates that were certain borrowers. Unfortunately, the records of the East Prussian Landschaft, as retained in the Secret State Archives of the Prussian Heritage Foundation (Geheimes Staatsarchiv Preussischer Kulturbesitz) in Berlin are extremely scarce. Borrowing records with detailed information at the estate level are only available for 1823 and 1829, when the Landschaft compiled surveys to review their full lending portfolio in detail. Using these borrowing records, this study effectively measures the effects of the initial wave of lending prior to 1830 and unfortunately cannot speak on the effects of the expansion of lending to the free farms after 1849. Nevertheless, learning about this first wave of Landschaften lending is instructive for measuring the impact of the Landschaft to the extent that these effects persist throughout the 19th century. Since Landschaft loans were not amortized in the first half of the 19th century, the loan portfolio of 1829 also probably presents the stock of loans accumulated to this date rather than a snapshot in time.

3 Landownership and Economic Growth

Growing literature at the intersection of development economics and economic history has shown that factor endowments predict economic inequality and economic inequality generates differential development trajectories. Early examples of this literature include, but are not limited to the works by Engerman and Solokoff, and Easterly. [18] Subsequent researchers have moved past the importance of factor endowments and narrowed the mechanism through which factor endowments affect economic growth. For example, in a comparison of countries, Galor, Moav and Vollrath show that varying patterns of landownership distribution can be related to diverging growth patterns through the differential emergence of human capital promoting institutions. [19] Similarly, Adamopoulus illustrates in a theoretical model that landownership concentration encourages the landed elite to lobby the government to raise barriers to industrialization to protect rural rents. [20] Expanding this work to developing countries, Frankema finds that high levels of land inequality result in persistent high levels of income inequality in former colonies. [21] More recently, Baten and Hippe argue that inequality in land distribution is negatively correlated to human capital formation for historical regions of Europe. [22]

This scholarship has mostly treated the distribution of land as an exogenous variable, often attributed to geographical characteristics such as soil quality, hilliness or climate. Several scholars write about the historic distribution of land and leave aside land reforms and emerging land markets that changed land concentration. [23] A notable exception is presented by the work of Grossman who examines conditions in which landlords are willing to redistribute land towards a landless. If the costs of looting and of protection against looting are too high, the landlord is more likely to give up land. [24]

For Prussia, Gerschenkron already advanced the hypothesis that the landowning Prussian elite, predominantly settled east of the river Elbe, systematically blocked German democratization and industrialization. [25] The elites manifested their privileged position by advancing grain tariffs, levied for their protection. A recent focus on landownership inequality in Prussia, documents its direct impact on democratization and the connection between land-ownership concentration and a variety of output variables. Ziblatt finds that electoral representatives from districts with large land inequality blocked a reform of the Prussian three-tier electoral system. [26] In contrast, income inequality did not have a significant effect on the likelihood that politicians would vote for or against democratization. This highlights the specific role of rural landholding inequality stemming from Prussia’s preindustrial economic structure. Land inequality in Prussia also had an impact on education, marriage, and fertility. [27] Higher landownership concentration was associated with lower school enrolment rates as well as a negative relationship between marriage and enrolment rates, which suggests that political and economic inequality might be an important cofactor of the demographic and economic transitions. Land inequality also negatively impacts economic development through a political channel: If the landed elite can concentrate their political powers, political institutions will be designed to perpetuate inequality and hinder redistributive policies. In many ways the creation of the Landschaften is an example of such an institution.

