Revisiting Multiplicity of Bubble Equilibria in a Search Model with Posted Prices

-

Stanislav Rabinovich

Abstract

Multiplicity of equilibria naturally obtains in search models of money with price posting: buyers’ money holdings depend on posted prices, which, in turn, depend on buyers’ money holdings. I show that this multiplicity of equilibria exists in general even when money is replaced with a dividend-bearing asset, as long as the asset is useful as a medium of exchange. If the fundamental value of the asset is sufficiently high, there is a unique equilibrium, in which the price of the asset equals its fundamental value. For lower fundamental values, there is a continuum of bubble equilibria, in which the price of the asset exceeds the fundamental value. For very low fundamental values, the equilibrium is again unique but the asset is not used as a medium of exchange. I characterize the set of symmetric and asymmetric bubble equilibria for both positive and negative fundamental values.

1 Introduction

Assets are valued both for their fundamental value – the stream of consumption that they generate – and for their liquidity, i. e. the extent to which they are useful as media of exchange. It is now well understood that the exchange role of assets can push their price above their fundamental value. This liquidity premium on assets has been emphasized by a growing literature in monetary economics, which explicitly models the frictions that make a medium of exchange essential. [1] This literature demonstrates that the endogeneity of the asset’s liquidity value often leads to multiple steady-state equilibria.

I study a particular channel through which decentralized trade can generate multiplicity of equilibria, namely a coordination problem resulting from price posting. In the model, agents use an asset to purchase an indivisible good in a frictional market. If sellers of this good post high prices, agents have an incentive to hold large amounts of the asset. This drives up the demand for the asset, which results in a high asset price. In turn, if the real value of the asset is high, sellers have an incentive to post high prices. Thus, there is a self-confirming equilibrium with a high asset price. Similarly, there is an equilibrium in which sellers post low prices, and the real value of the asset is low. Generically, whenever there exists a bubble equilibrium – one in which the asset price exceeds its fundamental value – there exists a continuum of such equilibria. I characterize the set of symmetric bubble equilibria for arbitrary fundamental values, including zero (fiat money) and negative values (e. g., a storage cost). In addition, even when a symmetric bubble equilibrium does not exist, I show that there may exist asymmetric bubble equilibria, in which some but not all agents carry the asset.

A growing literature in monetary theory, starting with Green and Zhou (1998), has established indeterminacy of steady state equilibrium in search models of fiat money. Jean, Rabinovich, and Wright (2010), and show that a continuum of steady-state monetary equilibria also exists in the price-posting version of the Lagos and Wright (2005) framework, which is more tractable than Green and Zhou (1998), and show that this indeterminacy can be interpreted as the result of a coordination problem between buyers and sellers. Since equilibrium indeterminacy seems to stem from the endogenous exchange value of money, Wallace (1998) conjectured that it disappears if fiat money is replaced by commodity money, or equivalently, by an asset that pays a dividend. I show this conjecture to be false in the Lagos and Wright (2005) framework: the indeterminacy is robust to the introduction of a positive dividend, as long as the value of the dividend is not too high. My contribution complements the work of Zhou (2003), who showed a similar robustness result in the Green and Zhou (1998) model. Furthermore, I provide a simple intuition for the multiplicity of equilibria when the dividend value is low, and the uniqueness when the dividend value is high. Specifically, when the dividend value of an asset exceeds the consumption utility of the good it is used to buy, the buyer’s budget constraint does not bind at the point of sale. As a result, the demand for the asset is not determined by whether it is useful in decentralized exchange, but is instead depends only on its dividend value. This uniquely pins down the price of the asset. When the dividend value is lower than the threshold, the value of the asset in exchange – which is endogenous – matters for its price, leading to the existence of bubble equilibria, in which the asset is valued above its dividend value. For very low dividend values, the equilibrium is again unique, but in this case the asset is not used as a medium of exchange.

The indivisibility of the good traded in the decentralized market is important for the result. Intuitively, because of the indivisibility, the exchange value of the asset is discontinuous in the amount of asset holdings. I discuss the role of indivisibility in more detail in Section 3.1. The nature of the price posting mechanism is also crucial. For example, there is a unique stationary equilibrium in the Lagos and Wright (2005) model if prices are instead determined by Nash bargaining, as shown in Wright (2010). In a closely related recent paper, Han et al. (2016) demonstrate that, even with indivisible goods, the equilibrium is unique under either Nash bargaining or competitive search. This is because, under Nash bargaining, the terms of trade are determined after the seller has observed the buyer’s asset holdings. Under competitive search, the seller commits to a price before meeting a buyer, but since buyers direct their search, the posted price affects the asset holdings choice of the buyer it attracts. In sharp contrast to Han et al. (2016), a coordination problem arises in my environment because each seller posts the selling price prior to observing the asset holdings of the buyer he/she is matched with; thus, posted prices can be conditioned only on the aggregate value of asset holdings.

