Loss Aversion and Consumption Plans with Stochastic Reference Points

-

Hyeon Park

Abstract

This paper studies the making of risky choices following loss aversion with endogenous reference expectations under the two schemes of state-independent and state-dependent stochastic reference points. Using a tractable, intertemporal choice model, this paper derives analytic solutions to show that, when loss aversion is high, the reference-dependent decision maker saves a markedly larger amount than is predicted by the standard model. When the loss aversion is low (i.e. the individual is loss-tolerant), the overall result is ambiguous, although the decision maker may deviate into consuming more; if he faces a small level of uncertainty relative to the intensity of his loss aversion, he may even do this by borrowing. Given the same loss aversion level, this study determines that, in the presence of positive state-dependence, the state-independent model generates greater deviation than the state-dependent one. Finally, this paper derives a two-period general equilibrium result with two agents who have different attitudes toward loss.

1 Introduction

Individuals’ attitudes toward loss affect their rational choices in the presence of uncertainty. As argued by Köszegi and Rabin (2006), individuals may not evaluate utilities in absolute level of outcomes, but instead in gains or losses of the outcomes relative to their reference expectations. The reference-dependent utility, a concept that was originally introduced by Kahneman and Tversky (1979), has been widely confirmed in lab experiments. [1],[2] The key features of their theory are reference dependence and loss aversion.

This paper, following the expectations approach by Köszegi and Rabin (2006, 2007, 2009), studies a stochastic intertemporal choice model for individuals who exhibit a reference-dependent preference and gain-loss utility. Unlike Köszegi and Rabin, however, we here posit that the attitudes of decision makers toward loss are not limited to loss aversion, but extend to the cases in which decision makers are tolerant of loss, [3] thereby illuminating the existence of decision makers with loss tolerance. This is important because a reference-dependent general equilibrium model of consumption and savings may not have an equilibrium interest rate without the existence of these consumers. In this paper, we analyze the behavior of both types of agents under both the state-independent [4] and state-dependent stochastic reference points, the latter of which are considered more empirically plausible in many applications including the field of finance according to Giorgi and Posty (2011). We specifically compare the results of this analysis with the results from a standard model under the condition of uncertainty. The general equilibrium result of the model shows that, at a given uncertainty level, both the borrowings and savings are smaller in the state-dependent model than in the state-independent one for all levels of interest rates. Moreover, the results of this study support the idea that, given a symmetric value of loss aversion/tolerance intensity, the state-dependent model agrees more with an even distribution of borrowers and savers in an economy for a wide range of income uncertainty.

It is well known that the standard lifecycle model alone cannot explain some puzzling features in consumption data, such as lifecycle consumption (which is hump-shaped) and the aggregate consumption growth (which is both excessively smooth and excessively sensitive). [5] Many researchers argue that a behavioral approach into consumption-saving models can solve these puzzles by introducing either time-inconsistent tastes or time-inconsistent expectations regarding future income. [6] In fact, the expectations-based reference-dependent preferences are thought to combine both of these elements, one through gain-loss utility (preferences) and the other through the reference points (expectations). [7] It is important, here, to ask what the reference point would be in the stochastic intertemporal choice model of reference expectation. Unlike in a deterministic intertemporal model of reference dependence wherein the reference points are the solutions to the dynamic optimization over time for a forward-looking agent, with uncertainty, it may be necessary to define the reference point over different states of the world for a state-contingent decision maker. [8]

This paper examines the making of intertemporal choices following loss aversion with stochastic reference expectations. We specifically want to study the consumption-saving behavior of decision makers who evaluate the utility in gains or losses of the outcomes relative to their reference expectations. The model that we analyze here is different from the majority of models of reference-dependent preferences. Unlike Chetty and Szeidl (2010), we develop this model with forward-looking expectations. Unlike Bowman, Minehart, and Rabin (1999), we construct its gain-loss utility in terms of reference-dependent expected utility instead of consumption-based habit formation. Also, avoiding the utility specification of exponential or HARA class that is used by Pagel (2013), we derive closed-form solutions [9] from CRRA. [10] In a method that differs from that used by many researchers, including Köszegi and Rabin (2009), we develop the consumption and saving model in the world of state-dependency. Moreover, we introduce a novel situation in which decision makers are allowed to have loss tolerance.

Our choice of expectation for the stochastic reference point follows from the recent developments in reference-dependent utilities models. One of these developments, studied by Cillo and Delquie (2006) and used by Köszegi and Rabin (2006, 2007, 2009), involves state-independent reference expectations. The other one involves state-dependent reference expectations, analyzed by Sugden (2003) and Giorgi and Posty (2011). The former posits that a decision maker evaluates every possible outcome of a prospect relative to all possible states of the reference point, while the latter assumes that the decision maker evaluates possible outcomes only in relation to the same state. Therefore, the decision maker should experience feelings of loss if the outcome of the prospect in a state falls short of any one of the reference outcomes in the other states in the state-independent world; in the state-dependent world, on the other hand, losses are only experienced when they occur within the same state.

