Delegation and Information Disclosure with Unforeseen Contingencies

-

Haoran Lei

Abstract

We incorporate unawareness into the delegation problem between a financial expert and an investor, and study their pre-delegation communication. The expert has superior awareness of the possible states of the world, and decides whether to reveal some of them to the investor. We find that the expert reveals all the possible states to the investor if the investor is initially aware of a large set of possible states, but reveals partially or nothing otherwise. An investor with a higher degree of unawareness tends to delegate a larger set of projects to the expert, giving rise to a higher incentive for the expert to keep her unaware.

Acknowledgments

We thank the editor Burkhard Schipper and a referee for constructive suggestions and seminar participants at Hong Kong University of Science and Technology, the 2017 China Meeting of the Econometric Society (Wuhan), the 2019 Asian Meeting of the Econometric Society (Xiamen), and the 2021 Zoom Mini-Workshop on Contract Theory with Unawareness for helpful discussions and comments. All errors are ours.

We provide proofs of all the lemmas and propositions in Appendix A.

A.1 Proof of Proposition 1

Following Alonso and Matouschek (2008), when

As we focus on the maximal delegation set, in equilibrium the investor delegates all projects above the threshold

The reason is that she believes these lower states will never be implemented by the expert. The lower cutoff is

where

A.2 Proof of Lemma 2

By Proposition 1, the delegation set is characterized by the gap

The expert’s expected utility depends on the interception of the set of undelegated options and his preferred options,

Suppose that the revelation choice is θ″ ∈ (0, 1). Then the intersection would be (θ″ − b, θ″ + b) ∩ [0, 1]. When b ≤ θ″ ≤ 1 − b, the expert’s expected utility would be

When

The same case holds for θ″ > 1 − b. Therefore, the expert’s optimal revelation choice would be

A.3 Proof of Proposition 3

If θ

2 − θ

1 ≥ 2b, the gap

First, the expert would choose

A.4 Proof of Proposition 4

Let the awareness set before revelation be [θ

1, θ

2]. The expert expands the awareness set to

By Proposition 3, if in the solution

On the other hand, decreasing

We identify the conditions under which the expert is willing to reveal extra awareness by comparing his expected utility in the two cases:

Suppose

Suppose

Last, note that the expert would choose full revelation (

A.5 Proof of Proposition 5

In this case, the investor’s delegation choice, given her interim awareness set

where

When

The delegation set with partial or no revelation is {y*}, and the expert’s expected utility is

The delegation set with full revelation is [2b, 1], and the expert’s expected utility is

