Corporate Tax Rates, Allocative Efficiency, and Aggregate Productivity

-

Marcos Dinerstein

Abstract

This paper quantifies the impact of effective corporate tax rates on aggregate total factor productivity (TFP). Using Chilean manufacturing data, we document a large dispersion in the effective tax rate faced by firms and a mass of firms facing a 0 percent tax rate. We integrate these findings into a standard monopolistic competition model, where firms are subject to corporate taxation and also face output and capital wedges, which represent all other distortions present in the economy. We find that eliminating corporate tax rates increases TFP between 4 and 11 percent. We consider counterfactual policies in which firms face a uniform flat tax rate and find a monotonically decreasing relationship between the level of the tax rate and TFP.

1 Introduction

Corporate tax regulation generates heterogeneity in the effective tax rates faced by firms due to exemptions, deductions, and deferrals. At the same time, there is a large amount of dispersion in firm-level revenue productivity even within narrowly defined industries. This suggests that effective corporate tax rates can potentially generate an inefficient allocation of resources across firms by directly impacting revenue productivity. An inefficient allocation of resources will have a direct negative effect on total factor productivity (TFP).

This paper quantifies the impact of effective corporate tax rates on aggregate TFP through allocative efficiency. First, we use Chilean manufacturing census data for the years 1998–2007 and document several characteristics of the effective tax rate distribution. Two important findings are a large dispersion in the effective tax rate faced by firms and a mass of firms with a 0 percent tax rate. Next, we incorporate these empirical findings into a standard monopolistic competition model with capital and output wedges, where firms also face corporate taxation. We then calibrate the model and find that if there were no corporate taxes in the economy, TFP would increase between 4 and 11 percent. Subsequently, we examine the allocative efficiency implications of implementing counterfactual uniform flat tax rate policies. Under these policies, firms with positive accounting profits face a flat tax rate, while those with non-positive profits incur a 0 percent tax rate. Our analysis reveals a monotonically decreasing relationship between the flat tax rate level of the counterfactual policies and TFP, stemming from the interaction of various mechanisms. While the counterfactual economies exhibit lower dispersion in effective tax rates compared to the observed economy leading to TFP gains, these gains diminish as the counterfactual flat tax rate level increases. This reduction in TFP is driven by higher flat tax rate levels exacerbating the misallocation impact of the distortions embedded within the output and capital wedges. The decline in TFP also occurs because higher flat tax rate levels generate more profit tax rate dispersion, stemming from firms with non-positive profits facing 0 percent tax rates, which further intensifies misallocation.

To carry out our analysis, we use the ENIA (Encuesta Nacional Industrial Anual), a plant-level manufacturing census from Chile that covers all establishments with more than 10 employees, for the time period 1998–2007.[1] The data set is an unbalanced panel that contains detailed balance sheet and production information. Importantly, it specifies net after-tax firm income and corporate taxes paid by firms. We use these two variables to construct the effective (average) tax rates faced by firms, which is essential for our analysis. The advantage of this effective tax rate measure is that it summarizes all the subtleties of the tax code into one measure. One drawback is that the average tax rate may be a distorted measure of firms’ marginal tax rate, resulting in endogeneity between firms’ choices and their average tax rate. We perform several exercises to address this drawback and find that our results do not change.

To study the impact of firm-specific corporate tax rates on TFP, we develop a small open economy model where firms are monopolists in the production of a differentiated product and are heterogeneous in their productivity. Firms are subject to a corporate tax policy that imposes a positive tax rate on accounting profits when these profits are positive, or a 0 percent tax rate when accounting profits are non-positive. This modeling feature incorporates a specific exemption present in the many tax codes, including the Chilean, which establishes that firms with non-positive profits face a corporate tax rate of 0 percent. This exemption is relevant for Chile, since it affects around 20 percent of firms in our sample. We also introduce firm-specific capital and output wedges to account for all other distortions. If we did not explicitly model the corporate tax rate, it would be accounted for by the capital and output wedges. By introducing it, we are stripping away its contribution to the wedges.

Using the data described above, we back out the capital and output wedges necessary to rationalize firms’ observed choices of inputs. We then take these wedges as primitives and measure the change in aggregate output between an economy in which firms face the observed effective tax rates, i.e. the observed Chilean economy, and counterfactual economies in which firms are subject to a tax rate policy with a uniform flat tax rate for firms with positive accounting profits and a 0 percent tax rate for firms with non-positive accounting profits. Last, we measure how much of this output change is generated by intrasectoral allocative efficiency, intersectoral reallocation of resources, and changes in the demand of resources. We define the contribution of intrasectoral allocative efficiency to the change in aggregate output as the TFP gap.

We find that if corporate taxes are removed, there is a positive TFP gap ranging from 4 to 11 percentage points, depending on the year analyzed. Additionally, the TFP gap between a counterfactual economy with a uniform flat tax rate policy and the observed Chilean economy consistently decreases with the level of the flat tax rate, eventually becoming negative. This trend arises from various interacting forces. While the counterfactual economies exhibit lower dispersion in effective tax rates compared to the observed economy, increasing TFP gains in the counterfactual scenarios, two offsetting mechanisms diminish these gains as the counterfactual uniform tax rate level rises. Firstly, higher levels of the flat tax rate amplify the distortions embedded in the output and capital wedges. Secondly, an increase in the uniform tax rate level raises tax rate dispersion in the counterfactual economies, stemming from the specific exemption in which firms with non-positive profits face a 0 percent tax rate. Consequently, these two forces lead to increased dispersion in marginal products and revenue productivity, progressively reducing the TFP gap as the flat tax rate level rises. This suggests that higher tax rate levels result in more resources being allocated to less productive firms. We also find that a revenue-neutral flat tax policy induces minor changes in TFP. Furthermore, the intersectoral component’s contribution to the change in aggregate output is minimal compared to the TFP gap in each year and policy scenario studied. Last, we perform several robustness checks to reinforce our results.

Our paper first contributes to the literature on misallocation of resources pioneered by Restuccia and Rogerson (2008) and Hsieh and Klenow (2009). This body of literature highlights significant dispersion in marginal products across firms, attributing it to allocative inefficiencies that hinder aggregate TFP. As outlined in Restuccia and Rogerson (2017), a large strand of work on misallocation has concentrated on identifying specific sources of misallocation and measuring their effect on aggregate TFP. For example, Buera, Kaboski, and Shin (2011), Midrigan and Xu (2014), and Gopinath et al. (2017) investigate financial frictions, yielding varied results regarding their quantitative impact on aggregate TFP.[2] Hopenhayn and Rogerson (1993), Hopenhayn (2014), and Da-Rocha, Restuccia, and Tavares (2019) examine firing costs and estimate that the aggregate TFP losses from firing costs equivalent to one year do not exceed 2 percent. Guner, Ventura, and Xu (2008) analyze size-dependent policies, such as operational restrictions on large firms or subsidies for small enterprises, finding TFP losses of 2.6 percent when the average size of establishments is reduced by 20 percent due to such policies. We contribute to this literature by examining the allocative efficiency impact of another misallocation source: corporate taxation. Our work is most closely related to Kaymak and Schott (2019), who examine how distortions in the corporate tax rate arising from loss carryforwards affect capital misallocation and aggregate TFP in the United States. Our analysis differs in that we consider distortions in the tax code stemming from any type of exemption, deduction, or deferral. By doing this, we are able to analyze the total impact of the dispersion and level of corporate tax rates on allocative efficiency.

Our contribution to the misallocation literature extends to studying the combined effect of multiple distortions on aggregate TFP. Prior studies, such as Restuccia and Rogerson (2008), Hsieh and Klenow (2009), and Whited and Zhao (2021) have focused on measuring the net effect of all the possible factors that generate misallocation without specifying a definite source. Other research has delved into analyzing the misallocation effects of more than one type of specific distortion simultaneously. For example, Calcagnini, Giombini, and Saltari (2009), Cingano et al. (2010, 2016, and Caggese, Cuñat, and Metzger (2019) investigate misallocation arising from both financial and labor market frictions. More closely related to our paper, Erosa and González (2019) and Ábrahám et al. (2023) study the impact of corporate taxes on firm performance and misallocation within frameworks characterized by financial frictions. In our paper, we explore the interaction between corporate taxation and all other potential sources of misallocation by incorporating firm-specific output and capital wedges, similar to the approach in Hsieh and Klenow (2009). These wedges are a reduced form of controlling for all frictions not explicitly modeled in our theoretical framework.[3] Thus, we are able to examine how heterogeneous effective corporate tax rates impact allocative efficiency, while potentially controlling for all other latent factors that contribute to misallocation.[4]

Finally, this paper contributes to the broad literature examining the impact of corporate tax rates on firm performance and macroeconomic aggregates. Much of this research, including studies by Poterba and Summers (1984), Auerbach (1986), Altshuler and Auerbach (1990), Cummins et al. (1994), Djankov et al. (2010), Gourio and Miao (2010), Erosa and González (2019), Kaymak and Schott (2019), Sedlácek and Sterk (2019), among others, focuses on how corporate taxes affect firms’ investment decisions. The general finding is that corporate taxation has significant adverse effects on investment. This literature has also examined the effects of corporate taxation on firm dynamics and entrepreneurship (Da Rin, Di Giacomo, and Sembenelli 2011; Djankov et al. 2010; Erosa and González 2019; Sedlácek and Sterk 2019), financing decisions (Auerbach 2002; Graham, Lemmon, and Schallheim 1998), firms’ market valuation (McGrattan and Prescott 2005), TFP (Kaymak and Schott 2019), and labor income (Auerbach 2018). One study on tax reforms in the Chilean economy is Hsieh and Parker (2007), which attributes Chile’s investment boom in the late eighties and nineties to a tax reform from 1984 to 1986 that reduced the tax rate on retained profits from 50 percent to 10 percent. Our analysis contributes to this literature by advancing the discussion on the effects of corporate tax rates on resource misallocation across firms and aggregate TFP.

The remainder of the paper is organized as follows. In Section 2, we describe the data used and document facts on the effective corporate tax rate distribution in Chile. Section 3 describes the theoretical framework used in our analysis and specifies the calibration of parameters. We perform our quantitative analysis in Section 4. In Section 5 we perform sensitivity analysis on the parameters chosen. Section 6 deals with caveats that may arise from using firm-specific effective tax rates to quantify the impact of corporate taxation on allocative efficiency. Last, we make concluding remarks in Section 7.

2 Description of the Data

This section describes the data used in our paper and presents facts about the effective corporate tax rate distribution in Chile.

2.1 The Annual Census of the Chilean Manufacturing Sector: ENIA

The data used are taken from the ENIA (Encuesta Nacional Industrial Anual), an annual census of the Chilean manufacturing sector. This data set is an unbalanced panel that covers all manufacturing plants with more than 10 employees and plants with less than 10 employees that belong to firms with multiple establishments. We use data for the period 1998–2007, as there were no reforms to the Chilean tax code in this time frame, except for pre-stipulated increases in the statutory tax rate. For the years of our sample, the statutory tax rate increased from 15 percent to 17 percent. After 2007, the ENIA’s panel structure is eliminated, so that firms cannot be identified across years. For this reason, we do not use data after 2007, as doing so would have limited some of our quantitative exercises.[5]

The ENIA collects data on revenue, net accounting profit, profit tax, employment, wage bill, fixed assets, and industry among other variables useful for our quantitative analysis. Previous versions of this census have been used in many studies, given its rich plant-level data. In Chile, the manufacturing sector accounted for roughly 17 percent of value added and 14 percent of employment for the period 1998–2007. Further details on the construction and representativeness of our sample can be found in Section A of the appendix.