My result also contributes to the aforementioned literature on the liquidity role of assets as media of exchange. This literature has emphasized the self-referential nature of liquidity: for example, since the liquidity value of an asset is at least partly endogenous, expectations of high asset prices in the future can lead to high asset prices today. I identify an additional – coordination-based – channel driving equilibrium indeterminacy. As explained above, my result shows that the liquidity role of an asset is more likely to cause its price to deviate from the fundamental value – and more likely to lead to multiple equilibria – when this fundamental value is low.

Finally, my result contributes to the literature on the Diamond (1971) paradox: the result that, in search models with price posting, sellers always extract the entire surplus from trade. Green and Zhou (1998) and Jean, Rabinovich, and Wright (2010) show that this need not hold when agents require money for trade, and their budget constraints are therefore endogenous. My result shows that the Diamond paradox reappears only if money is replaced with an asset of sufficiently high fundamental value.

2 Model

Time is discrete and the time horizon is infinite. There is a

There exists an asset that can serve as a medium of exchange in the DM. The asset is storable, is available in fixed supply,

3 Equilibrium

Let

Substituting

The optimal choice of

Suppose that a buyer with asset holdings

is the reservation price of a buyer with asset holdings

A stationary equilibrium, in general, features a distribution of posted DM prices and a distribution of asset holdings across agents in the DM, which, in turn, determines the distribution of reservation prices. Let

Since agents always have the option of buying the asset and not using it to purchase the DM good, any equilibrium must satisfy

the price of the asset must be at least equal to its discounted dividend value. Since I allow

In order for the asset market to clear in a symmetric equilibrium, each agent’s asset holdings must be equal to

Second, the posted price

The last restriction on the equilibrium with DM trade is more subtle. Agents must be willing ex ante to carry

Notice that eqs [5] and [9] imply eq. [7]: if buyers are willing to carry

From eqs [5] and [8], we conclude that

This motivates us to consider three regions of the parameter space; in particular, different values of

The first result shows that, if the fundamental value of the asset is sufficiently large, the equilibrium is unique.

Suppose that

By eq. [5],

If the fundamental value of the asset is large enough, then the buyer’s budget constraint cannot bind in the DM. Knowing this, the sellers charge the highest price that buyers are willing to pay ex post. This case is analogous to the Diamond (1971) result that the seller extracts the entire ex post surplus from trade. Moreover, because the buyer’s surplus from DM trades is zero, demand for the asset does not depend on its usefulness in exchange in the DM, and therefore the price of the asset,

I next consider the intermediate case, in which the fundamental value of the asset is enough to compensate the seller for the production cost in the DM, but smaller than the buyer’s utility of consumption in the DM.

Suppose that

Condition [5] implies

This gives an upper bound on

In this case, there is a continuum of equilibria, the lowest one of which has the asset priced at fundamental value. All other equilibria are bubble equilibria, in which sellers charge a price of the indivisible good that is – in terms of CM consumption – higher than the fundamental value of the asset. The buyer’s budget constraint binds in the DM, and demand for the asset on the margin is determined by the price that the seller charges, not the asset’s fundamental value. There thus exist multiple equilibria, despite the fact that the fundamental value of the asset is positive. Note that all the equilibria in Result 2 – and in Result 3 below – feature

Finally, I consider the case in which the dividend value of the asset is not enough to pay the cost of producing the DM good.

Suppose that

If

If

Note that the lower bound of this interval is strictly above

First, we show the existence of an equilibrium with

which can be rewritten as

The quantity

There are three important corollaries to Result 3. First, the fiat money case falls into this category. When

Second, Result 3 accommodates the possibility that

Third, when there is a continuum of equilibria, the lower bound on the range of equilibria is

In summary, I have established that a positive fundamental value does not eliminate the multiplicity of bubble equilibria unless this fundamental value is large enough – more precisely, so large that the buyer’s budget constraint is not binding in the DM. For an intermediate range of fundamental values, the set of symmetric bubble equilibria is an interval, with the fundamental value being its lower bound. Finally, for fundamental values below the cost of the DM good, the range of

The above analysis has demonstrated the multiplicity of symmetric bubble equilibria, in which the distribution of asset holdings is degenerate at