The current paper adds to the literature on the effects of landholding inequality by advancing the idea that the emergence of land markets changed the distribution of land in 19th century Prussia. It tests the hypothesis that the emergence of Landschaften, which offered privileged credit to noble estates, hindered land re-distribution and entrenched existing inequalities. By emphasizing this financial channel through which institutions can affect the re-distribution of factor endowments, the paper contributes to our understanding of the role of the Prussian Junker for Prussian economic development in the 19th century. It also shows how the landed elite was able to lobby for institutions that would advance and protect their interests. A secondary concern related to ownership concentration is the transition from noble to bourgeois ownership. For Prussia, the question whether noble estates could be sold to wealthy merchants or free farmers was a continuing source of controversy. As the knights’ estates traditionally entitled the estate owner to executive and judicial powers on the estates and came with voting and representation rights in local and district assemblies, both nobles and the crown had an interest in restricting these types of sales to maintain political control. On the other hand, especially in moments of financial distress, individual noble owners had an interest in selling to non-noble owners who represented an expansion of the demand for estates and were often eager buyers. This embourgeoisement of the estates has been discussed in the context of Prussian history focusing on the waning political influence of the Junkers. However, it could also impact economic growth directly if bourgeois owners improved the productivity of the estates. [28]

4 Estate Data

This study empirically estimates the effect of the Landschaften on land sales and transfers, using a difference strategy to assess the impact of the Landschaften on ownership structure and estate size in East Prussia in the 19th century. By analysing patterns of estate ownership and transfer, it traces the economic effects of the Landschaften on the Junker estates, and thereby Prussian economic history.

The paper builds on and expands the work by Eddie who discusses ownership patterns of estates at the end of the 19th century. [29] By matching estate records from 1796, 1834 and 1882, using records of the East Prussian Landschaft in 1822/23 and 1829, the current paper covers almost a century of estate changes.

Landschaften could increase the frequency of turnover by allowing buyers a reduced purchase price if they could take over and service the outstanding Landschafts loan. But they also reduced the need for distress sales since they provided privileged access to low interest long-term credit. The effect of the Landschaften on estate transfers is therefore ultimately an empirical question. Ownership transfer for estates borrowing from the Landschaft was frequent. Of the 887 estates listed in the 1829 survey as holding a Landschaft loan, 250 were sold and 260 changed hands through some form of foreclosure process, often involving the Landschaft between 1806‒1829. Only 144 estates from the 1829 survey had no change in ownership and 256 estates were passed on within the family. This suggests that the Landschaft did play a large role in the survival of estates and facilitated estate foreclosures and turnover for failing estates. But it also confirms that the Landschaft was used by estates that displayed all types of ownership change and was not exclusively relied on during times of financial distress. [30]

In addition to turnover, it is interesting to investigate which estates changed hands from noble to non-noble estate holders and whether and how the Landschaft influenced these transfers. Before 1807, estate sales to non-nobles were only allowed with special permission of the King, and restrictions were put in place to limit voting rights by bourgeois owners. [31] In 1811, all restrictions on the sale and ownership of estates were removed. [32] Previous studies of ownership changes document that two thirds of all Prussian estates (East and West Prussia combined) were owned by non-nobles by the mid-nineteenth century. Eddie speculates that most of this changeover took place in the 1820s, but cannot differentiate whether most purchases of estates were carried out for political or economic reasons. His study also lacks the data to verify when the ownership transfers took place. The 1834 estate register lists one third of the estates listed for East Prussia with noble ownership (463 out of 1388). [33]

The current study matches estates included in the register of leuds (Vasallentabelle) from 1796, the 1834 estate register (Matrikel), and the 1882 estate register (Güter-Adressbuch). This allows for a tracking of changes in estate size and ownership over a much longer timeframe than has been conducted in previous studies. The 1796 register of leuds lists the estate name, owner name, location of the estate (district) as well as the size of the estate and the corresponding tax payments. The status of the owner was matched from Mortensen et al. [34] To measure estate size in 1834, this paper uses the 1834 official estate register, sanctioned by the King, that designated estates as knight’s estates (Matrikel). [35] The estates listed in the Matrikel carried with them certain political privileges, such as voting rights in the local district assembly (Kreistag) and the provincial legislature (Landtag). A detailed description of this source can be found in Eddie. [36] The 1882 data stem from Ellerholz as used in Eddie and again include estate name, owner name, owner status and estate size. [37]

The paper relies on analysis at the estate rather than the ownership level, as estates are easier to track over time. Location information (Kreis, Department) improves matching, despite spelling inconsistencies between the different original sources. Moreover, all lending by the Landschaft was collateralized by and allocated to estates rather than individual owners.