2.2 Profit Tax Rate Facts in Chile

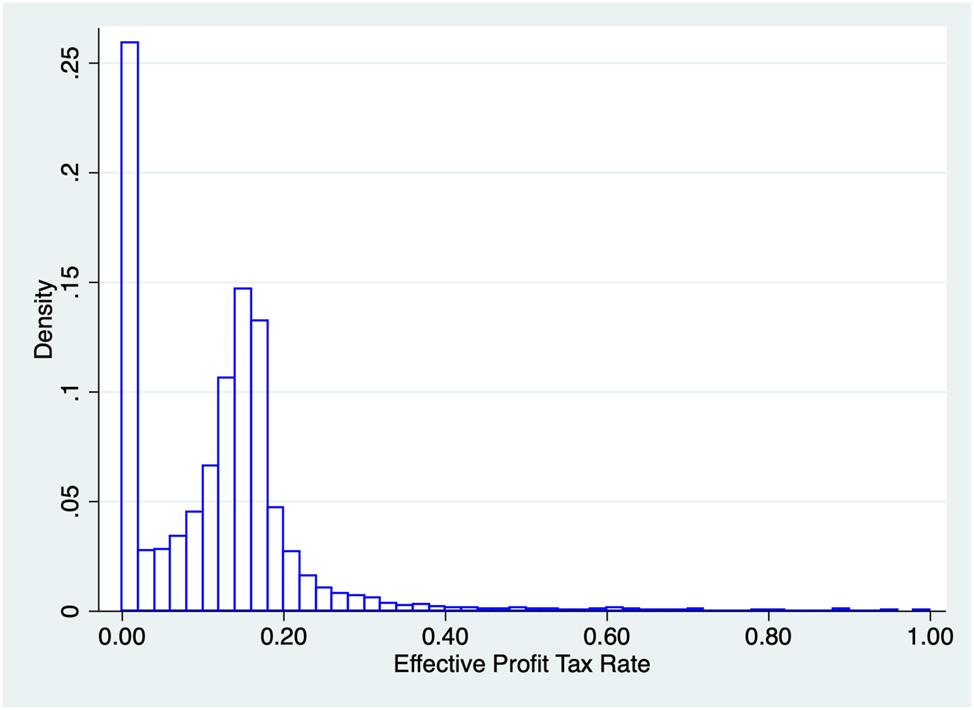

In this section, we document relevant tax facts about Chile. In Chile, all firms are subject to the same statutory tax rate, regardless of their level of profits. The ENIA collects plant-level data on net accounting profits and profit tax expenses. Using these two variables, we calculate the effective tax rate that each firm faces in a given year as the ratio between profit tax expenses and gross accounting profits.[6]

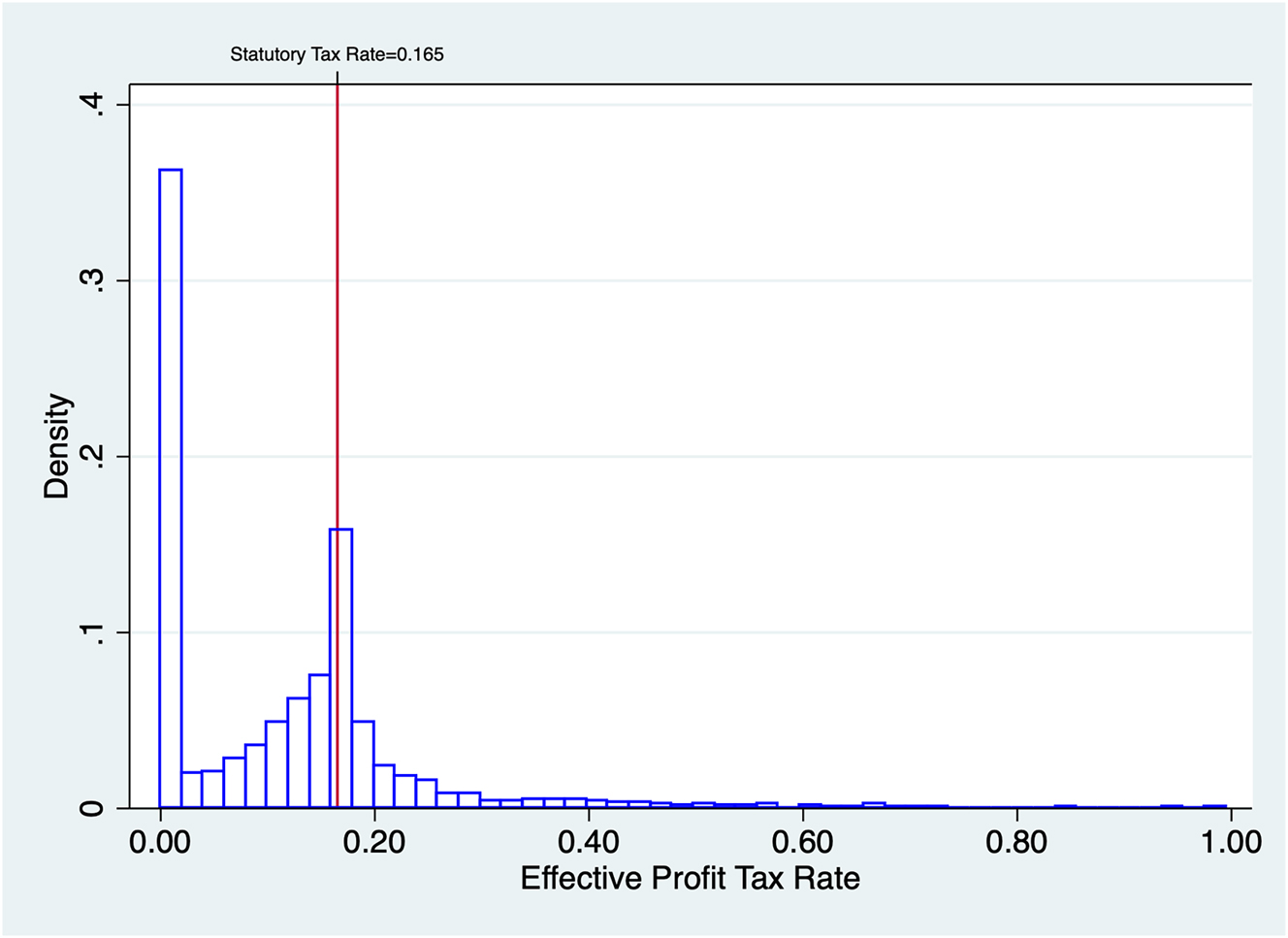

Figure 1 shows the distribution of effective profit tax rates for 2003, which we have used as an example year, as the distributions for all the years in our sample portray similar characteristics. In particular, four important features characterize the distributions of effective profit tax rates for each year in our time-window of analysis. First, a large number of firms face a 0 percent tax rate (around 30 percent for all years in our sample). This feature is mainly driven by the tax code exemption that specifies that firms with non-positive accounting profits face a corporate tax rate equal to 0 percent.[7] Second, there is a large concentration of firms with effective tax rates around the statutory tax rate, as seen in Figure 1.[8] Third, in Table 1 we document that close to 70 percent of plants have an effective tax rate below or equal to the statutory tax rate. Last, the effective profit tax rate that firms face has considerable dispersion, as depicted in Figure 1 as well as the last column of Table 1. Several exemptions outlined in the Chilean tax law, as well as fines for late payments and tax base revaluations to match economic activity with financial payments potentially generate dispersion in effective profit tax rates, as most firms have effective rates that differ from the statutory rate.

Distribution of effective profit tax rates (2003).

Characteristics of effective profit tax rates.

| Year | Statutory tax rate (percent) | Tax rate = 0 (percent of firms) | Tax rate < statutory (percent of firms) | St. dev. (percent) |

|---|---|---|---|---|

| 1998 | 15 | 29.09 | 68.06 | 13.95 |

| 1999 | 15 | 33.24 | 67.66 | 13.90 |

| 2000 | 15 | 34.52 | 71.71 | 12.87 |

| 2001 | 15 | 38.21 | 72.40 | 12.79 |

| 2002 | 16 | 38.81 | 76.20 | 12.56 |

| 2003 | 16.5 | 34.04 | 71.81 | 13.44 |

| 2004 | 17 | 29.96 | 71.82 | 12.52 |

| 2005 | 17 | 28.89 | 71.26 | 12.86 |

| 2006 | 17 | 28.19 | 68.52 | 12.38 |

| 2007 | 17 | 30.44 | 69.89 | 13.19 |

A plant may face an effective tax rate lower than the statutory tax due to several exemptions included in the tax code. For example, plants can deduct unlimited previous years’ losses from their current earnings (unlimited loss carryforward).[9] These losses are adjusted by cost of living. There are multiple expensing deductions. Plants can expense the cost of scientific investigation and technology either in the current year or up to six consecutive years after the expense has been incurred. Plants can also expense promotional and other expenses geared towards introducing new products and can prorate this expense in three consecutive years. There are also tax credits. Plants that pay the tax have a 4 percent tax credit of physical capital acquired during the fiscal year up to a maximum determined in the tax code. Other exemptions include different types of depreciation depending on the type of asset, and other expensing schemes.

Plants that face an effective tax rate that is higher than the statutory tax rate do so mainly for two reasons: late payment fines and tax base revaluations. Late payment fines range from 10 percent to 30 percent depending on how long it takes the plant to pay the amount owed. Plants also pay 1.5 percent interest per month on their debt. Taxes paid by tax base revaluations are technically called “deferred taxes”. These tax base revaluations arise from analyzing the differences, mostly temporary, between taxable and accounting profit.

The last column of Table 1 presents the standard deviation of effective corporate tax rates for every year of our sample. As mentioned previously, exemptions, deductions, and deferrals inherent to the Chilean tax code allow firms to have effective tax rates that are different than the statutory tax rate, resulting in dispersion in effective rates. To understand whether this dispersion is driven either by innate firm ability to utilize the tax code to reduce their tax burden over time (i.e. firm fixed effect), exemptions targeted at specific firm groups (i.e. region, industry, among others), or idiosyncratic variation, we carry out the following exercise. Using the unbalanced panel of firms between 1998 and 2007, we first regress effective profit tax rates on firm fixed effects and find that 41 percent of the variation in effective tax rates is explained by these fixed effects. Hence, a considerable fraction of the variation of effective profit tax rates is explained by firms’ innate ability to use exemptions in the tax code in order to modify their tax base over time.

To determine whether the remaining variation in effective tax rates is a result of exemptions targeted at firms, at a very granular level, we then regress the residual effective tax rates (residuals of the first regression) on firm size, region, business entity type, and industry, including the interactions between these variables.[10] Table 9 in the appendix reports the R 2 of this exercise across years. Our results show that most of the dispersion in the residual effective profit tax rates is idiosyncratic as exemptions that are targeted according to size, region, entity type, industry, or firm clusters defined by combinations of these variables, explain only between 3 percent and 5 percent of the variation in residual effective tax rates.

3 Theoretical Framework

This section develops the theoretical framework that will allow us to evaluate the effect of corporate profit tax rates on resource allocation and its impact on TFP. We set up a standard monopolistic competition model with firm-specific output and capital wedges and firm-specific profit tax rates. We then explain the calibration of key parameters and the measurement of the variables that will be used in our quantitative analysis.

3.1 Monopolistic Competition Model

We consider a static monopolistic competition model with heterogeneous firms. We assume a small open economy where the world interest rate r is given and all changes in aggregate capital are due to inflows into the economy. Aggregate labor supply

and P s is the price of industry s.

Industry output is a CES aggregator of M s differentiated products with elasticity parameter σ:

Differentiated product firms are monopolists over their variety and are heterogeneous in their physical productivity, A si . Their production function is given by

where K si and L si are the capital and labor inputs, respectively, and α s is the capital share of industry s.