Using these two reference plans, we derive closed-form solutions for the intertemporal choice of consumption and precautionary saving for various decision makers with different attitudes toward losses. A reference-dependent decision maker derives utility from making comparisons to the reference status, which may be a gain or loss to a reference point. A loss is assumed to be more important to a decision maker than a gain of the same size. Also, the intensity of loss aversion generates deviations in behavior among decision makers from that posited by the standard model of consumption-saving under uncertainty. Under the state-independent reference plan, these deviations come from a feeling of loss relative to the expected outcome of other states; under the state-dependent reference plan, they come from a feeling of loss relative to the expected outcome of the same state. However, in both plans, this study finds that decision makers with low loss aversion might want to overconsume, even via borrowing or dissaving. Unlike those who have high loss aversion, these individuals have relatively low loss feeling for a future outcome involving a bad state such as low income. Since the loss is not too painful than the gain is pleasant, their overall utilities would not be lowered by much even when a bad outcome is realized. Because they have little incentive to compensate for their feelings of loss by saving, they might be tempted to overconsume.

In the model we assume that a decision maker’s utility has two preference components. [11] One is the usual consumption utility (absolute level), and the other is the reference-dependent utility (contrast level); these two payoffs occurring over time interact with each other through intertemporal optimization in deterministic models. In the two-period consumption-saving model, however, because it is assumed that uncertainty arises only at the second period, the gain-loss utility relative to the reference state occurs at the second period. Our analysis shows that, when loss aversion is low relative to the standard model, it is possible for the decision maker to deviate from the usual precautionary saving behavior and engage in more consumption during the first period. When the loss aversion is high relative to the standard, however, the decision maker saves more than the standard model predicts. This results in a lesser amount of consumption in the first period, [12] but with a different magnitude according to which of the two state-related reference schemes is being used. Given the same intensity of loss aversion, this study finds that, when there is positive state-dependence, the state-independent model generates greater deviation than the state-dependent model from the standard behaviors involving both consumption and precautionary saving. [13] Finally, this study derives a two-period general equilibrium result of precautionary saving with two agents who have different attitudes toward loss.

2 Related Literature

By exploring forward-looking reference expectations and introducing a novel idea of loss tolerance, this paper contributes to the literature on consumption-savings model with reference dependence. The loss aversion in individuals’ consumption-saving behavior is well studied by Bowman, Minehart, and Rabin (1999) who develop a two-period consumption-savings model with loss aversion and show that when they are under sufficient income uncertainty, consumers may fail to reduce their consumption in response to adverse income shocks. This delayed response to shocks is due to loss aversion and reflection effects related to income uncertainty. Reducing their current consumption will lower consumers’ consumption below the reference point, which makes them feel a loss. The reflection effect implies that a risk-loving attitude toward loss makes consumers choose a lottery over a certain prospect. Thus consumers who would rather take a gamble will hesitate before reducing their consumption. However, the reference dependence as formulated in their model is not strictly different from the consumption-based habit, which might also be called reference dependence of consumption, [14] in that the reference point for the gain-loss utility is assumed to depend on past consumption. [15]

Chetty and Szeidl (2010) propose a model of forward-looking endogenous reference points, advancing an argument apparently similar to that of Köszegi and Rabin (2009) regarding recent expectations. Their model incorporates adjustment costs as the key mechanism for generating reference-dependent preferences whose reference points are consumption commitments. However, unlike the forward-looking mechanism used by Köszegi and Rabin (2009), their model is in fact backward-looking, in that the recent expectations are reflected in recent consumption choices and the current reference point is related to consumption in the recent past.

Pagel (2013) adapts the expectation-based, reference-dependent preferences used by Köszegi and Rabin (2009) to develop a lifecycle model based on news utility. Like that of Bowman et al. (1999), Pagel’s model demonstrates a delayed response to income shocks. This is because the lifecycle utility at a given point in the lifetime depends on layers of consumption expectations via the forward-looking formation of reference points through expectations about future income. This specification is closely related to the subject of the current paper, in that it posits that expectation comes from a forward-looking mechanism. However, Pagel’s model has two potential drawbacks: first, it assumes reference points that are state-independent. Second, its closed form solution is obtained only using unrealistic exponential utility functions.