In total, the dataset consists of information on 2008 estates for 1796, 1400 estates for 1834 and 2470 estates for 1882. It was possible to uniquely identify 449 estates in all three datasets. In the following this set of 449 estates is referred to as the matched sample, in contrast to the full sample of all estates. Estates were matched with a Levensthein algorithm and checked by hand by the author. [38]

One concern might be that the matching between the estates is not complete and thus might introduce bias into the regression results. Summary statistics also show different estate counts for the different sources (compare Table 1). However, as long as this bias is not systematic, implying that the reason an estate is missing or unmatched is not related to its borrowing status, this should not emerge as a concern. Since the borrowing information is drawn from a separate source and was not originally included in the original sources for the estate size and ownership data there is little reason to believe that it borrowing status influenced the compilation of these sources. Moreover, for all empirical results the results from the matched sample, i.e. the set of estates that can be identified across all three estate registers, as well as the full sample are shown.

Similarly, one might be concerned that the estate sizes in the three different sources are measured differently and are not comparable. To reduce error, the analysis relies on the total area of the estates, rather than the share of the estate used for farming, animal husbandry or forestry, following Eddie in the adjustment of the 1882 data for the inclusion of forest land that was underreported in the original source. [39] For 1834, results are reported for total size, as well as net size correcting for land that was transferred to free farmers after 1807, again following Eddie. [40] The empirical results are unaffected by this adjustment. Also, as discussed above, inconsistencies in the estate sizes between the different samples would only present a threat to the estimation of the impact of the Landschaften on estate size if they were correlated to the credit status of the estates.

To assess the impact of the Landschaften and identify the borrowing estates, the above data is matched with a survey conducted by the Landschaft in 1822/23 and a list of member estates from 1829, also published by the Landschaft. [41] The 1823 survey contains information on 554 estates with a total Pfandbrief volume of 33.9 million marks. [42] The aggregate number of estates listed in the survey matches the membership numbers given in other sources: The Denkschrift for the 125-year anniversary of the East Prussian Landschaft gives 574 estates and a total Pfandbrief amount of 31.6 million marks for 1823. [43] Part of the discrepancy could stem from the fact that the survey was completed over two years, 1822 and 1823. In addition to the survey, Landschaft documents include the 1829 list that enumerates 887 estates that had borrowed through the Landschaft in 1829. The joint set of borrowing estates thus includes 897 estates, 263 of which could be mapped into the matched sample of 449 estates identified in all three sources as described above.

The record of a Landschafts loan in 1823 or 1829 is considered as treatment, knowing that all estates listed here did take out a loan before 1829. Therefore, this presents a lower bound of estates that borrowed from the Landschaft. In the following, this group of estates that is identified as holding a loan in 1823 or 1829 is described as the set of known borrowers, in comparison with all other estates who are uncertain borrowers. As described above, the Landschaft continued to extend loans after 1829. By 1834, the number of estates that borrowed through the Landschaft had risen to 1,064 and the number of borrowers further rose in the second half of the 19th century. [44] As mentioned previously, there is no known record of borrowing information on individual estates after 1829, so later borrowing information could not be included in the empirical analysis. This implies that the empirical results in this paper certainly undercount the effects of the Landschaft, but this undercounting sets a downward bias on the results. Thus, if the empirical estimates show an effect of the Landschaft based on this limited sample, the true effect of the Landschaft was likely much larger. The timing of the borrowing measure also implies that this study captures the first big loan expansion by the Landschaft before 1830, thereby estimating the effects of its initial credit expansion on the estates. It is important to note, however, that even though all noble estates were included in the East Prussian Landschaft, including joint liability, being counted as a certain borrower captures the uptake of credit by individual estates, so the treatment is not random. All estimates can therefore not be interpreted as causal, but show the association between estate size and the reliance on a Landschaft loan.

