A linear model for LNG transport via existing pipeline and re-gasification terminals

-

Majed M. A. Munasser

und

Abdelbaki Benamor

und

Abdelbaki Benamor

Abstract

This paper presents a linear programming (LP) model for optimizing the transportation of liquefied natural gas (LNG) through existing regasification terminals and Europe’s cross-border pipeline network. While pipelines offer fixed, efficient, and direct transport over land, LNG shipping provides flexibility and scalability, particularly for regions lacking pipeline connectivity. The model is demonstrated through five different case studies. Each case involves the identification of optimal LNG supply strategies from Qatar to the European Union under Russian gas disruption scenarios of 25 %, 50 %, and 75 % (equivalent to 34, 68, and 102 MTPA, respectively). The results show that the model prioritizes deliveries to destinations with available regasification capacity and low transport costs, with key importers including Turkey, Italy, Spain, and northern corridor countries. Annual network costs range from $8.1–8.8 billion for a 25 % disruption to $21–24 billion for a 75 % disruption, with liquefaction as the largest cost component. Strategic supply routes via southern, northern, and Baltic corridors were identified to enhance EU energy security, though fully replacing Russian gas would require contract adjustments and infrastructure agreements within the EU. The findings highlight the importance of integrating LNG shipping with pipeline capacity and fostering partnerships with intermediary countries.

1 Introduction

Liquefied natural gas (LNG) primarily consists of methane which has been converted into a liquid form for ease of storage and transport. Following the removal of certain impurities from natural gas, such as carbon dioxide, sulfur dioxide…etc., the purified gas is then cooled down to lower temperatures to become liquid. As a liquid, LNG occupies a substantially lower volume than natural gas at standard atmospheric conditions. This in turn facilitates its transportation across long distances without the reliance on gas pipelines. Instead, the transportation of LNG can be very conveniently carried out in special tankers and/or ships. Upon reaching the final destination, LNG can then be re-gasified via appropriate methods [1], and distributed via gas networks. Compared to pipelines, LNG offers greater flexibility, making natural gas more attractive on an international scale. It enables transportation to a wider range of locations and allows for the utilization of previously untapped gas reserves, which would have otherwise remained unused [2], 3].

The transportation of liquefied natural gas (LNG) plays a critical role in meeting global energy demands, especially in regions with limited or no direct access to natural gas pipelines. In Europe, the growing need for diverse and secure energy sources has intensified the focus on optimizing LNG transport across a complex network of pipelines and re-gasification terminals [4]. This paper explores an integrated approach for optimizing LNG transportation by considering both pipeline and shipping methods. While pipelines offer a fixed and efficient means of delivering gas overland, LNG shipping provides the flexibility to reach regions without established pipeline infrastructure, making it a crucial component in enhancing LNG transport. The increasing demand for LNG in Europe, driven by factors such as geopolitical shifts and energy transition goals, necessitates a careful analysis of transportation strategies. To this end, a linear programming (LP) model was developed and tested through a case study to evaluate optimal LNG transport routes and logistics. This case study takes into account Europe’s existing pipeline infrastructure, major shipping routes, and re-gasification terminals, with a particular focus on how these transport methods can complement one another. The results aim to provide valuable insights into how strategic partnerships with intermediary countries can strengthen the overall LNG supply chain to Europe.

2 Literature review

The LNG industry is a complex and dynamic system, and modeling plays a crucial role in optimizing operations and improving decision-making. After reviewing the current literature, it was found that there exist four different modeling areas in LNG modeling. Firstly, there exist forecasting models that use various techniques to predict the future price of LNG [5] or the future supply/demand [6]. These models are essential for market participants to make informed decisions about buying and selling LNG [7]. Such models may use historical data, market trends, supply and demand dynamics, and other relevant factors to generate predictions [5]. These models may employ statistical methods such as time-series analysis or regression analysis [8], econometric models [9], or machine learning algorithms [10]. Secondly, there exist optimization models aim to determine the optimal timing and volume of LNG purchases and sales to maximize profits or minimize costs [11], 12]. The models may incorporate various factors such as prices, supply and demand dynamics [13], infrastructure constraints, and contractual obligations [11] to generate an optimal plan. These models may use optimization techniques such as linear programming or mixed-integer programming [12], 14]. Thirdly, there exist risk management models aim to identify and manage risks associated with LNG trading [15], 16]. These models can incorporate various risks, such as price volatility [17], 18], counterparty risk [16], and operational risk [19], 20] to develop a risk management strategy. These models may use financial models [17], Monte Carlo simulations [21], or other techniques to assess and manage risks. The fourth category are simulation models [22], 23], which are used to help market participants understand the impact of various factors, such as regulatory policies, weather patterns, or supply and demand dynamics, on the market. These models may use agent-based models [24], system dynamics models [25], or other simulation techniques [26] to generate insights into the behavior of the LNG market. Moreover, there exist many life cycle assessment and cost analysis models for evaluating the LNG environmental and economic trade-offs, which integrate fuel production pathways, transportation logistics, powertrain technologies, and carbon policy impacts to support sustainable fuel selection in shipping [27], [28], [29].

Most LNG supply chain modeling often involves the development of optimization programs, which seek to find the optimal solution to a problem, and game theory models, which model the strategic behavior of multiple stakeholders in the LNG supply chain. After reviewing the present literature, it was evident that the most commonly used modeling techniques in previously published studies were either deterministic or stochastic [30]. Deterministic modeling involves the use of a set of fixed inputs to generate a single output. Such models assume that there is no uncertainty in the inputs and that the output is entirely determined by these inputs. On the other hand, stochastic modeling involves incorporating uncertainty into the input parameters to generate multiple outputs. Stochastic modeling is based on probability distributions of input parameters, which allow for the modeling of potential variations in supply and demand [30]. One of the most common stochastic models used for LNG supply and demand is Monte Carlo simulation [31]. Input parameters such as LNG price, demand, and production are modeled as random variables. The model then generates multiple outputs based on the probability distribution of these variables, allowing for the analysis of the potential range of outcomes [31]. Overall, both deterministic and stochastic modeling approaches have their strengths and weaknesses, and the choice of modeling technique depends on the specific problem being addressed, the availability of data as well as the preferences of the decision-maker. However, deterministic methods are generally preferred over stochastic methods for LNG supply chain optimization due to the following advantages [32], 33]:

Deterministic methods provide exact solutions to the problem, which means that the optimal solution is guaranteed to be found. This is especially important for decision-making in the LNG industry, where the consequences of suboptimal decisions can be very costly.

Deterministic methods are often faster and more efficient than stochastic methods, especially for large-scale problems. This is because stochastic methods require multiple simulations to estimate the probability distributions of the input variables, which can be computationally intensive.

Deterministic methods provide a single optimal solution, which is easy to interpret and explain to stakeholders. In contrast, stochastic methods provide a range of possible solutions, which can be difficult to interpret and communicate.

Stochastic methods are highly sensitive to the assumptions made about the probability distributions of the input variables. In contrast, deterministic methods are less sensitive to such assumptions, as they rely on a single set of input values to generate a single optimal solution.

In many cases, the input data for LNG supply chain optimization is deterministic, meaning that there is no randomness or uncertainty involved. In such cases, deterministic methods are more appropriate than stochastic methods, which are designed to handle probabilistic data. Numerous contribution that involve the use of deterministic models have been proposed in the past decades to predict the growth and distribution of LNG and natural gas demand in Europe. These models include World Gas Model (WGM) [34], 35] and Gasmod [34], which discussed the expansion of LNG infrastructure and natural gas pipeline network in Europe. The majority of literature aimed to optimize European natural gas and LNG transportation routes and future strategic ways for EU countries. Some examples of these models are InTra Gas [36], Tiger [37], EUGAS [22], GAMMES [38], and NATGAS [39], 40]. These models program mixed complementary problems (MCP) with multi-objectives to reflect the strength of the market based on the upstream, downstream, midstream, and main EU countries suppliers such as Russia, Norway, USA, Algeria, Qatar, and Nigeria. Literature showed the possibility of LNG supply in the EU market in the long and short term during Russian disruption of Nord Stream and Ukraine war conflict. Additionally, studies focused on internal storages, pipe networks, and nodes in Europe, Many of the studies revealed various interactions between EU demand and supply and proposed several investments in natural gas corridors pipeline transport, LNG, and storage facilities. Moreover, some studies analyzed several scenarios for supply interruption for pipeline gas transit and LNG shipping receiving location and distribution. Others applied Ant Colony Optimization (ACO) to optimize fuel consumption in a real gas pipeline networks, and the results of which were compared to traditional optimization methods using Generalized Gradient Principles (GAMS) [41]. Moreover, studies involving chance-constrained multiobjective optimization framework for designing gas transmission lines which consider the minimization of the total annual were also made [42]. Recent studies focused on LNG regasification terminal capacity, pipeline network distribution and gas transit, storage, and underground strategic storage. These models developed various correlations and equations to solve EU demand and attempted several approaches to maximize indigenous demand reserves in the EU network, minimize costs (operational & capital), and optimize gas and LNG demand and availability in the region. A summary and comparison between those models is provided in Table 1.

Summary of the most prominent optimization models developed for LNG.

| Model description | Model type | Scope of application | |

|---|---|---|---|

| Meza et al. [24] | The model emulates the LNG value chain and predicts the future natural gas and LNG supply and demand until 2030 | Simulation, global | Global |

| Egging & Holz [43] | GASMOD analyzes the EU gas market based on supply and demand and upstream conditions | MCP | Global |

| Abada et al. [38] | The GAMMES model analyzes various disruption scenarios to the EU content by Russian gas and algerian stream | MCP | Global |

| Lise et al. [44] | The GASTALE model simulates the natural gas market and the transportation network in europe | MCP | Europe |

| Neumann et al. [36] | InTraGas maximizes the availability of natural gas reserves in the EU, identifies possible investments, and considers infrastructure, pipeline, LNG, and storage constraints | NLP | Europe |

| Lochran [25] | GNOME optimizes the natural gas supply, transportation, and storage on a monthly basis from 2015 to 2040 in 5-year steps and generates investment in pipelines, LNG regasification, and gas storage capacity | MILP | Europe |

| Egging et al. [34], 35] | The world gas model forecasts the worldwide natural gas industry and considers the cost of production, transportation cost via pipeline and LNG storages, and investment in pipelines and storage, permitting expansion of regasification and liquefaction facilities | LP | Global |

| Mulder & Zwart [39], 40] | NATGAS is a dynamic equilibrium model MCP that accounts for the actions of all market participants, including gas producers, investment in infrastructure (pipeline, LNG capacity, and storage), traders, and end-users in EU countries | MCP | Europe |

| Goryachev [45] | The nexant world gas model provides global and regional supply and demand balances and focuses on international trade via cross-border lines or LNG | LP | Global |

| Perner & Seeliger [22] | EUGAS predicts natural gas supply and demand in the EU up to 2030 quantitively | LP | Europe |

| Chyong et al. [46] | The EGMM is a mathematical model that represents horizontal oligopolistic relationships between gas producers and consumers | MCP | Europe |

| Hecking & Panke [47], 48] | The columbus model optimizes the future development of production, transport, and storage capacities considering LNG and pipelines | MCP | Europe |

| Lochner et al. [37] | The tiger model optimizes the supply of natural gas to the EU-27 countries plus Norway and Switzerland via the transmission grid using european production, non-european production injected at border points, and LNG imported through regasification terminals | LP | Europe |

-

LP: Linear programming; NLP: non – linear programming; MILP: Mixed – integer linear programming; MCP: mixed complementarity problem.