Note that

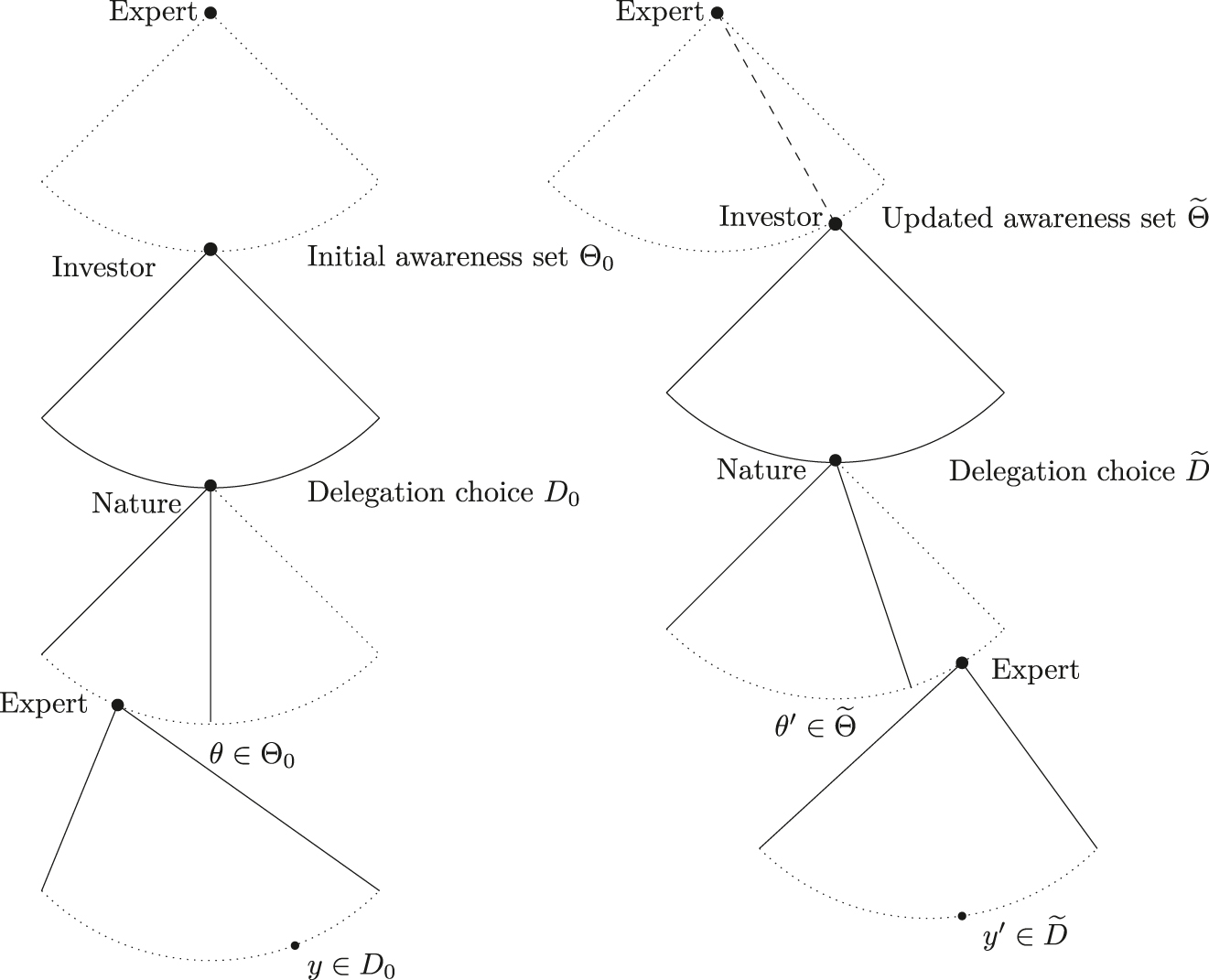

Heifetz, Meier, and Schipper (2011) pointed out that a more expressive framework than the standard extensive form game is needed to model strategic reasoning with unawareness. To capture the possibility that different players have different views of the game, Heifetz, Meier, and Schipper (2013) propose the notion of generalized extensive-form game. In this appendix, we describe how our model can be formalized using their framework. The key is to use subtrees to characterize different views of players.

There are three players: the investor, the expert, and Nature. Let T denote the set of all subtrees, each subtree induced by a specific revelation choice of the expert. A subtree characterizes a subjective game from the perspective of the investor. At the beginning of the game, the investor’s awareness set is Θ0. If the expert reveals nothing, the subjective game of the investor is depicted as the left subtree in Figure 6. If the expert expands the investor’s awareness set to

Subtrees T

0 and

References

Aghion, P., and J. Tirole. 1997. “Formal and Real Authority in Organizations.” Journal of Political Economy 105 (1): 1–29. https://doi.org/10.1086/262063.Suche in Google Scholar

Alonso, R., and N. Matouschek. 2008. “Optimal Delegation.” The Review of Economic Studies 75 (1): 259–93. https://doi.org/10.1111/j.1467-937x.2007.00471.x.Suche in Google Scholar

Amador, M., and K. Bagwell. 2013. “The Theory of Optimal Delegation with an Application to Tariff Caps.” Econometrica 81 (4): 1541–99. https://doi.org/10.3982/ecta9288.Suche in Google Scholar

Auster, S. 2013. “Asymmetric Awareness and Moral Hazard.” Games and Economic Behavior 82: 503–21. https://doi.org/10.1016/j.geb.2013.08.011.Suche in Google Scholar

Auster, S., and N. Pavoni. 2020. Limited Awareness and Financial Intermediation. Mimeo.Suche in Google Scholar

Auster, S., and N. Pavoni. 2021. Optimal Delegation and Information Transmission under Limited Awareness. Mimeo.Suche in Google Scholar

Baron, D. P., and R. B. Myerson. 1982. “Regulating a Monopolist with Unknown Costs.” Econometrica 50 (4): 911–30. https://doi.org/10.2307/1912769.Suche in Google Scholar

Bendor, J., A. Glazer, and T. Hammond. 2001. “Theories of Delegation.” Annual Review of Political Science 4 (1): 235–69. https://doi.org/10.1146/annurev.polisci.4.1.235.Suche in Google Scholar

Bucher-Koenen, T., and J. Koenen. 2015. “Do Seemingly Smarter Consumers Get Better Advice?” In MEA discussion paper series 201501, Munich Center for the Economics of Aging (MEA) at the Max Planck Institute for Social Law and Social Policy. Also available at https://EconPapers.repec.org/RePEc:mea:meawpa:201501.10.2139/ssrn.2572961Suche in Google Scholar

Calcagno, R., and C. Monticone. 2015. “Financial Literacy and the Demand for Financial Advice.” Journal of Banking & Finance 50: 363–80. https://doi.org/10.1016/j.jbankfin.2014.03.013.Suche in Google Scholar

