Public Research Support for an Innovative Integrated Payment Model of Service Delivery

-

Antonio Bracaglia

Antonio Bracaglia is technical manager of TITAN Project and he is professional master at Poste Italiane Information Technology – E-payments Dept. He is mainly involved in R&D e-payments EU projects as CTO. Antonio has extensive professional experience in different sectors in the Card Payment Industry, managing and maintaining relationships with payment service providers and solution providers. For many years, he has been working on e-payments products and SEPA initiatives related to standardization, namely on the following issues: definition of security and functional requirements for new payment products, certification and type approval processes, implementation and testing of new protocols, risk analysis and risk assessment.

Giulia Monetta is temporary researcher at Department of Management and Information Technology, University of Salerno (Italy). She has worked in TITAN Project for Poste Italiane. Her current research interests are aimed to analyze the role of public governments can play in contributing to the development of entrepreneurial culture. Giulia has a PhD in public management and her principal research themes regarding strategic management and corporate governance of public and private firms. Her publications are the result of empirical and industrial research and are published in academic and professional journal such as

Total Quality Management and Business Excellence . and

William Vanobberghen

and

William Vanobberghen

William Vanobberghen is secretary general of EPASOrg (Electronic Protocols Application Software) and he is head of International Projects at Groupement des Cartes Bancaires. He initiated and co-ordinated the EPAS initiative. William has been co-ordinating various international projects funded by the European Commission in the framework of research and development programs in the field of information technology. William is in charge of the coordination of international projects of co-operation related to card payments. He also launched the first ISO 20022 – standardization initiative in card payments. William holds a degree in commercial and financial sciences as well as a degree and master in computer sciences. He also holds an executive MBA from HEC Paris.

Abstract

This paper introduces an entrepreneurial innovation supported by public research. TITAN is an R&D project funded by European Structural Funds with the National Operational Program for “Research and Competitiveness” 2007–2013 (NOP for R&C). General purpose of TITAN project is to achieve a multi-application and multi-channel platform to manage value-added services (VAS) and e-payments. From the EPAS protocols perspective of standardizing the electronic payment, VAS data management will be included in the current financial messages (CAPE – ISO 20022). In order to improve the process of card payment transactions through the delivery of new VAS was born the cooperation between EPASOrg and TITAN’s team. This cooperation would facilitate the examination and submission to ISO 20022 of data components related to the provision of added-value services meeting the requirements of those new contactless applications developed in the framework of the project. This is the principal and most entrepreneurial innovation concentrated on the integration of payment and VAS that draws attention to a new model delivering the VAS on a multi-application device used by both payment and VAS, during the same payment transaction. The latter result has led a Change Request to ISO in order to allow the extension to the VAS on the standard ISO 20022 related to card payment. The innovative model proposed is validated through a sample scenario and, finally, the conclusions summarize the next steps and underlines possible implications for future business and technological developments.

1 Introduction

The paper analyzes a co-funded project of entrepreneurial innovation, emphasizing the role of European Structural Funds for industrial research and innovative models of enterprise. The project in question, TITAN, is co-funded by a specific Action of the Italian R&D Program and European Union (EU) structural funds. The activities involved and results obtained, i.e. an innovative business and technological model developed in the TITAN framework, confirm that public support for research and innovation is necessary, but not always sufficient for the diffusion of an entrepreneurial culture.

The main purpose of the paper is to highlight how public policy can exploit technology and business outputs deriving from a funded R&D project. An overview of the nature and success of the project is provided and expected and achieved results indicated together with details: project description, beneficiaries, objectives, etc. A particular focus on the entrepreneurial innovation of the project is highlighted and feedback from the direct beneficiaries of the resources and from those who have supported and financed the project is provided.

Grounded on previous academic theory, Section 2 investigates the nature of the relationship between industrial research and entrepreneurial innovation, and in particular the role and contribution of public support on business development. Section 3 introduces the role of Europe in the process of industrial restructuring and economic development and describes the framework of National Operational Program for “Research and Competitiveness” 2007–2013. Section 4 pivots on its principal objective and highlights the integration of multiple actors and the scientific and pre-industrial activities to create an innovative model for managing “Multichannel Electronic Money and Value Added Services.”

Given the purpose of TITAN as outlined above, Section 5 presents the results obtained by integrating ISO 20022 financial messages for service delivery within the same smart card used for payment. A subsection shows how the innovative model is validated through a sample scenario in which users decide to buy a bus ticket from an accredited “merchant” using their multi-application card as device for electronic payment and delivery. The conclusion delineates potential steps and implications for business and technological development, taking into account that entrepreneurial innovation manifests itself as a key driver of improved productivity and sustainable growth in today’s global economic landscape (Subramanian et al. 2003). In this respect, the TITAN project is knowledge, technology and innovation intensive and fosters network development, bringing together a variety of themes, i.e. technology and human resources, process creativity and, finally, entrepreneurship, demonstrating results at industrial scale of European public support for research and innovation.