Siegmann (2002) also uses reference-dependent preferences to construct a two-period consumption-savings model. The utility specification of his reference-dependence model is a one-sided value function (for losses) similar to the one used by Aizenman (1998), who also shows a positive relation between precautionary saving and uncertainty via disappointment aversion. Siegmann emphasizes the role of precautionary savings for a loss-averse agent by demonstrating that an increase in the uncertainty of future wealth has a nondecreasing effect on savings regardless of the expected return. His emphasis on the relationship between uncertainty and precautionary saving related to loss aversion is one element that the topic of the current paper has in common, although his approach does not provide a clear decomposition of loss aversion and risk aversion. He focuses specifically on the distribution of the return on savings and finds non-linearity in savings out of wealth. [16] Related with these, the classical literature on precautionary savings is: the importance of precautionary savings relative to the borrowing frictions of the model (Feigenbaum 2009); income uncertainty and precautionary savings (Carroll 1997; Gourinchas and Parker 2002; Feigenbaum 2008).

Two papers make cases for alternative positions regarding the model we are studying of the formulation of reference points. Sugden (2003), [17] who generalizes the subjective expected utility theory into a reference-dependent model, notices that an agent’s reference point may depend on the state of the world, but he adopts the status quo practice for the reference points. An agent’s reference point can simply be interpreted as the agent’s current endowments, letting the reference points be state-dependent. This is one way of modeling an agent’s reference point so that it is a function of the agent’s expectations. Another way to construct a reference point out of expectations may be the equilibrium approach suggested by Köszegi and Rabin (2006, 2007). On this view, the reference point is the optimal expectation, the one that maximizes an agent’s utility given any expectation generated by a strategy. Furthermore, these authors endogenize the reference point by allowing agents' beliefs to follow rational expectations. [18] In the case of stochastic reference points, they assume that an agent's beliefs fully reflect the true distribution of outcomes [19] and that gain-loss utility comes from comparisons made between the consumption lottery and a reference lottery, which are assumed to be independent. Köszegi and Rabin (2009) extend their model to a dynamic case that they construct by specifying that the agent should meet the rational consistency condition: any expectation generated by a dynamic strategy will maximize the agent’s utility in each period as long as the continuation strategies are consistent with rationality.

Other readings on the conceptual development about loss aversion include Rabin (2000), who shows that reference dependence may be an important factor in an agent's attitudes toward risk; many people have argued that aversion to small gambles is due in considerable part to loss aversion. Köbberling and Wakker (2005) demonstrate this by decomposing the risk attitude into three components: utility, probability weighting, and loss aversion. Krähmer and Stone (2013) discuss anticipated regret as an explanation of uncertainty aversion. They posit that the reference point depends on the agent's ex post beliefs about what he should have done ex ante (if he had the wisdom of hindsight), and thus in their model the loss aversion arises endogenously. Choosing a compound lottery for an uncertain option reveals information, and this changes the agent's ex post evaluation of the best decision to have made. They are in fact searching for the psychological foundations of uncertainty aversion. The work of Halevy and Felkamp (2005) takes a similar line.

Regarding the applicability of reference-dependence to economic models, Freeman (2013) claims that standard economic data can be consistent with the testable implications of the expectations-based reference-dependence models. [20] Because expectations do not appear in the data, reference points obtained from rational expectations may not properly reveal preferences. Freeman provides axiomatic foundations characterizing the testable implications of those models. A testable application of reference dependence in financial market can be found in Pasquariello (2014), who studies loss aversion and risk seeking in losses in terms of market quality.

3 Reference-Dependent Preferences

Following Köszegi and Rabin (2006), a riskless reference-dependent utility is defined by

where

where

Continuous, differentiable except at

Strictly increasing.

If

In a state-independent stochastic world, its outcome may be evaluated according to expected utility as suggested by the Von Neumann-Morgenstern preferences. This is one of the points at which the Köszegi and Rabin model is different from prospect theory by Kahneman and Tversky (1979). In prospect theory, a subjective weight function is used to evaluate a lottery. Reference-dependent expected utility implies a weighted average of the utilities of each of its possible outcomes relative to each possible realization of a stochastic reference point. Therefore, given a stochastic reference point

Assume further that there is only one dimensional state space for

where

in which

With intertemporal decision making, it is necessary to modify the gain-loss utility to incorporate the decision maker's psychological weight on the gain-loss utilities over time.

[24] Also, it is natural to posit that the weighting is likely to decay as its effect fades. To simplify the model for this, we assume that the initial strength of the concern for loss relative to gain is

4 Stochastic Reference Points

In this section we study a parametric model of reference-dependent utility with loss aversion. Specifically, we examine the consumption and precautionary saving plan of a reference-dependent decision maker who lives for two periods but faces uncertainty in the second period. Regarding the reference point, we first consider the case in which a decision maker evaluates every possible outcome of a prospect with all possible outcomes of the reference points, which effectively makes the reference point state-independent. In Section 4.2, we consider the case in which a decision maker evaluates all the possible outcomes of a prospect only in the same state. In this state-dependent situation, the decision maker experiences a loss only if the outcome of a prospect falls short of the reference point in the same state.