These firms maximize economic profit, which is the sum of accounting profit and the opportunity cost of capital, while facing a corporate tax policy. We make the distinction between economic and accounting profits, since the latter constitutes firms’ net income for tax purposes.[11] The corporate tax policy is explicitly modeled as follows: if a firm’s accounting profit is positive, it faces a profit tax rate denoted by t si ≥ 0. Conversely, if a firm’s accounting profit is non-positive, its profit tax rate is 0. This modeling feature incorporates a specific exemption common to many tax systems, including the Chilean system, wherein firms with non-positive accounting profits face a 0 percent corporate tax rate.[12]

Given the corporate tax policy, a firm chooses capital, K si , labor, L si , and its differentiated good’s price, P si , to maximize economic profit:

where

where δ is the depreciation rate, λ is the fraction of capital that is financed by debt and Γ si is non-operational income net of non-operational costs.[13]

Economic profit for a firm facing profit tax rate t si , subject to positive accounting profit is:

The Lagrange multiplier for the accounting profit’s non-negativity constraint is denoted as

Economic profit for a firm facing a 0 percent profit tax rate, subject to non-positive accounting profit is:

The Lagrange multiplier for the accounting profit’s non-positivity constraint is denoted as

Section C.1 in the appendix derives the explicit solutions of firms’ optimal choices of K si , L si , and P si .

Similar to Hsieh and Klenow (2009) and Foster, Haltiwanger, and Syverson (2008), we define revenue-based factor productivity as TFPR si ≡ P si A si . Under a Cobb-Douglas production function, this can be expressed as:

From Equations (5)–(8), we observe that firms’ marginal products differ when they face different wedges and profit tax rates. The output wedge distorts firms’ output decisions, as it affects the firms’ marginal products in the same proportion. On the other hand, the capital wedge distorts decisions of capital relative to labor. Importantly, we assume that tax rates do not affect capital and output wedges. However, the tax rate interacts with the wedges in the marginal products of the firm. If we were to set wedges and taxes to zero, then all firms would have the same marginal products. Given this, Equation (9) shows that revenue productivity would also equalize across firms. On the contrary, when firms face different wedges and profit taxes, there is dispersion in revenue productivity. Furthermore, firms with higher TFPR si are those that have higher wedges, raising their marginal products and lowering their capital, labor, and output levels.

Using the above framework, we construct the aggregate measures for capital, labor, TFP, and output. First, we express the equilibrium allocations for sectoral resources, K s and L s , as:

where

where

We derive industry productivity as:

where

Last, aggregate output can be expressed as a function of K s , L s , and TFP s :

Section C.2 in the appendix describes the computation of this model’s equilibrium.

3.2 Calibration and Measurement

We follow an approach similar to Hsieh and Klenow (2009) in our calibration. That is, we set the rental rate of capital to r = 0.05 and the depreciation rate to δ = 0.05. The elasticity of substitution between varieties is fixed at σ = 3, so that firms’ price is 50 percent higher than their marginal cost. In Section 5.1, we evaluate the sensitivity of our results with respect to these assumptions. The capital share α s in industry s is equal to 1 minus the labor share in that corresponding industry for the United States.[15] These shares are obtained from the NBER Productivity Database.[16]

We use the data described in Section 2.1 to measure firms’ average tax rates, output and capital wedges, and revenue and physical productivities. Industries in the model correspond to the four-digit industries within the manufacturing sector according to the ISIC Rev. 3 industry classification.[17] We measure firms’ value added, P si Y si , as the difference between gross revenue and intermediate inputs. We use four-digit industry deflators for gross revenue and intermediate inputs, provided by the data set, to deflate our estimate of firms’ value added. Industry value added, P s Y s , is measured as the sum of all firms’ value added within industry s. The capital input, K si , is measured as the book value of fixed assets, which we deflate using the gross revenue deflators. To control for differences in human capital, hour requirements, and rent sharing across plants, we follow Hsieh and Klenow (2009) and use the wage bill deflated by the intermediate input industry deflator as the measure for labor, L si . In a robustness check, we also consider hours worked for our measure of labor.[18]

As described above, we calculate effective tax rates as the ratio between a firm’s profit taxes and its gross accounting profits. We denote the measured firm-specific average tax rate as

Using the data and parameter values described above, we back out the capital and output wedges in the following manner. For firms with positive accounting profits, we use Equations (5) and (6) to obtain the firm-specific wedges. Since

On the other hand, for firms with negative accounting profits the capital and output wedges are obtained from Equations (7) and (8). In this case,

Last, we use Equations (3) and (9) to calculate firms’ physical productivity, A si , and revenue productivity, TFPR si , respectively.[20] Using Equations (10)–(15), we construct industry and aggregate measures of output, productivity, capital, and labor.

4 Misallocation and Corporate Taxes

In this section, we utilize the framework developed above to examine the impact of corporate tax rates on allocative efficiency. First, we characterize and provide a decomposition of the output gap. We define this gap as the change in output between two economies characterized by different wedges and corporate tax policies, while holding the distribution of firm productivities constant. The output gap decomposition allows us to determine the extent to which changes in intrasectoral allocative efficiency contribute to this gap. Next, we consider counterfactual corporate tax policies and measure the implied output gap relative to the observed distribution of tax rates, which we refer to as the observed Chilean economy. By employing the decomposition, we quantify the intrasectoral reallocation of resources resulting from these counterfactual policies in comparison to the observed effective tax rates. Finally, we investigate the implications for government revenue across our various counterfactual scenarios.

4.1 Output Gap Decomposition

To study the impact of different tax policies, it is convenient to define the output gap between two economies that only differ in the wedges and effective tax rates each firm faces. We decompose this gap into five objects: the TFP gap, intersectoral capital reallocation, intersectoral labor reallocation, change in aggregate capital, and change in aggregate labor. The TFP gap reflects changes in intrasectoral allocative efficiency (i.e. intrasectoral reallocation of resources), as can be seen from Equations (9) and (14). Capital and labor intersectoral reallocation are also affected by tax rates and wedges since the industry shares of capital and labor, ω K and ω L , are a function of firms’ marginal products. Aggregate capital demand changes for different tax rates and wedges through the marginal cost of capital. Last, in equilibrium aggregate labor demand equates aggregate labor supply, and given that aggregate labor supply is fixed, the change in aggregate labor is always zero between any two economies that differ in firm wedges and firm effective tax rates.

Consider two economies that have different firm-specific output and capital wedges and profit tax rates but are equal in all other aspects. Denote the levels of output of these two economies by Y and

Below, we analyze the output and TFP gaps between different counterfactual tax rates policies and the observed Chilean economy.

4.2 Output and TFP Gains from Eliminating Corporate Taxation

In this section, we quantify the output gap decomposition using Equation (20). We consider two economies that differ only in the corporate tax policy implemented. Both economies are subject to the same firm-specific output and capital wedges. By doing this, we ensure that firms face the same frictions implied by the data in both economies. In one economy, we set taxes to t

si

= 0, regardless of firms’ level of accounting profits, and, in the other economy, we set taxes to the observed firm-specific average tax rates,

Table 2 presents the results from the output gap decomposition. Moving to a counterfactual scenario with no corporate tax rates generates an increase in output that ranges from 20 percent to 38 percent, depending on the year considered. In all of the years analyzed, TFP increases due to the policy change. This increase ranges from 4 percent to 11 percent and is due to a more efficient intrasectoral allocation of resources. The effect on intersectoral reallocation is small. Intersectoral allocation of capital accounts for between −3 percent and 2 percent of the change in output. In three years, the effect of intersectoral allocation of capital is negative. Intersectoral allocation of labor increases in all years but only between 0 percent and 2 percent. Most of the change in the output gap is generated by large increases in the demand for aggregate capital. This is an implication of the small open economy assumption of the model. Setting t si = 0 directly changes the cost of capital, which in this case generates large inflows of capital into the economy. Last, since aggregate labor supply is inelastic, the change in aggregate labor is always zero for any counterfactual policy scenario. Hence, we do not report this change in Table 2.

Output gap decomposition: t si = 0 (percent).

| Year | Output gap | TFP gap | Intersectoral K | Intersectoral L | ΔAggregate capital |

|---|---|---|---|---|---|

| 1998 | 20.00 | 5.47 | 1.32 | 1.38 | 11.82 |

| 1999 | 21.20 | 6.43 | 0.41 | 1.05 | 13.31 |

| 2000 | 28.46 | 8.22 | 1.60 | 0.95 | 17.69 |

| 2001 | 22.79 | 5.64 | 0.10 | 0.72 | 16.33 |

| 2002 | 19.60 | 4.52 | 0.61 | 0.34 | 14.14 |

| 2003 | 19.85 | 4.82 | 0.03 | 0.55 | 14.45 |

| 2004 | 22.30 | 4.16 | −0.41 | 0.80 | 17.75 |

| 2005 | 31.20 | 4.33 | −2.94 | 1.74 | 28.07 |

| 2006 | 35.29 | 6.83 | 0.06 | 1.53 | 26.86 |

| 2007 | 38.02 | 11.12 | −0.55 | 1.31 | 26.14 |

-

Notes: Since aggregate labor supply is inelastic, ΔAggregate Labor = 0 for any counterfactual policy scenario.

4.3 Allocative Efficiency Gains and Corporate Tax Rates

In this section, we analyze the allocative efficiency impact of different levels of profit tax rates by examining a series of counterfactual flat tax rate policies. Our approach involves implementing counterfactual exercises where firms operate under corporate tax policies that apply a uniform flat tax rate,

Equations (5)–(8) portray the mechanisms through which intrasectoral reallocation of resources occurs due to these counterfactual tax policies. Profit tax rates affect the dispersion of firms’ marginal products in two ways. Firstly, dispersion in profit tax rates directly leads to heterogeneous marginal products. Secondly, the level of profit tax rates indirectly impacts the dispersion of marginal products through its interaction with firm-level wedges. Higher variance in marginal revenue products results in higher dispersion in revenue productivity, thereby depressing TFP. In the counterfactual economies, the only source of dispersion in corporate tax rates stems from the exemption considered within the theoretical model, wherein firms with non-positive accounting profits are subjected to a 0 percent tax rate. In contrast, the dispersion in corporate tax rates for the observed Chilean economy reflects all the exemptions and deductions of the tax system. Consequently, the counterfactual scenarios are anticipated to exhibit less dispersion in profit tax rates compared to the observed Chilean economy, as the latter accounts for all exemptions under the Chilean tax system. However, this does not imply that across all counterfactual scenarios, dispersion in marginal products and revenue productivity would be lower, due to the interaction between the counterfactual tax rate levels and the existing firm-level wedges. Hence, these counterfactual flat profit tax rate policies have the potential to either enhance or diminish intrasectoral allocative efficiency.