3 Mathematical model

One of the most common deterministic models used for LNG supply and demand is the linear programming model. In this model, the supply and demand of LNG are represented as linear equations, and the objective is to minimize the cost of supply and demand while meeting the required demand. The model takes into account factors such as shipping costs, infrastructure costs, and production costs.

Sets:

Let I be the set of NG exporting countries.

Let J be the set of NG importing countries.

Let K be the set intermediate countries through which NG imports/exports can be handled.

3.1 Objective function

The objective function of the model involves the maximization of the total profit of the NG network (revenue – cost), represented by equation (1) below:

Where Ri,j is the revenue generated as a result of sending NG from exporting country i to importing country j, R i,k is the revenue generated as a result of sending NG from exporting country i to intermediate country k, R k,j is the revenue generated as a result of sending NG from intermediate country k to importing country j, C i,j is the cost incurred as a result of sending NG from exporting country i to importing country j, C i,k is the cost incurred as a result of sending NG from exporting country i to intermediate country k, C k,j is the cost incurred as a result of sending NG from intermediate country k to importing country j.

To find the respective revenues, equations (2)–(4) can be used:

Where F i,j represents the amount of LNG sent from exporting country i to importing country j, P LNG is the price of LNG, while F PIPE i,j represents the amount of NG sent via pipelines from exporting country i to importing country j, and P NG is the price of natural gas send via pipelines.

Where F i,k represents the amount of LNG sent from exporting country i to intermediate country k, P LNG is the price of LNG, while F PIPE i,k represents the amount of NG sent via pipelines from exporting country i to intermediate country k, and P NG is the price of natural gas send via pipelines

Where F LNG k,j represents the amount of LNG sent from intermediate country k to importing country j, P LNG is the price of LNG, while F PIPE k,j represents the amount of NG sent via pipelines from intermediate country k to importing country j, and P NG is the price of natural gas send via pipelines.

To find the respective costs, equations (2)–(4) can be used:

Where F LNG i,j represents the amount of LNG sent from exporting country i to importing country j, C RG,CAPEX is the capital cost of regasification, C RG,OPEX is the operating cost of regasification, C SHIP is the cost of LNG shipping, while F PIPE i,j represents the amount of NG sent via pipelines from exporting country i to importing country j, C PIPE is the pipe maintenance cost, C LIQ is the liquefaction cost and C STR is the storage cost. It should be noted that since all pipeline infrastructure was assumed to exist, there were no capex considerations for pipelines.

Where F LNG i,k represents the amount of LNG sent from exporting country i to intermediate country k, C RG,CAPEX is the capital cost of regasification, C RG,OPEX is the operating cost of regasification, C SHIP is the cost of LNG shipping, while F PIPE i,k, represents the amount of NG sent via pipelines from intermediate country k i to importing country j, C PIPE is the pipe maintenance cost, C LIQ is the liquefaction cost and C STR is the storage cost. Similar to equation (5), since all pipeline infrastructure was assumed to exist, there were no capex considerations for pipelines.

Where F LNG k,j represents the amount of LNG sent from intermediate country k to importing country j, C RG,CAPEX is the capital cost of regasification, C RG,OPEX is the operating cost of regasification, C SHIP is the cost of LNG shipping, while F PIPE k,j represents the amount of NG sent via pipelines from intermediate country k to importing country j, C PIPE is the pipe maintenance cost, C LIQ is the liquefaction cost and C STR is the storage cost. Similar to equations (5) and (6), since all pipeline infrastructure was assumed to exist, there were no capex considerations for pipelines.

3.2 Constraints

The summation of all LNG flowrates F LNG i,j sent from exporting country i to all importing countries j plus the summation of all LNG flowrates F LNG i,k sent from exporting country i to all intermediate countries k must be less than or equal to the total LNG export capacity of country i, F i LNG Export Capacity , according to equation (8) below:

The summation of all NG flowrates via pipelines F PIPE i,j sent from all exporting countries i to importing country j plus the summation of all NG flowrates via pipelines F PIPE i,k sent from all intermediate countries k to importing country j must be less than or equal to the total pipe capacity of country j, F j PIPE Import Capacity , according to equation (9) below:

Since the aim is to replace a portion of the Russian NG to the EU by NG exports from other countries, the summation of all NG pipeline import capacities F j PIPE Import Capacity across all importing countries j, plus the summation of the LNG export capacities F i LNG Export Capacity from all exporting countries i, must be less than or equal to a fraction (θ) of the total LNG exports from Base, F NG-Base according to equation (10) below:

Additionally, the following constraints are also necessary:

The summation of LNG flowrates F LNG i,j from all exporting countries i to an importing country j, must be less than or equal to the existing gasification capacity of country j, GC j Exist plus the expanded gasification capacity of country j, GC j Expand , as per equation (11) below:

Moreover, the summation of LNG flowrates F LNG i,k from all exporting countries i to an intermediate country k, must be less than or equal to the existing gasification capacity of country k, GC k Exist plus the expanded gasification capacity of country k, GC k Expand , as per equation (12) below:

Moreover, the summation of LNG flowrates F LNG i,k from all exporting countries i to an intermediate country k, plus the summation of pipe flowrates F PIPE i,k from all exporting countries i to an intermediate country k, must be equal to the summation of all LNG flowrates F LNG k,j from country k across all importing countries j, plus the summation of all pipe flowrates F PIPE k,j from country k across all importing countries j, as per equation (13) below:

Moreover, the summation of LNG flowrates F LNG i,k from all exporting countries i to an intermediate country k, must be equal to the summation of all LNG flowrates from country k across all importing countries j, as per equation (13) below:

It is also very important to ensure that all LNG flowrates are non-negative:

Last but not least, all pipeline flowrates must also be non-negative:

The Linear Program (LP) presented above was implemented using the “Solver” option in MS-Excel 2021 on a Windows laptop with the following specifications: Intel(R) Core i7-7820HQ CPU @ 2.90 GHz 2.90 GHz, installed RAM 16.0 GB, and a 64 bit operating System, and the main variables are

4 Case study description

The developed model has been implemented and illustrated using several case studies. Those case studies involve different scenarios for Qatar to supply the EU, based on various percentages of Russian gas supply disruptions. Table 2 below summarizes the five scenarios that were carried out in this work, and their key features. Figure 1 also shows the main pipelines that were associated for conducting scenarios 2–5. Since case 1 is the base case, a random selection of all pipelines connecting different EU countries to the ENSTOG was assumed. Tables 3–5 also summarize all the data that were used to conduct the five different cases pertaining to the regasification capacities and the costing information. The proposed Linear Problem (LP) has been implemented using “What’sBest 19.0” LINDO solver for MS-Excel via a laptop with Intel Core i5 Duo processor, 8 GB RAM and a 64- bit operating system.

Summary of the five different case study scenarios investigated.

| Scenario | Description | Key features |

|---|---|---|

| 1 | [Base case scenario] random selection of existing pipelines for the supply of natural gas to the EU from intermediate countries that receive LNG from Qatar | Qatar supplies 50 % of Russian demand; no expansion or FID projects for regasification terminals; 20–30 % EU supplied via pipeline network |

| 2 | Using the southern corridor (between Turkey, Italy, Greece and Croatia) as the main corridor for the supply of natural gas to the EU from intermediate countries that receive LNG from Qatar |

|

| 3 | Using the new pipelines from Spain to the EU (midi catalonia pipeline) for the supply of natural gas to the EU from intermediate countries that receive LNG from Qatar | Assuming that Spain has excess LNG regasification terminal capacity, it could be used as an intermediate to supply excess LNG to the EU. Using the new pipelines from Spain to the EU (midi catalonia pipeline), or other proposed network for EU to diversify gas transit in EU. EU can use these facilities to develop network from Spain to nearest EU countries; surplus quantities cab be transported to the nearest EU countries via existing pipeline infrastructure. |

| 4 | Using the northern corridor (UK-Belgium-Netherlands) as the main corridor for the supply of natural gas to the EU from intermediate countries that receive LNG from Qatar | UK established an agreement with Qatar in the south hook terminal; whereby any surplus quantities can be sold to Belgium and Netherlands using exiting gas transmission infrastructure. France also has a terminal whereby it can send surplus gas to neighboring EU countries |

| 5 | Using the baltic sea corridor (between Germany, Lithuania, Poland) as the main corridor for the supply of natural gas to the EU from intermediate countries that receive LNG from Qatar | Germany ordered 4 FRSUs with total capacity around 18 MPTA; Qatar can supply Germany and Poland; Lithuania can regasify gas and send it to Poland and neighboring EU countries. |

