Corporate Profit Tax and Strategic Corporate Social Responsibility Under Foreign Acquisition

-

Lili Xu

Abstract

This study investigates government public policies facing competing firms’ strategic corporate social responsibility (CSR) activities and finds that the choice of CSR crucially depends on corporate profit tax. We demonstrate that strategic CSR decreases while social welfare increases with corporate tax. When the government grants uniform output subsidies, we show that bilateral CSR leads to a lower CSR level than under unilateral CSR but bilateral CSR is always beneficial to society. However, when the government grants discriminatory output subsidies which yield different levels of unilateral CSR, we show that domestic CSR leads to a lower CSR level than under foreign CSR. In an endogenous CSR choice game, domestic CSR (no CSR) is a Nash equilibrium when corporate tax is low (high) under the uniform subsidy, while foreign CSR could be a Nash equilibrium when corporate tax is low under the discriminatory subsidy.

1 Introduction

As globalization increasingly prevails, domestic industries in most countries are concentrated by a few large foreign-owned firms, which account for a substantial share of aggregate international trade.[1] The acquisition of domestic firms’ stocks by those firms is also a widespread, visible phenomenon.[2] For example, the French automotive company Renault acquired a 36.8% equity stake in Nissan Motor in 1999. There are more recent examples in the global energy, airline, and steel industries in the world. In the last decade, we have witnessed a rapid development of new energy vehicles. According to the electric vehicle world sales database, the world annual sales volume was 10,000 units in 2012, while it quickly increased to two million units in 2018. In particular, China’s new energy vehicle sales accounted for 56% of global sales, which can be attributed to the sustainable fiscal subsidies provided by the Chinese government since 2013. As the champion in global energy vehicle sales ranked by OEM group 2018, the American Tesla Motors decided to build factories in China in 2018 to compete with some local new energy vehicle companies, such as BYD, Basic BJEV, et al.

In the process of globalization, on the other hand, the popularity of corporate social responsibility (CSR) by global firms has also grown rapidly in recent years.[3] Some practical examples include GE’s Ecomagination program, Nestlé’s Creating Shared Values, and Unilever’s Simple Living Plan. Furthermore, it is becoming more common to suggest global standards of international CSR for global firms. For example, the European Commission promotes CSR in the EU and encourages foreign-owned firms to adhere to international guidelines and principles. The Global Reporting Initiative provides a globally applicable framework for drawing up sustainability reports in accordance with internationally recognized criteria.[4]

Both international acquisitions and CSR activities by foreign-owned firms have now become imperative global business strategies. As they have significant welfare implications on the design of government policies, recent research on international oligopoly markets with heterogeneous objective functions has analyzed different forms of market competition where profit-maximizing private firms may compete with other private firms that have adopted various CSR activities.[5] Accordingly, recent theoretical studies have also examined the effect of CSR on tariffs and welfare in international trade, such as Wang, Wang, and Zhao (2012), Chang et al. (2014), Manasakis, Mitrokostas, and Petrakis (2018), Liu, Wang, and Chen (2018), and Xu and Lee (2019). However, these works took the level of CSR as an exogenously given variable that was a normative goal established in the social contract.

From a shareholder’s viewpoint, CSR is an instrument of the firm’s choice variables to engage in a global business strategy that reflects a management’s incentive contracts. For example, Starbucks increases its demand by buying fair-trade coffee and tea, and other firms heavily advertise their organic products. This enhances their reputations and increases the firms’ values. Similarly, some foreign-owned firms focus a fair amount of attention on image signaling concerns, and thus provide incentives for employee engagement in community service, which boosts their public relations with local communities and attracts motivated employees in the home country.[6] Accordingly, recent papers have formulated a model of strategic choice of CSR from the strategic motivation of adopting CSR behaviors, and showed that profit maximization could motivate a firm to engage in CSR.[7] To our knowledge, however, studies on the foreign-owned firms’ strategic utilization of CSR initiatives under international acquisitions and the interactions with governmental policies are limited.

There are several definitions used in the CSR literature, even for the purpose of the profit-maximizing or so-called “business” case.[8] Moreover, CSR incentive contracts may reflect different corporate governance, resulting from different interest group controls, in which consumer interest is important (Königstein and Müller 2001; Planer-Friedrich and Sahm 2018). As an interesting case of strategic CSR in a market transaction, we regard consumer surplus as a proxy for CSR, which is widely accepted in the literature.[9] In this case, the firm with CSR activities is defined as a profit-oriented private firm with a concern for consumer surplus as a CSR initiative.

This paper investigates the strategic relationship between consumer-oriented CSR initiatives and international acquisition, and examines the effect of government policies on strategic CSR. In particular, we address the strategic motivations for CSR arising from the interactions between domestic and foreign-owned firms under government public policies such as corporate profit taxes and (uniform or discriminatory) output subsidies.[10] Interestingly, we show that there exists the strategic effect of corporate profit tax on the strategic CSR and output subsidy policy.[11] This finding is important to the policymakers because, in the literature of microeconomics, corporate profit taxes are neutral toward firm behaviors.

In a duopoly model of Cournot competition, we examine the governmental policies facing firms’ strategic CSR activities and summarize our findings as follows: First, the strategic level of CSR decreases while social welfare increases with corporate tax. Second, unilateral CSR case in which only one firm adopts CSR leads to a higher level of CSR than that under bilateral CSR case in which both firms adopt CSR. Third, the optimal output subsidy increases with corporate tax while it decreases with foreign penetration, and the optimal output tax is possible when the foreign penetration is high and the corporate tax is low. Fourth, the welfare effects of CSR crucially depend on both corporate profit tax and foreign acquisition, but bilateral CSR always yields the highest welfare irrespective of corporate tax or foreign penetration. Fifth, we consider an endogenous choice game of CSR between the two firms and examine the equilibrium choice of CSR. When each firm decides whether to engage in CSR at the beginning of the game, we show that domestic CSR (no CSR) is a Nash equilibrium when corporate tax is low (high). Finally, we consider a discriminatory subsidy where the government grants different subsidies to the firms. We find that foreign CSR (no CSR) is a Nash equilibrium when corporate tax is low (high) in an endogenous choice game of CSR under the discriminatory subsidy; however, neither is socially desirable. Therefore, an appropriate regulatory framework for CSR guidelines is necessary in certain cases with a lower corporate tax.