In Section 5, we derive a closed form solution in a simplified version of the model for both of the specifications. Based on the solution, in Section 6, we derive a two-period general equilibrium result with two agents who differ from each other in their attitudes toward loss. In partial equilibrium, where the interest rate is fixed, the policy variables such as consumption and bond demand are derived given any parameter values. However, in general equilibrium, the bond demand is a function of the equilibrium interest rate and the net bond supply should be equal to zero in equilibrium: b1+b2= 0 is the market clearing condition for the economy of two agents who have bond holdings, b1 and b2, respectively. The candidates for the two different agents of general equilibrium are many. [26] Because our focus in the model is on the strength of concern about loss, the first step may be to build a general equilibrium model with two different types of decision makers with respect to their degrees of loss aversion.

4.1 State-Independent Reference Points

To introduce formal models of stochastic reference points, let us define several notations first. Let

where

This specification of state-independence implies that every outcome of a prospect may act as a reference point. By this definition, a decision maker should have a feeling of loss whenever the outcome of a prospect in any state falls short of the one of the reference point in any other states. Let us assume that the decision maker (DM hereafter) lives for two periods

where

Notice that only two terms survive from the four expected contemporaneous gain-loss utility: there will be one gain utility and one loss utility at

4.2 State-Dependent Reference Points

In this subsection, we examine the case in which the reference points are state-dependent and may be chosen endogenously due to this dependency. Let us assume the same state space as in Section 4.1 and consider the following state-dependent model of reference-dependent preferences (RDP hereafter). For jointly continuous random variables, a risky prospect

where

where

In the example of the two-period consumption-saving model, in which the consumption and reference points are positively related, the total state-dependent RDP utility is given by

Comparing with

5 An Analytic Solution

In this section, we analyze a simplified two-period model of stochastic reference points that can be solved analytically. We first present the state-independent RDP model, then a state-dependent one, and then we compare the two. The purpose of this step is to show the role of gain-loss utility in the intertemporal decision-making and disentangle the implication of partial equilibrium from the one of general equilibrium. Consider an economy populated by different types of DMs who receive the same stochastic incomes in their second periods but differ from one another in their attitudes toward loss. We specifically focus on the case in which a DM deviates from the standard model due to loss aversion that is higher

First, we construct a simple model in which the DM faces uncertainty of his income in the second period. Assume that

The second term is expected consumption utility and the third and fourth terms are expected contemporaneous gain and loss utilities for the second period. The optimality condition leads to

Excepting the third term, this condition coincides with the standard Euler equation. The first two terms of

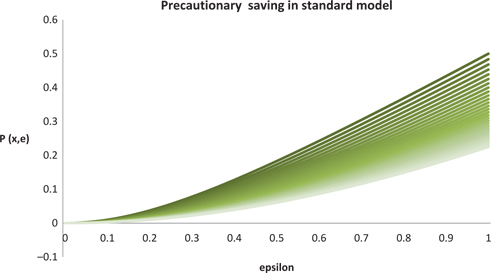

5.1 Precautionary Saving in A Standard Model

Following Deaton (1991), let us define cash on hand

assuming the same budget constraint. To compare this with the above reference-dependence model, we posit the same assumption of

Then the solution to the maximization problem in the standard model is

which is decreasing as the uncertainty parameter

which is increasing as the uncertainty parameter

Thus, it is clear that the last term in the above equation has a greater effect on the expected consumption under the condition of uncertainty (

One may notice that both the direction and the magnitude of consumption and saving remain the same in terms of

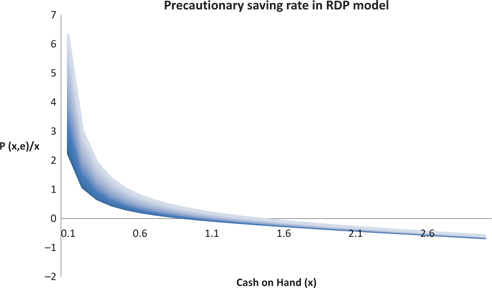

Equation [25] implies that given a level of cash on hand, the bond demand is always larger with uncertainty than without it. Using this fact, the precautionary saving is defined by

The precautionary saving increases as income uncertainty increases. However the effect of cash on hand on the precautionary saving is mixed: from eq. [27], when