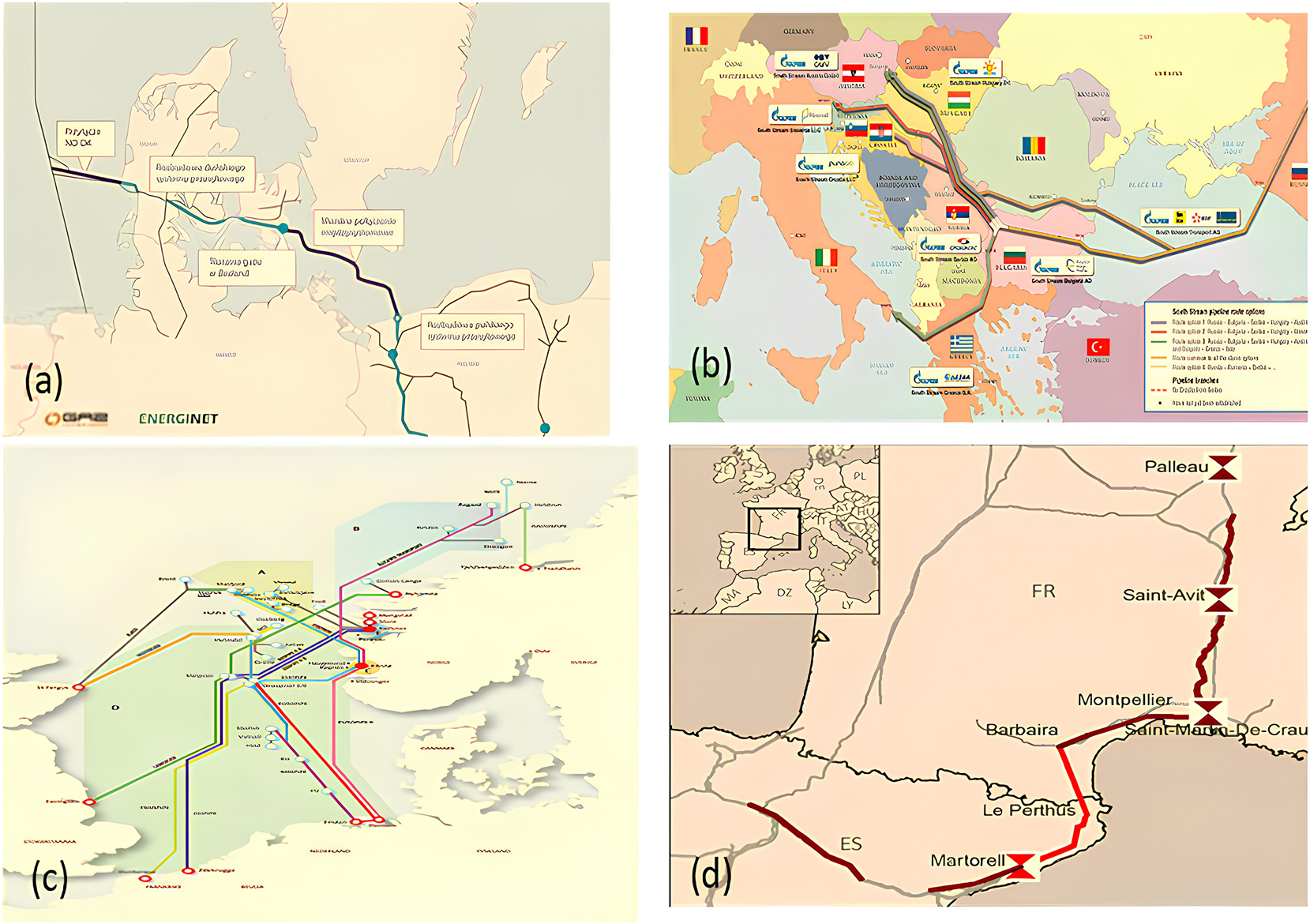

Illustrative figures for scenarios 2–5 pipe corridors (a) baltic sea – scenario 5 (b) southern corridor- scenario 3 (c) northern corridor – scenario 4 (d) Spain corridor – scenario 2.

Summary of the existing regasification capacities for various EU countries that were utilized in the 5 case studies described in Table 2.

| Country | Maximum regasification capacity in MTPA

|

|---|---|

| Turkey | 837.9 |

| Italy & Greece | 160.72 |

| Croatia | 211.484 |

| Spain | 965.3 |

| UK | 218.54 |

| Netherlands | 158.76 |

| France | 649.74 |

| Belgium | 160.72 |

| Germany | 490 |

| Poland | 42.63 |

| Lithuania | 88.2 |

Summary of the regasification capacity expansions for various EU countries that were utilized in the 5 case studies described in Table 2.

| Country | Expansion in regasification

|

Details |

|---|---|---|

| Turkey | +9.2 BCM/y equivalent to 6.8 MTPA | Gulf of saros FRSU |

| Italy | 8 BCM/y equivalent to 5.92 MPTA | Italy porto empedocle LNG plant project |

| Belgium | +8 BCM/y equivalent to 5 MPTA | Zebrugge LNG terminal expansion 1 & 2 |

| Croatia | 4.4 BCM/y equivalent to 3.256 MPTA | Krk LNG terminal expansion |

| Netherland | 1.5 BCM/y equivalent to 1.11 MPTA | Gate LNG terminal |

| Germany | 25 BCM/y equivalent to 18.5 | 4 FRSU new project announce in 2022 |

| Poland | 2.1 BCM/y equivalent to 1.554 | Świnoujście expansion |

Costs and parameters utilized in the modela.

| LNG shipping cost $/MBTU/km C SHIP | 1.3 |

| Pipe costs (OPEX) $/MBTU/km C PIPE | 2.1 |

| Cost of liquefaction $/MBTU C LIQ | 1.2 |

| Cost of storage $/MBTU C STR | 0.2 |

| Cost of regasification (OPEX) $/MBTU C RG,OPEX | 0.5 |

| Cost of regasification (CAPEX) $/MTPA C RG,CAPEX | 115 |

| Russian gas disruption percentage θ | 25 %, 50 % and 75 % |

-

a[IEA 2003, Oxford Institute for Energy Studying, The Palgrave Handbook of International Energy Economics].

5 Analysis of existing infrastructure in europe

In terms of the existing European pipeline infrastructure, there is an extensive network operating throughout the continent, supplying natural gas from various sources. The major suppliers include Russia, Norway, Algeria, and Asian countries via the Turkish Stream. Key pipelines in Europe include [49], 50]:

Northern Light: This pipeline originates from the Yamal gas field in Russia, passing through Poland. Its operational capacity is estimated to be 46-48 bcm per year.

Brotherhood Line: Supplying Europe with 120 BCM via Belarus and Ukraine, it transports gas produced from the Yamburgskoy reservoir in Russia. Its operational capacity is estimated to be 30 bcm per year.

Turkish Stream one and Turkish Stream 2: These pipelines facilitate the South-Eastern Corridor, transporting gas from Caucasus, Central Asia, and the Middle East via Turkey and the Black Sea. This route has a significant future potential. As such, the Turkish Stream pipeline project consists of two parallel pipelines, and their combined operational capacity is estimated to be 15.75 bcm/year.

Nord Stream 1: Twin pipelines with a capacity of 55 bcm to provide around 12 % of Europe’s total natural gas imports by 2035. It contributes to Europe’s energy supply security, passing through the Baltic Sea and serving consumers in Germany, Denmark, the UK, the Netherlands, Belgium, France, the Czech Republic, and other countries.

Nord Stream 2: is currently suspended, and some parts are still under construction. It is expected that Nord Stream 2 (which also consists of two lines) to further increase the total capacity of the Nord Stream to 110 BCM per year.

Pipeline from Algeria: The South-Western Corridor receives imports from Algeria, accounting for approximately 10 % of EU-27 annual consumption (50 bcm). The GPDF pipeline connects Morocco to Spain, while the Trans-Mediterranean pipeline supplies Italy.

These pipeline networks play a crucial role in meeting Europe’s natural gas demand and ensuring the continent’s energy security. Moreover, the European Network of Transmission System Operators for Gas (ENTSOG) is an organization dedicated to improving the national gas transmission infrastructure between European countries (Illustrated in Figure 2) [51]. It basically provides comprehensive information on pipelines and gas facilities across Europe through its Dashboard. The Dashboard offers daily forecasts of gas supply and demand, as well as real-time updates on gas quantities within The European Network. The data presented in this paper have been sourced primarily from ENTSOG to ensure accuracy and reliability. Moreover, Table 6 summarizes various pipelines that connect Europe to the ENSTOG network.

![Figure 2:

European network of transmission system operators for gas (Enstog) [51].](/document/doi/10.1515/cppm-2025-0017/asset/graphic/j_cppm-2025-0017_fig_002.jpg)

European network of transmission system operators for gas (Enstog) [51].

Summary of pipelines that connect various European countries to ENSTOG gas pipelines.

| Country | Pipeline connected with ENSTOG |

|---|---|

| Turkey | Turkish stream (Russia to Turkey), TNAP (Azerbaijan, Turkey, Greece), blue stream gas line (Russia to Turkey), kipi-komotini pipeline (Turkey to Greece) |

| Italy/Greece | Trans-mediterranean gas pipeline (Algeria, Tunisia, Italy, Croatia), Trans-Adriatic gas pipeline (Turkey, Greece, Albania, Italy) |

| Croatia | Croatian-Hungarian interconnection gas (Croatia section), Trans-Mediterranean gas pipeline (one supply branch to Croatia), donje mijoljac-oroslavke gas pipeline (Croatia main pipeline), interconnector Croatia-Serbia |

| Spain | Midi-catalonia pipeline (Spain, France – proposed), maghreb-europe gas pipeline (Algeria, Morocco, Spain) |

| UK | Balgzand-bacton line BBL gas pipeline (Netherlands, United Kingdom), zeebrugge-bacton gas pipeline (UK, Belgium) |

| Netherlands | Balgzand-bacton line gas pipeline BBL (Netherlands, United Kingdom), ravenstein-echt gas pipeline (Netherlands-Germany), bunde-emden gas pipeline (Netherlands-Germany), noordgastransport gas pipeline (Denmark to Netherlands), rotterdam antwerp pipeline (Netherlands to Belgium) |

| France | Franpipe gas pipeline, hauts de France II gas pipeline, paris-taisnieres gas pipeline (France-Belgium), morelmaison-rodersdorf gas pipeline, larrau-villar de arnedo gas pipeline (Spain), midi-catalonia pipeline |

| Belgium | Zeepipe gas pipeline (Norway to Belgium), zeebrugge-berneau gas pipeline, paris-taisnieres gas pipeline (France-Belgium), rotterdam antwerp pipeline (Netherlands to Belgium), zeebrugge-bacton gas pipeline (UK to Belgium) |

| Germany | Yamal stream (Belarus, Poland, Germany), nord stream gas pipeline (Russia to Germany), urengoy-pomary-uzhgorod gas pipeline, MIDAL gas pipeline (connect Dutch system with other distribution in Germany), STEGAL gas pipeline, europipe II gas pipeline, baltic sea project (under construction), norpipe gas pipeline |