The remainder of this paper is organized as follows. Section 2 presents the basic model of Cournot competition in which a domestic firm and a foreign-owned firm compete with CSR initiatives under output subsidy and corporate tax policies. We then analyze the market equilibrium under different choices of CSR in Section 3. We then compare the equilibrium outcomes among the four models and extend to an endogenous choice game of CSR in Section 4. In Section 5, we further examine the discriminatory subsidy. Finally, Section 6 concludes the paper.

2 The Model

We consider a duopoly market with two private firms that produce homogeneous products, but with possibly different objectives. Firm 1 and firm 2 are the pure profit-oriented private firms and both of them might engage in CSR activities. We assume that firm 1 is a domestic firm fully owned by domestic investors, while firm 2 is a foreign firm owned by both domestic and foreign investors.[12]

Inverse demand is given by: p = 1 − Q, where Q = q

1 + q

2 is the market output and q

1 and q

2 denote the quantities supplied by domestic firm 1 and foreign-owned firm 2, respectively. The cost function of firm i is identical and given as:

The profits of the firms are as follows:[15]

It is assumed that each firm maximizes its profit as a pure private firm, and both of them can strategically choose profit-oriented CSRs. In particular, we assume that the firm is in a managerial delegation contract in which output production decisions are delegated to a manager. That is, the owner of the firm specifies a degree of CSR as an incentive contract with the manager to maximize the profit.[16] In this managerial delegation contract, the manager is assumed to maximize the profit of the firm plus a fraction of consumer surplus in output production that is imposed by the owner. Thus, the objective function of the manager of the firm is given as follows:

where α

i

∈ [0, 1] represents the level of CSR of firm i and

Considering the share of foreign ownership, we define producer surplus as: PS = π

1 + (1 − β)π

2, where β ∈ (0, 1] is the foreign penetration in the foreign-owned firm, which can be potentially affected by policymakers acting on capital liberalization.[17] We define domestic welfare as the sum of consumer surplus, producer surplus, and tax revenue,

This study considers different scenarios regarding the choice of CSR unilaterally or bilaterally under government policies in a certain industry. In particular, when the two firms decide whether to engage in CSR activities or not in the beginning, we classified with four scenarios: “bilateral CSR” where both firms adopt CSR bilaterally, “domestic CSR only” or “foreign CSR only” where either one of two firms adopts CSR unilaterally, and “no CSR” where no firms adopt CSR. In each scenario, the timing of each game is as follows. In the first stage, the government decides the level of output subsidy. In the second stage, given the level of subsidy s, the firm chooses the level of CSR to maximizes its own profit.[18] In the final stage, given the level of CSR α i , both firms compete in quantities. We solve the subgame perfect Nash equilibrium using backward induction.

3 The Analysis

3.1 Bilateral CSR

We consider a bilateral case in which two firms simultaneously engage in CSR activities. In the last stage, both firms choose the outputs. For a domestic firm, the differentiation of V 1 in Eq. (2) with respect to q 1 yields[19]

For a foreign-owned firm, the differentiation of V 2 in Eq. (2) with respect to q 2 yields

From Eqs. (4) and (5), we obtain the following equilibrium outputs:

The profits of the domestic and foreign-owned firms are respectively

In the second stage, each firm chooses the level of CSR to maximize the profits in (7). The differentiation of π i in Eq. (7) with respect to α i yields

Note that the strategic CSR activities can be strategic complements or strategic substitutes, depending on the level of corporate tax, that is,

Combining two reaction functions in Eq. (8), we have the optimal level of CSR of the firm:

where superscript “B” represents the equilibrium outcome under Bilateral CSR and i = 1, 2. From Eq. (9), both firms adopt the same level of CSR where

The resulting social welfare is

In the first stage, the government chooses the level of subsidy to maximize social welfare. The differentiating of W in Eq. (10) with respect to s yields

Then, we have that

The equilibrium market output and price are

Note that the market output increases with corporate tax, while decreases with foreign penetration, for instance,

The profit of the firm is, respectively

Note that the profit of the firm decreases with corporate tax rate and foreign penetration, that is,

Finally, the social welfare is

Note that the welfare increases with corporate tax, but decreases with foreign penetration, for instance,

3.2 Domestic CSR Only

We consider one unilateral case in which only domestic firm engages in CSR activities. In the last stage, substituting α 2 = 0 into Eqs. (6) and (7) yield the following profit of the domestic firm:

In the second stage, the differentiation of π 1 in Eq. (15) with respect to α 1 yields

where superscript “D” represents the equilibrium outcome when only Domestic firm engages in CSR activities. From Eq. (16), domestic firm always adopts CSR activities where

The resulting social welfare is

In the first stage, the differentiating of W in Eq. (17) with respect to s yields

From Eq. (18), we have that

The equilibrium market output and price are

Note that the market output increases with corporate tax, while it decreases with foreign penetration, that is,

The profit of the firm is respectively

Note that the profit of the firm decreases with corporate tax rate and foreign penetration, namely,

Finally, the social welfare is

Note that the welfare increases with corporate tax, but it decreases with foreign penetration, that is,

3.3 Foreign CSR Only

We consider the other unilateral case in which only foreign-owned firm engages in CSR. In the last stage, substituting α 1 = 0 into Eqs. (6) and (7) yields the following profit of the foreign-owned firm:

In the second stage, the differentiation of π 2 in Eq. (22) with respect to α 2 yields

where superscript “F” represents the equilibrium outcome when only Foreign-owned firm engages in CSR activities. From Eq. (23), foreign-owned firm always engages in CSR where

The resulting social welfare is

In the first stage, the differentiating of W in Eq. (24) with respect to s yields

From Eq. (25), we have that

The resulting market output and price are

Note that the market output increases with corporate tax, while it decreases with foreign penetration.