The East Prussian Landschaft was founded in 1788 and already counted 210 borrowers in 1796, thus the estate data from 1796 do not present a clean pre estimate. However, data constraints make the available sample the best approximation of the pre-Landschaft ownership distribution. As loans were not amortized, one can assume that the set of existing borrowers is relatively stable. For example, comparing the borrowers in 1823 and 1829, the large majority of Landschaft borrowers in 1823 also borrow in 1829. The true variation that drives the empirical results is thus the set of about 700 estates that took out their first loan with the Landschaft between 1796 and 1829, proxied through the full set of borrowers that we observe in 1829, in comparison to those that do not. Since the years of the Napoleonic Wars and the agricultural crisis of the 1820s were a turbulent time for the estates with lots of economic insecurity and estate turnover, one can expect many of the relevant transactions to have taken place during this period. This also captures the first two decades after restrictions on land sales had been removed and the bourgeoisie (except Jews) could freely purchase noble estates.

Moreover, this study only uses the existence of a loan, not the size of the loan provided to measure borrowing. From the 1823 data, we know that the average loan amounted to 54.16 percent of the assessed tax value of the estate, so most borrowers took out the maximum loan amount. On average, estates held arrears of 4.45 percent of the outstanding loan amount. [45]

Summary statistics, as shown in Table 1, document the overall decline in estate size as well as the reduction in the number of estates owned by the nobility. In 1794, the average estate size in the full sample was 711.5 ha, dropping to 572 ha by 1834 and 554 by 1882. The average net size in 1834 was 505.8 ha with a standard deviation of 666.9 (not shown). Similarly, in 1796, 82.6 percent of estates were held by nobles, dropping to 33.4 percent in 1834 and 23.5 percent in 1882. This is consistent with the findings of Eddie that date the majority of transfers from the nobility to the bourgeois population to before 1834. [46] For the matched sample, the overall pattern holds, albeit with larger average estate size and also a somewhat higher share of nobility in all three time periods.

Summary Statistics.

| Full Sample | Matched Sample | |||||

|---|---|---|---|---|---|---|

| 1796 | 1834 | 1882 | 1796 | 1834 | 1882 | |

| Size | ||||||

| mean | 711.532 | 572.163 | 553.817 | 751.062 | 739.915 | 630.564 |

| std dev | 883.496 | 824.043 | 1047.237 | 541.969 | 965.677 | 721.652 |

| # of estates Nobility | 1,673 | 1,400 | 2,436 | 399 | 449 | 449 |

| mean | 0.826 | 0.334 | 0.235 | 0.831 | 0.468 | 0.373 |

| std dev | 0.379 | 0.472 | 0.424 | 0.375 | 0.500 | 0.484 |

| # of estates | 1490 | 1,388 | 2,341 | 384 | 447 | 408 |

Source: Author’s calculations based on Matrikel (1834), in: GStA PK I. HA, Rep 77 Tit. 438, Nr. 62, Bd. 2, and Mortensen et al., Historisch-geographischer Atlas des Preussenlandes; Ellerholz, Handbuch des Grundbesitzes; Eddie, Landownership in Eastern Germany.

Table 2 compares the difference between estates that borrowed from the Landschaft (as identified through listing in the 1823 or 1829 estate lists) with estates that did not borrow in 1796. This comparison provides us with a baseline for our following statistical analysis comparing the sample of certain and uncertain borrowers in 1834 and 1882. Intuitively, this presents a check on the differences between the two samples, ideally before loans are taken out.