| Poland | Baltic pipe (Norway, Denmark, Sweden, Poland), yamal-europe gas pipeline (Russia), gas interconnection Poland-Lithuania, potential connection to Czech republic, Slovakia, Hungary, the baltic states and even Ukraine |

| Lithuania | Gas interconnection Poland-Lithuania |

6 Results and discussion

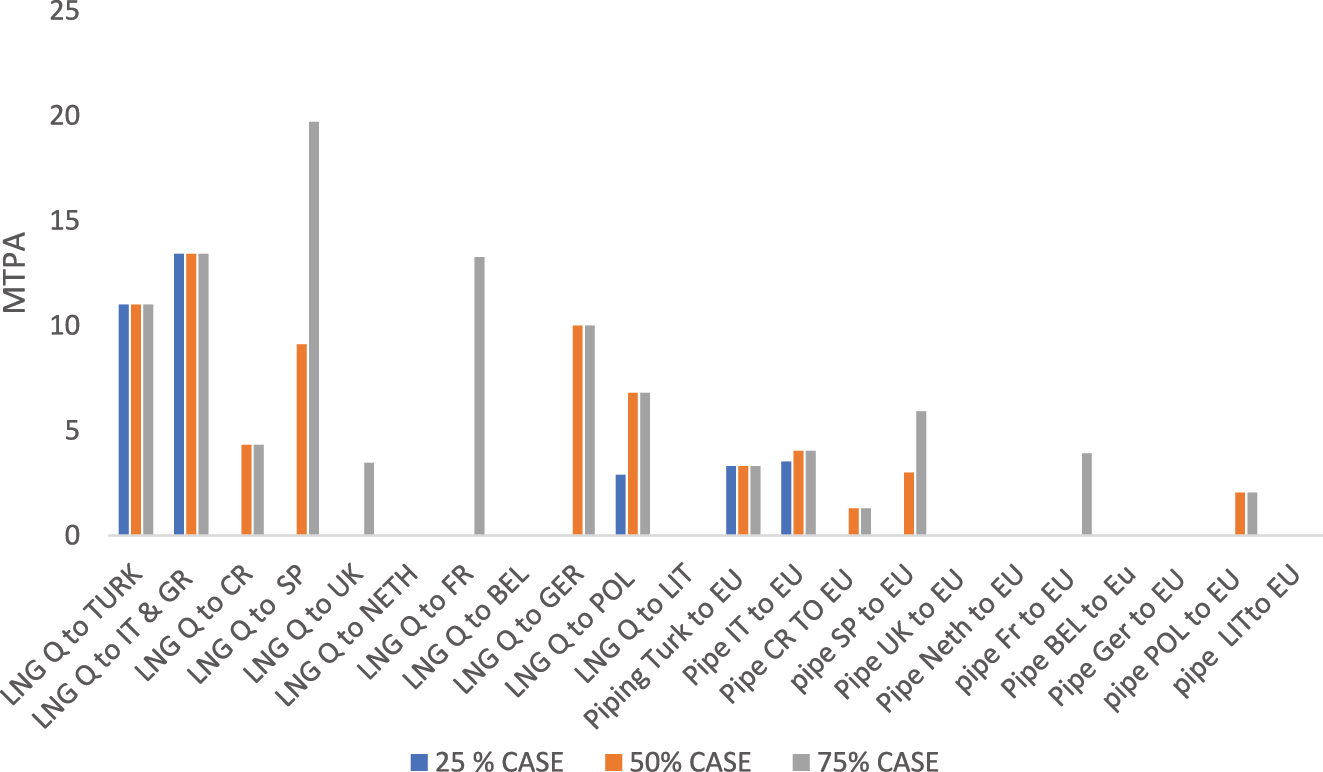

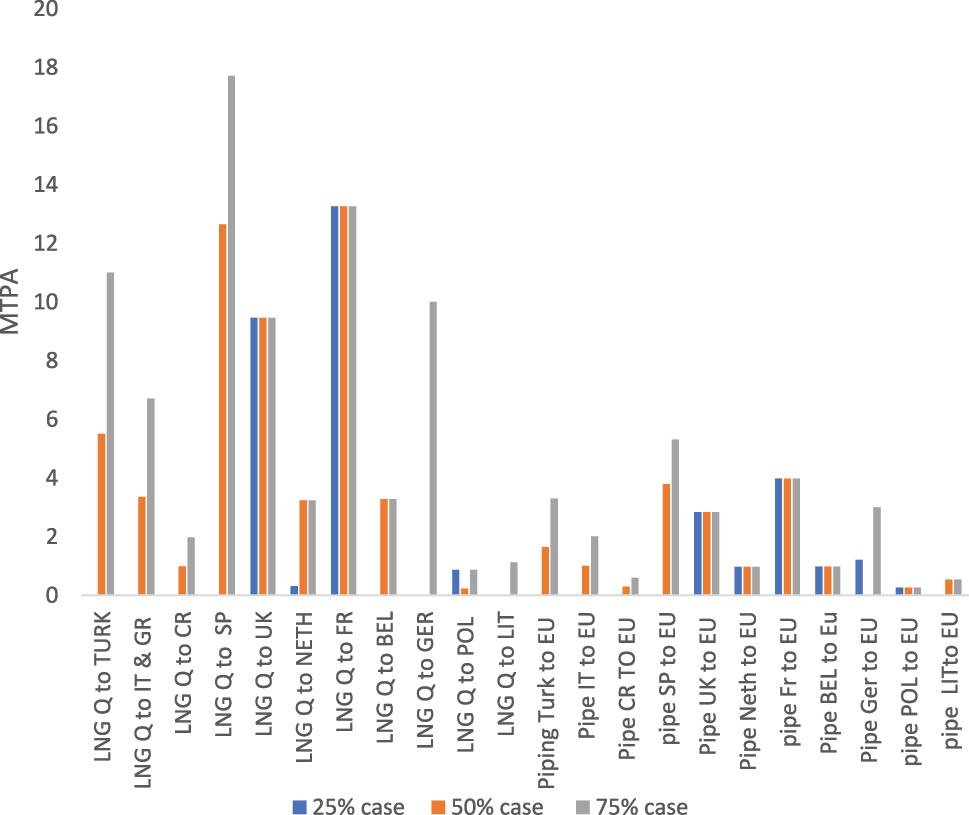

Various scenarios were investigated to replace Russian gas, considering disruptions of 25 %, 50 %, and 75 %, equivalent to 34 MTPA, 68 MTPA, and 102 MTPA, respectively. The results of the analysis show that the model converges on the nearest destinations that optimize the total operation cost of shipping. Each scenario was conducted by applying the different gas percentage disruptions (25 %, 50 % and 75 %) on the required EU demand. The capacities of the pipeline network were obtained from ENTSOG EU, with a focus on cross-border countries. Figure 3 illustrates the optimal allocation attained for Qatar’s LNG export to the EU for the base case scenario, considering 25 %, 50 % and 75 % of EU demand affected by Russian gas disruptions. The results indicate that Qatar’s LNG will primarily target the nearest destinations with sufficient buffer space in regasification and the pipeline network. In the base scenario (Scenario 1), Turkey, Italy, and Spain emerge as the major importers due to their available net free capacity in regasification units and optimal shipping costs. In the case of a 50 % Russian disruption, the model quantitatively solved for 7.6–8.38 MTPA to Turkey, Italy, and Greece, and 19.7 MTPA to Spain. The amount of natural gas to be transported via pipelines was found to be between 20 and 30 % of the total EU natural gas demand. Moreover, the remaining quantity would be supplied through intermediate pipelines to the UK, Netherlands, France, and ultimately to Germany and Poland. Table 7 provides a summary for the costs obtained for Scenario 1. The results show that for Scenario one and other scenarios with a 25 % replacement, Qatar would need to supply 34 MTPA, with an average network cost ranging from $8.1 billion to $8.8 billion per year. In the case of a 50 % disruption, the cost nearly doubles to a range of $16.5 billion to $17.5 billion, and for a 75 % disruption, it reaches $21 billion to $24 billion per year. The highest cost component in the LNG chain is liquefaction, accounting for around 38–40 %, followed by upstream operations (20–24 %) and shipping costs (13–18 %).

Scenario 1, optimal allocations attained for LNG flows from Qatar to the EU in metric tons per annum (MTPA), and optimal allocations for natural gas pipe flows after regasification, from intermediate countries to the EU in metric tons per annum (MTPA) assuming 25 %, 50 % and 75 % of total gas import disruptions from Russia to Europe.

Summary of costs obtained for Scenario 1- base case.

| 25 % case | 50 % case | 75 % case | |

|---|---|---|---|

| Shipping cost (billion $/y) | 1.175 | 2.644 | 3.601 |

| Gasification cost (billion $/y) | 0.809 | 1.667 | 2.103 |

| Pipeline operation cost (billion $/y) | 0.803 | 1.574 | 1.574 |

| Upstream operation cost (billion $/y) | 2.008 | 4.015 | 5.114 |

| Storage cost (billion $/y) | 0.335 | 0.669 | 0.852 |

| Liquefaction cost (billion $/y) | 18.778 | 37.557 | 56.335 |

| LNG revenue (billion $/y) | 51.862 | 103.725 | 132.119 |

| CO2 emissions (million tons/y) | 0.478 | 0.956 | 1.152 |

| Boil off methane (million tons/y) | 0.034 | 0.068 | 0.082 |

Scenario two suggests several strategic routes for Qatar to supply LNG to the EU through the southern corridor, which involves exporting LNG from Qatar to Turkey, Italy, Greece, and Croatia. These countries have significant gas and LNG infrastructure and are connected to major stream pipelines and intermediate countries with high natural gas demand in the southeastern EU. Qatar could secure long-term supply in this region by negotiating with Gazprom, which has shares in many of the pipeline networks. The southern corridor also has existing cross-border lines connecting Turkey, Italy, Greece, and Croatia, extending up to Hungary, Austria, Slovenia, and the border of Switzerland. This region has a high demand perspective for natural gas and LNG, and proposed stream projects could potentially reach Germany in the future. Figure 4 shows the optimal allocations attained for LNG flows from Qatar to the EU in metric tons per annum (MTPA), and optimal allocations for natural gas pipe flows after regasification, from intermediate countries to the EU in metric tons per annum (MTPA) assuming 25 %, 50 % and 75 % of total gas import disruptions from Russia to Europe. The linear solver converges to provide maximum amount capacity LNG shipping to countries like Turkey, Italy, Greece and Croatia.