The profits of the firms are respectively

Note that the profits of firms decrease with corporate tax rate and foreign penetration. In addition, note that foreign-owned firm engaged in CSR only always earns more profit than that of the domestic firm under the output subsidy, for instance,

Finally, the social welfare is

Note that social welfare increases with corporate tax but decreases with foreign penetration.

3.4 No CSR

We finally consider a case in which no firm engages in CSR. In the last stage, substituting α i = 0 into Eq. (6), we can obtain the output of the two firms. Thus, the resulting social welfare is:

In the first stage, the differentiating of W in Eq. (29) with respect to s yields

where superscript “N” represents the equilibrium outcome when No firm engages in CSR activities. From Eq. (30), we have that

The equilibrium market output and price are

Note that the market output increases with corporate tax, while it decreases with foreign penetration.

The profit of the firm is respectively

Note that the profit of the firm decreases with corporate tax rate and foreign penetration.

Finally, the social welfare is

Note that the welfare increases with corporate tax, but it decreases with foreign penetration.

4 Comparisons and Discussions

4.1 Comparisons

We first compare the results in each equilibrium and provide some findings on the strategic levels of CSR and relations with government policies.[20]

Proposition 1:

The unilateral CSR leads to a higher level of CSR than that under bilateral CSR.

Proposition 1 states that the competitive choice of strategic CSR in which both firms engage in CSR activities simultaneously leads to a lower level of CSR than the unilateral case in which only one firm engages in CSR activities. This is because the firm that engages in CSR can be more aggressive and thus can produce more output to enlarge its market share and improve its profit under quantity competition. However, this effect softens when the rival firm also adopts CSR to increase output, which will produce too much output thereby flooding the market.

Proposition 2:

The strategic CSR decreases with corporate tax, while it is independent of output subsidy and foreign penetration.

Proposition two states that under a higher corporate tax, both firms choose a lower level of CSR and produce less output, that is, there is a negative relationship between CSR strategy and corporate tax policy.[21] This result implies that the corporate tax can affect market outcomes, which might distort allocation efficiency through output production in the presence of strategic CSR. This is an interesting policy finding. In the previous literature without CSR, it is well known that corporate tax is neutral to the firm’s product strategy in the market; and thus, allocation efficiency is independent of corporate tax rate. However, the corporate tax policy is crucial for the government to improve welfare when the firm can choose the level of CSR strategically. On the other hand, the subsidy policy does not affect the decision of CSR for the firms. This result is also interesting in that the firm’s strategic decision of CSR to increase the output is neutral to the government’s subsidy policy to encourage the firms to produce more output. This implies that the output subsidy policy has a direct effect on the output, but does not have an indirect effect on the output through CSR strategies.

Proposition 3:

(i) The optimal output subsidy increases with corporate tax and decreases with foreign penetration; (ii) The output tax is optimal when the foreign penetration is high and corporate tax is low enough.

The first part of Proposition 3 represents that the output subsidy and corporate tax policies are complements; an increase in corporate tax leads to a higher output subsidy at equilibrium. However, the government’s policies between output subsidy and foreign ownership are strategic substitutes: an increase in foreign penetration leads to a lower domestic surplus, thus resulting in a lower subsidy at equilibrium. The second part of Proposition 3 indicates that when the foreign investors become major stakeholders of the foreign-owned firm, but the corporate tax rate is low, the government can impose an output tax on the firm, instead of subsidy. Since the foreign-owned firm with a higher foreign penetration (more than 50%) does not contribute to the producer surplus when the corporate tax is low enough, the government has to shrink the quantities produced by the foreign-owned firm by charging a negative output subsidy.

Lemma 1:

The ranks of optimal output subsidies among the four models are as follows:

Lemma 1 shows the policy relationships between the output subsidy and corporate tax rates. Then, we can summarize the findings in Lemma 1 as follows: (a) min{s

D

, s

N

} > max{s

B

, s

F

}, (b)

Second, (b) domestic CSR requires a higher subsidy when the corporate tax is low, while no CSR requires a higher subsidy when the corporate tax is relatively high. In particular, when the corporate tax is low enough, namely, 0 < τ < τ 1 < τ N , we have that s N < s D < 0. Thus, the government imposes an output tax on both firms where that under no CSR is higher than that under domestic CSR. Moreover, we have that s N ≥ 0 > s D when τ N ≤ τ < τ D . That is, when the corporate tax is intermediate, the government imposes an output tax on two firms under domestic CSR and provides an output subsidy to two firms under no CSR. However, when the corporate tax is high enough, for instance, τ D ≤ τ < 1, we have that s N > s D ≥ 0. Thus, the government provides an output subsidy to both firms where that under no CSR is higher than that under domestic CSR.

Finally, (c) bilateral CSR requires a higher subsidy when the corporate tax is low, while foreign CSR requires a higher subsidy when the corporate tax is relatively high. In particular, when the corporate tax is low enough, that is, 0 < τ ≤ τ 2, we have that s F < s B < 0. Thus, the government imposes an output tax on both firms where that under foreign CSR is higher than that under bilateral CSR. However, when the corporate tax is high enough, namely, τ 2 < τ < 1, we have that s F > s B > 0. Thus, the government provides an output subsidy to both firms where that under foreign CSR is higher than that under bilateral CSR.

Proposition 4:

The social welfare increases with corporate tax and decreases with foreign penetration.

Proposition 4 states that an increase in corporate tax leads to higher levels of subsidy and market output, resulting in higher consumer surplus, subsidy expenditure, and tax revenue, while it reduces two firm’s profits. The former effect outweighs the latter effect and thus, an increase in corporate tax makes the society better off. On the other hand, an increase in foreign penetration works negatively in both the former and the latter effects and thus, resulting in lower social welfare.