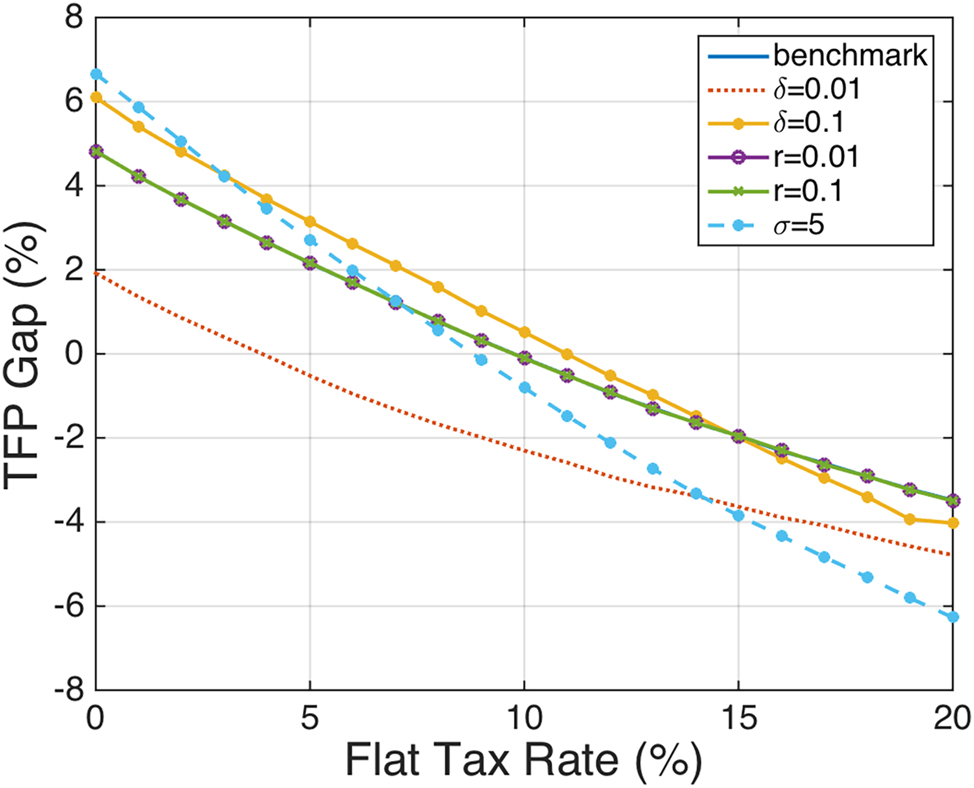

The schedule in Figure 2 portrays the TFP gap between a counterfactual corporate tax policy with

Relationship between TFP gap and

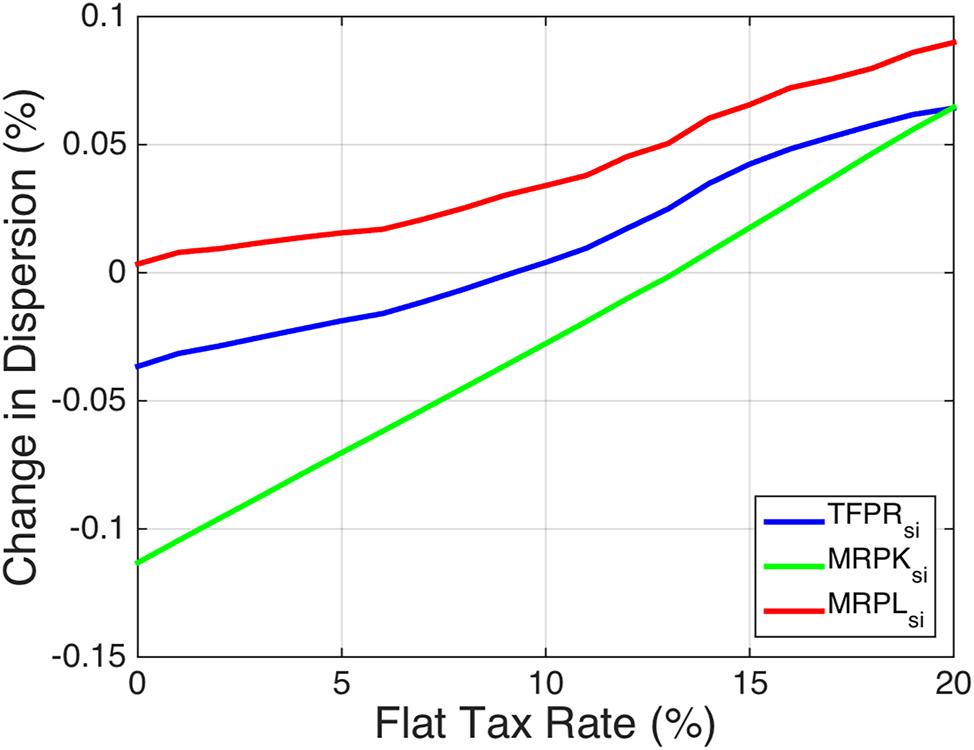

The monotonically decreasing relationship between the level of the uniform tax rate policy and the TFP gap can be rationalized as follows. As expected, the profit tax rate dispersion in the observed Chilean economy exceeds that of all the counterfactual economies studied. In 2003, the dispersion of profit tax rates in the observed Chilean economy was 13.44 percent, while in the counterfactual economies, it ranged from 0 percent

Change in dispersion measures relative to

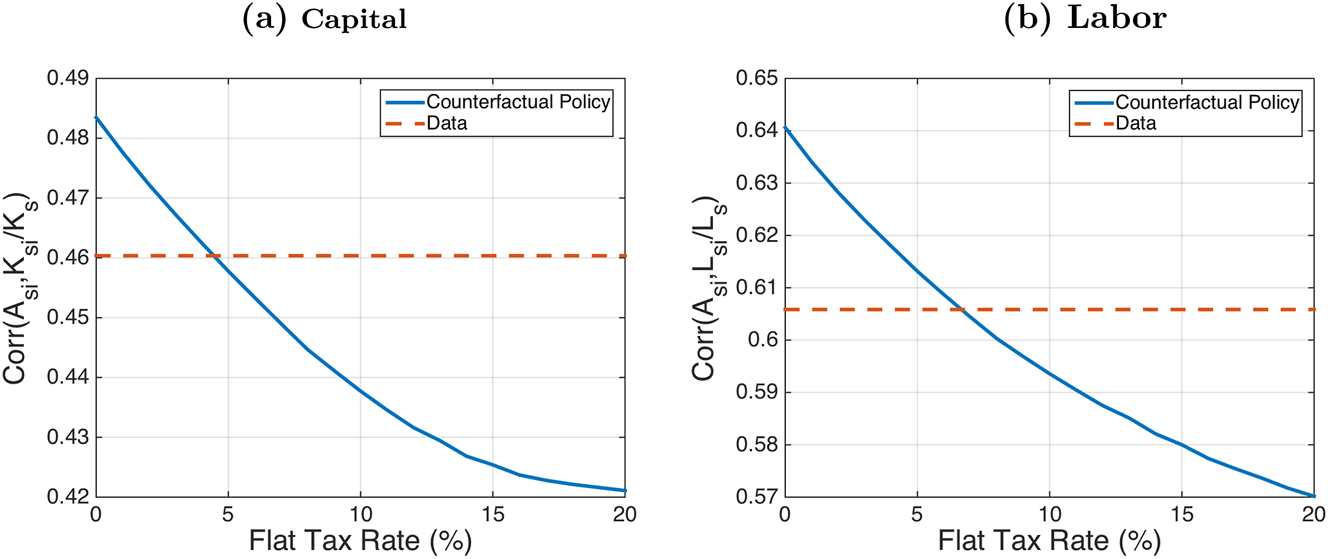

To corroborate our results, we perform an alternative measure of allocative efficiency similar to Olley and Pakes (1996). Our results are summarized in Figure 4. In Panel (a), the schedule labeled “Counterfactual Policy” plots the correlation between firm productivity, A

si

, and the share of firm i’s capital stock, K

si

, in sector s’s capital stock, K

s

, for different flat tax rate levels

Correlation between firm productivity and activity share (2003). Notes: The solid blue line labeled “counterfactual policy” corresponds to the correlation between firm productivity and firm activity share for different levels of

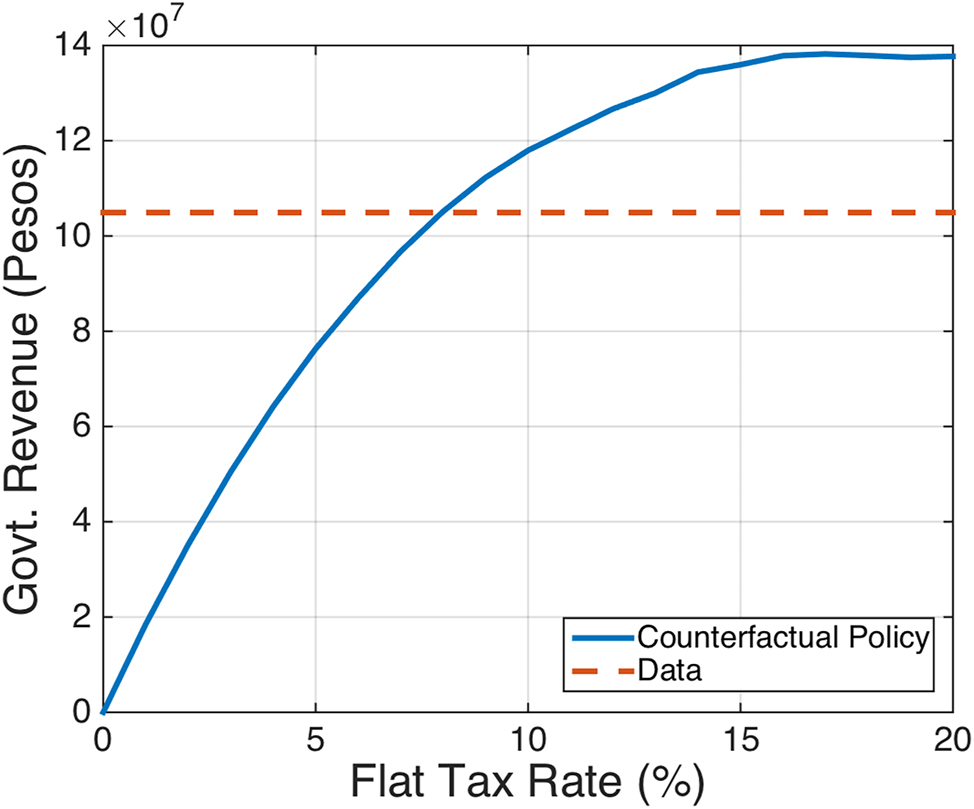

Next, we analyze the effect of these tax policies on government revenue. In Figure 5, the blue schedule labeled “Counterfactual Policy” portrays the Laffer curve for different flat tax rate policies. A clear trade-off stands out. Although very low flat tax rates yield higher levels of TFP, government revenue from corporate taxation is smaller. The dotted line labeled “Data” is the government revenue collected from the observed corporate tax rates. The flat tax rate policy that yields the same revenue is

Relationship between government revenue and

5 Sensitivity Analysis

In this section, we analyze the sensitivity of the results in Section 4 to our choice of parameter values and our measure of labor input.

5.1 Sensitivity to Parameter Values

Table 3 shows the TFP gap from eliminating corporate taxes for different interest rates r, depreciation rates δ, and values of σ, the parameter of the elasticity of substitution across varieties. For different interest rates, results are identical to the benchmark. As seen in Equation (4), when λ = 0, the interest rate r does not affect the accounting profits of firms. Hence, it does not interact with the corporate tax rate in the marginal revenue products, as shown in Equations (5)–(8). For this reason, different interest rates do not affect the TFP gap when corporate tax rates are eliminated. This is not the case anymore when we consider different values of λ.

TFP gap for different parameter values: t si = 0 (percent).

| Year | Benchmark | r = 0.01 | r = 0.1 | δ = 0.01 | δ = 0.1 | σ = 5 |

|---|---|---|---|---|---|---|

| 1998 | 5.47 | 5.47 | 5.47 | 4.26 | 5.92 | 11.04 |

| 1999 | 6.43 | 6.43 | 6.43 | 0.93 | 7.90 | 11.43 |

| 2000 | 8.22 | 8.22 | 8.22 | 5.37 | 9.48 | 15.74 |

| 2001 | 5.64 | 5.64 | 5.64 | 0.86 | 7.49 | 9.98 |

| 2002 | 4.52 | 4.52 | 4.52 | 1.46 | 5.62 | 8.00 |

| 2003 | 4.82 | 4.82 | 4.82 | 1.92 | 6.10 | 6.66 |

| 2004 | 4.16 | 4.16 | 4.16 | 0.92 | 6.15 | 7.42 |

| 2005 | 4.33 | 4.33 | 4.33 | −4.08 | 7.48 | 6.52 |

| 2006 | 6.83 | 6.83 | 6.83 | 2.32 | 8.52 | 10.08 |

| 2007 | 11.12 | 11.12 | 11.12 | 7.75 | 12.56 | 16.73 |

On the other hand, the depreciation rate has a direct impact on accounting profits, regardless of the value of λ. Moreover, as the depreciation rate increases, the TFP gains from eliminating corporate taxes are higher. Finally, we have chosen a conservative σ at the low end of the empirical estimates. Under σ = 5, the TFP gains are higher from eliminating corporate taxation.