Normalized differences between the certain and unknown borrowers, 1796.

| Full sample | Matched Sample | |||||

|---|---|---|---|---|---|---|

| Credit | No Credit | Norm. Diff. | Credit | No Credit | Norm. Diff. | |

| Size | ||||||

| mean | 792.373 | 692.854 | 797.660 | 687.644 | ||

| std dev | 580.237 | 938.930 | 0.090 | 549.084 | 527.142 | 0.145 |

| count | 314 | 1,359 | 230 | 169 | ||

| Nobility | ||||||

| mean | 0.842 | 0.817 | 0.851 | 0.801 | ||

| std dev | 0.365 | 0.387 | 0.047 | 0.357 | 0.400 | 0.092 |

| count | 532 | 958 | 228 | 156 | ||

Note: Normalized differences are calculated as

where

As can be seen in Table 2, the average size between certain borrowers and the unknown group differs in both the matched and the unmatched sample, with the borrowing estates showing an average size of just under 800 hectares and the estates of unknown borrowing status showing a smaller average size of just under 700 ha. [47] A similar pattern emerges when comparing the number of noble estates taking out loans in the full and the matched sample. In the full sample, 84.2 percent of the borrowers were noble, while the share drops to 81.7 percent for uncertain borrowers. In the matched sample, these shares are 85.1 percent and 80.1 percent, respectively. [48] This implies that estates that are certain borrowers and those of unknown borrowing status are not statistically different in terms of their size and their likelihood of being noble estates and that the differences seen for 1834 and 1882 are related to the effects of the Landschaften.

5 Empirical Analysis

The following analysis relies on a difference-in-difference approach for estimating the effects of the Landschaft loans for the certain borrowers with respect to estate size and ownership status. Equation (1) is the estimating equation, where credit indicates whether an estate is identified as a certain borrower by being included in the 1823 or 1829 Landschaft surveys, post captures the estate size and ownership status in the years 1834 and 1882. This set-up primarily focuses on the sign and significance of

Table 3 shows the results of OLS regressions both on the full sample and the matched sample, taking size and adjusted size as dependent variables. In all four regressions, the credit variable is positive and significant at 1 percent, while the post dummy which captures the values for 1834 and 1882 is negative and significant, confirming that estate size dropped on average over the 19th century, but that estates that are known borrowers from the Landschaft before 1834 are larger on average. The interaction term is positive and significant at 1 percent for the full sample and at 10 percent for the matched sample respectively, showing that estates that were known borrowers from the Landschaft were on average 32-29 percent larger in the post period than estates that were uncertain borrowers for the full sample, and 14 percent larger for the matched sample. [49]

Base line regression, dependent variable estate size.

| Full Sample | Matched Sample | |||

|---|---|---|---|---|

| VARIABLES | OLS | OLS | OLS | OLS |

| Dependent variable: | size | adj. size | size | adj. size |

| Credit | 0.280*** | 0.274*** | 0.191*** | 0.189*** |

| (0.0474) | (0.0473) | (0.0719) | (0.0718) | |

| Post (1834 & 1882) | -0.514*** | -0.534*** | -0.324*** | -0.367*** |

| (0.0278) | (0.0275) | (0.0506) | (0.0498) | |

| Credit*Post | 0.279*** | 0.257*** | 0.131* | 0.132* |

| (0.0515) | (0.0512) | (0.0718) | (0.0711) | |

| Constant | 6.082*** | 6.088*** | 6.259*** | 6.262*** |

| (0.0230) | (0.0229) | (0.0549) | (0.0549) | |

| Observations | 5,509 | 5,505 | 1,297 | 1,295 |

| Number of id | 3,869 | 3,868 | 449 | 449 |

| Robust standard errors in parentheses | ||||

| *** p<0.01, ** p<0.05, * p<0.1 | ||||

Source: Author’s calculations based on Survey (1823) and List of Estates in Receivership, Survey (1829), cf. footnote 41; Matrikel (1834), in: GStA PK I. HA, Rep 77 Tit. 438, Nr. 62, Bd. 2, and Mortensen et al., Historisch-geographischer Atlas des Preussenlandes; Ellerholz, Handbuch des Grundbesitzes; Eddie, Landownership in Eastern Germany.