2 Theoretical Background

Research on entrepreneurship has been evolving for over a half century, observational at first (Drucker 1985; Schumpeter 1934) and subsequently becoming an eclectic and disjointed beginning without theory building (Shane and Venkataraman 2000). Entrepreneurship, traditionally considered as an “outward-looking” phenomenon, has been greatly influenced over the years Kirzner (1997) mainly by the Austrian school of economics (Schumpeter 1934; Hayek 1945; Shackle 1979; Littlechild 1986) and is probably one of the most studied yet least understood concepts in science (Vallini and Simoni, 2009). Presently, there is a lack of consensus about defining or conceptualizing entrepreneurship (Acs, Autio, and Szerb 2013, 11). Several factors contribute to this, including the various uses of the term entrepreneurship in different academic fields, diverse aims and diverse perspectives (Parker 2005). However, a compromise seeing entrepreneurship as a complex and multifaceted phenomenon has taken shape over the last 20 odd years (OECD 2006; Wennekers and Thurik 1999).

Success of entrepreneurial initiatives is heavily dependent on contextual determinants. Acs, Autio, and Szerb (2013), for example, highlight the prominent role played in Europe by entrepreneurship policy. Unlike other less-institutionalized economies, EU countries are characterized by the salient role of environmental and external contingencies. Acting on these factors is therefore essential in fostering entrepreneurship. Starting from the Schumpeterian premise that new opportunities depend upon newly created information, knowledge thus becomes the driving force of economic growth and is key for the evolution of industries. The connection between entrepreneurship and economic development is a common feature of EU initiatives in creating an enabling entrepreneurial environment. In this context, the TITAN project is empirical evidence that external conditions such as actions supported by EU-funding schemes foster and stimulate entrepreneurial innovation. In short, external conditions can improve entrepreneurship as determinants facilitating fund procurement for R&D and underpin new entrepreneurial and innovation opportunities for business success.

It is widely recognized that entrepreneurship status cannot merely be attributed only to established, mature firms (Stevenson and Jarillo 1990) and that new ventures also need to be supported by public initiatives. However, studies of entrepreneurship are now going beyond small and medium enterprises (SMEs). The focus currently is on the process of entrepreneurship rather than the domain (Shane and Venkataraman 2000). Covin and Slevin (1991) argue, for example, that large established entrepreneurial firms are risk-taking, innovative and proactive. They also claim that a variety of factors influence the choice of entrepreneurial intensity, including environment, strategic position, organizational structure and culture together with firm resources. The interface between public support and entrepreneurship is therefore of paramount important also in later stages of firm development.

One of the greatest challenges facing European economies is the comparatively limited capacity to convert scientific breakthroughs and technological achievements into industrial and commercial success. As a result, there is growing awareness of the proactive approach being undertaken by some firms, with many adopting a direct entrepreneurial role in collaborating with other (including academic) institutions. The paper examines the activities of those businesses involved with universities and research centers developing an innovative model of service delivery originating from the TITAN project experience. The evidence highlights furthermore, how European structural funds for promoting entrepreneurship could help large established firms in the definitions of value propositions, new business models and value creation networks.

As is well known, entrepreneurship is the essence of managing change for business success. Market-driving firms change their value propositions and business models to provide the market with higher customer value and competitive advantage. The intensity of change and innovation is key and most likely distinguishes market-driven behavior (entrepreneurial phenomenon) limiting it to market-related decisions. Schindehutte, Morris, and Kocak (2008, 5) define market driving as “a dynamic advantage-creating capability and a disruptive advantage-destroying performance outcome” that “reflects a strong entrepreneurial orientation.” In this sense, the market-driving approach is the marketing essence of entrepreneurship in Schumpeterian terms, i.e. a creative destruction force. The authors maintain that market driving is not to be intended as opposed to market-driven nor are the two constructs part of a continuum (Kumar, Scheer, and Kotler 2002). The market-driven approach is aimed at redefining market orientation, whereas the emergence of market driving behavior is the essence of entrepreneurial action; it is an outcome of innovation activities and at the same time, an indicator of sustainable and competitive advantage. Clearly, the innovative model of service delivery integrated with payment is strongly related to entrepreneurship on the part of partners in the TITAN project. Their joint activities enable TITAN partners to act as first movers in industrial and payment sectors by proposing a standard to manage service delivery contextually with payment services, the change impacting strongly on the behavior of all the market stakeholders in the related value chain. While market-driven firms focus on customers (sometimes in the conceptually wider competitive context, which includes competition), market-driving firms consider the entire range of industry participants (Narver, Slater, and MacLachlan 2004; Hills and Sarin 2003). Market-driving behavior, for example, has been found particularly effective for marketing high-technology products and innovations in industries characterized by high levels of technological and market uncertainty and of competitive volatility, such as that of e-payment. In other words, the aim of businesses and actors in this sector, rather than serving a target that already exists, is to create such a market. In this respect, TITAN partners will be the driving force that shapes the structure, preferences and the rules of competition in a radically redefined or newly created market.

The article therefore discusses how entrepreneurship should be defined, not simply in terms of self-employment or new firm creation but rather as an “entrepreneurial orientation” or firm-level behavioral disposition (Lumpkin and Dess 1996) generated at collective level, i.e. a cognitive attribute such as perception of opportunity (Shane and Venkataraman 2000). In other words, forms of entrepreneurship that are market driving are analyzed, highlighting at the same time, how market expectations have driven TITAN project activities possible, thanks to the support of external funding for entrepreneurial innovation.