Precautionary Saving in standard model

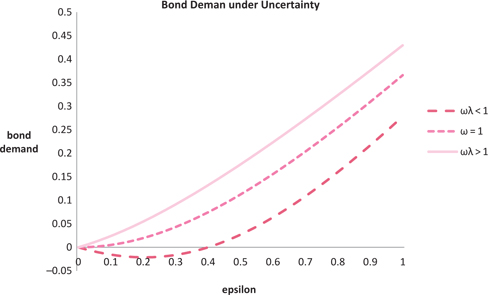

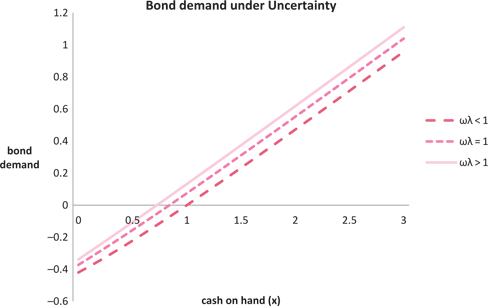

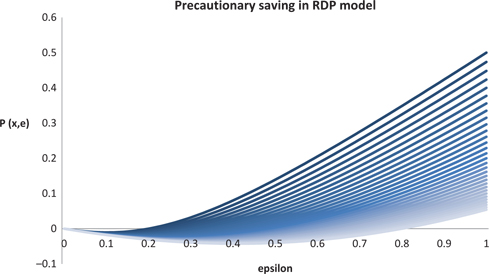

5.2 RDP Precautionary Saving

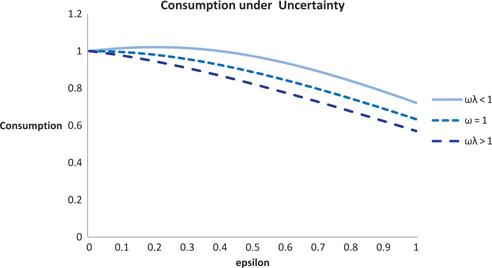

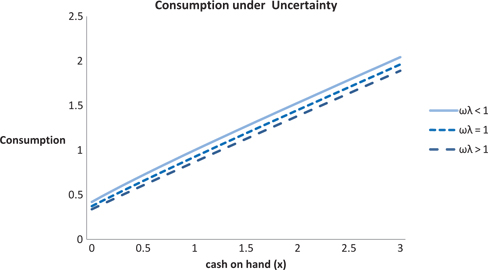

In the reference-dependence model, the consumption and saving profiles are affected by the gain-loss parameters. The loss aversion arises here with respect to bad outcomes due to uncertainty. Thus, as explained by eq. [15], high loss aversion (

The following (Figures 2, 3, 4, 5) show

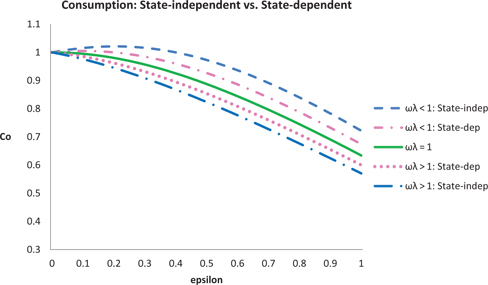

The next two figures (Figures 6 and 7) show

RDP plots of

RDP plots of

RDP plots of

RDP plots of

RDP(

RDP(

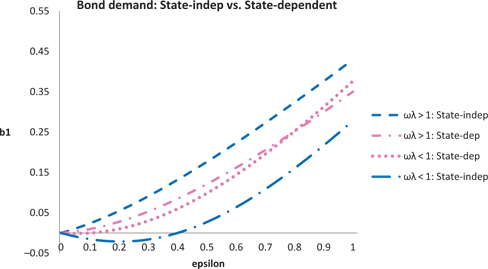

First, let us examine the bond demand. If

5.3 RDP-Dep Precautionary Saving

In the example of the two-period consumption-saving model, in which the consumption and reference points are positively related, the state-dependent RDP maximization problem is given by

Unlike the state-independent case, the gain or loss utility arises with

Excepting the third term, this optimality condition is equal to that of the state-independent RDP in previous subsection. Compared to state-independent RDP, for those who have a high loss aversion (

Likewise, the precautionary saving is obtained from

However, it is still true that if

Figure 8 displays RDP consumption when

RDP plots of

RDP plots of

6 General Equilibrium

In this section, we analyze equilibrium savings related to interest rates in a general equilibrium model, in which the economy is populated by two types of agents who are different in their degrees of loss aversion, but identical otherwise. Though it is possible to construct a general equilibrium model between loss-averse agents and standard agents

6.1 State-Independent RDP

From eq. [15], we know that each type of DM meets one of the following optimality condition:

How can we compare the two? Because

This implies that the three gain-loss marginal utilities satisfy:

Solving the equation brings consumption

while the bond demand of the DM(B) who is tolerant to loss (

Now let us introduce a market clearing condition for the economy. Assume that there are only two types of agents in the economy and that their intensity of loss aversion/tolerance is symmetric, i.e.