Note that, if the distribution of posted prices is degenerate at

It is easy to verify from eq. [12] that

This provides upper and lower bounds on

Suppose that

If

and the corresponding

If

and the corresponding

If

If

and the corresponding

If

This follows directly from combining [13] with the restriction

Intuitively, a lower bound on

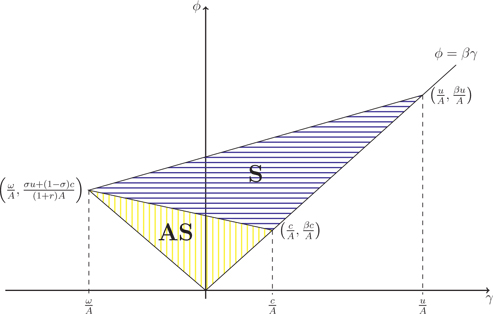

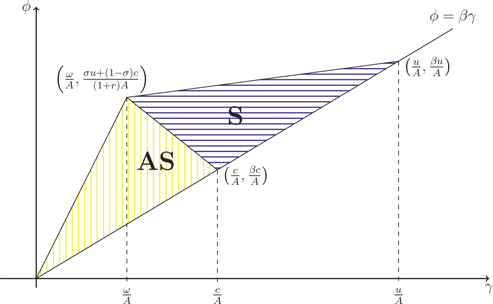

Figures 1 and 2 illustrate the set of equilibria for

The

The

3.1 Discussion: the role of indivisibility

This paper has established that the endogeneity of buyers’ budget constraints overturns the result of Diamond (1971) that sellers always extract the full surplus from buyers, and leads to the possibility of multiple equilibria, even with intrinsically valued assets.

As mentioned in the introduction, the indivisibility of the DM good is important for these results. To illustrate this, I now consider a modification of the model in which this good is divisible: the seller’s cost of producing a quantity

Instead of posting a price, sellers now post pairs

subject to the buyer’s individual rationality constraint

and the buyer’s budget constraint

It is easy to see that eq. [14] always binds. If it holds with strict inequality, the seller could increase profits by slightly lowering

In the above argument, the price of the asset always equals its fundamental value because DM trade generates zero surplus for the buyer. A growing literature suggests that this zero-surplus result is fragile, even with divisible goods. For example, Head et al. (2012) and Bethune, Choi, and Wright (2016) allow buyers to observe multiple prices or occasionally contact multiple sellers in the DM, as in Burdett and Judd (1983) and Lester (2011). Ennis (2008) and Dong and Jiang (2014) demonstrate that the zero-surplus result disappears when buyers have private information about their preferences. Revisiting the multiplicity of equilibria in these environments with intrinsically valued assets is a potential avenue for future research.

Acknowledgments

I thank Randall Wright for inspiration and useful advice on this paper. I thank Daniela Puzzello, Bruno Sultanum, two anonymous referees, and participants at the Workshop on Money, Banking, Payments and Finance at the Federal Reserve Bank of Chicago for helpful comments and discussions.

References

Bethune, Z., M. Choi, and R. Wright. 2016. Frictional Goods Markets: Theory and Applications.10.2139/ssrn.2727597Search in Google Scholar

Burdett, K., and K. L. Judd. 1983. “Equilibrium Price Dispersion.” Econometrica 51 (4):955–69.10.2307/1912045Search in Google Scholar

Diamond, P. A. 1971. “A Model of Price Adjustment.” Journal of Economic Theory 3 (2):156–68.10.1016/0022-0531(71)90013-5Search in Google Scholar

Dong, M., and J. H. Jiang. 2014. “Money and Price Posting Under Private Information.” Journal of Economic Theory 150 (C):740–77.10.1016/j.jet.2013.12.005Search in Google Scholar

Ennis, H. M. 2008. “Search, Money, and Inflation Under Private Information.” Journal of Economic Theory 138 (1):101–31.10.1016/j.jet.2007.01.016Search in Google Scholar

Geromichalos, A., J. M. Licari, and J. Suarez-Lledo. 2007. “Monetary Policy and Asset Prices.” Review of Economic Dynamics 10 (4):761–79.10.1016/j.red.2007.03.002Search in Google Scholar

Green, E. J., and R. Zhou. 1998. “A Rudimentary Random-Matching Model with Divisible Money and Prices.” Journal of Economic Theory 81 (2):252–71.10.1006/jeth.1997.2356Search in Google Scholar

Han, H., B. Julien, A. Petursdottir, and L. Wang. 2016. “Monetary Equilibria with Indivisible Goods.” Journal of Economic Theory 166:152–63.10.1016/j.jet.2016.08.007Search in Google Scholar

Head, A., L. Q. Liu, G. Menzio, and R. Wright. 2012. “Sticky Prices: A New Monetarist Approach.” Journal of the European Economic Association 10 (5):939–73.10.3386/w17520Search in Google Scholar