3 European Public Funds Support for Industrial Research and Entrepreneurial Innovation

At a global level, technological research and development is taking on a primary role in the process of industrial restructuring and socioeconomic development. In this sense, policy makers attribute ever more importance both to policies and programs that support and enhance industrial research and to specific financial operations aimed at using the results of research activities in a socioeconomic context (Shane 2005).

In Italy, only in recent years has legislation has gradually come into alignment with European Commission policy directives. In particular, government proposed programs are supporting industrial research for the creation of economic and social value, and to reward firms, even small firms, that are capable of product and process innovation (Ciasullo and Monetta 2013).

The National Operational Program for “Research and Competitiveness” 2007–2013 (NOP for R&C) is Italy’s means of contributing to the development of a EU Cohesion Policy for Italy’s least-favored regions. In this regard, Italy and the EU have agreed that a significant amount of European Structural Funds should be invested in research and innovation to improve drivers of social and economic development. To this aim, the Italian Ministry of Education, University and Research (MIUR) and the Ministry of Economic Development (MiSE) have defined and implemented various measures for growth and development for which the EU has allocated resources. In particular, funding industrial research projects for the innovation of products and services of businesses in specific Italian areas has been contemplated to foster competitiveness (Rolfo and Calabrese 2006) by promoting sustainable development, diversifying specialization and strengthening sectors of excellence. A further objective concerns support measures for productivity and employment, the dissemination of entrepreneurial culture and the development of forms of self-employment and entrepreneurship. Innovative technology and product and process creativity is envisaged to foster new entrepreneurship especially in Italy’s disadvantaged areas. In short, MIUR and MiSE have allocated public funds to strengthen and enhance the entire chain of research and cooperation networks and the research system and businesses. Expected results are competitiveness and economic growth, dissemination and use of new technologies and advanced services, heightened level of scientific and technical knowledge and skills in the production system and in institutions.

With the directorial decree no. 1/Ric. of January 18, 2010, and by means of an open call, businesses were invited to submit industrial research projects in nine scientific and technological areas, including Information and Communication Technologies (ICT). The aim was to encourage knowledge and skills exchanges between Italy’s disadvantaged areas and the more advanced sectors of the country, The Head Office in Rome of the Poste Italiane, respecting indications and criteria, presented the TITAN project jointly with the University of Salerno, the CRMPA, public research organization, the Qui! Group, a large-scale business, and MOMA, a small business.

In 2011, MIUR selected several scientific and technological projects aimed at innovating business products, procedures and services and the TITAN project was considered eligible for financing (identification number: PON01_02136). A decisive factor in the selection of the projects was the demonstration of how the implementation and development of these enabling technologies would improve industry competitiveness and quality of life. The main funding support was based on how innovation in scientific research studies could be related to industrial development and how interventions which, on one hand, improve the focus on business innovation and development, and on the other, modify the factors that contribute to entrepreneurship, could improve national appeal and competitiveness (Lion, Martini, and Volpi 2004).

4 An Overview of the TITAN Project

The evolution of microchips and embedded technologies of the mobile world has led to the growth and proliferation of devices and systems for end users to buy and pay for products or services. Over the last few years, in the electronic payment landscape, the trend has been to provide users with electronic services, denominated value added services (VAS) as accessories to the payment for use on completion of the financial transaction (Pasquet et al. 2008). VAS in effect, digital services with payment included cover transport (tickets, monthly passes, etc.), health (booking health services and collecting medical data), government (tax and fees), etc. Besides conventional payment services, VAS have naturally become a new opportunity for providers to create revenue. In this respect, the use of integrated payment VAS is a fast-growing and powerful combination in the electronic payment market creating new sources of income for payment service providers, financial institutions, banks and major retail operators. To date, the vast array of user devices and instruments as well as acceptance devices and service platforms have tended to make life harder for new service providers and their users.

In this context, the main objective of the TITAN project is to create an integrated innovative model for managing a customer-centric “Electronic Money and Value Added Services multichannel” that satisfies both customers and service providers by defining a business partner (BP) network, modeled semantically that supports marketing policies and is facilitated by exploiting user profiles (D’Aniello, De Vivo, and De Rosa 2014).

The TITAN project furthermore addresses the complexity of payment services and VAS for delivery to end users through different channels such as smart cards or mobile apps based on user interests, localization and profile. In addition to these features, a layer of automated business cooperation is defined in order for merchants to publish new services through a common platform, rendering them discoverable at run-time by other merchants and also allowing them to define and shape composite products and services for delivery to end users. This approach has led to a common inter-partner platform, where the composite products and services are combined with the payment services and VAS provided by TITAN itself. In addition, the main benefits for the end-user consist of choosing different channels and devices for payment and VAS delivery. This helps to make the system flexible, improve customer experience and increment the purchase of services and goods.