Charness, G., R. Cobo-Reyes, N. Jiménez, J. A. Lacomba, and F. Lagos. 2012. “The Hidden Advantage of Delegation: Pareto Improvements in a Gift Exchange Game.” The American Economic Review 102 (5): 2358–79. https://doi.org/10.1257/aer.102.5.2358.Suche in Google Scholar

Chater, N., S. Huck, and I. Roman. 2010. “Consumer Decision-Making in Retail Investment Services: a Behavioural Economics Perspective.” In Final Report. Brussels: European Commission Directorate-General for Health and Consumers.Suche in Google Scholar

Falk, A., and M. Kosfeld. 2006. “The Hidden Costs of Control.” The American Economic Review 96 (5): 1611–30. https://doi.org/10.1257/aer.96.5.1611.Suche in Google Scholar

Filiz-Ozbay, E. 2012. “Incorporating Unawareness into Contract Theory.” Games and Economic Behavior 76 (1): 181–94.10.1016/j.geb.2012.05.009Suche in Google Scholar

Galperti, S. 2019. “Persuasion: The Art of Changing Worldviews.” The American Economic Review 109 (3): 996–1031. https://doi.org/10.1257/aer.20161441.Suche in Google Scholar

Georgarakos, D., and R. Inderst. 2014. Financial Advice and Stock Market Participation. Mimeo. Also Available at SSRN http://ssrn.com/abstract=1641302.Suche in Google Scholar

Gui, Z., Y. Huang, and X. Zhao. 2021a. Financial Fraud and Investor Awareness. Mimeo. Also Available at SSRN http://ssrn.com/abstract=3025400.10.2139/ssrn.4129680Suche in Google Scholar

Gui, Z., Y. Huang, and X. Zhao. 2021b. “Whom to Educate? Financial Literacy and Investor Awareness.” China Economic Review 67: 101608. https://doi.org/10.1016/j.chieco.2021.101608.Suche in Google Scholar

Hackethal, A., M. Haliassos, and T. Jappelli. 2012. “Financial Advisors: a Case of Babysitters?” Journal of Banking & Finance 36 (2): 509–24. https://doi.org/10.1016/j.jbankfin.2011.08.008.Suche in Google Scholar

Hackethal, A., R. Inderst, and S. Meyer. 2012. Trading on Advice. Mimeo. Available at SSRN http://ssrn.com/abstract=1701777.10.2139/ssrn.1701777Suche in Google Scholar

Halpern, J. Y., and L. C. Rêgo. 2014. “Extensive Games with Possibly Unaware Players.” Mathematical Social Sciences 70: 42–58. https://doi.org/10.1016/j.mathsocsci.2012.11.002.Suche in Google Scholar

Heifetz, A., M. Meier, and B. C. Schipper. 2011. “Prudent Rationalizability in Generalized Extensive-Form Games with Unawareness.” In MPRA Paper 30220. Germany: University Library of Munich. Also available at https://ideas.repec.org/p/pra/mprapa/30220.html.10.2139/ssrn.1804687Suche in Google Scholar

Heifetz, A., M. Meier, and B. C. Schipper. 2013. “Dynamic Unawareness and Rationalizable Behavior.” Games and Economic Behavior 81: 50–68. https://doi.org/10.1016/j.geb.2013.04.003.Suche in Google Scholar

Holmstrom, B. 1977. “On Incentives and Control in Organizations.” Ph.D. thesis, Stanford University. Also available at https://economics.mit.edu/files/3856.Suche in Google Scholar

Holmstrom, B. 1980. “On The Theory of Delegation.” In Discussion Papers 438. Northwestern University, Center for Mathematical Studies in Economics and Management Science. Also available at https://ideas.repec.org/p/nwu/cmsems/438.html.Suche in Google Scholar

Inderst, R., and M. Ottaviani. 2012. “How (Not) To Pay For Advice: a Framework For Consumer Financial Protection.” Journal of Financial Economics 105 (2): 393–411. https://doi.org/10.1016/j.jfineco.2012.01.006.Suche in Google Scholar

Karni, E., and M.-L. Vierø. 2013. ““Reverse Bayesianism”: A Choice-Based Theory of Growing Awareness.” The American Economic Review 103 (7): 2790–810. https://doi.org/10.1257/aer.103.7.2790.Suche in Google Scholar

Karni, E., and M.-L. Vierø. 2015. “Probabilistic Sophistication and Reverse Bayesianism.” Journal of Risk and Uncertainty 50 (3): 189–208. https://doi.org/10.1007/s11166-015-9216-5.Suche in Google Scholar