Jean, K., S. Rabinovich, and R. Wright. 2010. “On the Multiplicity of Monetary Equilibria: Green-Zhou Meets Lagos-Wright.” Journal of Economic Theory 145 (1):392–401.10.1016/j.jet.2009.03.006Search in Google Scholar

Kiyotaki, N., and R. Wright. 1989. “On Money as a Medium of Exchange.” Journal of Political Economy 97 (4):927–54.10.1086/261634Search in Google Scholar

Kiyotaki, N., and R. Wright. 1993. “A Search-Theoretic Approach to Monetary Economics.” American Economic Review 83 (1):63–77.Search in Google Scholar

Lagos, R. 2008. “The Research Agenda: Ricardo Lagos on Liquidity and the Search Theory of Money.” Economic Dynamics Newsletter 10 (1).Search in Google Scholar

Lagos, R. 2010. “Asset Prices and Liquidity in an Exchange Economy.” Journal of Monetary Economics 57 (8):913–30.10.1016/j.jmoneco.2010.10.006Search in Google Scholar

Lagos, R. 2011. “Asset Prices, Liquidity, and Monetary Policy in an Exchange Economy.” Journal of Money, Credit and Banking 43:521–52.10.1111/j.1538-4616.2011.00450.xSearch in Google Scholar

Lagos, R., G. Rocheteau, and R. Wright. 2016. “Liquidity: A New Monetarist Perspective.” Journal of Economic Literature (forthcoming).10.1257/jel.20141195Search in Google Scholar

Lagos, R., and R. Wright. 2005. “A Unified Framework for Monetary Theory and Policy Analysis.” Journal of Political Economy 113 (3):463–84.10.26509/frbc-wp-200211Search in Google Scholar

Lester, B. 2011. “Information and Prices with Capacity Constraints.” American Economic Review 101 (4):1591–600.10.1257/aer.101.4.1591Search in Google Scholar

Rocheteau, G., and R. Wright. 2005. “Money in Search Equilibrium, in Competitive Equilibrium, and in Competitive Search Equilibrium.” Econometrica 73 (1):175–202.10.26509/frbc-wp-200405Search in Google Scholar

Rocheteau, G., and R. Wright. 2013. “Liquidity and Asset-Market Dynamics.” Journal of Monetary Economics 60 (2):275–94.10.26509/frbc-wp-201016Search in Google Scholar

Wallace, N. 1998. “Introduction to Modeling Money and Studying Monetary Policy.” Journal of Economic Theory 81 (2):223–31.10.1006/jeth.1998.2440Search in Google Scholar

Wright, R. 2010. “A Uniqueness Proof for Monetary Steady State.” Journal of Economic Theory 145 (1):382–91.10.1016/j.jet.2009.11.004Search in Google Scholar

Zhou, R. 2003. “Does Commodity Money Eliminate the Indeterminacy of Equilibrium?” Journal of Economic Theory 110 (1):176–90.10.1016/S0022-0531(03)00007-3Search in Google Scholar

©2017 by De Gruyter

Articles in the same Issue

- Research Articles

- Economising, Strategising and the Vertical Boundaries of the firm

- Tight and Loose Coupling in Organizations

- Managerial Reputation, Risk-Taking, and Imperfect Capital Markets

- Simple Unawareness in Dynamic Psychological Games

- Better Product Quality May Lead to Lower Product Price

- Technology Licensing between Rival Firms in Presence of Asymmetric Information

- Risk-Averse Managers, Labour Market Structures, Public Policies and Discrimination

- Revisiting Multiplicity of Bubble Equilibria in a Search Model with Posted Prices

- Notes

- Welfare Analysis in an Extended Harris-Todaro Model: An Application of the Atkinson Theorem

- Are Invisible Hands Good Hands in Health Care Markets? Extension

- A Short Note on Discrimination and Favoritism in the Labor Market

Articles in the same Issue

- Research Articles

- Economising, Strategising and the Vertical Boundaries of the firm

- Tight and Loose Coupling in Organizations

- Managerial Reputation, Risk-Taking, and Imperfect Capital Markets

- Simple Unawareness in Dynamic Psychological Games

- Better Product Quality May Lead to Lower Product Price

- Technology Licensing between Rival Firms in Presence of Asymmetric Information

- Risk-Averse Managers, Labour Market Structures, Public Policies and Discrimination

- Revisiting Multiplicity of Bubble Equilibria in a Search Model with Posted Prices

- Notes

- Welfare Analysis in an Extended Harris-Todaro Model: An Application of the Atkinson Theorem

- Are Invisible Hands Good Hands in Health Care Markets? Extension

- A Short Note on Discrimination and Favoritism in the Labor Market