In terms of future implications and impact on business, the main goal of the TITAN project is to explore new techniques to support a multi-service platform and analyze the critical issues involving the payment constraints in order to design a flexible architecture to follow the evolution of the modern business. In other words, the vision underpinning the TITAN project takes shape in the form of a platform enabling innovative business scenarios for e-money, e-payments and VAS, by means of key features able to support

access to platform services using multiple channels (Kiosk/ATM, PoS, PC, etc.) and devices (smart cards, apps, etc.);

interoperability among diverse products and services provided by internal and external partners to the platform (transport companies, health-care organizations, merchants, etc.);

listing of products and services offered by BPs through a semantic layer to improve product/service discovery and composition;

word of mouth recommendation of product and services through user profiling model.

TITAN overview.

The aim of the TITAN platform is to improve customer experience by means of user modeling and profiling methodologies in order to recommend, for example, suitable offerings on the basis of user needs, profiles and context information. Information is modified when the customer uses the platform (e.g. buys a service, searches for a product, etc.). Services provided by the platform to the customers are the result of service integration involving the elementary services offered by the platform (e.g. authentication, promotion manager, loyalty manager) with the services provided by the external BP (e.g. registry officer). The platform also enables integration and interoperability among BPs. Each BP can be seen as a domain, i.e. a set of resources such as procedures, data and services that define the boundary of responsibility. Each domain can export services to other domains or require services from other domains. Each BP can access the TITAN platform in order to register and sign service agreements with the platform. Another characteristic is the use of semantic technologies to describe product and service offerings based on ontologies able to model their characteristics (OWL-S, GoodRelations, domain ontologies). The use of semantic technologies and linked data principles enables innovative discovery methods for end users and flexible annotation capabilities of the product and service offerings provided by BPs. The platform also provides service delivery utilities by means of a service pass on the user’s device. The service pass is used to access real services purchased by the user (e.g. museum tickets, discount coupons). Services can be purchased either through the web (e.g. online payment) or through the acceptance device provided (and managed) by the platform itself. The acceptance devices can also be used to check the service pass.

Industrial research activities to date have been focused on the smart card industry i.e. characterized by a complex and expanding knowledge base. A smart card application requires not only the availability of chips and cards but also an extensive infrastructure of readers and terminals, which are part of an overall system and/or network architecture (M’Chirgui 2009). TITAN’s team has studied international protocol specifications, national and international certifications, user interaction models with which to improve customer experience, dynamic service composition and delivery and security services needed to handle and store sensible data, provide mechanisms for the generation and management of symmetric and asymmetric cryptography keys and not least, identity access management. An example is a museum ticket that can be bought with a payment card and then delivered to the card itself or to the user’s smart phone.

Some prototypes of the main findings identified in the TITAN project have already been realized and tested. Currently experimental validation of the whole platform is ongoing by means of advanced approaches modeled in a multi-channel and multi-service context.

The results obtained are encouraging and tend to confirm the validity and soundness of results and their potential implementation in a real multi-channel and multi-service platform. The main entrepreneurial innovation of this project is that of the integration of payment in the VAS by means of a new model delivering the VAS on a multi-application device during the same payment transaction. The latter result has led to a change request to ISO in order to allow the extension to VAS of the standard ISO 20022 related to electronic card payments (Bracaglia, Monetta, and Vanobberghen 2015). In this context, the submission of the request is being managed jointly with the Acquirer Working Group of EPASOrg. [1]

5 The New Model of Integrated Payment Service Delivery

The state of the art of electronic money systems indicates rapid evolution while respecting the basic concepts (Asokan et al. 1997) linked to electronic payment models and relative constraints and standardizations. The payments market in Europe offers great opportunities for innovation. The growing number of card payments demonstrates that consumers have already significantly changed their payment behaviors in recent years (Study on the impact of Directive 2007/64/EC on payment services and on the application of Regulation EC NO 924/2009 on Cross-border payments in the Community, Final report).

As technology develops, the range of devices and processes to transact electronically continues to multiply while the percentage of cash and check transactions continues to decrease (Bruggink, Karsten, and de Meijer 2012). Electronic payments involve both the payer and the payee. (Merchant) and the purpose of electronic payment protocols are to transfer monetary value from the payer to the payee. The process also involves financial institutions. Typically, financial institutions participate in payment protocols in a two-way system: as an issuer (interacting with the payer) and as an acquirer (interacting with the payee). The issuer is responsible for validating the payer during account registrations and holds the payer’s account and assets. The acquirer holds the payee’s account and assets. The payee deposits the payments received during a transaction with the acquirer. The acquirer and the issuer then proceed to perform an inter-banking transaction for clearance of funds (Junxuan 2010, 339). The issuer and the acquirer can be from the same financial institution.

Figure 2 shows the participating entities in an e-payment system.

e-Payment model.

Credit cards, debit cards and prepaid cards currently represent the most common model of electronic payments. For all three types of cards the consumer or the business usually uses a smart card, plastic cards in the main with an embedded computer chip. For buying goods or services, the cardholder gives his or her card to a merchant who inserts the card in an acceptance device, commonly called PoS. The terminal transmits data to the cardholder’s bank, the acquirer. The acquirer transmits the data through a card association with the card issuer who makes a decision on the transaction and relays it back to the merchant, who gives goods or services to the cardholder. Funds flow later for settlement with credit cards and are debited immediately for debit or prepaid cards.