As in Section 4.3, we carry out the same flat tax rate policy counterfactuals. Our results are robust when we consider different parameter values for r, δ, and σ. Figure 6 shows the same decreasing relationship between the TFP gap and the level of the flat tax rate,

Relationship between TFP gap and

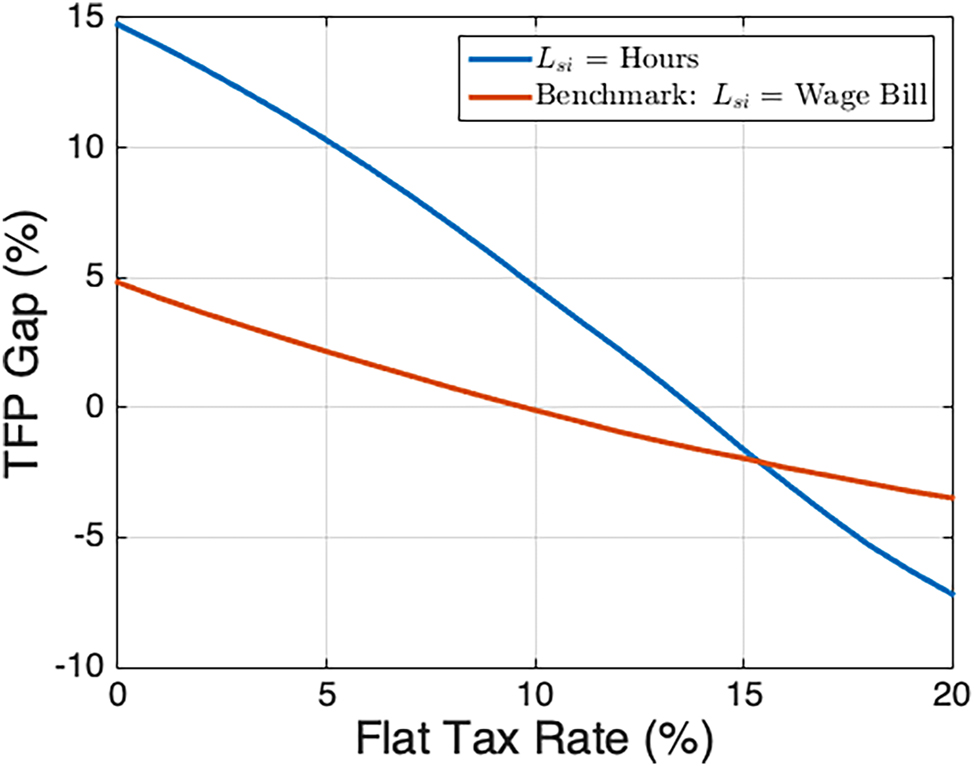

5.2 Hours Worked as Input for Labor

In the results described above, we measure L si as the firm’s wage bill. As a robustness check, we recalculate our estimates using hours worked as labor input.[22] Similar to Hsieh and Klenow (2009), using the wage bill for the labor input allows us to control for between-firm heterogeneity in rent sharing, skill level, and hours worked requirements. As these differences are not modeled in our framework, when we use hours as labor input, they are loaded into the output and capital wedges. As a result, dispersion in TFPR si is higher.

Repeating our exercise with hours as labor input yields two main findings. First, in line with the results in Section 4.3, the TFP gap falls when we increase the level of the flat corporate tax rate in the counterfactual economies, as seen in Figure 7. Second, the TFP gap across different counterfactual policies is larger. This is because our results are amplified since the corporate tax rate interacts with output and capital wedges, which are more dispersed for the reasons mentioned at the beginning of this section. This result holds across all years of our sample, as seen in the output gap decomposition in Table 10 in the appendix.

Relationship between TFP gap and

6 Robustness Checks on the Measurement of Effective Tax Rates

Given that we use average tax rates in our analysis, there is concern about the endogeneity of firms’ characteristics and choices with our measure of the observed profit tax rate. To address this concern, we conduct several robustness checks. First, we analyze what would happen if all capital was financed with debt, which would change the financing structure of the firm and lower accounting profits, since interest can be subtracted. Second, to address potential mismeasurement issues arising from using the average tax rate as a proxy for the marginal tax rate, we calculate TFP gains from eliminating corporate taxes under the assumption that the effective marginal tax rate Chilean firms face is equal to the statutory tax rate. Third, we address the issue of loss carryforward by firms, which could explain our results since we are considering a static model. Last, we repeat our analysis with the permanent sample of firms. By doing this, we discard the possibility that special tax incentives of young or old firms may be driving our results. As shown below, we find that our results do not vary when taking these issues into account.

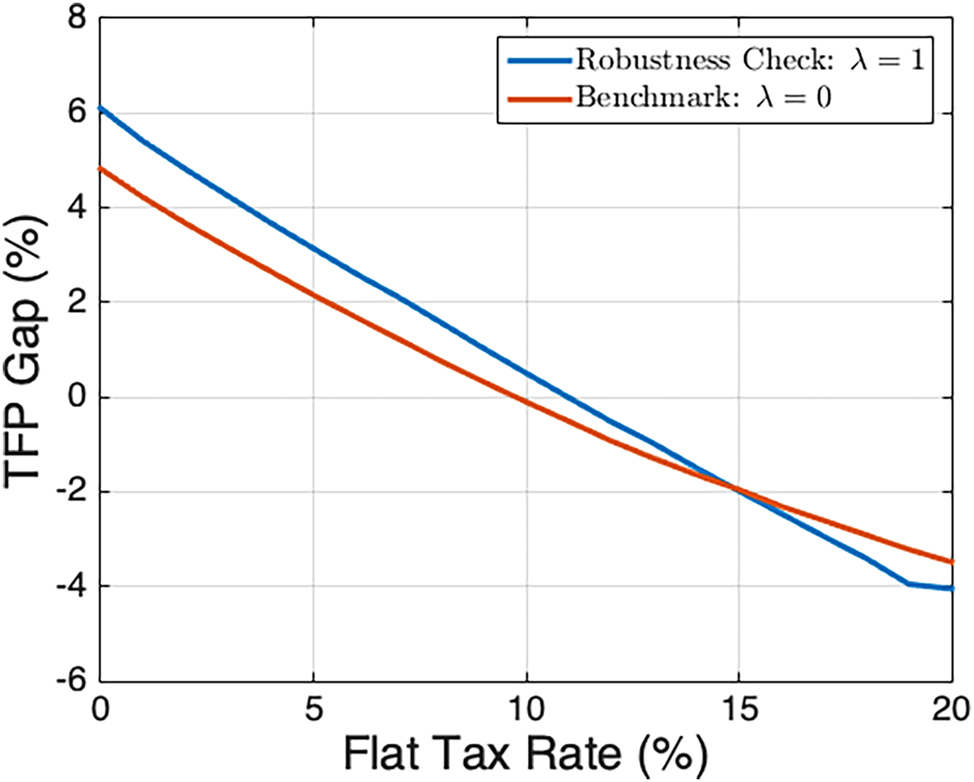

6.1 Financing Capital with Debt

So far, we have assumed that capital is financed entirely with equity, λ = 0. This is a strong assumption since firms may finance capital with a mix of capital and debt. Firms have incentives to finance capital with debt since interest payments are discounted from accounting profits and therefore lower the tax that firms must pay. In this section, we analyze the other extreme case in which all capital is financed with debt λ = 1 to determine whether our results are sensitive to this assumption. Note that our calculation of the effective tax rate that firms face is not affected by the capital structure decision of the firm since we observe profits net of interest and taxes. Hence, the tax rate we calculate already takes into account the firm’s capital structure. However, our results will vary depending on the amount of capital a firm finances with debt, since λ interacts with the effective tax rate t si in the marginal revenue product of capital.

Note that if we observed profits before subtracting interest and taxes instead of using profits net of interest and taxes, differences in access to credit and other distortions that may affect the capital structure would also be loaded into the effective tax rate instead of the capital and output wedges. Also, it is important to note that the fraction of capital financed with debt can potentially be firm specific. For example, some firms may have better access to credit than others. Uras (2014) explores this mechanism and finds that it has important implications for capital misallocation. In our setup, these differences in access to credit are reflected in the capital and output wedges.

Table 4 shows the output gap decomposition under λ = 1 and under the scenario in which corporate tax rates are equal to t si = 0. Results are very similar to those of Table 2. The increase in output from eliminating the effect of dispersion and level of corporate taxes is mainly explained by an increase in aggregate capital demand and an increase in TFP. Hence, we can see that intrasectoral reallocation of resources plays a significant role in explaining the output gap, while intersectoral reallocation of resources has a negligible effect on the output gap. This finding is consistent with the results found in Section 4.2.

Output gap decomposition: λ = 1, t si = 0 (percent).

| Year | Output gap | TFP gap | Intersectoral K | Intersectoral L | ΔAggregate capital |

|---|---|---|---|---|---|

| 1998 | 16.58 | 5.92 | 1.72 | 1.34 | 7.60 |

| 1999 | 17.51 | 7.90 | 1.31 | 1.00 | 7.30 |

| 2000 | 24.10 | 9.48 | 1.91 | 0.97 | 11.74 |

| 2001 | 18.75 | 7.49 | 0.85 | 0.71 | 9.70 |

| 2002 | 15.90 | 5.62 | 1.43 | 0.34 | 8.51 |

| 2003 | 16.79 | 6.10 | 1.13 | 0.52 | 9.03 |

| 2004 | 19.09 | 6.15 | 0.78 | 0.79 | 11.38 |

| 2005 | 26.57 | 7.48 | 0.16 | 1.68 | 17.26 |

| 2006 | 31.18 | 8.52 | 0.64 | 1.52 | 20.50 |

| 2007 | 34.54 | 12.56 | 0.58 | 1.29 | 20.11 |

-

Notes: Since aggregate labor supply is inelastic, ΔAggregate Labor = 0 for any counterfactual policy scenario.

As in Section 4.3, we carry out different counterfactual flat tax rate policies and evaluate their relationship to the TFP gap. In Figure 8 we can observe that results are similar under the scenario in which all capital is financed by debt, λ = 1, and under the benchmark scenario in which capital is financed by equity, λ = 0. That is, as the flat tax rate level increases, the TFP gap falls. Also under the assumption that λ = 1, the dispersion of marginal products and revenue productivity increases as the flat tax rate levels increase. Higher flat tax rates exacerbate the effect of the output and capital wedges and also create higher tax rate dispersion in comparison to lower flat tax rates. As in Section 4.3, these two mechanisms increase revenue productivity dispersion as the flat tax rate rises, which indicates that resources are reallocating from more productive firms to less productive firms.

Relationship between TFP gap and

6.2 Statutory Tax Rate as the Marginal Tax Rate

The literature, including papers by Graham (1996), Plesko (2003), Graham and Mills (2008), among others, has highlighted concerns regarding the accuracy of average tax rates as estimates of firms’ marginal tax rates, proposing various alternative proxies. To address this issue, this section examines one such alternative: the statutory tax rate. Similar to Graham (1996) and Djankov et al. (2010), we use the statutory tax rate as a marginal tax rate proxy. For this, we recalibrate the benchmark economy under the following corporate tax policy: firms with positive profits face the statutory tax rate, while those with non-positive profits face a 0 percent tax rate. Subsequently, we contrast this alternative benchmark economy with a counterfactual scenario in which corporate taxation is entirely eliminated.