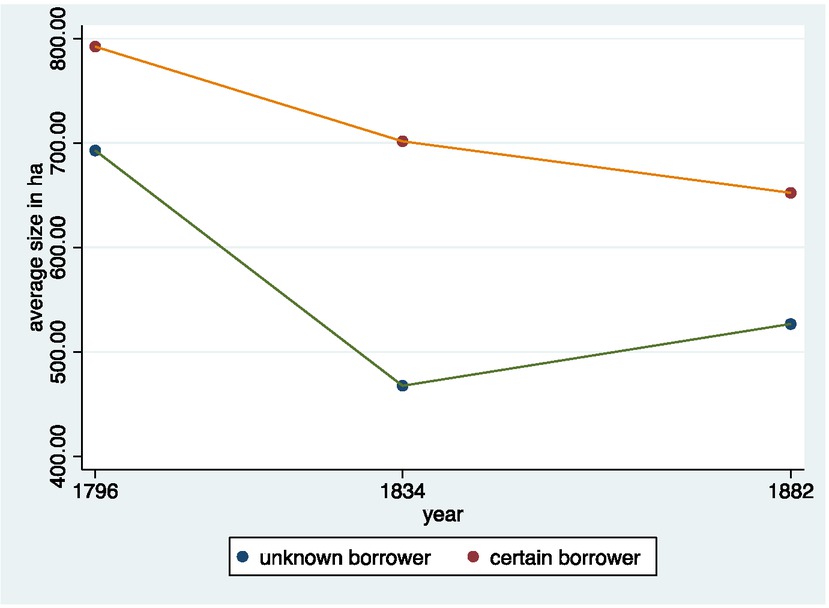

Figure 2 visualizes the results from Table 3. While all estates demonstrate an overall drop in estate size, estates that were certain borrowers are significantly larger than estates of unknown borrowing status in all three period. It is also noticeable that the decline between 1796 and 1834 is much more pronounced for the uncertain (non-) borrowers, demonstrating the effect of the Landschaft.

Size Comparisons Between Certain and Unknown Borrowers Over Time, 1796, 1834 and 1882. Source: Author’s calculations based on Survey (1823) and List of Estates in Receivership, Survey (1829), cf. footnote 41.

A similar picture emerges for the share of estates held by nobles. Table 4 shows the results of OLS and Probit regressions, taking noble ownership as a dependent variable, again for the full and the matched sample. The coefficient on post is significant and negative in all specifications and confirms the decline in noble ownership for all estates. Interestingly, here the interaction term, interacting certain borrower status with the years 1834 and 1882 is only positive and significant in the full sample, indicating that estates with a Landschaft loan were more likely to retain noble ownership. Following this specification, known borrowers were 13.7 percent more likely to be of noble status in the post period. [50]

Baseline regression, dependent variable noble ownership.

| Full Sample | Matched Sample | |||

|---|---|---|---|---|

| VARIABLES | OLS | Probit | OLS | Probit |

| Dependent variable: noble owner | ||||

| Credit | 0.0324 | 0.0979 | 0.0472 | 0.194 |

| (0.0200) | (0.0807) | (0.0398) | (0.153) | |

| Post (1834 & 1882) | -0.582*** | -1.663*** | -0.428*** | -1.162*** |

| (0.0144) | (0.0523) | (0.0397) | (0.126) | |

| Credit*Post | 0.128*** | 0.367*** | 0.0279 | 0.00719 |

| (0.0257) | (0.0900) | (0.0503) | (0.166) | |

| Constant | 0.806*** | 0.905*** | 0.807*** | 0.846*** |

| (0.0124) | (0.0471) | (0.0320) | (0.115) | |

| Observations | 5,219 | 5,219 | 1,239 | 1,239 |

| Number of id | 3.204 | 449 | ||

| Robust standard errors in parentheses | ||||

| *** p<0.01, ** p<0.05, * p<0.1 | ||||

Source: Author’s calculations based on Survey (1823) and List of Estates in Receivership, Survey (1829), cf. footnote 41; Matrikel (1834), in: GStA PK I. HA, Rep 77 Tit. 438, Nr. 62, Bd. 2, and Mortensen et al., Historisch-geographischer Atlas des Preussenlandes; Ellerholz, Handbuch des Grundbesitzes; Eddie, Landownership in Eastern Germany.