Other parties that may be present in a payment protocol include certification authorities who are necessary if the e-payment systems involve public key infrastructure. They issue public key certificates to entities involved in a payment protocol so that their authenticity can be publicly verified. Certain payment systems might involve more players such as payment gateways (PG) who are entities acting as a medium for transaction processing with other entities (e.g. MasterCard, Visa).

The new model proposed comprises a new key feature: the TITAN platform is an intermediary agent with the ability to perform both payment and VAS management in a single transaction contextually, introducing into the system a new actor called the service provider. The latter is a firm or an organization (public administration, transport operator, shopper, etc.) “that provides goods, facilities or services to the public, whether paid for or free, no matter how large or small the organization is.”

Currently, among multi-application service-oriented systems numerous proposals and solutions (Ling and Hang 2011; Wada et al. 2001; Donsez, Lecomte, and Jean 2001) abound for various application domains such as e-government, multi-service smart cards, ticketing and couponing services, etc. e-Government, for example, is closely linked to e-payment and VAS applications by virtue of the requirement for public administrations to make available electronic payments for services provided (e.g. payment of taxes and fees), in order to facilitate the relationship that companies and citizens have with the public administration.

The key feature of the platform as illustrated above is the ability to perform both a payment and a VAS transaction contextually, through an extended version of ISO 20022 messages [2]. The International Organization Standard for Financial Services Messaging provides the financial industry with a common platform for the development of messages in standardized syntax. Device-oriented electronic money systems, which have been detected, are now turning their focus to smart cards (Song and Sheng 2009) and mobile apps (Asghar Amidian et al. 2010), etc. Over time, the chip for payment will be moved onto other devices. A “smart card” might then become the computer chip in a phone, PDA or other device that can perform the same function as chip in a plastic card, eliminating the need for the plastic card itself. Smart cards could thus evolve into “smart phones,” “smart PDAs” or other “smart” devices.

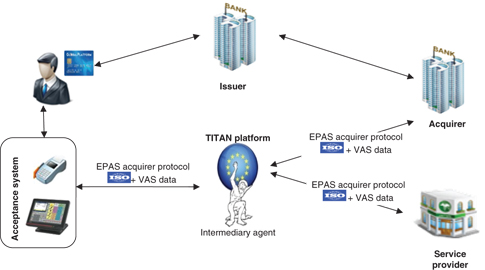

In short, the innovative model proposed defines new business processes and roles such as an acceptance system, a TITAN intermediary agent, service provider and acquirer using the extended version of EPAS acquirer protocol (Figure 3).

Payment and contextual VAS delivery.

The platform provides utilities for delivery by means of the service pass on the user’s device (Figure 4). The service pass is used to access real services purchased by the user (e.g. museum ticket, discount coupons). Service is purchased through the acceptance device provided and managed by the platform itself. Acceptance devices can be used also to check the service pass.

Service pass on user’s card.

The novelty of this innovative card payment model lies in the competitive advantage it offers compared to other systems in the payment market place. Currently no systems exist that bring together the features of a payment system infrastructure and the integration of diverse services, while managing the entire life cycle of payments and VAS. Besides issuing electronic money instruments, the model deals with upgrading, the dynamic loading of VAS, the acquiring of authorization for transactions, reporting, monitoring and implementing loyalty programs, etc.

5.1 A Use Case: The EPAS Protocol Extension

The main result of cooperation between the EPASOrg Acquirer Working Group and TITAN’s team is the proposal extension of the acquirer EPAS protocol in order to manage VAS integrated with payment. a small demo was completed of a transaction carried out using a post-personalized java chip card where the cardholder could integrate with VAS applications within the card, new payment applications such as public transport, access to museums, etc.

Below a simulated scenario is presented where a cardholder desires to renew his/her monthly city train pass. The preliminary requirement is that the card contains payment and VAS applications and that service delivery (monthly city train pass) is on the multi-application card.

The steps, with reference to Figure 3, are as follows:

Cardholder shows his/her multi-application card to the merchant and requests a monthly city train pass for delivery on the same device.

Merchant inserts card in acceptance system and starts the payment and VAS transaction using its PoS.

An extended ISO 20022 message is sent to the platform, which acts as an intermediary agent for the acquirer, i.e. responsible for authorization of payment and for the service provider, i.e. responsible for the ticketing service.

The platform splits the message into two parts: a financial request to the acquirer and a VAS request to the service provider.

The answer to the payment authorization is sent back to the platform. If the authorization is rejected the transaction simply ends uncompleted.

With a positive answer, the payment transaction can be fully completed for the service provider.

Once it receives the response from both service provider and acquirer, the platform aggregates the responses and sends a unique response to the acceptance system.

PoS terminal can execute the delivery of the required service on the multi-application card.

Cardholder uses his/her multi-application card to access the urban train pass purchased (Figure 4).

The final element of the scenario proposed is related to ticket delivery service. In the simulated scenario the user decides to buy the ticket from a merchant using his/her smart card and contextually choosing the same smart card as a delivery device. This process is possible using the extended ISO 20022 protocol that allows the request/response message to contain both payment transaction details and VAS details (see Figure 3). Given that TITAN is a multichannel platform, the user consequently can choose different payment or delivery devices (e.g. payment by ATM or delivery on smart phone), if BP allows the user to use the same device.