Kováč, E., and T. Mylovanov. 2009. “Stochastic Mechanisms in Settings without Monetary Transfers: The Regular Case.” Journal of Economic Theory 144 (4): 1373–95.10.1016/j.jet.2008.06.008Suche in Google Scholar

Krishna, V., and J. Morgan. 2001. “A Model of Expertise.” Quarterly Journal of Economics 116 (2): 747–75. https://doi.org/10.1162/00335530151144159.Suche in Google Scholar

Li, S., M. Peitz, and X. Zhao. 2014. “Vertically Differentiated Duopoly with Unaware Consumers.” Mathematical Social Sciences 70: 59–67. https://doi.org/10.1016/j.mathsocsci.2012.11.001.Suche in Google Scholar

Li, S., M. Peitz, and X. Zhao. 2016. “Information Disclosure and Consumer Awareness.” Journal of Economic Behavior & Organization 128: 209–30. https://doi.org/10.1016/j.jebo.2016.05.003.Suche in Google Scholar

Loewenstein, G., M. C. Daylian, and S. Sah. 2011. “The Limits of Transparency: Pitfalls and Potential of Disclosing Conflicts of Interest.” The American Economic Review 101 (3): 423–8. https://doi.org/10.1257/aer.101.3.423.Suche in Google Scholar

Lusardi, A., and O. S. Mitchell. 2014. “The Economic Importance of Financial Literacy: Theory and Evidence.” Journal of Economic Literature 52 (1): 5–44. https://doi.org/10.1257/jel.52.1.5.Suche in Google Scholar

Ma, W., and B. C. Schipper. 2014. Indescribable Contingencies versus Unawareness in Incomplete Contracting. Mimeo. Also available at https://bit.ly/2P31WL3.Suche in Google Scholar

Martimort, D., and A. Semenov. 2006. “Continuity in Mechanism Design without Transfers.” Economics Letters 93 (2): 182–9. https://doi.org/10.1016/j.econlet.2006.04.011.Suche in Google Scholar

Schipper, B. C., and H. Y. Woo. 2019. “Political Awareness, Microtargeting of Voters, and Negative Electoral Campaigning.” Quarterly Journal of Political Science 14 (1): 41–88. https://doi.org/10.1561/100.00016066.Suche in Google Scholar

van Rooij, M., A. Lusardi, and R. Alessie. 2011. “Financial Literacy and Stock Market Participation.” Journal of Financial Economics 101 (2): 449–72. https://doi.org/10.1016/j.jfineco.2011.03.006.Suche in Google Scholar

von Thadden, E.-L., and X. Zhao. 2012. “Incentives for Unaware Agents.” The Review of Economic Studies 79 (3): 1151. https://doi.org/10.1093/restud/rdr050.Suche in Google Scholar

von Thadden, E.-L., and X. Zhao. 2014. “Multi-task Agency with Unawareness.” Theory and Decision 77 (2): 197–222. https://doi.org/10.1007/s11238-013-9397-9.Suche in Google Scholar

Zhao, X. 2011. “Framing Contingencies in Contracts.” Mathematical Social Sciences 61 (1): 31–40. https://doi.org/10.1016/j.mathsocsci.2010.09.003.Suche in Google Scholar

© 2021 Walter de Gruyter GmbH, Berlin/Boston

Artikel in diesem Heft

- Frontmatter

- Special Issue on Unawareness

- Editorial

- Introduction to the Special Issue on Unawareness

- Research Articles

- Game Theory Without Partitions, and Applications to Speculation and Consensus

- Do I Know Ω? An Axiomatic Model of Awareness and Knowledge

- Games with Unawareness

- Knowledge, Awareness and Probabilistic Beliefs

- Prudent Rationalizability in Generalized Extensive-form Games with Unawareness

- Reverse Bayesianism: A Generalization

- Ambiguity and Awareness: A Coherent Multiple Priors Model

- Updating Awareness and Information Aggregation

- Delegation and Information Disclosure with Unforeseen Contingencies

Artikel in diesem Heft

- Frontmatter

- Special Issue on Unawareness

- Editorial

- Introduction to the Special Issue on Unawareness

- Research Articles

- Game Theory Without Partitions, and Applications to Speculation and Consensus

- Do I Know Ω? An Axiomatic Model of Awareness and Knowledge

- Games with Unawareness

- Knowledge, Awareness and Probabilistic Beliefs

- Prudent Rationalizability in Generalized Extensive-form Games with Unawareness

- Reverse Bayesianism: A Generalization

- Ambiguity and Awareness: A Coherent Multiple Priors Model

- Updating Awareness and Information Aggregation

- Delegation and Information Disclosure with Unforeseen Contingencies