In the matched sample, which is more homogeneous and skewed towards noble estates, the effect cannot be detected. Again, since one can only compare the known borrowers with the uncertain borrowers in this empirical design, these results are conservative estimates for the relationship between Landschaften borrowing and noble status. Also, the smaller sample size for the matched sample increases the standard errors. Therefore, the mixed results on the effect of the Landschaften on noble ownership are interpreted as weak evidence that the Landschaften enabled noble owners to hold onto their estates.

In sum, the results presented here do support a narrative consistent with the historical literature that the privileged access to credit enabled large noble landholders to expand the size of their estates, or at least slow their decline. There is weak evidence that Landschaften also supported noble landholders in maintaining ownership over their estates.

This evidence on the estates can also be corroborated by a brief look at estate owners. Table 5 lists the 15 largest landowning families by area in 1796 with their noble status and the number of loans recorded on their estates in the 1823/29 Landschaften records. It is striking to see that many of the large noble landholders took out multiple loans, typically on several estates or estate partitions, providing evidence that the Prussian nobility took advantage of the Landschaften. While there are no surviving sales records to document a direct link, the majority of these families (among them the families of Dohna, Doenhoff, Groeben, Schlieben, Finckenstein, Eulenburg, Kuhnheim and Schwerin) also remained among the largest landowners in both the matrikel of 1834 and the 1882 estate records.

Large Landowners and Landschaften Loans.

| Number | Estate Ownership 1796 (ha) | # Loans | Nobility | Lastname |

|---|---|---|---|---|

| 1 | 68,242 | 8 | yes | Dohna |

| 2 | 52,998 | 3 | yes | Doenhoff |

| 3 | 51,992 | 12 | yes | Groeben |

| 4 | 43,909 | 6 | yes | Schlieben |

| 5 | 37,940 | 1 | yes | Finckenstein |

| 6 | 25,580 | 3 | yes | Eulenburg |

| 7 | 22,749 | 6 | yes | Kuhnheim |

| 8 | 21,444 | 2 | yes | Kreyzen |

| 9 | 16,233 | 4 | yes | Brandt |

| 10 | 14,590 | 3 | yes | Kalckstein |

| 11 | 14,550 | 2 | yes | Schwerin |

| 12 | 14,388 | 4 | yes | Domhardt |

| 13 | 14,052 | 7 | yes | Buddenbrock |

| 14 | 13,287 | 6 | yes | Knobloch |

| 15 | 11,716 | 3 | yes | Waldburg |

Source: Author’s calculations based on archival records Geheimes Staatsarchiv Preussischer Kulturbesitz, Berlin Dahlem: Survey (1823) and List of Estates in Receivership. Survey (1829).

6 Conclusion

This study of landownership changes in East Prussia between 1796 and 1882 empirically tests the effect of the Landschaften in providing credit to the noble estates, and thereby impacting on estate size and estate ownership status in the 19th century. The East Prussian Landschaft, established in 1788, provided owners of knights’ estates privileged access to credit. It has been documented in the literature that this credit enabled noble estates to expand their landholdings at the expense of free farms. [51] By taking out credit on existing estates, using the proceeds to purchase additional land, and then incorporating this additional land into their estates, landholders could increase the size of their estates, while at the same time increasing their collateral which would give them additional access to funds. In previous studies, this effect has not been systematically studied.

The paper fills this gap by empirically testing the hypothesis that Landschaften, through their provision of privileged credit, enabled noble estates to expand their landholdings and that the existence of Landschaft-credit helped noble estates to remain in the hands of nobles and halted estate sales to the emerging bourgeoisie. The analysis combines several datasets on East Prussian landed estates in 1796, 1834 and 1882 and matches these with borrowing records of the East Prussian Landschaft from 1823 and 1829. The study finds that access to Landschaft-credit correlates positively to estate size over the 19th century. It also presents weak evidence that the Landschaft influenced the ownership patterns of estate holdings and halted the sale of estates from noble to bourgeois owners.