Case 2, optimal allocations attained for LNG flows from Qatar to the EU in metric tons per annum (MTPA), and optimal allocations for natural gas pipe flows after regasification, from intermediate countries to the EU in metric tons per annum (MTPA) assuming 25 %, 50 % and 75 % of total gas import disruptions from Russia to Europe.

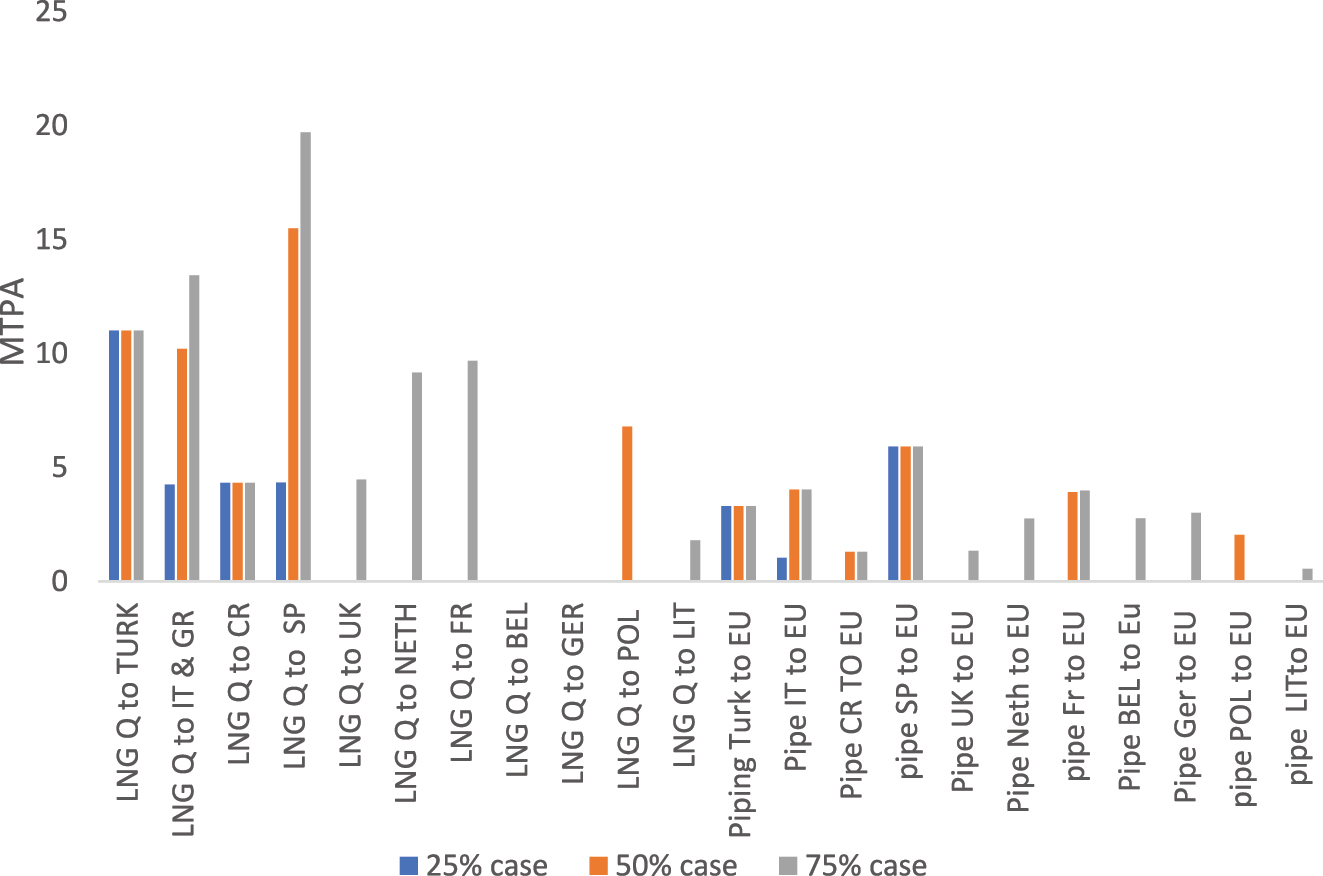

As for the third scenario, the maximum share of Qatar’s LNG was allocated to Spain, which has the highest LNG terminal capacity in the EU. Figure 5 shows the optimal allocations attained for LNG flows from Qatar to the EU in metric tons per annum (MTPA), and optimal allocations for natural gas pipe flows after regasification, from intermediate countries to the EU in metric tons per annum (MTPA) assuming 25 %, 50 % and 75 % of total gas import disruptions from Russia to Europe. For a 50 % Russian disruption, it was found that Spain could receive 25.3 MTPA from Qatar, with 7 MTPA distributed through pipelines to other EU countries via France. Any excess amount could be exported to the UK, Netherlands, Belgium, and France. However, for a 75 % disruption, Spain will not be able to receive additional LNG due to the lack of regasification terminal expansion projects. Instead, the surplus capacity could be supplied to the southern corridor and northern corridor regions. Enhancing the pipeline network between Spain and EU countries would help diversify energy imports and exports, according to the EU commission. Moreover, proposed projects like Midi-Catalonia and VIP Pirineos could also improve the network connection between France and Spain.

Case 3, optimal allocations attained for LNG flows from Qatar to the EU in metric tons per annum (MTPA), and optimal allocations for natural gas pipe flows after regasification, from intermediate countries to the EU in metric tons per annum (MTPA) assuming 25 %, 50 % and 75 % of total gas import disruptions from Russia to Europe.

The fourth scenario focuses on expanding LNG supply from Qatar to the northern corridor countries, including the UK, Belgium, the Netherlands, and France. The natural gas transmission networks in these countries are interconnected, facilitating gas trade. Qatar already has agreements with the UK’s South Hook terminal. This scenario also accounts for the expansion of the Gate terminal in the Netherlands and the Zeebrugge LNG terminal in Belgium. Figure 6 shows the optimal allocations attained for LNG flows from Qatar to the EU in metric tons per annum (MTPA), and optimal allocations for natural gas pipe flows after regasification, from intermediate countries to the EU in metric tons per annum (MTPA) assuming 25 %, 50 % and 75 % of total gas import disruptions from Russia to Europe. Around 46 to 47 million tonnes per annum (MTPA) of LNG imported through the northern corridor were obtained, whilst considering the upcoming expansion. Any excess gas can then be supplied to neighboring countries or routed through the Netherlands trade point to Germany. However, it is important to note that the cost for the LNG chain and shipping in this scenario was 70 % higher compared to other scenarios due to the increased distance covered by LNG ships, including multiple canals and seas. Additionally, any surplus gas from the network can also be stored in underground storage (UGS) facilities to meet winter and high peak season demands.

Case 4, optimal allocations attained for LNG flows from Qatar to the EU in metric tons per annum (MTPA), and optimal allocations for natural gas pipe flows after regasification, from intermediate countries to the EU in metric tons per annum (MTPA) assuming 25 %, 50 % and 75 % of total gas import disruptions from Russia to Europe.