Lemma 2:

The welfare ranks among the four models are as follows:

Lemma 2 shows the relationship between the welfare and corporate tax rate. Then, we can summarize the findings in Lemma 2 as follows: (a) W

B

> max{W

D

, W

F

, W

N

}, (b) W

D

> W

F

, (c)

Second, (b) domestic CSR yields a higher welfare than that under foreign CSR, even though the strategic levels of CSR are the same. This is because the market output will be higher under domestic CSR, that is, Q D > Q F , since the government provides a higher subsidy, s D > s F , from Lemma 1. Thus, the less leakage of the welfare under the domestic CSR leads to a higher welfare at equilibrium.

Third, (c) foreign CSR yields a higher welfare when the corporate tax is low, while no CSR yields a higher welfare when the corporate tax is relatively high. Thus, there exists a trade-off between the foreign CSR and no CSR depending on corporate tax rate. Note that no CSR provides a higher subsidy when the corporate tax is relatively high, we have

Finally, (d) domestic CSR yields a higher social welfare when the corporate tax is low, while no CSR yields a higher welfare when the corporate tax is relatively high. There is also a trade-off between domestic CSR and no CSR, but the threshold is higher under domestic CSR. Note that no CSR provides a higher subsidy when the corporate tax is relatively high, we have

4.2 Endogenous CSR Choice Game

We then offer an extended game in which we consider an endogenous choice of CSR between the two firms. Before examining CSR choice game, we compare the profits of the two firms in each game.

Lemma 3:

The profit ranks among the four models are as follows:

Lemma 3 shows the relationship between the profits of the two firms and corporate tax rate. It states that (i) the foreign-owned firm always obtains the highest profit under no CSR, compared to other CSR cases including foreign CSR, irrespective of the corporate tax, while it earns a higher profit under foreign CSR than that under bilateral CSR. This is because, although no CSR strategy yields relatively smaller output,

On the other hand, (ii) states that the domestic firm could obtain the highest profit under domestic CSR only when the corporate tax is relatively low. In particular, we can summarize the findings in Lemma 3 (ii)–(iv) as follows: (a)

Finally, we consider an extensive game with endogenous choice of CSR in which each firm decides whether to engage in CSR activities or not simultaneously and non-cooperatively before the first stage of the previous analysis. Then, we have an endogenous CSR choice game in Table 1.

Endogenous CSR choice game under uniform subsidies.

| Firm 1, 2 | CSR | No CSR |

|---|---|---|

| CSR |

|

|

| No CSR |

|

|

Then, from Lemma 3(i), we have that

Proposition 5:

Domestic CSR (no CSR) is a Nash equilibrium when the corporate tax is low (high), however neither one is socially desirable.

Proposition 5 shows that domestic CSR is a Nash equilibrium when τ is low, namely 0 < τ < τ 3, while no CSR is a Nash equilibrium when τ is high, for instance, τ 3 < τ < 1. Moreover, both domestic CSR and no CSR are the Nash equilibria when τ = τ 3. However, Lemma 2 reveals that neither of the Nash equilibria is socially desirable. Therefore, an appropriate regulatory framework for CSR guidelines is necessary in certain cases with a lower corporate tax and a higher foreign penetration.

5 Discriminatory Subsidy

We now consider a discriminatory subsidy according to which the government grants different levels of output subsidies to the firms, s

i

, in the first stage. The profit of the firm is

First, we consider a bilateral CSR case. In the last stage, the differentiation of V i with respect to q i yields the following outputs:

The profits of the domestic and foreign-owned firms are respectively

In the second stage, the differentiation of π i in Eq. (35) with respect to α i yields the following optimal level of CSR of the firm:

where

The resulting social welfare is

In the first stage, the government opts for discriminatory subsidies to maximize social welfare. As obtaining the explicit outcomes in the equilibrium is challenging, we use numerical simulations with τ ∈ (0, 1). Table 2 presents the equilibrium outcomes in this model, where superscript “*” represents the equilibrium outcome under the discriminatory subsidy. Note that

Equilibrium outcomes in the bilateral CSR case under discriminatory subsidies.

| τ |

|

|

|

|

|

W B∗ |

|---|---|---|---|---|---|---|

| 0 | 0.2162 | 0.3604 | −0.2677 | 0.2471 | 0.0106 | 0.2933 |

| 0.1 | 0.1923 | 0.3550 | −0.2511 | 0.2180 | 0.0114 | 0.2944 |

| 0.2 | 0.1687 | 0.3490 | −0.2318 | 0.1894 | 0.0122 | 0.2958 |

| 0.3 | 0.1453 | 0.3422 | −0.2091 | 0.1613 | 0.0130 | 0.2975 |

| 0.4 | 0.1222 | 0.3345 | −0.1820 | 0.1340 | 0.0137 | 0.2996 |

| 0.5 | 0.0996 | 0.3255 | −0.1491 | 0.1075 | 0.0142 | 0.3021 |

| 0.6 | 0.0774 | 0.3149 | −0.1085 | 0.0820 | 0.0144 | 0.3053 |

| 0.7 | 0.0559 | 0.3019 | −0.0571 | 0.0579 | 0.0141 | 0.3095 |

| 0.8 | 0.0355 | 0.2855 | 0.0101 | 0.0356 | 0.0127 | 0.3149 |

| 0.9 | 0.0166 | 0.2640 | 0.1017 | 0.0159 | 0.0089 | 0.3224 |

| 1 | 0 | 0.2339 | 0.2339 | 0 | 0 | 0.3333 |

Second, we consider a domestic CSR case. In the last stage, by substituting α

2 = 0 into Eq. (35), we calculate the profit of the domestic firm. In the second stage, the differentiation of π

1 with respect to α

1 yields

Third, we consider a foreign CSR case. In the last stage, by substituting α

1 = 0 into Eq. (35), we obtain the profit of the foreign-owned firm. In the second stage, the differentiation of π

2 with respect to α

2 yields

Fourth, we consider a no CSR case. In the last stage, substituting α

1 = α

2 = 0, we confirm the social welfare. In the first stage, the differentiation of W with respect to s

i

yields:

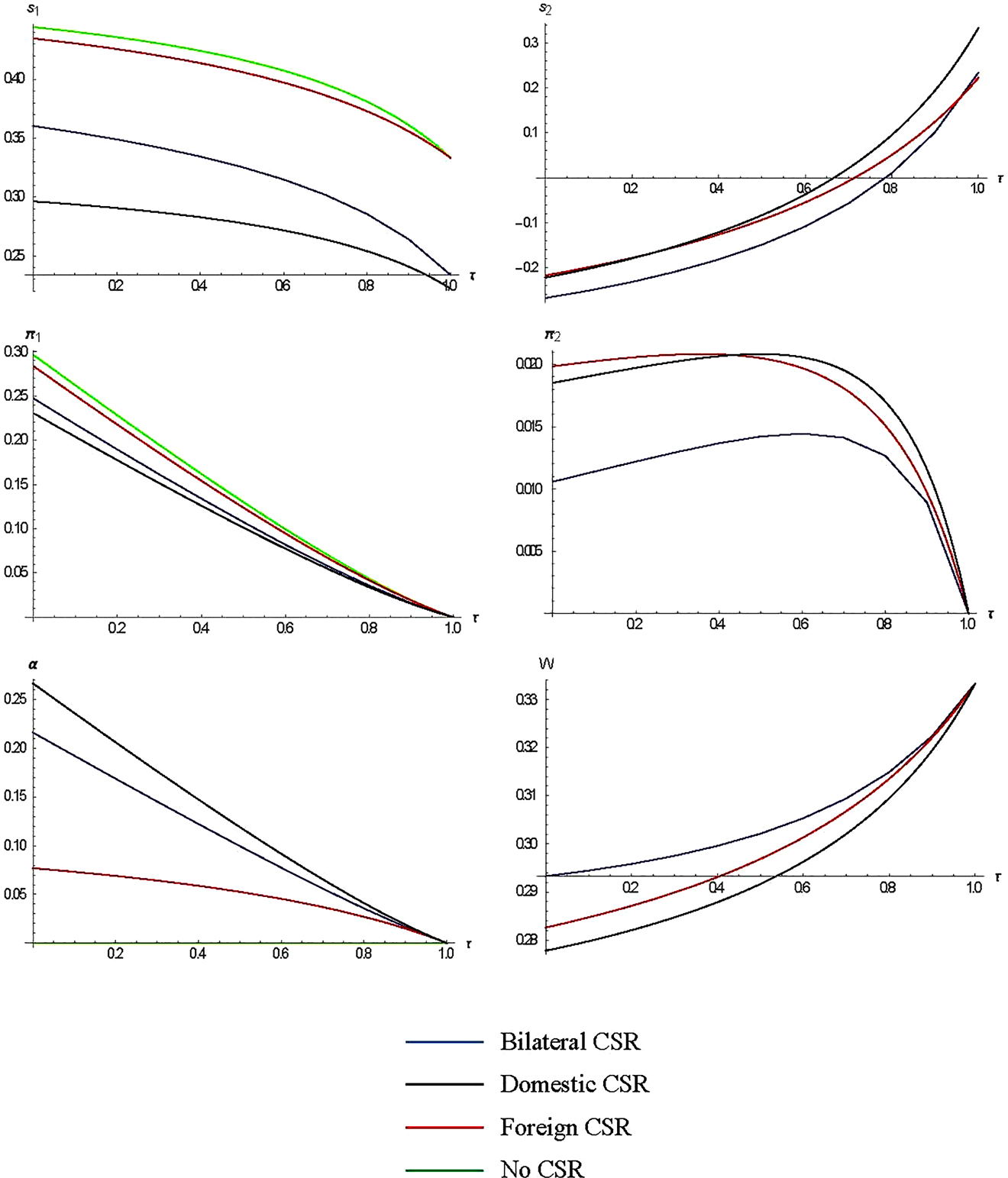

Lastly, we compare the optimal levels of CSR, discriminatory subsidies, profits of the two firms, and social welfare among the four models. Figure 1 indicates the comparisons between the four models under discriminatory subsidies. Then, we obtain the following lemmas and propositions.

Comparisons among the four models under discriminatory subsidies.

Proposition 6:

The domestic CSR leads to the highest CSR level, while foreign CSR leads to the lowest CSR level under discriminatory subsidies.

Proposition 6 implies that the discriminatory subsidy policy yields different levels of CSR in the two unilateral CSR cases, which is in contrast to the result under the uniform subsidy in Proposition 1, that is,

Lemma 4:

The ranks of optimal discriminatory subsidies among the four models are as follows:

Lemma 4 presents the policy relationships between optimal discriminatory subsidies and corporate tax rates. First, we illustrate that the optimal discriminatory subsidy of the domestic firm is independent of corporate tax. In particular, to enlarge market outputs, the government grants the highest subsidy to the domestic firm when none of the firms engage in CSR activities. As domestic CSR leads to the highest CSR level, the government grants the lowest subsidy to the domestic firm under domestic CSR.

Regarding the foreign-owned firm, we summarize the findings of Lemma 4 as follows: (a)

Lemma 5:

The ranks of profits and social welfare under discriminatory subsidies are as follows:

Lemma 5 states that the domestic firm is most profitable under no CSR, while it is the least profitable under domestic CSR in contrast to the result under the uniform subsidy in Lemma 3. Further, the foreign-owned firm generates minimum profit under bilateral CSR and maximum profit under foreign CSR (domestic CSR) when corporate tax is low (high). Lemma 5 also implies that irrespective of government policies that include discriminatory subsidies and corporate tax, bilateral CSR yields the highest social welfare, whereas no CSR yields the lowest social welfare. Note that

Finally, we consider an endogenous choice game of CSR under discriminatory subsidies in which each firm decides whether to engage in CSR activities simultaneously and non-cooperatively before the first stage of the previous analysis.

Proposition 7:

Foreign CSR (no CSR) is a Nash equilibrium when corporate tax is low (high) under the discriminatory subsidy, while neither one is socially desirable.