These results are relevant on two dimensions: First, this study expands our understanding of the credit provision by the Landschaften and the role of the Prussian nobility for East Prussia in the 19th century. In contrast to previous assessments of the Landschaften, which had concluded that the Landschaften only played a small formal role for the estates, this study shows that in terms of estate size and possibly also in terms of estate ownership for noble owners, Landschaften had an effect. [52] For the influence of the Prussian Junkers in the 19th century, this confirms that even with progressing industrialization at least part of the Prussian nobility was able to protect and entrench their influence with the very institutions designed for their support.

Second, this study also highlights a financial channel through which existing inequalities in the distribution of land could be further propagated. By emphasizing this financial channel, it contributes to our understanding of the mechanism of how institutions can affect the distribution of factor endowments and thus a country’s growth path. Prussian Junkers not only used their political influence to block industrialization and the expansion of education, but they also lobbied for and then used financial instruments at their disposal. The extension of privileged credit towards the noble estate owner through the creation of the Landschaften fulfilled its intended purpose, even if it could not fully prevent the embourgeoisement of the estates.

About the author

Kirsten Wandschneider is Assistant Professor of Economics and Economic and Social History at the University of Vienna. Her research focuses on the development of financial markets and institutions, and on macroeconomic policy, especially in Europe. Among other outlets her work has been published in the Journal of Economic History, the Journal of International Economics, Cliometrica and World Economy.

Acknowledgement

Support from the Prussian State Archive and from the Institute for New Economic Thinking (#INO13-00017) is gratefully acknowledged. The author thanks Erik Hornung and the late Scott Eddie for sharing data on the 1882 estate register, and the 1834 Matrikel. Thanks also go to Roswitha Ristau who allowed me access to her late husband’s transcription of the 1823 survey data. Part of this paper was completed while visiting the Lehrstuhl für Sozialand Wirtschaftsgeschichte at the WWU Münster, Germany.

© 2022 Walter de Gruyter GmbH, Berlin/Boston

This work is licensed under the Creative Commons Attribution 4.0 International License.

Artikel in diesem Heft

- Frontmatter

- Abhandlungen

- Immobilienmärkte in der historischen Forschung

- Between Rack Rents and Paternalism: Economic Behaviour and the Lease Market in Westphalia, with a Particular Focus on the 19th Century

- (Mal-)practices of Auctioneering on the English Property Market During the 19th Century

- Financial Markets and Land Redistribution in 19th Century East Prussia

- Deutsche Hypothekenbanken zwischen Sicherheitsdenken und Spekulationsfieber: Immobilienfinanzierung im Bauboom des späten 19. Jahrhunderts

- Glücksspiel oder ökonomisches Werturteil mit Folgen?

- Gegen Immobilienspekulation und steigende Mieten?

- The Great De-Mortgaging: the Retreat of Life Insurances From Housing Finance in US-German Historical Perspective

- Forschungs- und Literaturbericht

- In the Shadow of the Golden Calf.

- Mass Weddings, Baby Boom and Full Employment?

Artikel in diesem Heft

- Frontmatter

- Abhandlungen

- Immobilienmärkte in der historischen Forschung

- Between Rack Rents and Paternalism: Economic Behaviour and the Lease Market in Westphalia, with a Particular Focus on the 19th Century

- (Mal-)practices of Auctioneering on the English Property Market During the 19th Century

- Financial Markets and Land Redistribution in 19th Century East Prussia

- Deutsche Hypothekenbanken zwischen Sicherheitsdenken und Spekulationsfieber: Immobilienfinanzierung im Bauboom des späten 19. Jahrhunderts

- Glücksspiel oder ökonomisches Werturteil mit Folgen?

- Gegen Immobilienspekulation und steigende Mieten?

- The Great De-Mortgaging: the Retreat of Life Insurances From Housing Finance in US-German Historical Perspective

- Forschungs- und Literaturbericht

- In the Shadow of the Golden Calf.

- Mass Weddings, Baby Boom and Full Employment?