Table 5 presents the output gap resulting from eliminating the effects of both the dispersion and level of corporate taxes, relative to the alternative benchmark. The findings closely mirror those of Table 2. The rise in output attributed to the removal of corporate taxation primarily stems from an increase in aggregate capital demand, followed by improved intrasectoral allocative efficiency (TFP Gap), while the impact of intersectoral reallocation of resources on the output gap remains minimal. In this robustness exercise, intrasectoral efficiency gains range from 7 to 12 percent across all years in our sample, aligning closely with the estimates of the benchmark calibration, which range from 4 to 11 percent across all years in the sample. It is important to note that in this robustness exercise, the estimated output and capital wedges that rationalize observed firms’ input choices, differ from the wedges derived in the benchmark calibration due to the different marginal tax rate proxy. As a result, the dispersion in corporate tax rates resulting from all the tax code’s exemptions not considered in our theoretical framework is now attributed to other distortions in the economy rather than solely to the Chilean Tax Code.[23]

Output gap decomposition: statutory tax rate as marginal tax rate (percent).

| Year | Output gap | TFP gap | Intersectoral K | Intersectoral L | ΔAggregate capital |

|---|---|---|---|---|---|

| 1998 | 29.02 | 9.74 | 1.15 | 1.76 | 16.37 |

| 1999 | 25.37 | 9.37 | 0.93 | 1.13 | 13.94 |

| 2000 | 32.03 | 11.28 | 1.58 | 1.03 | 18.14 |

| 2001 | 24.47 | 7.19 | 0.44 | 0.79 | 16.05 |

| 2002 | 26.72 | 7.85 | 0.75 | 0.49 | 17.63 |

| 2003 | 26.57 | 8.28 | 0.43 | 0.84 | 17.02 |

| 2004 | 29.62 | 9.07 | −0.98 | 0.91 | 20.62 |

| 2005 | 35.38 | 10.20 | −0.16 | 1.55 | 23.79 |

| 2006 | 39.15 | 9.03 | −0.23 | 1.78 | 28.57 |

| 2007 | 39.04 | 11.93 | 0.00 | 1.40 | 25.71 |

-

Notes: Since aggregate labor supply is inelastic, ΔAggregate Labor = 0 for any counterfactual policy scenario.

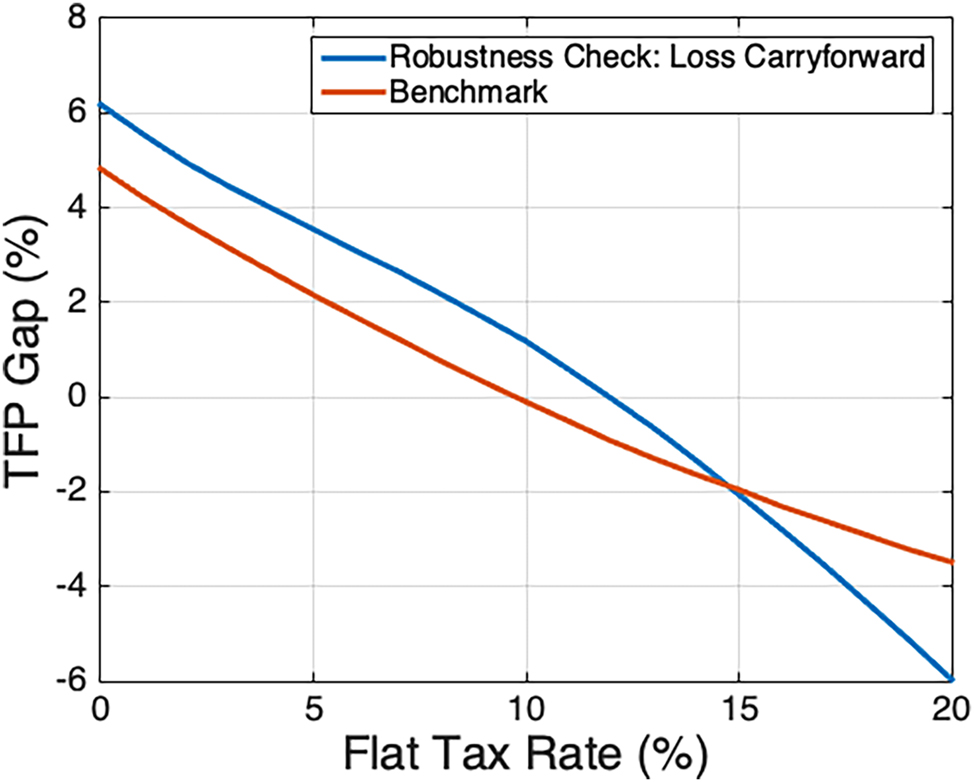

6.3 Accounting for Loss Carryforward

One of the exemptions that may generate dispersion in effective corporate tax rates is the fact that plants can carry forward losses from one period to the next to reduce their tax base. Our results in Section 2.2 show that firm fixed effects account for a considerable fraction of the variation of effective corporate tax rates. Firm fixed effects capture plants’ ability to utilize the tax code to the modify their tax base, through exemptions like loss carryforward. In particular, firms optimally choose capital and labor taking into account that this exemption allows them to reduce their tax burden. However, we do not model this explicitly since our analysis is static, and thus this specific source of distortion is loaded into the wedges. To measure how sensitive our results are to this omission, we consider the following exercise. We take the average across years for each plant’s relevant variables and estimate the TFP gap for our policy counterfactuals. By doing this, any losses that could have been carried forward will smooth out. Note that if all the dispersion in effective tax rates was due to this channel, the tax rates that firms face in this exercise should be less dispersed and similar to the statutory rate. This is not the case, however, as the effective tax rate calculated by averaging profit and profit tax across years is distributed similarly to the effective tax rates calculated year by year. We can see this by comparing Figures 1 and 9.

Distribution of effective profit tax rates – loss carryforward (2003).

Our results for this exercise are similar to our benchmark results. The decomposition of the output gap when firms face t si = 0 can be seen in Table 11 in the appendix. When firms do not face corporate tax rates, TFP increases by 6.18 percent, which is within the range of values of our benchmark analysis, as seen in Table 2. Hence, loss carryforward is not the main driver of the distortions generated by heterogeneous tax rates. Similar to Section 4.2, intersectoral reallocation of resources accounts for a very small portion of the output gap, while changes in aggregate capital demand play a more significant role.

As in the benchmark, we also carry out flat tax rate counterfactual policies and measure their effect on aggregate TFP. We find that the negative relationship between the TFP gap and the flat tax rate level still persists, as seen in Figure 10. Hence, despite eliminating the dispersion in corporate tax rates coming from loss carryforward, as the flat tax rate increases, resources are reallocated from more efficient firms to less efficient firms.

Relationship between TFP gap and

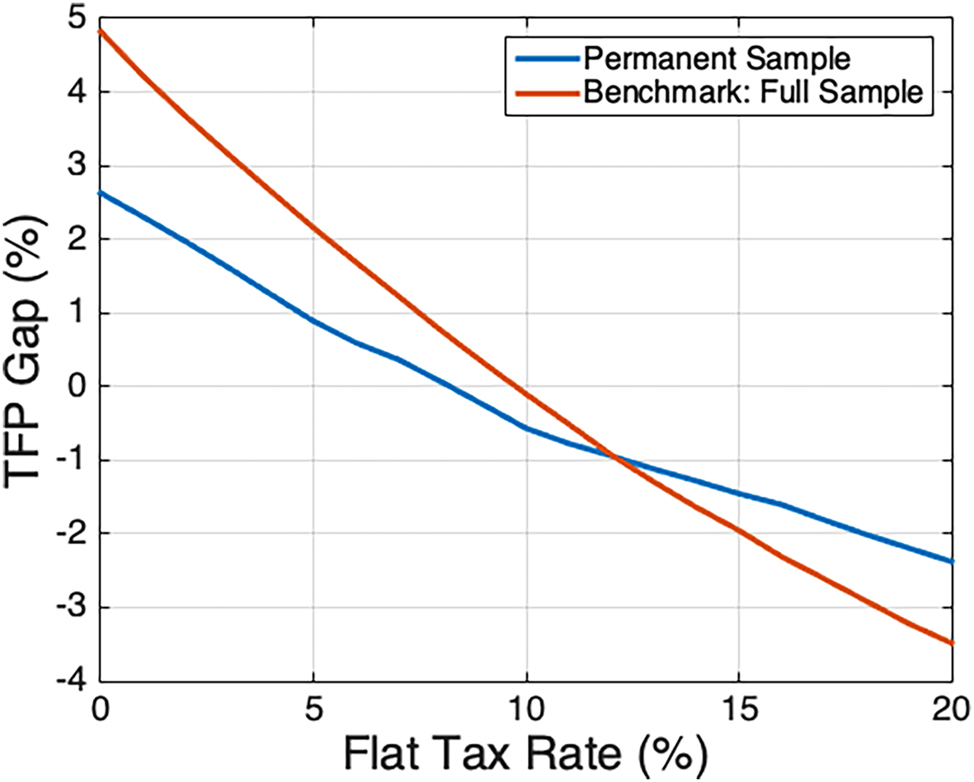

6.4 Permanent Sample

Dispersion in corporate tax rates can potentially be driven by tax exemptions given to young entrant firms, which are usually directed at fostering industry competition. If this is the only source of tax rate dispersion and entrant firms are relatively less productive than incumbent firms, then these tax exemptions would be responsible for the positive TFP gap shown in Table 2. Intuitively, these tax exemptions would be allocating more resources to less productive entrant firms and fewer resources to more productive incumbent ones. Hence, if Chile moved to a tax policy with no corporate taxes, then resources would reallocate to the more productive incumbent firms, generating the positive TFP gap.

To control for this mechanism, we focus on the firms that were always in operation for the period 1998 to 2007 and then perform the output gap decomposition for the years 2003–2007. By doing this, we make sure that the firms had been in operation at least five years.[24] If the only source of tax rate dispersion was exemptions to less productive entrant firms, then when we eliminate them from the sample, the TFP gap would be 0. This is not the case, however, as can be seen in Table 6, which implies that there are other sources of corporate tax rate dispersion that generate a positive TFP gap. In this exercise, we also control for the fact that less productive exiting firms are driving our results, since the permanent sample comprises highly productive firms that have been operating for at least 10 years.

Output gap decomposition: permanent sample, t si = 0 (percent).

| Year | Output gap | TFP gap | Intersectoral K | Intersectoral L | ΔAggregate capital |

|---|---|---|---|---|---|

| 2003 | 19.23 | 2.63 | −0.08 | 0.75 | 15.98 |

| 2004 | 22.40 | 4.32 | 0.16 | 1.29 | 16.99 |

| 2005 | 22.96 | 3.54 | −0.09 | 1.36 | 18.13 |

| 2006 | 27.75 | 4.74 | −0.91 | 2.18 | 21.72 |

| 2007 | 26.36 | 5.36 | −0.20 | 1.68 | 19.51 |

-

Notes: Since aggregate labor supply is inelastic, ΔAggregate Labor = 0 for any counterfactual policy scenario.

As shown in Table 12 in the appendix, there is significant dispersion in the effective corporate tax rates faced by the firms in the permanent sample for all years. Hence, tax exemptions given to young firms are not the main driver of this dispersion.