Proposition 7 illustrates that foreign CSR is a Nash equilibrium when τ is low, that is,

6 Concluding Remarks

In this study, we examined strategic CSR in a Cournot duopoly between domestic and foreign-owned firms in a managerial delegation framework facing the government’s public policies. We then investigated how the government could combine policies to regulate the firms’ CSR behavior and to enhance market performance. Our main findings are as follows: first, the strategic effect of corporate profit tax on strategic CSR and the output subsidy policy, exists. In particular, the effects of corporate tax on strategic CSR and social welfare are conflicting: the strategic level of CSR decreases but social welfare increases with corporate tax. These results are robust under the discriminatory subsidy. This finding is significant for policymakers because corporate profit taxes are not neutral toward firm behavior in the presence of strategic CSR. Second, the optimal unilateral CSR is higher than bilateral CSR under the uniform subsidy, while domestic (foreign) CSR leads to the highest (lowest) CSR level under the discriminatory subsidy. However, irrespective of corporate tax or foreign penetration, social welfare is highest under bilateral CSR. Finally, the Nash equilibrium of an endogenous CSR choice game depends on corporate tax and output subsidy policies. In particular, when corporate tax is low, domestic CSR is a Nash equilibrium under the uniform subsidy, while foreign CSR is a Nash equilibrium under the discriminatory subsidy. However, neither is socially desirable. Therefore, an appropriate policy framework on CSR guidelines is necessary for lower corporate taxes.

Even though our methodology can be applied to different models with other public policies on CSR, future research avenues remain. For example, while we regarded a corporate tax as an exogenously given parameter in this model, the government may determine it endogenously in the general equilibrium model. Alternative scenarios should include product differentiation, Stackelberg competition, and more general specifications for the demand and cost functions among the oligopolistic firms. Extending our analysis to different CSR activities with commitment investment would be another direction for future research.

Funding source: Key Program of National Natural Science Foundation of China 10.13039/501100010903

Award Identifier / Grant number: 42030409

Funding source: China Postdoctoral Science Foundation 10.13039/501100002858

Award Identifier / Grant number: 2019M651098

Acknowledgments

We thank to an anonymous referee for their careful and constructive comments on an earlier version of this paper. All remaining errors are ours. This research was funded by the Key Program of National Natural Science Foundation of China, grant number 42030409, and the Postdoctoral Science Foundation of China, grant number 2019M651098.

Appendix Proofs of Lemmas

Proof of Lemma 1:

Comparing the value of τ i provides: τ 1 < τ N < τ D < τ 3 < τ B < τ F < τ 2 < τ 4 < τ 5 < τ 6. Then, we have the following relationships:

Proof of Lemma 2:

Comparing the social welfare among the four models provides the following relationships:

Proof of Lemma 3:

First, comparing the profits of domestic firm provides the followings:

Second, comparing the profits of foreign-owned firm provides the following:

References

Aaronson, S. A. 2007. “A Match Made in the Corporate and Public Interest: Marrying Voluntary CSR Initiatives and the WTO.” Journal of World Trade 41 (3): 629–59.10.54648/TRAD2007024Search in Google Scholar

Alley, W. A. 1997. “Partial Ownership Arrangements and Collusion in the Automobile Industry.” Journal of Industrial Economics 45 (2): 191–205.10.1111/1467-6451.00043Search in Google Scholar

Barcena-Ruiz, J., and N. Olaizola. 2007. “Cost-Saving Production Technologies and Partial Ownership.” Economics Bulletin 15 (6): 1–8.Search in Google Scholar

Benabou, R., and J. Tirole. 2010. “Individual and Corporate Social Responsibility.” Economica 77 (305): 1–19.10.1111/j.1468-0335.2009.00843.xSearch in Google Scholar

Bernard, A. B., J. B. Jensen, S. J. Redding, and P. K. Schott. 2018. “Global Firms.” Journal of Economic Literature 56 (2): 565–619, https://doi.org/10.1257/jel.20160792.Search in Google Scholar

Besley, T., and M. Ghatak. 2005. “Competition and Incentives with Motivated Agents.” American Economic Review 95 (3): 616–36, https://doi.org/10.1257/0002828054201413.Search in Google Scholar

Brand, B., and M. Grothe. 2013. “A Note on ‘Corporate Social Responsibility and Marketing Channel Coordination’.” Research in Economics 67 (4): 324–7, https://doi.org/10.1016/j.rie.2013.09.003.Search in Google Scholar

Brand, B., and M. Grothe. 2015. “Social Responsibility in a Bilateral Monopoly.” Journal of Economics 115 (3): 275–89, https://doi.org/10.1007/s00712-014-0412-6.Search in Google Scholar

Brekke, K., and K. Nyborg. 2008. “Attracting Responsible Employees: Green Production as Labor Market Screening.” Resource and Energy Economics 30 (4): 509–26, https://doi.org/10.1016/j.reseneeco.2008.05.001.Search in Google Scholar

Carroll, A., and K. Shabana. 2010. “The Business Case for Corporate Social Responsibility: A Review of Concepts, Research and Practice.” International Journal of Management Reviews 12 (1): 85–105, https://doi.org/10.1111/j.1468-2370.2009.00275.x.Search in Google Scholar

Chang, Y. M., H. Y. Chen, L. F. S. Wang, and S. J. Wu. 2014. “Corporate Social Responsibility and International Competition: A Welfare Analysis.” Review of International Economics 22 (3): 625–38, https://doi.org/10.1111/roie.12117.Search in Google Scholar

Choi, J. P., T. Furusawa, and J. Ishikawa. 2020. “Transfer Pricing Regulation and Tax Competition.” Journal of International Economics 127: 103367, https://doi.org/10.1016/jinteco.2020.103367.Search in Google Scholar

Crifo, P., and V. Forget. 2015. “The Economics of Corporate Social Responsibility: A Firm-Level Perspective Survey.” Journal of Economic Surveys 29 (1): 112–30, https://doi.org/10.1111/joes.12055.Search in Google Scholar