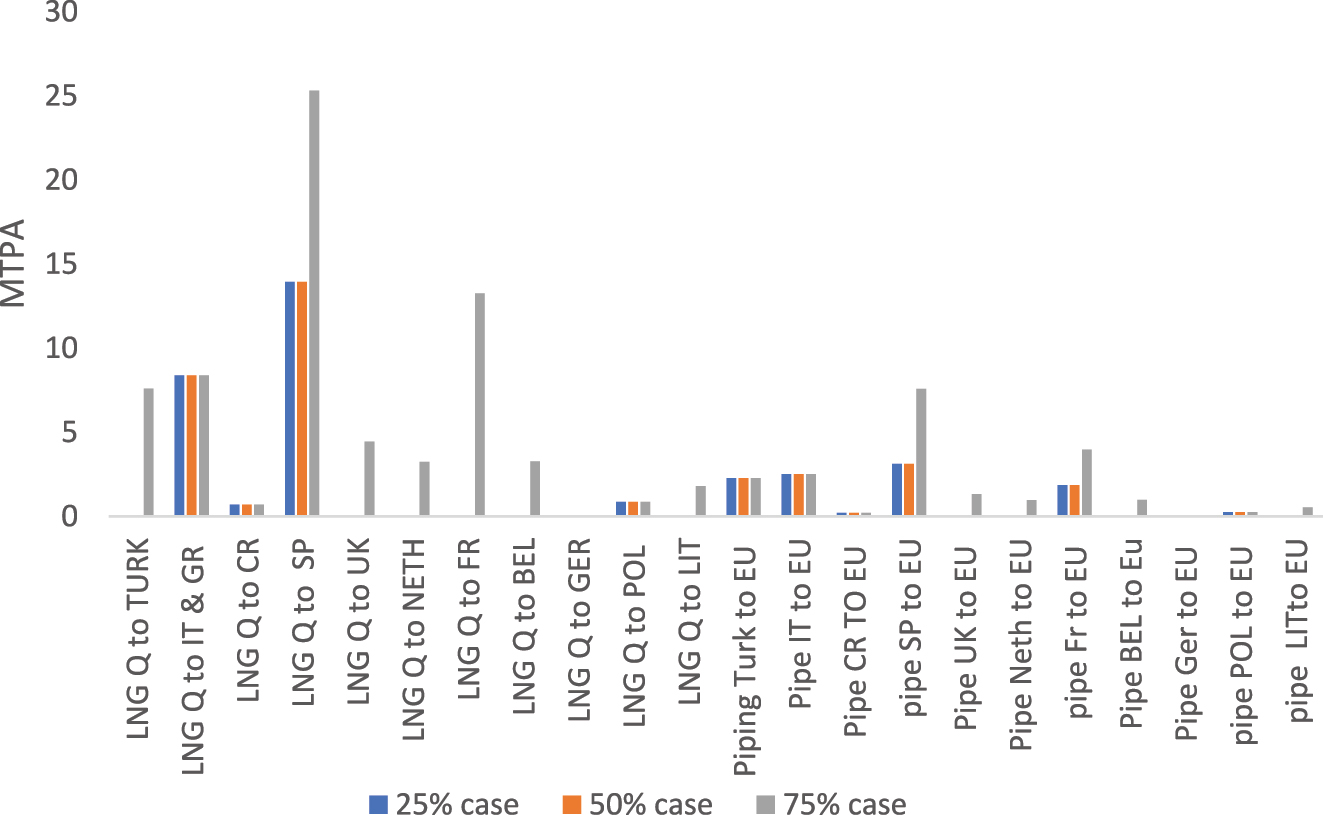

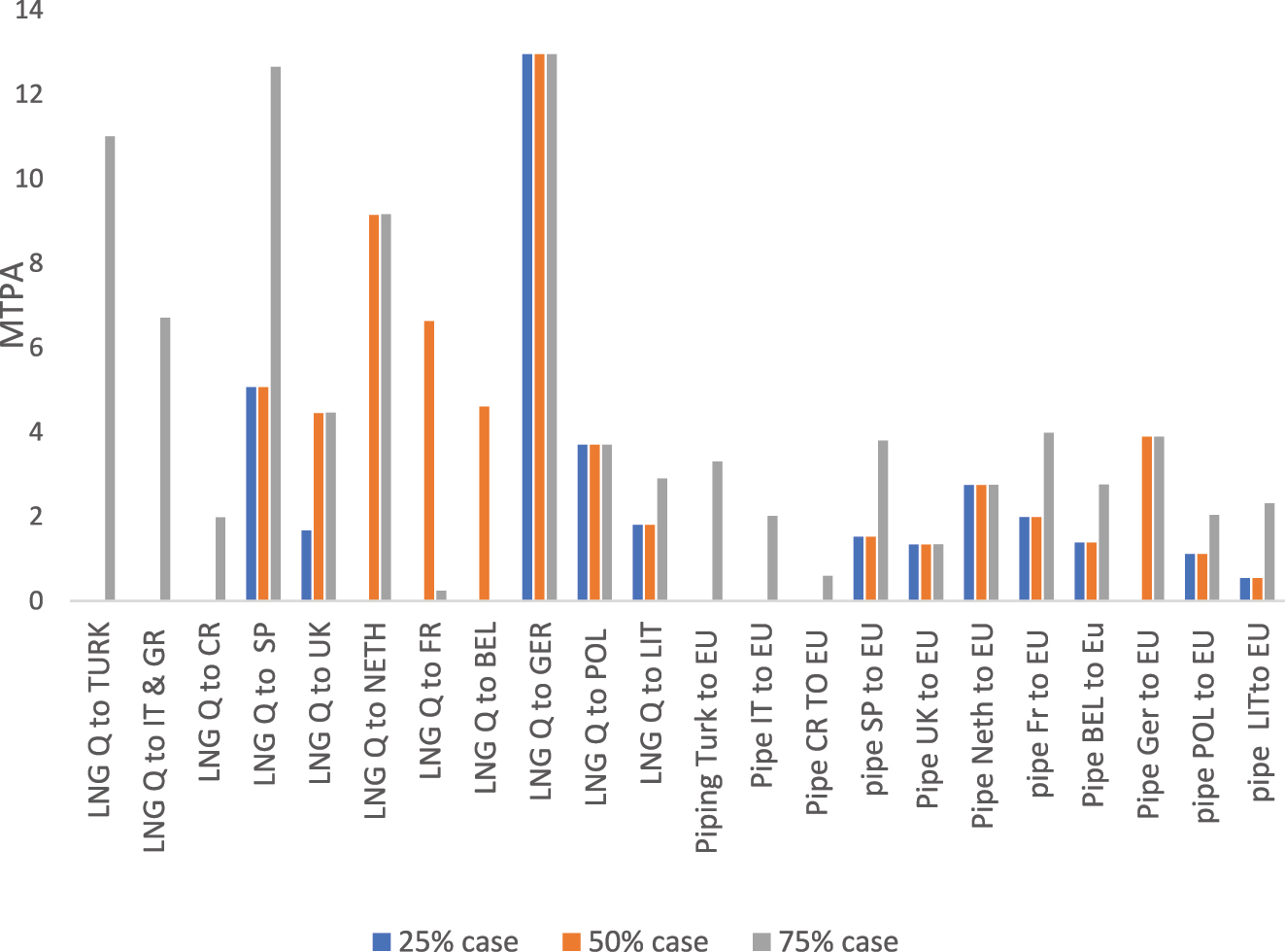

Lastly, Scenario five explore the opportunity for Qatar to consider exporting LNG to the Baltic Sea region through Germany and Poland. The expansion of the Swinoujcie LNG Terminal in Poland, along with the floating regasification unit (FRSU) in Germany, would allow Qatar to supply several EU countries in the Baltic Sea region, including Germany. In this scenario, additional regasification capacities in Germany and the expansion of regasification terminals in Poland were taken into consideration. Figure 7 provide the optimal allocations attained for LNG flows from Qatar to the EU in metric tons per annum (MTPA), and optimal allocations for natural gas pipe flows after regasification, from intermediate countries to the EU in metric tons per annum (MTPA) assuming 25 %, 50 % and 75 % of total gas import disruptions from Russia to Europe. In the 50 % case, the output from the mathematical model converged to fill the gap in the furthest region of the EU, encompassing Germany, Poland, and Lithuania, which includes regasification terminals and the upcoming Germany FRSU (Floating Storage and Regasification Unit). The optimal solution attained for this case involved shipping 18.5 MTPA of LNG to the region, with 12.25 MTPA allocated to Germany, 3.7 MTPA to Poland, and 1.8 MTPA to Lithuania. The remaining capacity was distributed through the pipeline network to supply neighboring regions near the Baltic Sea and the Northern corridor. It’s worth noting that the total network cost was higher compared to cases 2–4, due to the increased distance covered by LNG shipping, ranging between 7,500 and 8,200 miles.

Case 5, optimal allocations attained for LNG flows from Qatar to the EU in metric tons per annum (MTPA), and optimal allocations for natural gas pipe flows after regasification, from intermediate countries to the EU in metric tons per annum (MTPA) assuming 25 %, 50 % and 75 % of total gas import disruptions from Russia to Europe.

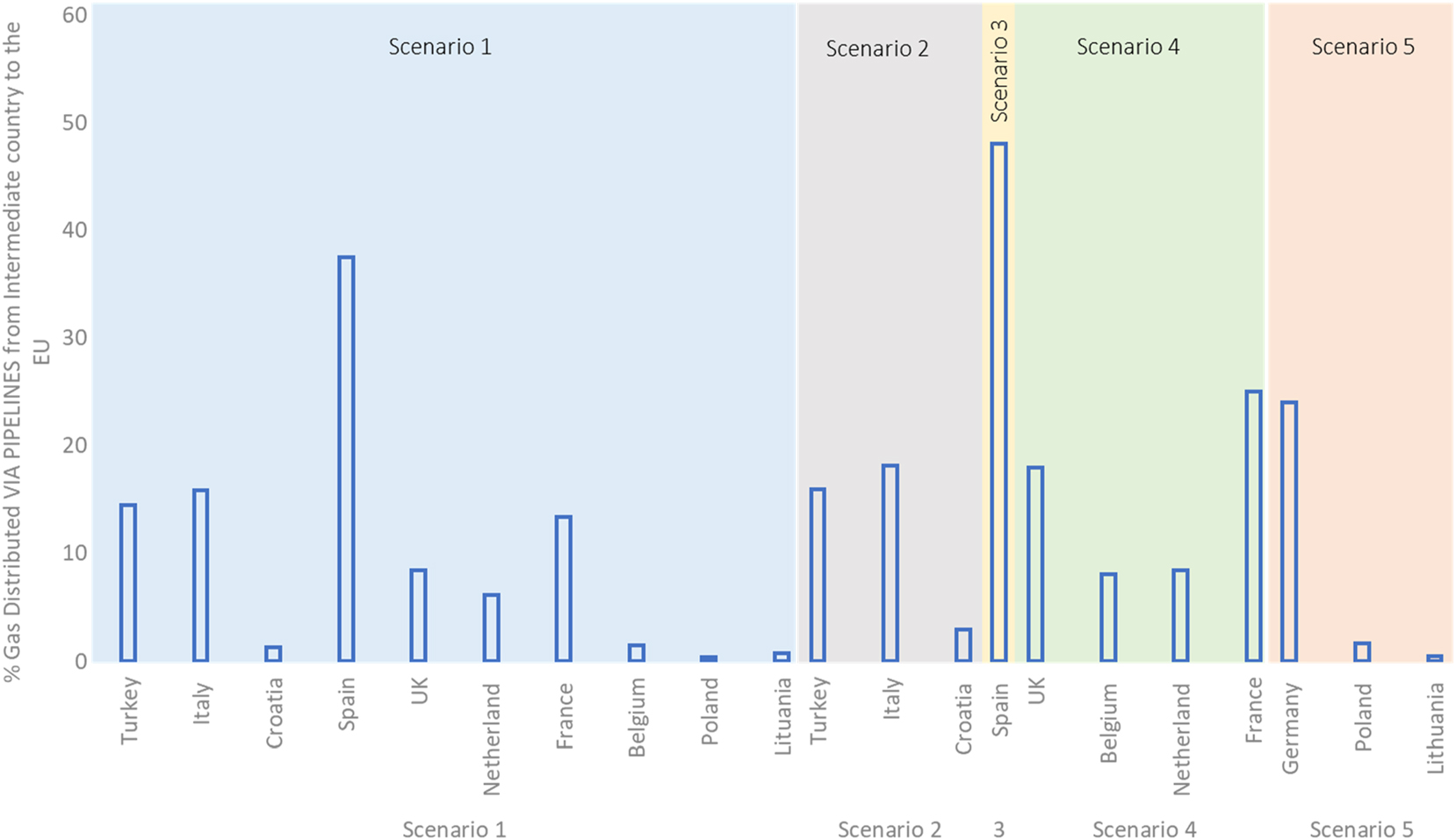

In summary, the analysis conducted in Scenarios 1–5 provides insights into various strategic scenarios for Qatar to export LNG to the EU, considering different corridors and their associated costs, capacities, and infrastructure. The southern corridor, Spain, the northern corridor, and the Baltic Sea region all present opportunities for Qatar to supply LNG to the EU, with each scenario having its own advantages and challenges. Each scenario involves a number of different countries acting as intermediate suppliers (whereby they receive excess LNG from Qatar, and any excess gas is regasified within the intermediate countries and sent via existing pipe infrastructure to the EU through ENSTOG). Figure 8 provides a summary of the optimal gas distribution percentages via ENSTOG pipelines associated with the intermediate countries that were identified in scenarios 1–5.

Summary of the optimal gas distribution percentages via ENSTOG pipe associated with the intermediate countries that were identified in scenarios 1-5.