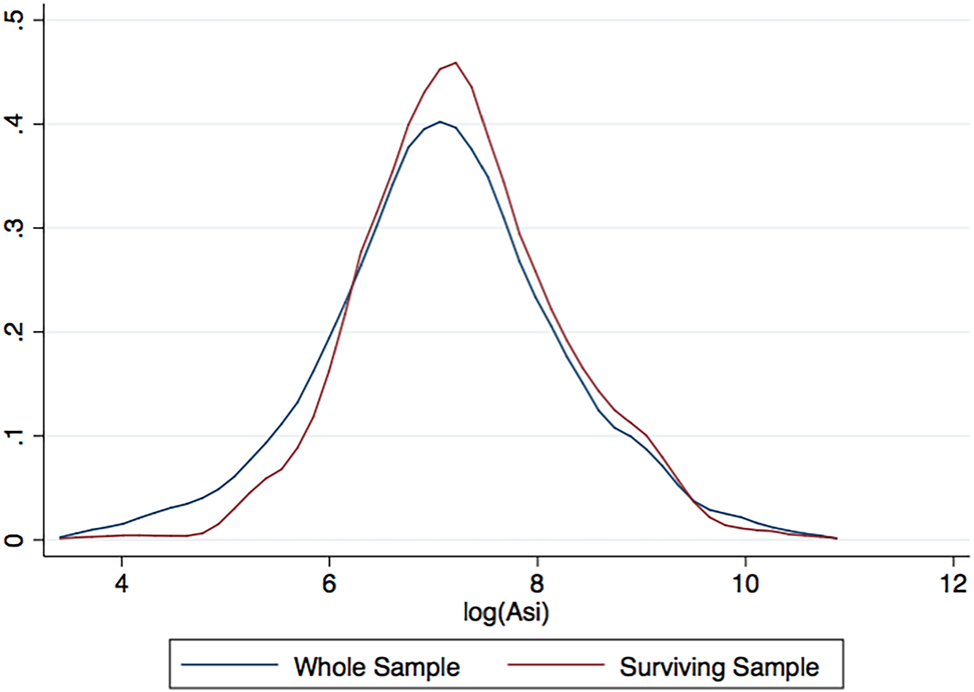

By comparing Tables 6 with 2, we can see that the results for intersectoral reallocation of resources and changes in input demands are similar. Also, we can observe that the TFP gap from eliminating corporate taxes is smaller in the permanent sample in comparison to the whole sample. The main reason for this finding is that the permanent sample controls for firm entry and exit. Firms in this sample had been in operation for at least 10 years in 2007. Hence, they were relatively more productive than the firms that entered or exited the sample during the time period we analyze. We document this finding in Figure 11, in which we compare the distribution of

Distribution of

We find that the mean of

7 Conclusions

The objective of this paper is to quantify the effects of corporate tax rates on aggregate TFP through allocative efficiency. To do this, we set up a standard monopolistic competition model that includes firm-specific corporate tax rates as well as output and capital wedges. In our framework, corporate tax policy is modeled as a positive corporate tax rate, if a firm has positive accounting profit, or as 0 percent tax rate, if a firm has non-positive accounting profit. We calibrate the model and find that if Chile had eliminated corporate tax rates, TFP would have increased between 4 percent and 11 percent for the period 1998–2007. We also analyze how different levels of flat corporate tax rates affect TFP in an economy characterized by other distortions. We show that there is a monotonically decreasing relationship between the TFP gap and the level of the flat tax rate. We carry out a sensitivity analysis on parameters and robustness checks on our measure of effective tax rates and find that our results do not vary.

A The Annual Census of the Chilean Manufacturing Sector

We use the manufacturing sector census data from Chile to construct our sample in the following manner. First, we drop all observations with negative values for output, capital, wage bill, and tax rates. These observations are very small in number and their negative values are due to reporting error. Our model explains that aggregate TFP is affected by the dispersion of marginal revenue products. For this reason, we trim the 1 percent tails of the observations by the marginal revenue product of capital, MRPK si , and the marginal revenue product of labor, MRPL si . Then we eliminate the 0.5 percent tails of the observations by physical productivity, A si . Last, when we consider counterfactual flat tax rate policies, there are cases in which some plants have marginal revenue products with negative values, a result that is mathematically possible but theoretically inconsistent. As a result, we eliminate observations with negative marginal revenue products for a counterfactual flat tax rate of 20 percent, which is the highest flat tax level we analyze. If a firm has positive marginal revenue products for this tax rate, then it also does for a lower flat tax rate. On average, the number of firms that are eliminated because of this criterion are only 1.7 percent of the total sample.

The total number of plants in our sample each year ranges between 3,919 and 4,726, as can be seen in Table 7. Between 1998 and 2007, plants with 10–49 workers accounted for 60 percent of the total number of establishments, on average. Plants with 0–9 workers, 50 to 199 workers, and 200+ workers had an average participation share in the total number of firms of 9 percent, 23 percent, and 8 percent, respectively.

Number of plants and shares in total plants by size class.

| Year | Number of plants | 0–9 employees | 10–49 employees | 50–199 employees | 200+ employees |

|---|---|---|---|---|---|

| 1998 | 4,530 | 0.02 | 0.65 | 0.25 | 0.08 |

| 1999 | 4,052 | 0.06 | 0.64 | 0.23 | 0.07 |

| 2000 | 3,998 | 0.07 | 0.64 | 0.22 | 0.07 |

| 2001 | 4,214 | 0.11 | 0.60 | 0.21 | 0.08 |

| 2002 | 4,576 | 0.11 | 0.61 | 0.21 | 0.07 |

| 2003 | 4,509 | 0.10 | 0.60 | 0.22 | 0.08 |

| 2004 | 4,726 | 0.09 | 0.61 | 0.22 | 0.08 |

| 2005 | 4,461 | 0.11 | 0.56 | 0.24 | 0.09 |

| 2006 | 4,183 | 0.11 | 0.55 | 0.25 | 0.09 |

| 2007 | 3,919 | 0.10 | 0.54 | 0.25 | 0.11 |

Table 8 presents the representativeness of our sample with respect to the manufacturing sector by size category. For value added, the share of firms with more than 200 employees is 7 percentage points higher in the manufacturing sector than in our sample. On the contrary, this share is 6 percentage points lower in the manufacturing sector relative to our sample for firms with 50–199 employees. The representativeness of our sample is better across the three different size categories for employment and the wage bill.

Shares of total manufacturing economic activity by firm size category (average for 1998–2007).

| Economic activity | 10–49 employees | 50–199 employees | 200+ employees |

|---|---|---|---|

| Share of value added: | |||

| Sample | 0.11 | 0.26 | 0.63 |

| Manufacturing sector | 0.10 | 0.20 | 0.70 |

| Share of employment: | |||

| Sample | 0.19 | 0.30 | 0.51 |

| Manufacturing sector | 0.18 | 0.28 | 0.54 |

| Share of wage bill: | |||

| Sample | 0.14 | 0.29 | 0.57 |

| Manufacturing sector | 0.12 | 0.26 | 0.62 |

-

Notes: This table only analyzes plants with more than 10 employees since those with less than 10 are underrepresented in the ENIA.

B Profit Tax Rate Facts in Chile

Variation of tax rates explained by firm group exemptions (R 2).

| Year | Size by employment | Size by sales | Size by value added |

|---|---|---|---|

| 1998 | 0.0332 | 0.0460 | 0.0443 |

| 1999 | 0.0377 | 0.0397 | 0.0365 |

| 2000 | 0.0347 | 0.0329 | 0.0416 |

| 2001 | 0.0445 | 0.0450 | 0.0550 |

| 2002 | 0.0271 | 0.0299 | 0.0345 |

| 2003 | 0.0260 | 0.0354 | 0.0345 |

| 2004 | 0.0262 | 0.0422 | 0.0324 |

| 2005 | 0.0320 | 0.0320 | 0.0392 |

| 2006 | 0.0336 | 0.0445 | 0.0386 |

| 2007 | 0.0308 | 0.0503 | 0.0468 |

-

Notes: This table reports the R 2 for the regressions of residual effective tax rates on firm size, region, business entity type, and industry, as well as the interactions between them. Residual effective tax rates are the residuals of a regression of effective tax rates on firm fixed effects and year fixed effects. We use three different size variables, which are measured by employment, sales, and value added. The table reports results separately for each size variable. The groups for each size variable are based on a standard categorization by the ENIA. There are 9 groups for employment and 10 groups for sales and value added. Firms are classified into 12 region groups and 8 types of business entities. Last, we group firms by two-digit industries according to the ISIC Rev. 3 industry classification.

C Model Solution

C.1 Firms’ Policy Functions

In this section, we characterize the explicit solutions of firm i’s optimal inputs and price choices. Define firm i’s optimal choices of capital, labor, and price as

where

and accounting profit,

Let

Hence, the first order condition of labor in Equation (6) yields:

Substituting this into the first order condition of capital in Equation (5) provides the expression of

The explicit solution of

Analogously, the explicit expression of

Similarly, define

Using the first order conditions for capital and labor, Equations (7) and (8), respectively,

The expression of

Analogously, the explicit expression of

Last, if

C.2 Equilibrium Computation Algorithm

In this section we describe the algorithm used to compute the model’s equilibrium for different tax policies. The algorithm considers a series of loops that leverage the bisection method to solve for aggregate, industry, and firm-level quantities and prices so that all markets clear. The algorithm is the following:

Firm output wedges

At the aggregate level, guess the equilibrium wage, w, and the aggregate output level, Y.

At the industry level, guess the set of industry prices

Taking the guesses of wage, aggregate output, and industry prices as given, solve each firms’ optimal choices of price, P si , labor, L si , and capital, K si , and compute firm-level output, Y si .

Taking the guesses of wage and aggregate output, ensure that the industry good demand,

At the aggregate level, ensure that the equilibrium price of the final good,

D Sensitivity Analysis

Output gap decomposition: hours as labor input, t si = 0 (percent).

| Year | Output gap | TFP gap | Intersectoral K | Intersectoral L | ΔAggregate capital |

|---|---|---|---|---|---|

| 2001 | 67.93 | 14.94 | −2.50 | 2.10 | 53.38 |

| 2002 | 60.80 | 14.36 | −0.81 | 1.98 | 45.32 |

| 2003 | 66.75 | 14.74 | −1.78 | 3.10 | 50.71 |

| 2004 | 80.08 | 23.41 | −3.88 | 3.21 | 57.39 |

| 2005 | 101.54 | 31.07 | −3.95 | 2.36 | 72.02 |

| 2006 | 123.91 | 33.70 | −1.40 | 13.15 | 78.42 |

| 2007 | 118.84 | 32.19 | −4.47 | 4.97 | 86.14 |

E Robustness Checks on the Measurement of Effective Tax Rates

Output gap decomposition: loss carryforward, t si = 0 (percent).

| Output gap | TFP gap | Intersectoral K | Intersectoral L | ΔAggregate capital |

|---|---|---|---|---|

| 22.99 | 6.18 | 0.78 | 0.74 | 15.30 |

Characteristics of effective profit tax rates: permanent sample.

| Year | Statutory tax rate (percent) | Tax rate = 0 (percent of firms) | Tax rate < statutory (percent of firms) | St. dev. (percent) |

|---|---|---|---|---|

| 2003 | 16.5 | 22.91 | 65.17 | 12.53 |

| 2004 | 17 | 16.74 | 64.54 | 11.06 |

| 2005 | 17 | 16.84 | 64.75 | 11.52 |

| 2006 | 17 | 16.95 | 64.85 | 10.38 |

| 2007 | 17 | 18.51 | 63.39 | 13.05 |

Relationship between TFP gap and

References

Ábrahám, Árpád, Piero Gottardi, Joachim Hubmer, and Lukas Mayr. 2023. “Tax Wedges, Financial Frictions and Misallocation.” Journal of Public Economics 227: 105000. https://doi.org/10.1016/j.jpubeco.2023.105000.Search in Google Scholar

Altshuler, Rosanne, and Alan J. Auerbach. 1990. “The Significance of Tax Law Asymmetries: An Empirical Investigation.” Quarterly Journal of Economics 105 (1): 61–86. https://doi.org/10.2307/2937819.Search in Google Scholar