6 Conclusions and Implications for Enterprise

Rather than a point of arrival, the findings and project results represent a starting point for further investigation and practical developments for enterprise.

The novelty of the paper lies in its validation of how entrepreneurship can be improved in the EU member states by means of public and EU-funded R&D projects. Moreover, empirical evidence confirms that the innovative process using new technologies and integrated business model proposed necessitate EU public support. The TITAN project is an example of how systematic research activity can generate a virtuous circle of technological improvements and entrepreneurial innovation.

The specific aim of the proposal is to contribute to developing an EU-wide market for payments to enable consumers, merchants and other market players to enjoy to the full the benefits of innovative and integrated payment services. In other words, what is suggested is a scenario where cardholders are able to acquire a service and pay for it with the same card and where accredited “merchants,” in a single transaction, accept the card on their own PoS terminal and deliver the service paid for, earning at the same time, commission for two transactions, i.e. both from the acquirer bank and the service provider.

From a business viewpoint, impacts and expected benefits regard both service providers and payment service providers as the EPAS protocol extension enhances competitiveness by increasing profitability and reaching more customers. In other words, for “merchants,” market expansion is fostered and the creation of an integrated, competitive and innovative market for retail payments is facilitated (Leinonen 2010). Last but not least, cardholders can access services (both payment and VAS) by means of a single multi-application card paying via an acceptance system (PoS, ATM, Kiosk, etc.).

In this context, standardization is crucial, not only as regards the payment market. At the same time, the benefits of better market integration and reduced fragmentation in this field at European level would be substantial. A new model of integrated payment service delivery through the EPAS protocol extension could satisfy regulatory pressure in Europe and, at the same time, contribute to devising universal norms in line with Europe 2020 and the Digital Agenda. The policy of harmonizing the existing fragmented landscape of national retail payment systems, schemes and formats has been strongly supported by the EU Commission, the European Central Bank (ECB) and the European Parliament and Council (Wandhöfer 2011). Moreover, the ECB and Eurosystem also strongly support the integration of payment services in Europe to generate cost savings and gains in productivity and to foster industrial growth. A shift from cash to electronic payments is also a relevant objective of Single Euro Payments Area (SEPA) initiatives. Political and strategic imperatives to reduce cash usage are the best way of controlling tax evasion and noncompliance activities within a national fiscal system. Furthermore, the revised draft of the Payment Services Directive (proposal for directive of the European Parliament Council on payment services in internal markets) stipulates that standards should be developed by industry and fit into the global context.

The innovative and original features of the new model proposed in this paper would enable everyone to make e-payments to anyone located anywhere in the EU using a single smart card based on a single set of standards and business rules. In other words, both payments and VAS delivery defining business rules can thus be standardized also for other service providers in order to promote market access for new non-payment service players. Thus, entrepreneurial innovation can be fostered thanks to public and EU-funded R&D projects and the TITAN project is an indicative case in point.

Funding statement: Funding: The authors would like to thank the Italian Ministry of University and Research for supporting the Project “TITAN – System for e-Money and Multi-Channel Value Added Service,” PONREC 2007–2013, number PON01_02136.

About the authors

Antonio Bracaglia is technical manager of TITAN Project and he is professional master at Poste Italiane Information Technology – E-payments Dept. He is mainly involved in R&D e-payments EU projects as CTO. Antonio has extensive professional experience in different sectors in the Card Payment Industry, managing and maintaining relationships with payment service providers and solution providers. For many years, he has been working on e-payments products and SEPA initiatives related to standardization, namely on the following issues: definition of security and functional requirements for new payment products, certification and type approval processes, implementation and testing of new protocols, risk analysis and risk assessment.

Giulia Monetta is temporary researcher at Department of Management and Information Technology, University of Salerno (Italy). She has worked in TITAN Project for Poste Italiane. Her current research interests are aimed to analyze the role of public governments can play in contributing to the development of entrepreneurial culture. Giulia has a PhD in public management and her principal research themes regarding strategic management and corporate governance of public and private firms. Her publications are the result of empirical and industrial research and are published in academic and professional journal such as Total Quality Management and Business Excellence.

William Vanobberghen is secretary general of EPASOrg (Electronic Protocols Application Software) and he is head of International Projects at Groupement des Cartes Bancaires. He initiated and co-ordinated the EPAS initiative. William has been co-ordinating various international projects funded by the European Commission in the framework of research and development programs in the field of information technology. William is in charge of the coordination of international projects of co-operation related to card payments. He also launched the first ISO 20022 – standardization initiative in card payments. William holds a degree in commercial and financial sciences as well as a degree and master in computer sciences. He also holds an executive MBA from HEC Paris.