The state-independent bond demand with

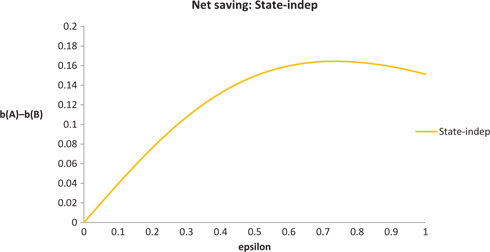

The state-independent net saving of the economy with

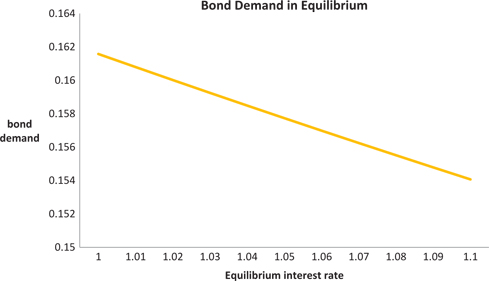

This implies that the economy should have more of the savers to lower the interest rate to meet the borrowers. In fact, a higher

where

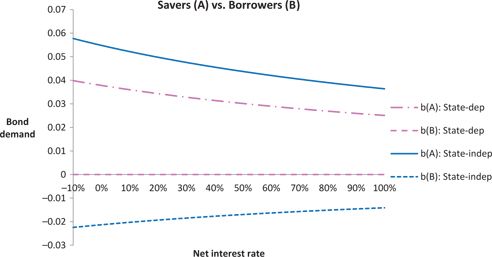

The state-independent equilibrium bond demand: the two agents are represented by

6.2 State-dependent RDP and Comparison

Following the similar steps as those in the state-independent RDP, the optimality condition for the two types of agents in the state-dependent model is given by:

The bond demand of the DM(A) who is loss averse (

while the bond demand of the DM(B) who is tolerant of loss (

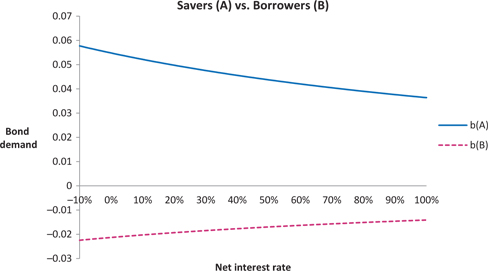

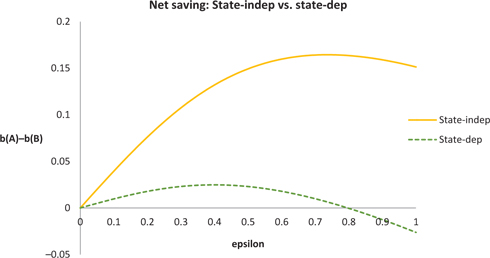

Figure 13 explains the saving and borrowing behaviors when the economy has an equal population of the two types of agents with both state-independent and state-dependent reference dependences. From the figure, it is clear that both borrowing and saving amounts are smaller for all levels of interest rates with the state-dependent model. Figure 14 demonstrates the variation in net savings corresponding to the uncertainty level. From this we may infer that for all levels of income uncertainty,

The state-independent and state-dependent bond demands with

The state-independent and state-dependent net savings of the economy with

7 Conclusion

In this paper, we study a model of reference-dependent preferences with endogenous reference expectations under the two schemes of state-independent and state-dependent stochastic references points. A key issue in reference-dependent utility models is the reference point, because as Pesendorfer (2006) claims, a reference point can be anything and may be selected arbitrarily by researchers. Often the reference point is assumed to be a current status, such as current consumption, position, or endowment. In this paper, we build a tractable, intertemporal choice model following two recent developments regarding expectation-based reference points: state-independent reference expectations, which originated in disappointment theory, and state-dependent reference expectations, which are based on regret theory.

We build the model according to the novel notion that some individuals might be loss-tolerant. Because of this assumption, we can provide a richer analysis that helps us better understand the consumption and precautionary saving behaviors of different types of consumers. Moreover, the model we develop has many merits in terms of economic modeling, in that it departs from typical aspects of reference-dependence, such as habit formation; adapts forward looking expectations; and uses realistic preference specifications.