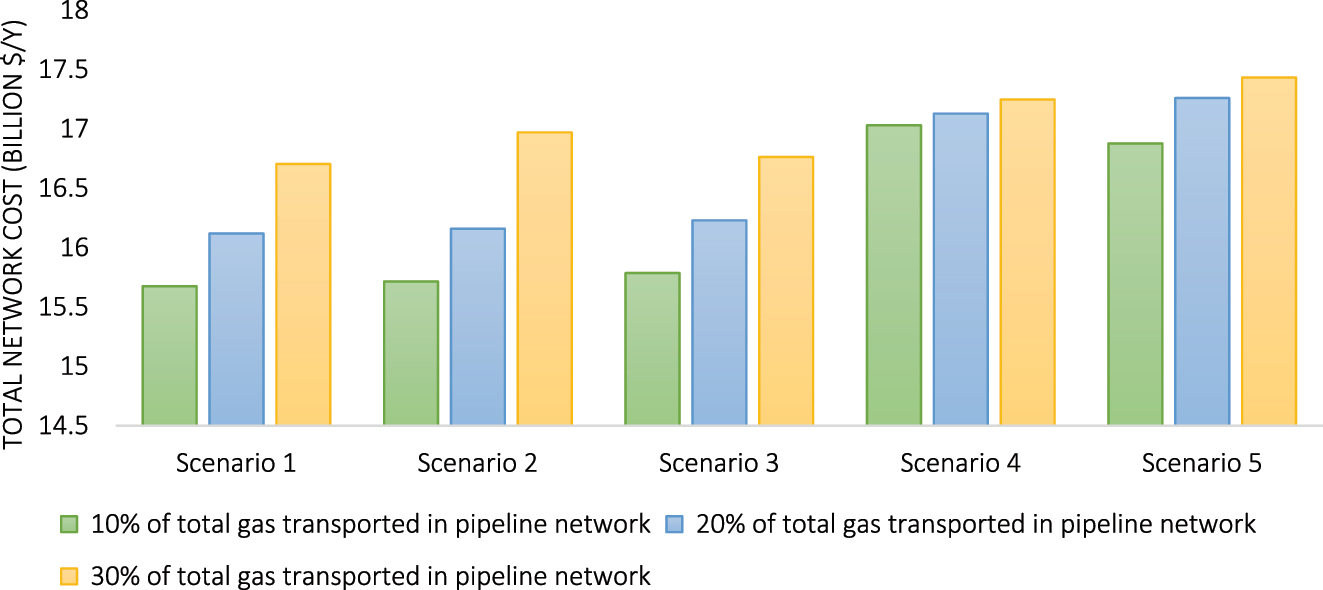

This analysis was further extended, by adjusting the maximum percentage of the total gas that can be supplied to the EU via pipelines. In scenarios 1–5, the EU pipeline network was able to meet around 20 %–30 % of the usual demand for natural gas in the EU, since the maximum constraint was set to 30 %. This percentage was revisited, based on which a corresponding change in the cost margin was observed, amounting to $0.5 billion. Figure 9 summarizes the total costs of the network obtained for scenarios 1–5, after placing an additional constraint on the maximum amount of gas that is allowed to be transported via pipelines. Three different cases were studied for each scenario, being 10 %, 20 % and 30 % as the maximum percentages set for the total gas that can be supplied to the EU via pipelines, which scenarios four and five yielding the highest network costs. It was found that scenarios four was the least sensitive to increasing the % of the total gas that can be supplied to the EU via pipelines, while scenario two was the most sensitive to the placement of this additional constraint.

Scenarios 1–5 revisited, after placing an additional constraint on the maximum amount of gas that is allowed to be transported via pipelines.

By 2027, with Qatar’s LNG output projected to reach 128 MTPA and the addition of four mega trains, the country would be able to meet the entire demand in Russia. However, achieving the goal of completely replacing Russian gas in the European Union would certainly require Qatar to cancel some of its long-term contracts in Asia. Typically, there already exists a cross-border line and network connectivity near the LNG import destinations. The main challenge lies in reaching agreements with the Gas Network operator to facilitate the regasification LNG from Qatar in intermediate countries, and enable the distribution of this gas via existing pipeline infrastructure within the EU.

While this study primarily addresses the technical and economic optimization of LNG transportation routes by taking Qatar to Europe as an example, it is important to recognize that the practical implementation of such rerouting strategies is heavily influenced by geopolitical and contractual factors. Qatar currently holds long-term supply contracts with key markets in the Far East, and redirecting volumes to Europe would require complex renegotiations. These contractual obligations, coupled with broader geopolitical dynamics, create significant challenges that cannot be resolved solely through infrastructure or cost optimization. Therefore, any proposed changes in LNG supply patterns must be viewed within the context of evolving international relations and market negotiations, highlighting that technical feasibility does not automatically translate into immediate practical solutions. Future work should integrate these political and commercial dimensions to provide a more comprehensive assessment of LNG supply reconfiguration possibilities.

7 Conclusions

In conclusion, this study presents a comprehensive approach to optimizing LNG transportation to Europe by integrating pipeline networks with LNG shipping through a linear programming (LP) model. The model simultaneously considers infrastructure capacities, operational constraints, and cost components, including liquefaction, shipping, regasification, and pipeline transport, so as to identify cost‐optimal allocation strategies under different Russian gas disruption scenarios (25 %, 50 %, and 75 %, equivalent to 34, 68, and 102 MTPA, respectively). Results show that the solver prioritizes deliveries to destinations with available regasification capacity and low transport costs, with key importers including Turkey, Italy, Spain, and northern corridor countries. Total network costs were reported to range from $8.1–8.8 billion for a 25 % disruption, $16.5–17.5 billion for 50 %, and $21–24 billion for 75 %, with liquefaction representing the largest cost share (38–40 %). The LP model results also highlight that fully replacing Russian gas is costly, and would require renegotiating long‐term contracts and improving EU pipeline connectivity through agreements with many network operators.

-

Research ethics: Not applicable.

-

Informed consent: Not applicable.

-

Author contributions: All authors have accepted responsibility for the entire content of this manuscript and approved its submission. M.M performed statistical and computational analyses, developed the LP model, gathered and processed the data, wrote an initial draft of the manuscript and contributed to the results and discussion sections. S.A. developed the research idea, designed the study, assisted in the development of the LP model, ensured technical accuracy and supervised the overall project. Moreover, S.A. contributed to data analysis, the interpretation and visualization of the results, in addition to editing and finalizing the manuscript. A. B. assisted in literature review, manuscript formatting, contributed to editing and finalizing the manuscript, and provided critical revisions to enhance the intellectual content of the paper.

-

Use of Large Language Models, AI and Machine Learning Tools: None declared.

-

Conflict of interest: The authors state no conflict of interest.

-

Research funding: None declared.

-

Data availability: Not applicable.

Nomenclature

- R i,j

-

NG revenue made by exporting country i to importing country j

- R i,k

-

NG revenue made by exporting country i to intermediate country k

- R k,j

-

NG revenue made by intermediate country k to importing country j

- C i,j

-

NG cost incurred by exporting country i to importing country j

- C i,k

-

NG cost incurred by exporting country i to intermediate country k

- C k,j

-

NG cost incurred by intermediate country k to importing country j

- F LNG i,j

-

LNG flowrate from exporting country i to importing country j

- F LNG i,k

-

LNG flowrate from exporting country i to intermediate country k

- F LNG k,j

-

LNG flowrate from intermediate country k to importing country j

- F PIPE i,j

-

flowrate of NG via pipeline from exporting country i to importing country j

- F PIPE i,k

-

flowrate of NG via pipeline from exporting country i to intermediate country k

- F PIPE k,j

-

flowrate of NG via pipeline from intermediate country k to importing country j

- F i LNG Export Capacity

-

total LNG export capacity of country i

- F j PIPE Import Capacity

-

total pipe capacity of country j

- C RG,CAPEX

-

Regasification capital cost

- C RG,OPEX

-

Regasification operating cost

- C LIQ

-

LNG liquefaction cost

- C STR

-

LNG storage cost

- C SHIP

-

LNG shipping cost

- C PIPE

-

Pipe maintenance cost

- (θ)

-

Fraction

- F NG-Base

-

Total LNG exports from base country

- GC j Exist

-

Existing gasification capacity of country j

- GC j Expand

-

Expanded gasification capacity of country j

- GC k Exist

-

Existing gasification capacity of country k

- GC k Expand

-

Expanded gasification capacity of country k

References

1. Fahmy, MFM, Nabih, HI, El-Rasoul, TA. Optimization and comparative analysis of LNG regasification processes. Energy 2015;91:371–85. https://doi.org/10.1016/j.energy.2015.08.035.Suche in Google Scholar

2. Meza, A, Koç, M. The LNG trade between Qatar and east Asia: potential impacts of unconventional energy resources on the LNG sector and Qatar’s economic development goals. Resour Policy 2021;70:101886. https://doi.org/10.1016/j.resourpol.2020.101886.Suche in Google Scholar

3. Meza, A, Koç, M, Al-Sada, MS. Perspectives and strategies for LNG expansion in Qatar: a SWOT analysis. Resour Policy 2022;76:102633. https://doi.org/10.1016/j.resourpol.2022.102633.Suche in Google Scholar

4. Farag, M, Zaki, C On the economic and political determinants of trade in natural gas. World Econ 2024;47:806–36. https://doi.org/10.1111/twec.13453.Suche in Google Scholar

5. Tamba, JG, Essiane, SN, Sapnken, EF, Koffi, FD, Nsouandélé, JL, Soldo, B, et al.. Forecasting natural gas: a literature survey. Int J Energy Econ Policy 2018;8:216.Suche in Google Scholar

6. Walls, MAJR. Modeling and forecasting the supply of oil and gas: a survey of existing approaches. Energy 1992;14:287–309. https://doi.org/10.1016/0165-0572-92-90012-6.Suche in Google Scholar

7. Kim, K, Lim, S, Lee, C, Lee, WJ, Jeon, H, Jung, J, et al.. Forecasting liquefied natural gas bunker prices using artificial neural network for procurement management. 2022;10:1814, https://doi.org/10.3390/jmse10121814.Suche in Google Scholar

8. Su, M, Zhang, Z, Zhu, Y, Zha, D. Data-driven natural gas spot price forecasting with least squares regression boosting algorithm. 2019;12:1094. https://doi.org/10.3390/en12061094.Suche in Google Scholar