References

Acs, Z., E.Autio, and L. A.Szerb. 2013. “Entrepreneurship and Policy: The National System of Entrepreneurship in the European Union and in Its Member Countries.” Entrepreneurship Research Journal3 (1):9–34.Search in Google Scholar

Amidian, A. A., J.Muhammadi, H.Rabiee, and A. M.Tehrani. 2010. “A Survey of System Platforms for Mobile Payment.” Paper presented at the 4th International Conference on Data Management of e-Commerce and e-Government (ICMECG), 367–81.Search in Google Scholar

Asokan, N., P.Janson, M.Steiner, and M.Waidner. 1997. “State of the Art in Electronic Payment Systems.” IEEE Computer30 (9):28–35.10.1109/2.612244Search in Google Scholar

Bracaglia, A., G.Monetta, and W.Vanobberghen. 2015. “Innovative Model of Service Delivery to Improve Standardization and Market Integration. Extension Framework for ISO 20022 Card Payments.” Journal of Payments Strategy & Systems8 (2):1–15.Search in Google Scholar

Bruggink, D., P.Karsten, and C. R. W.de Meijer. 2012. “The European Cards Environment and ISO 20022.” Journal of Payments Strategy & Systems6 (1):80–99.Search in Google Scholar

Ciasullo, M., and G.Monetta. 2013. “Commercial Spinoffs Generated by Italian Universities: An Empirical Analysis.” In Rethinking Innovation. Global Perspectives, edited by R.Subramanian, M.Rahe, V.Nagadevara, and C.Jayachandran, 79–117. London: Routledge.Search in Google Scholar

Covin, J. G., and D. P.Slevin. 1991. “A Conceptual Model of Entrepreneurship as Firm Behaviour.” Entrepreneurship Theory and Practice16 (1):7–25.10.1177/104225879101600102Search in Google Scholar

Donsez, S., D.Lecomte, and S.Jean. 2001. “Using Some Database Principles to Improve Cooperation in Multi-Application Smart Cards.” Proceedings of XXI International Conference of the Chilean, Computer Science Society, 154–160.Search in Google Scholar

Drucker, P.1985. Innovation and Entrepreneurship: Practices and Principles. New York, NY: Harper & Row.Search in Google Scholar

D’Aniello, G., A.De Vivo, and A. C.De Rosa et al. 2014. “A Semantic-Based Architecture for Electronic Money System and Multi-channel Value-Added Services.” Paper presented at 6th International Conference on Intelligent Networking and Collaborative Systems, September 10–12.Search in Google Scholar

EPAS. 2014. “Electronic Protocol Software Applications Organization.” Accessed September 19, 2014. http://www.epasorg.eu/.Search in Google Scholar

Global Entrepreneurship Monitor. “Global Report 2012.” Accessed September 19, 2014. http://www.gemconsortium.org/docs/2645/gem-2012-global-report.Search in Google Scholar

Hayek, F. A. V.1945. “The Use of Knowledge in Society.” American Economic Review35 (4):33–54.Search in Google Scholar

Hills, S. B., and S.Sarin. 2003. “From Market Driven to Market Driving: An Alternative Paradigm for Marketing in High Technology Industries.” Journal of Marketing Theory and Practice11 (3):13–24.10.1080/10696679.2003.11658498Search in Google Scholar

Howard, S. H., and J. J.Carlos. 1990. “A Paradigm of Entrepreneurship: Entrepreneurial Management.” Strategic Management Journal11 (5):17–27.Search in Google Scholar

ISO 20022. 2014. “Universal Financial Industry Message Scheme.” Accessed September 19, 2014. http://www.iso20022.org/.Search in Google Scholar

Junxuan, Z.2010. “Research on E-Payment Model.” Proceedings of International Conference on E-Business and E-Government, 339–41.Search in Google Scholar

Kirzner, I. M.1997. “Entrepreneurial Discovery and the Competitive Market Process: An Austrian Approach.” Journal of Economic Literature35 (1):60–85.Search in Google Scholar

Kumar, N., L.Scheer, and P.Kotler. 2002. “From Market Driven to Market Driving.” European Management Journal18 (2):129–42.Search in Google Scholar

Leinonen, H.2010. “Transparent Price Competition or Two-Sided Subsidization in Card Payments? Is There a Need for a More Efficient Business Model for the Card Industry?.” Journal of Payments and Strategy & Systems4 (2):102–15.Search in Google Scholar

Ling, Li., and D.Hang. 2011. “Building a Change Management Model for E-Government Services Evolution.” Paper presented at International Conference on Management of e-Commerce and e-Government, 87–92.Search in Google Scholar

Lion, C., P.Martini, and S.Volpi. 2004. “The Evaluation of European Social Fund Programmes in a New Framework of Multilevel Governance: The Italian Experience.” Regional Studies38:207–12.10.1080/0034340042000190172Search in Google Scholar

Littlechild, S. C.1986. “Three Types of Market Process.” In Economics as a Process, edited by R. N.Langlois. Cambridge: Cambridge University Press.Search in Google Scholar

Lumpkin, G. T., and G. G.Dess. 1996. “Clarifying the Entrepreneurial Orientation Construct and Linking It to Performance.” Academy of Management Review21:135–72.10.2307/258632Search in Google Scholar

M’Chirgui, Z.2009. “Dynamics of R&D Networked Relationships and Mergers and Acquisitions in the Smart Card Field.” Research Policy38: 1453–67.10.1016/j.respol.2009.07.002Search in Google Scholar

Narver, J. C., S. F.Slater, and D. L.MacLachlan. 2004. “Responsive and Proactive Market Orientation and New-Product Success.” Journal of Product Innovation Management21:334–47.10.1111/j.0737-6782.2004.00086.xSearch in Google Scholar