Fanti, L., and D. Buccella. 2017. “Corporate Social Responsibility in a Game-Theoretic Context.” Economia e Politica Industriale 44 (3): 371–90, https://doi.org/10.1007/s40812-016-0064-3.Search in Google Scholar

Gandullia, L., and S. Pisera. 2020. “Do Income Taxes Affect Corporate Social Responsibility? Evidence from European-Listed Companies.” Corporate Social Responsibility and Environmental Management 27 (2): 1017–27, https://doi.org/10.1002/csr.1862.Search in Google Scholar

Garcia, A., M. Leal, and S. H. Lee. 2018a. “Social Responsibility in a Bilateral Monopoly with R&D.” Economics Bulletin 38: 1467–75.Search in Google Scholar

Garcia, A., M. Leal, and S. H. Lee. 2018b. “Time-Inconsistent Environmental Policies with a Consumer-Friendly Firm: Tradable Permits Versus Emission Tax.” International Review of Economics and Finance 58: 523–37. https://doi.org/10.1016/j.iref.2018.06.001.Search in Google Scholar

Garcia, A., M. Leal, and S. H. Lee. 2019. “Endogenous Timing with a Socially Responsible Firm.” Korean Economic Review 35 (2): 345–70.Search in Google Scholar

Garcia, A., M. Leal, and S. H. Lee. 2020a. “Cooperation with a Multiproduct Corporation in a Strategic Managerial Delegation.” Managerial and Decision Economics 41 (1): 3–9. https://doi.org/10.1002/mde.3073.Search in Google Scholar

Garcia, A., M. Leal, and S. H. Lee. 2020b. “Welfare-Improving Cooperation with a Consumer-Friendly Multiproduct Corporation.” Managerial and Decision Economics 41 (7): 1144–55. https://doi.org/10.1002/mde.3161.Search in Google Scholar

Gilo, D., and Y. Spiegel. 2004. “Network Interconnection with Competitive Transit.” Information Economics and Policy 16 (3): 439–58, https://doi.org/10.1016/j.infoecopol.2004.01.009.Search in Google Scholar

Goering, G. E. 2012. “Corporate Social Responsibility and Marketing Channel Coordination.” Research in Economics 66 (2): 142–8, https://doi.org/10.1016/j.rie.2011.10.001.Search in Google Scholar

Halm, D. 2009. The Effects of Partial Cross-Ownership on Competition. Netherlands: Tilburg University.Search in Google Scholar

Haraguchi, J., and T. Matsumura. 2014. “Price Versus Quantity in a Mixed Duopoly with Foreign Penetration.” Research in Economics 68 (4): 338–53, https://doi.org/10.1016/j.rie.2014.09.001.Search in Google Scholar

Hino, Y., and Y. Zennyo. 2017. “Corporate Social Responsibility and Strategic Relationships.” International Review of Economics 64 (3): 231–44, https://doi.org/10.1007/s12232-016-0267-y.Search in Google Scholar

Hong, H., and M. Kacperczyk. 2009. “The Price of Sin: The Effects of Social Norms on Markets.” Journal of Financial Economics 93 (1): 15–36, https://doi.org/10.1016/j.jfineco.2008.09.001.Search in Google Scholar

Kim, S. L., S. H. Lee, and T. Matsumura. 2019. “Corporate Social Responsibility and Privatization Policy in a Mixed Oligopoly.” Journal of Economics 128 (1): 67–89, https://doi.org/10.1007/s00712-018-00651-7.Search in Google Scholar

Kitzmueller, M., and J. Shimshack. 2012. “Economic Perspectives on Corporate Social Responsibility.” Journal of Economic Literature 50 (1): 51–84, https://doi.org/10.1257/jel.50.1.51.Search in Google Scholar

Konigstein, M., and W. Muller. 2001. “Why Firms Should Care for Customers.” Economics Letters 72 (1): 47–52, https://doi.org/10.1016/s0165-1765(01)00400-1.Search in Google Scholar

Kopel, M. 2015. “Price and Quantity Contracts in a Mixed Duopoly with a Socially Concerned Firm.” Managerial and Decision Economics 36 (8): 559–66, https://doi.org/10.1002/mde.2707.Search in Google Scholar

Kopel, M., and B. Brand. 2012. “Socially Responsible Firms and Endogenous Choice of Strategic Incentives.” Economic Modelling 29 (3): 982–9, https://doi.org/10.1016/j.econmod.2012.02.008.Search in Google Scholar

KPMG. 2013. Survey of Corporate Responsibility Reporting. 2013. England: KPMG International.Search in Google Scholar

KPMG. 2015. International Survey of Corporate Responsibility Reporting. 2015. England: KPMG International.Search in Google Scholar

Lambertini, L., and A. Tampieri. 2015. “Incentives, Performance and Desirability of Socially Responsible Firms in a Cournot Oligopoly.” Economic Modelling 50: 40–8, https://doi.org/10.1016/j.econmod.2015.05.016.Search in Google Scholar

Leal, M., A. Garcia, and S. H. Lee. 2018. “The Timing of Environmental Tax Policy with a Consumer-Friendly Firm.” Hitotsubashi Journal of Economics 59 (1): 25–43.Search in Google Scholar

Lee, S. H., and C. H. Park. 2019. “Eco-firms and the Sequential Adoption of Environmental Corporate Social Responsibility in the Managerial Delegation.” B.E. Journal Theoretical Economics 19 (1): 20170043.10.1515/bejte-2017-0043Search in Google Scholar

Lee, S. H., S. Sato, and T. Matsumura. 2018. “An Analysis of Entry-then-Privatization Model: Welfare and Policy Implications.” Journal of Economics 123 (1): 71–88, https://doi.org/10.1007/s00712-017-0559-z.Search in Google Scholar

Liu, C. C., L. F. S. Wang, and S. H. Lee. 2015. “Strategic Environmental Corporate Social Responsibility in a Differentiated Duopoly Market.” Economics Letters 129: 108–11, https://doi.org/10.1016/j.econlet.2015.02.027.Search in Google Scholar