In the two-period consumption-saving model, we derive analytic solutions to show that, when loss aversion is high, the decision maker saves more than the standard model predicts and thus consumes less in the current period. However, when the loss aversion is low, the overall result is ambiguous, although the decision maker may even want to borrow to consume more for the current period if he faces mild uncertainty relative to the intensity of his loss aversion. Given the same intensity of loss aversion, we find that the state-dependent model generates a smaller deviation than the standard one for both consumption and precautionary saving. Consequently, it is implied that for positively related consumption and its reference points, the state-independent model tends to exaggerate the true outcome of gain-loss feeling and vice versa. In both of the models, the meaning of precautionary saving can be defined in a different way from the standard model under uncertainty, although the size of this effect depends on whether it is state-dependent or not. Throughout this paper, we show that precautionary saving behavior is closely related to the degree of loss aversion, by which the decision makers may deviate for more or less consumption (and thus less or more saving) than what the standard uncertainty model predicts. Finally, from the general equilibrium exercise, we find that at a given uncertainty level, both borrowings and savings are smaller for all levels of interest rates with the state-dependent model. Also for all levels of income uncertainty, the state-dependent model agrees more with the even distribution of borrowers and savers.

References

Aizenman, J. 1998. “Buffer Stocks and Precautionary Savings with Loss Aversion.” Journal of International Money and Finance 17:931–47.10.1016/S0261-5606(98)00035-7Search in Google Scholar

Andersen, S., G. Harrison, M. Lau, and E. Rutström. 2008. “Eliciting Risk and Time Preferences.” Econometrica 76:583–618.10.1111/j.1468-0262.2008.00848.xSearch in Google Scholar

Bowman, D., D. Minehart, and M. Rabin. 1999. “Loss Aversion in a Consumption-Savings Model.” Journal of Economic Behavior and Organization 38:155–78.10.1016/S0167-2681(99)00004-9Search in Google Scholar

Carroll, C. D. 1997. “Buffer-Stock Saving and the Life-Cycle/Permanent Income Hypothesis.” Quarterly Journal of Economics 112:1–55.10.3386/w5788Search in Google Scholar

Chetty, R., and A. Szeidl. 2010. “Consumption Commitments: A Foundation for Reference-Dependent Preferences and Habit Formation.” Working Paper.Search in Google Scholar

Cillo, A., and P. Delquie. 2006. “Disappointment Without Prior Expectations: A Unifying Perspective on Decision Under Risk.” Journal of Risk and Uncertainty 33:197–215.10.1007/s11166-006-0499-4Search in Google Scholar

Deaton, A. 1991. “Saving and Liquidity Constraints.” Econometrica 59:1221–48.10.3386/w3196Search in Google Scholar

Feigenbaum, J. 2008. “Information Shocks and Precautionary Saving.” Journal of Economic Dynamics and Control 32:3917–38.10.1016/j.jedc.2008.04.008Search in Google Scholar

Feigenbaum, J. 2009. “Precautionary Saving Unfettered.” Working Paper, University of Pittsburgh.Search in Google Scholar

Freeman, D. 2013. “Revealed Preference Foundations of Expectations-Based Reference-Dependence.” Working paper.Search in Google Scholar

Giorgi, E., and T. Posty. 2011. “Loss Aversion with a State-Dependent Reference Point.” Management Science 57:1094–110.10.1287/mnsc.1110.1338Search in Google Scholar

Gourinchas, P., and J. A. Parker. 2002. “Consumption Over the Life Cycle.” Econometrica 70:47–89.10.3386/w7271Search in Google Scholar

Gul, F. 1991. “A Theory of Disappointment Aversion.” Econometrica 59:667–86.10.2307/2938223Search in Google Scholar

Halevy, Y., and V. Felkamp. 2005. “A Baysian Approach to Uncertainty Aversion.” Review of Economic Studies 72:449–66.10.1111/j.1467-937X.2005.00339.xSearch in Google Scholar

Kahneman, D., and A. Tversky. 1979. “Prospect Theory: An Analysis of Decision Under Risk.” Econometrica 47:263–91.10.21236/ADA045771Search in Google Scholar

Kobberling, V., and P. Wakker. 2005. “An Index of Loss Aversion.” Journal of Economic Theory 122:119–31.10.1016/j.jet.2004.03.009Search in Google Scholar

Krähmer, D., and R. Stone. 2013. “Anticipated Regret as an Explanation of Uncertainty Aversion.” Economic Theory 52:709–28.10.1007/s00199-011-0661-3Search in Google Scholar

Köszegi, B., and M. Rabin. 2006. “A Model of Reference-Dependent Preferences.” Quarterly Journal of Economics 121:1133–165.Search in Google Scholar