National Operational Programme for Research and Competitiveness.2007–2013. Accessed April 8, 2014. http://www.ponrec.it/en.Search in Google Scholar

OECD. 2006. “Understanding Entrepreneurship: Developing Indicators for International Comparisons and Assessments.” Statistics Directorate Committee on Statistics, May.Search in Google Scholar

Parker, S.2005. “The Economics of Entrepreneurship: What We Know and What We Don’t.” Foundations & Trends in Entrepreneurship1 (1):1–55.10.1561/0300000001Search in Google Scholar

Pasquet, M., S.Vernois, W.Aubry, and F.Cuozzo. 2008. “Electronic Payments.” In Encyclopedia of Information Science and Technology, edited by Mehdi Khosrow-Pour, 2nd edn, 1341–8. PA: Idea Group, Hershey.10.4018/978-1-60566-026-4.ch212Search in Google Scholar

Rolfo, S., and G.Calabrese. 2006. “From National to Regional Approach in R&D Policies: The Case of Italy.” International Journal Foresight and Innovation Policy2 (3/4):345–62.10.1504/IJFIP.2006.010408Search in Google Scholar

Schindehutte, M., M. H.Morris, and A.Kocak. 2008. “Understanding Market-Driving Behavior: The Role of Entrepreneurship.” Journal of Small Business Management46 (1):4–26.10.1111/j.1540-627X.2007.00228.xSearch in Google Scholar

Schumpeter, J.1934. The Theory of Economic Development: An Enquiry into Profits, Capital Credit, Interest and Business Cycle. Cambridge, MA: Harvard University Press.Search in Google Scholar

Shackle, G. L. S.1979. Imagination and the Nature of Choice. Edinburgh: Edinburgh University Press.Search in Google Scholar

Shane, S.2005. “Government Policies to Encourage Economic Development through Entrepreneurship: The Case of Technology Transfer.” In Economic Development through Entrepreneurship. Government, University and Business Linkages, edited by S.Shane, 33–49. Northampton: Edward Elgar.Search in Google Scholar

Shane, S., and S.Venkataraman. 2000. “The Promise of Entrepreneurship as a Field of Research.” Academy of Management Review25 (1):217–26.10.5465/amr.2000.2791611Search in Google Scholar

Singh, M.2002. “E-Services and Their Role in B2C e-Commerce.” Managing Service Quality: An International Journal12 (6):434–46.10.1108/09604520210451911Search in Google Scholar

Song, J. B., and C. Y.Sheng. 2009. “Contemporary Bank Card Solution Models.” Paper presented at International Conference on Information Management, Innovation Management and Industrial Engineering, December 26–27.Search in Google Scholar

Stevenson, H. H. and Jarillo, J. C.1990. “A Paradigm of Entrepreneurship: Entrepreneurial Management.” Strategic Management Journal11 (5): 17–27.Search in Google Scholar

Subramanian, R., and Rahe, M., and Nagadevara, V. and Jayachandran, C. eds. 2013. Rethinking Innovation. Global Perspectives. London: Routledge.Search in Google Scholar

Vallini, C., and C.Simoni. 2009. “Market-Driven Management as Entrepreneurial Approach.” Symphonya. Emerging Issues in Management1:26–39. Accessed September 18, 2014. doi:10.4468/2009.1.03vallini.simoni.10.4468/2009.1.03vallini.simoniSearch in Google Scholar

Wada, R., Y.Hirata, S.Suzuki, and K.Toji. 2001. “A Network-Based Platform for Multi-Application Smart Cards.” Proceedings of the 5th IEEE International Conference on Enterprise Distributed Object Computing (EDOC), 34–45.Search in Google Scholar

Wandhöfer, R.2011. “The Next Chapter of EU Payments Harmonisation: SEPA Gets Real.” Journal of Payments Strategy & Systems5 (1):6–16.Search in Google Scholar

Wennekers, A. R. M., and A. R.Thurik. 1999. “Linking Entrepreneurship and Economic Growth.” Small Business Economics13 (1):27–55.10.1023/A:1008063200484Search in Google Scholar

©2015 by De Gruyter

Articles in the same Issue

- Frontmatter

- Editors’ Corner

- The Role of Sunk Cost and Slack Resources in Innovation: A Conceptual Reading in an Entrepreneurial Perspective

- Competitive Research Articles

- Identify Innovative Business Models: Can Innovative Business Models Enable Players to React to Ongoing or Unpredictable Trends?

- Public Research Support for an Innovative Integrated Payment Model of Service Delivery

- Balancing Risk and Learning Opportunities in Corporate Venture Capital Investments: Evidence from the Biopharmaceutical Industry

Articles in the same Issue

- Frontmatter

- Editors’ Corner

- The Role of Sunk Cost and Slack Resources in Innovation: A Conceptual Reading in an Entrepreneurial Perspective

- Competitive Research Articles

- Identify Innovative Business Models: Can Innovative Business Models Enable Players to React to Ongoing or Unpredictable Trends?

- Public Research Support for an Innovative Integrated Payment Model of Service Delivery

- Balancing Risk and Learning Opportunities in Corporate Venture Capital Investments: Evidence from the Biopharmaceutical Industry