Liu, Q., L. F. S. Wang, and C. L. Chen. 2018. “CSR in an Oligopoly with Foreign Competition: Policy and Welfare Implications.” Economic Modelling 72: 1–7, https://doi.org/10.1016/j.econmod.2018.01.002.Search in Google Scholar

Liu, Y., T. Matsumura, and C. Zeng. 2018. The Relationship Between Privatization and Corporate Taxation Policies. MPRA working paper, No. 89784.Search in Google Scholar

Manasakis, C., E. Mitrokostas, and E. Petrakis. 2018. “Strategic Corporate Social Responsibility by a Multinational Firm.” Review of International Economics 26 (3): 709–20, https://doi.org/10.1111/roie.12320.Search in Google Scholar

Matsumura, T., and A. Ogawa. 2014. “Corporate Social Responsibility or Payoff Asymmetry? A Study of an Endogenous Timing Game.” Southern Economic Journal 81 (2): 457–73, https://doi.org/10.4284/0038-4038-2012.182.Search in Google Scholar

Planer-Friedrich, L., and M. Sahm. 2016. “Strategic Corporate Social Responsibility.” In: CESifo Conference Paper.10.2139/ssrn.2990958Search in Google Scholar

Planer-Friedrich, L., and M. Sahm. 2018. “Why Firms Should Care for All Consumers.” Economics Bulletin 38: 1623–12.Search in Google Scholar

Schreck, P. 2011. “Reviewing the Business Case for Corporate Social Responsibility: New Evidence and Analysis.” Journal of Business Ethics 103 (2): 167–88, https://doi.org/10.1007/s10551-011-0867-0.Search in Google Scholar

Siegel, D. S., and D. F. Vitaliano. 2007. “An Empirical Analysis of the Strategic Use of Corporate Social Responsibility.” Journal of Economics and Management Strategy 16 (3): 773–92, https://doi.org/10.1111/j.1530-9134.2007.00157.x.Search in Google Scholar

The UN-Global Compact-Accenture CEO Study. 2010. UN Global Compact Reports.Search in Google Scholar

The UN-Global Compact-Accenture CEO Study on Sustainability. 2013. UN Global Compact Reports.Search in Google Scholar

Vidal-Leon, C. 2013. “Corporate Social Responsibility, Human Rights, and the World Trade Organization.” Journal of International Economic Law 16 (4): 893–920, https://doi.org/10.1093/jiel/jgt030.Search in Google Scholar

Wang, L. F. S., Y. C. Wang, and L. Zhao. 2012. “Tariff Policy and Welfare in an International Duopoly with Consumer-Friendly Initiative.” Bulletin of Economic Research 64 (1): 56–64, https://doi.org/10.1111/j.1467-8586.2010.00382.x.Search in Google Scholar

Withisuphakorn, P., and P. Jiraporn. 2016. “The Effect of Firm Maturity on Corporate Social Responsibility (CSR): Do Older Firms Invest More in CSR?” Applied Economics Letters 23 (4): 298–301, https://doi.org/10.1080/13504851.2015.1071464.Search in Google Scholar

Xu, L., and S. H. Lee. 2019. “Tariffs and Privatization Policy in a Bilateral Trade with Corporate Social Responsibility.” Economic Modelling 80: 339–51, https://doi.org/10.1016/j.econmod.2018.11.020.Search in Google Scholar

Xu, L., S. H. Lee, and T. Matsumura. 2017. “Ex-Ante Versus Ex-Post Privatization Policies with Foreign Penetration in Free-Entry Mixed Markets.” International Review of Economics and Finance 50: 1–7, https://doi.org/10.1016/j.iref.2017.03.023.Search in Google Scholar

© 2020 Lili Xu and Sang-Ho Lee, published by De Gruyter, Berlin/Boston

This work is licensed under the Creative Commons Attribution 4.0 International License.

Articles in the same Issue

- Frontmatter

- Research Articles

- On the Microfoundation of Linear Oligopoly Demand

- Uncertain Outcomes and Climate Change Policy Using an Expo-Power Utility Function

- Price Versus Quantity Competition in a Vertically Related Market with Retailer’s Effort

- Search Costs and Wage Inequality

- Product Differentiation in a Vertical Structure

- Corporate Profit Tax and Strategic Corporate Social Responsibility Under Foreign Acquisition

- Examining the Impact of Electoral Competition and Endogenous Lobby Formation on Equilibrium Policy Platforms

- Entry Deterrence and Free Riding in License Auctions: Incumbent Heterogeneity and Monotonicity

- When is Knowledge Acquisition Socially Beneficial in the Laffont–Tirole Regulatory Framework?

- Notes

- Long-Run Growth, Speed of Convergence and the Specification of Technology

- Working Time under Alternative Pay Contracts in the Ride-Sharing Industry

- Tacit Collusion with Consumer Preference Costs

- Competitively-Issued Convertible Bank Notes in a Theory of Finance: Earl Thompson Meets Fischer Black

Articles in the same Issue

- Frontmatter

- Research Articles

- On the Microfoundation of Linear Oligopoly Demand

- Uncertain Outcomes and Climate Change Policy Using an Expo-Power Utility Function

- Price Versus Quantity Competition in a Vertically Related Market with Retailer’s Effort

- Search Costs and Wage Inequality

- Product Differentiation in a Vertical Structure

- Corporate Profit Tax and Strategic Corporate Social Responsibility Under Foreign Acquisition

- Examining the Impact of Electoral Competition and Endogenous Lobby Formation on Equilibrium Policy Platforms

- Entry Deterrence and Free Riding in License Auctions: Incumbent Heterogeneity and Monotonicity

- When is Knowledge Acquisition Socially Beneficial in the Laffont–Tirole Regulatory Framework?

- Notes

- Long-Run Growth, Speed of Convergence and the Specification of Technology

- Working Time under Alternative Pay Contracts in the Ride-Sharing Industry

- Tacit Collusion with Consumer Preference Costs

- Competitively-Issued Convertible Bank Notes in a Theory of Finance: Earl Thompson Meets Fischer Black