9. Wadud, Z, Dey, HS, Kabir, MA, Khan, SI. Modeling and forecasting natural gas demand in Bangladesh. 2011;39:7372-80, https://doi.org/10.1016/j.enpol.2011.08.066.Suche in Google Scholar

10. Mouchtaris, D, Sofianos, E, Gogas, P, Papadimitriou, T. Forecasting natural gas spot prices with machine learning. 2021;14:5782. https://doi.org/10.3390/en14185782.Suche in Google Scholar

11. Al-Haidous, S, Govindan, R, Elomri, A, Al-Ansari, T. An optimization approach to increasing sustainability and enhancing resilience against environmental constraints in LNG supply chains: a Qatar case study. Energy Rep 2022;8:9742–56. https://doi.org/10.1016/j.egyr.2022.07.120.Suche in Google Scholar

12. Bittante, A, Jokinen, R, Pettersson, F, Saxén, H. Optimization of LNG supply chain. In: Computer aided chemical engineering. Amsterdam: Elsevier; 2015:779–84 pp.10.1016/B978-0-444-63578-5.50125-0Suche in Google Scholar

13. Sabegh, ZA, Rasi, RE. A fuzzy goal-programming model for optimization of sustainable supply chain by focusing on the environmental and economic costs and revenue: a case study. Adv Math Finanace Appl 2019;4:103–23.Suche in Google Scholar

14. Doymus, M, Denktas Sakar, G, Topaloglu Yildiz, S, Acik, A. Small-scale LNG supply chain optimization for LNG bunkering in Turkey. 2022;162:107789. https://doi.org/10.1016/j.compchemeng.2022.107789.Suche in Google Scholar

15. Furlonge, H. A stochastic optimisation framework for analysing economic returns and risk distribution in the LNG business. Int J Energy Sect Manag 2011. https://doi.org/10.1108/17506221111186332.Suche in Google Scholar

16. Thompson, M. Natural gas storage valuation, optimization, market and credit risk management. J Commod Mark 2016;2:26–44. https://doi.org/10.1016/j.jcomm.2016.07.004.Suche in Google Scholar

17. Halkos, G, Tsirivis, A. Policy, Effective energy commodity risk management: Econometric modeling of price volatility. Munich: University Library of Munich; 2019, 63:234–50 pp.10.1016/j.eap.2019.06.001Suche in Google Scholar

18. Lv, X, Shan, X. Modeling natural gas market volatility using GARCH with different distributions. Phys A: Stat Mech Appl 2013;392:5685–99.10.1016/j.physa.2013.07.038Suche in Google Scholar

19. Barua, S, Gao, X, Pasman, H, Mannan, S. Bayesian network based dynamic operational risk assessment. J Loss Prev Process Ind 2016;41:399–410.10.1016/j.jlp.2015.11.024Suche in Google Scholar

20. Yang, X, Sam Mannan, M. The development and application of dynamic operational risk assessment in oil/gas and chemical process industry. Reliab Eng Syst Saf 2010;95:806–15. https://doi.org/10.1016/j.ress.2010.03.002.Suche in Google Scholar

21. Praks, P, Kopustinskas, V, Masera, M. Monte-Carlo-based reliability and vulnerability assessment of a natural gas transmission system due to random network component failures. Sustain Resilient Infrastruct 2017;2:97–107. https://doi.org/10.1080/23789689.2017.1294881.Suche in Google Scholar

22. Perner, J, Seeliger, A. Prospects of gas supplies to the European market until 2030—results from the simulation model EUGAS. Util Policy 2004;12:291–302. https://doi.org/10.1016/j.jup.2004.04.014.Suche in Google Scholar

23. Lochner, S. Modeling the European natural gas market during the 2009 Russian–Ukrainian gas conflict: ex-Post simulation and analysis. J Nat Gas Sci Eng 2011;3:341–8. https://doi.org/10.1016/j.jngse.2011.01.003.Suche in Google Scholar

24. Meza, A, Ari, I, Al-Sada, MS, Koç, M. Future LNG competition and trade using an agent-based predictive model. Energy Strategy Rev 2021;38:100734. https://doi.org/10.1016/j.esr.2021.100734.Suche in Google Scholar

25. Lochran, S. GNOME: a dynamic dispatch and investment optimisation model of the European natural gas network and its suppliers. Oper Res Forum 2021;2:67. https://doi.org/10.1007/s43069-021-00109-5.Suche in Google Scholar

26. Woldeyohannes, AD, Majid, MAA. Simulation model for natural gas transmission pipeline network system. Simulat Model Pract Theor 2011;19:196–212. https://doi.org/10.1016/j.simpat.2010.06.006.Suche in Google Scholar

27. Taghavifar, H, Perera, L. Life cycle assessment of different marine fuel types and powertrain configurations for financial and environmental impact assessment in shipping. In: ASME 2022 41st International Conference on Ocean. Hamburg, Germany: The American Society of Mechanical Engineers; 2022.10.1115/OMAE2022-78774Suche in Google Scholar

28. Taghavifar, H, Perera, LP. Life cycle emission and cost assessment for LNG-Retrofitted vessels: the risk and sensitivity analyses under fuel property and load variations. Ocean Eng 2023;282:114940. https://doi.org/10.1016/j.oceaneng.2023.114940.Suche in Google Scholar

29. Taghavifar, H, Prasad Perera, L. The effect of LNG and diesel fuel emissions of marine engines on GHG-reduction revenue policies under life-cycle costing analysis in shipping. In: ASME 2023 42nd International Conference on Ocean. Melbourne, Australia: The American Society of Mechanical Engineers; 2023.10.1115/OMAE2023-104508Suche in Google Scholar

30. Al-Haidous, S, Al-Ansari, T. Sustainable liquefied natural gas supply chain management: a review of quantitative models. Sustainability 2020;12:243. https://doi.org/10.3390/su12010243.Suche in Google Scholar

31. Berle, Ø, Norstad, I, Asbjørnslett, B. Optimization, risk assessment and resilience in LNG transportation systems. Int J Supply Chain Manag 2013;18:253–64. https://doi.org/10.1108/SCM-03-2012-0109.Suche in Google Scholar

32. Francisco, M, Revollar, S, Vega, P, Lamanna, R. A comparative study of deterministic and stochastic optimization methods for integrated design of processes. IFAC Proc Vol 2005;38:335–40. https://doi.org/10.3182/20050703-6-cz-1902.00917.Suche in Google Scholar

33. Liberti, L, Kucherenko, S. Comparison of deterministic and stochastic approaches to global optimization. Int Trans Oper Res 2005;12:263–85. https://doi.org/10.1111/j.1475-3995.2005.00503.x.Suche in Google Scholar

34. Egging, R, Holz, F, Gabriel, SA. The world gas model: a multi-period mixed complementarity model for the global natural gas market. Energy 2010;35:4016–29. https://doi.org/10.1016/j.energy.2010.03.053.Suche in Google Scholar

35. Egging, R, Holz, F, Christian von, H, Steven, AG. Representing GASPEC with the World Gas Model. Energy J 2009;30:97–117. http://www.jstor.org/stable/41323198.10.5547/ISSN0195-6574-EJ-Vol30-NoSI-7Suche in Google Scholar

36. Neumann, A, Viehrig, N, Weigt, H. InTraGas - a stylized model of the European natural gas network. Berlin: German Institute for Energy Economics and Economic Research; 2009. https://ssrn.com/abstract=1468247.10.2139/ssrn.1468247Suche in Google Scholar

37. Lochner, S, Bothe, D, Lienert, M. Analysing the sufficiency of european gas infrastructure-the tiger model. In: Conference Paper presented at ENERDAY. Dresden, Germany: TU Dresden; 2007.Suche in Google Scholar

38. Abada, I, Gabriel, S, Briat, V, Massol, O. A generalized nash–cournot model for the northwestern european natural gas markets with a fuel substitution demand function: the GaMMES model. Network Spatial Econ 2013;13:1–42. https://doi.org/10.1007/s11067-012-9171-5.Suche in Google Scholar

39. Mulder, M, Zwart, G. NATGAS. A model of the European natural gas market. CPB Netherlands Bureau for Economic Policy Analysis; 2006.Suche in Google Scholar

40. Zwart, G, Mulder, M. NATGAS: a model of the European natural gas market. CPB Netherlands Bureau for Economic Policy Analysis; 2006.Suche in Google Scholar

41. Arya, DAK, Honwad, DS. Optimal operation of a multi source multi delivery natural gas transmission pipeline network. Chem Prod Process Model 2018;13. https://doi.org/10.1515/cppm-2017-0046.Suche in Google Scholar

42. Behrooz, HA. A multiobjective robust approach for the design of natural gas transmission pipelines. Chem Prod Process Model 2019;14. https://doi.org/10.1515/cppm-2019-0055.Suche in Google Scholar

43. Egging, R, Holz, F. Global gas model: model and data documentation v3. 0 (2019). Berlin, Germany: Deutsches Institut für Wirtschaftsforschung; 2019.Suche in Google Scholar

44. Lise, W, Hobbs, BF, van Oostvoorn, F. Natural gas corridors between the EU and its main suppliers: simulation results with the dynamic GASTALE model. Energy Policy 2008;36:1890–906. https://doi.org/10.1016/j.enpol.2008.01.042.Suche in Google Scholar

45. Goryachev, AA. World gas models. Ind & Interind Compl 2015;26:327–37. https://doi.org/10.1134/s107570071504005x.Suche in Google Scholar

46. Chyong, CK, Hobbs, B. Strategic Eurasian natural gas market model for energy security and policy analysis: formulation and application to South Stream. Energy Econ 2014;44:198–211.10.1016/j.eneco.2014.04.006Suche in Google Scholar

47. Hecking, H and T Panke, COLUMBUS-A global gas market model. 2012, EWI Working Paper.Suche in Google Scholar

48. Hecking, H, Panke, T. COLUMBUS-A global gas market model. Cologne, Germany: Institute of Energy Economics at the University of Cologne; 2012.Suche in Google Scholar

49. IGU, World LNG Report 2022. International Gas Union; 2023.Suche in Google Scholar

50. British Petroleum. Statistical review of world energy; 2022.Suche in Google Scholar

51. ENSTOG. European network of transmission system operators for gas; 2023. [cited 2023 April]; Available from: https://www.entsog.eu/.Suche in Google Scholar

© 2025 the author(s), published by De Gruyter, Berlin/Boston

This work is licensed under the Creative Commons Attribution 4.0 International License.