Köszegi, B., and M. Rabin. 2007. “Reference-Dependent Risk Attitudes.” American Economic Review 97:1047–73.10.1257/aer.97.4.1047Search in Google Scholar

Köszegi, B., and M. Rabin. 2009. “Reference-Dependent Consumption Plans.” American Economic Review 99:909–36.10.1257/aer.99.3.909Search in Google Scholar

Ludvigson, S. C., and A. Michaelides. 2001. “Does Buffer-Stock Saving Explain the Smoothness and Excess Sensitivity of Consumption?” American Economic Review 91:631–47.10.1257/aer.91.3.631Search in Google Scholar

Pagel, M. 2013. “Expectations-Based Reference-Dependent Life-Cycle Consumption.” Working Paper.10.2139/ssrn.2268254Search in Google Scholar

Park, H. 2015. “Bounded Rationality and Lifecycle Consumption.” Working paper.Search in Google Scholar

Pasquariello, P. 2014. “Prospect Theory and Market Quality.” Journal of Economic Theory 149:276–310.10.1016/j.jet.2013.09.010Search in Google Scholar

Pesendorfer, W. 2006. “Behavioral Economics Comes of Age: A Review Essay on ‘Advances in Behavioral Economics’”. Journal of Economic Literature 44:712–21.10.1257/jel.44.3.712Search in Google Scholar

Rabin, M. 2000. “Risk Aversion and Expected-Utility Theory: A Calibration Theorem.” Econometrica 68:1281–92.10.1142/9789814417358_0013Search in Google Scholar

Siegmann, A. 2002. “Optimal Saving Rules for Loss-Averse Agents Under Uncertainty.” Economics Letters 77:27–34.10.1016/S0165-1765(02)00113-1Search in Google Scholar

Sugden, R. 2003. “Reference-Dependent Subjective Expected Utility.” Journal of Economic Theory 111:172–91.10.1016/S0022-0531(03)00082-6Search in Google Scholar

Tversky, A., and D. Kahneman. 1992. “Advances in prospect theory: Cumulative representation of uncertainty.” Journal of Risk and Uncertainty 5:297–323.10.1007/BF00122574Search in Google Scholar

©2016 by De Gruyter

Articles in the same Issue

- Frontmatter

- Research Articles

- Currency Exchange in an Open-Economy Random Search Model

- Relative Concerns on Visible Consumption: A Source of Economic Distortions

- Workplace Deviance and Recession

- Strategic Delay in Global Games

- Assortative Outsourcing with Exit

- On the Impossibility of Fair Risk Allocation

- Price and Inventory Dynamics in an Oligopoly Industry: A Framework for Commodity Markets

- The Dynamics of Incentives, Productivity, and Operational Risk

- Dynamic Contests With Bankruptcy: The Despair Effect

- Welfare-Improving Effect of a Small Number of Followers in a Stackelberg Model

- The Predominant Role of Signal Precision in Experimental Beauty Contests

- Loss Aversion and Consumption Plans with Stochastic Reference Points

- Teamwork Efficiency and Company Size

- A Model of Access in the Absence of Markets

- The Core of Aggregative Cooperative Games with Externalities

- Notes

- Competition and Personality in a Restaurant Entry Game

- Editorial

- Editorial comment on “A Note on the Equivalence of the Conjectural Variations Solution and the Coefficient of Cooperation” by Escrihuela-Villar, M., The B.E. Journal of Theoretical Economics. Volume 15, Issue 2, Pages 473–480, 2015

Articles in the same Issue

- Frontmatter

- Research Articles

- Currency Exchange in an Open-Economy Random Search Model

- Relative Concerns on Visible Consumption: A Source of Economic Distortions

- Workplace Deviance and Recession

- Strategic Delay in Global Games

- Assortative Outsourcing with Exit

- On the Impossibility of Fair Risk Allocation

- Price and Inventory Dynamics in an Oligopoly Industry: A Framework for Commodity Markets

- The Dynamics of Incentives, Productivity, and Operational Risk

- Dynamic Contests With Bankruptcy: The Despair Effect

- Welfare-Improving Effect of a Small Number of Followers in a Stackelberg Model

- The Predominant Role of Signal Precision in Experimental Beauty Contests

- Loss Aversion and Consumption Plans with Stochastic Reference Points

- Teamwork Efficiency and Company Size

- A Model of Access in the Absence of Markets

- The Core of Aggregative Cooperative Games with Externalities

- Notes

- Competition and Personality in a Restaurant Entry Game

- Editorial

- Editorial comment on “A Note on the Equivalence of the Conjectural Variations Solution and the Coefficient of Cooperation” by Escrihuela-Villar, M., The B.E. Journal of Theoretical Economics. Volume 15, Issue 2, Pages 473–480, 2015