Asker, John, Allan Collard-Wexler, and Jan De Loecker. 2014. “Dynamic Inputs and Resource (Mis)Allocation.” Journal of Political Economy 122 (5 (October): 1013–63. https://doi.org/10.1086/677072.Search in Google Scholar

Auerbach, Alan J. 1986. “The Dynamic Effects of Tax Law Asymmetries.” The Review of Economic Studies 53 (2): 205–25. https://doi.org/10.2307/2297647.Search in Google Scholar

Auerbach, Alan J. 2002. “Taxation and Corporate Financial Policy.” Handbook of Public Economics 3: 1251–92.10.1016/S1573-4420(02)80023-4Search in Google Scholar

Auerbach, Alan J. 2018. “Measuring the Effects of Corporate Tax Cuts.” The Journal of Economic Perspectives 32 (4): 97–120. https://doi.org/10.1257/jep.32.4.97.Search in Google Scholar

Buera, Francisco J., Joseph P. Kaboski, and Yongseok Shin. 2011. “Finance and Development: A Tale of Two Sectors.” The American Economic Review 101 (5): 1964–2002. https://doi.org/10.1257/aer.101.5.1964.Search in Google Scholar

Caggese, Andrea, Vicente Cuñat, and Daniel Metzger. 2019. “Firing the Wrong Workers: Financing Constraints and Labor Misallocation.” Journal of Financial Economics 133 (3): 589–607. https://doi.org/10.1016/j.jfineco.2017.10.008.Search in Google Scholar

Calcagnini, Giorgio, Germana Giombini, and Enrico Saltari. 2009. “Financial and Labor Market Imperfections and Investment.” Economics Letters 102 (1): 22–6. https://doi.org/10.1016/j.econlet.2008.10.005.Search in Google Scholar

Cingano, Federico, Marco Leonardi, Julian Messina, and Giovanni Pica. 2010. “The Effects of Employment Protection Legislation and Financial Market Imperfections on Investment: Evidence from a Firm-Level Panel of EU Countries.” Economic Policy 25 (61): 117–63. https://doi.org/10.1111/j.1468-0327.2009.00235.x.Search in Google Scholar

Cingano, Federico, Marco Leonardi, Julian Messina, and Giovanni Pica. 2016. “Employment Protection Legislation, Capital Investment and Access to Credit: Evidence from Italy.” The Economic Journal 126 (595): 1798–822. https://doi.org/10.1111/ecoj.12212.Search in Google Scholar

Cummins, Jason G., Kevin A. Hassett, R. Glenn Hubbard, Robert E. Hall, and Ricardo J. Caballero. 1994. “A Reconsideration of Investment Behavior Using Tax Reforms as Natural Experiments.” Brookings Papers on Economic Activity 1994 (2): 1–74. https://doi.org/10.2307/2534654.Search in Google Scholar

Da Rin, Marco, Marina Di Giacomo, and Alessandro Sembenelli. 2011. “Entrepreneurship, Firm Entry, and the Taxation of Corporate Income: Evidence from Europe.” Journal of Public Economics 95 (9–10): 1048–66. https://doi.org/10.1016/j.jpubeco.2010.06.010.Search in Google Scholar

Da-Rocha, José-María, Diego Restuccia, and Marina Mendes Tavares. 2019. “Firing Costs, Misallocation, and Aggregate Productivity.” Journal of Economic Dynamics and Control 98: 60–81. https://doi.org/10.1016/j.jedc.2018.09.005.Search in Google Scholar

David, Joel M., Hugo A. Hopenhayn, and Venky Venkateswaran. 2016. “Information, Misallocation, and Aggregate Productivity.” Quarterly Journal of Economics 131 (2): 943–1005. https://doi.org/10.1093/qje/qjw006.Search in Google Scholar

Devereux, Michael P., and Rachel Griffith. 2003. “Evaluating Tax Policy for Location Decisions.” International Tax and Public Finance 10: 107–26. https://doi.org/10.1023/a:1023364421914.10.1023/A:1023364421914Search in Google Scholar

Djankov, Simeon, Tim Ganser, Caralee McLiesh, Rita Ramalho, and Andrei Shleifer. 2010. “The Effect of Corporate Taxes on Investment and Entrepreneurship.” American Economic Journal: Macroeconomics 2 (3): 31–64. https://doi.org/10.1257/mac.2.3.31.Search in Google Scholar

Erosa, Andrés, and Beatriz González. 2019. “Taxation and the Life Cycle of Firms.” Journal of Monetary Economics 105: 114–30. https://doi.org/10.1016/j.jmoneco.2019.04.006.Search in Google Scholar

Foster, Lucia, John Haltiwanger, and Chad Syverson. 2008. “Reallocation, Firm Turnover, and Efficiency: Selection on Productivity or Profitability?” The American Economic Review 98 (1): 394–425. https://doi.org/10.1257/aer.98.1.394.Search in Google Scholar

Gopinath, Gita, Şebnem Kalemli-Özcan, Loukas Karabarbounis, and Carolina Villegas-Sanchez. 2017. “Capital Allocation and Productivity in South Europe.” Quarterly Journal of Economics 132 (4): 1915–67. https://doi.org/10.1093/qje/qjx024.Search in Google Scholar

Gourio, Francois, and Jianjun Miao. 2010. “Firm Heterogeneity and the Long-Run Effects of Dividend Tax Reform.” American Economic Journal: Macroeconomics 2 (1): 131–68. https://doi.org/10.1257/mac.2.1.131.Search in Google Scholar

Graham, John R. 1996. “Proxies for the Corporate Marginal Tax Rate.” Journal of Financial Economics 42 (2): 187–221. https://doi.org/10.1016/0304-405x(96)00879-3.Search in Google Scholar

Graham, John R., and Lillian F. Mills. 2008. “Using Tax Return Data to Simulate Corporate Marginal Tax Rates.” Journal of Accounting and Economics 46 (2–3): 366–88. https://doi.org/10.1016/j.jacceco.2007.10.001.Search in Google Scholar

Graham, John R., Michael L. Lemmon, and James S. Schallheim. 1998. “Debt, Leases, Taxes, and the Endogeneity of Corporate Tax Status.” The Journal of Finance 53 (1): 131–62. https://doi.org/10.1111/0022-1082.55404.Search in Google Scholar

Guner, Nezih, Gustavo Ventura, and Yi Xu. 2008. “Macroeconomic Implications of Size-Dependent Policies.” Review of Economic Dynamics 11 (4): 721–44. https://doi.org/10.1016/j.red.2008.01.005.Search in Google Scholar

Haltiwanger, John, Robert Kulick, and Chad Syverson. 2018. “Misallocation Measures: The Distortion that Ate the Residual,” National Bureau of Economic Research Working Paper 24199 (January).10.3386/w24199Search in Google Scholar

Hopenhayn, Hugo A. 2014. “Firms, Misallocation, and Aggregate Productivity: A Review.” Annual Review of Economics 6 (1): 735–70. https://doi.org/10.1146/annurev-economics-082912-110223.Search in Google Scholar

Hopenhayn, Hugo, and Richard Rogerson. 1993. “Job Turnover and Policy Evaluation: A General Equilibrium Analysis.” Journal of Political Economy 101 (5): 915–38. https://doi.org/10.1086/261909.Search in Google Scholar

Hsieh, Chang-Tai, and Peter J. Klenow. 2009. “Misallocation and Manufacturing TFP in China and India.” Quarterly Journal of Economics 124 (4): 1403–48. https://doi.org/10.1162/qjec.2009.124.4.1403.Search in Google Scholar

Hsieh, Chang-Tai, and Jonathan A. Parker. 2007. “Taxes and Growth in a Financially Underdeveloped Country: Evidence from the Chilean Investment Boom.” Economia 8 (1): 1, https://doi.org/10.1353/eco.2008.0004.Search in Google Scholar

Kaymak, Barış, and Immo Schott. 2019. “Loss-Offset Provisions in the Corporate Tax Code and Misallocation of Capital.” Journal of Monetary Economics 105: 1–20. https://doi.org/10.1016/j.jmoneco.2019.04.011.Search in Google Scholar

Levinsohn, James, and Amil Petrin. 2003. “Estimating Production Functions Using Inputs to Control for Unobservables.” The Review of Economic Studies 70 (2): 317–41. https://doi.org/10.1111/1467-937x.00246.Search in Google Scholar

Liu, Lili. 1993. “Entry-Exit, Learning, and Productivity Change: Evidence from Chile.” Journal of Development Economics 42 (2): 217–42. https://doi.org/10.1016/0304-3878(93)90019-j.Search in Google Scholar

McGrattan, Ellen R., and Edward C Prescott. 2005. “Taxes, Regulations, and the Value of US and UK Corporations.” The Review of Economic Studies 72 (3): 767–96. https://doi.org/10.1111/j.1467-937x.2005.00351.x.Search in Google Scholar

Midrigan, Virgiliu, and Daniel Yi Xu. 2014. “Finance and Misallocation: Evidence from Plant-Level Data.” The American Economic Review 104 (2): 422–58. https://doi.org/10.1257/aer.104.2.422.Search in Google Scholar

Oberfield, Ezra. 2013. “Productivity and Misallocation During a Crisis: Evidence from the Chilean Crisis of 1982.” Special Issue: Misallocation and Productivity. Review of Economic Dynamics 16 (1): 100–19. https://doi.org/10.1016/j.red.2012.10.005.Search in Google Scholar

Olley, G. Steven, and Ariel Pakes. 1996. “The Dynamics of Productivity in the Telecommunications Equipment Industry.” Econometrica 64 (6): 1263–97. https://doi.org/10.2307/2171831.Search in Google Scholar

Petrin, Amil, and Jagadeesh Sivadasan. 2013. “Estimating Lost Output from Allocative Inefficiency, with an Application to Chile and Firing Costs.” The Review of Economics and Statistics 95 (1): 286–301. https://doi.org/10.1162/rest_a_00238.Search in Google Scholar

Plesko, George A. 2003. “An Evaluation of Alternative Measures of Corporate Tax Rates.” Journal of Accounting and Economics 35 (2): 201–26. https://doi.org/10.1016/s0165-4101(03)00019-3.Search in Google Scholar

Poterba, James M., and Lawrence H. Summers. 1984. The Economic Effects of Dividend Taxation. Technical report. National Bureau of Economic Research.10.3386/w1353Search in Google Scholar

Restuccia, Diego, and Richard Rogerson. 2008. “Policy Distortions and Aggregate Productivity with Heterogeneous Establishments.” Review of Economic Dynamics 11 (4): 707–20. https://doi.org/10.1016/j.red.2008.05.002.Search in Google Scholar

Restuccia, Diego, and Richard Rogerson. 2017. “The Causes and Costs of Misallocation.” The Journal of Economic Perspectives 31 (3): 151–74. https://doi.org/10.1257/jep.31.3.151.Search in Google Scholar

Rossbach, Jack, and Jose Asturias. 2017. Misallocation in the Presence of Multiple Production Technologies. 2017 Meeting Papers 1094. Society for Economic Dynamics.Search in Google Scholar

Sedlácek, Petr, and Vincent Sterk. 2019. “Reviving American Entrepreneurship? Tax Reform and Business Dynamism.” Journal of Monetary Economics 105: 94–108. https://doi.org/10.1016/j.jmoneco.2019.04.009.Search in Google Scholar

Shevlin, Terry J. 1999. “A Critique of Plesko’s’ an Evaluation of Alternative Measures of Corporate Tax Rates.” Working Paper, University of Washington.10.2139/ssrn.190436Search in Google Scholar

Uras, Burak R. 2014. “Corporate Financial Structure, Misallocation and Total Factor Productivity.” Journal of Banking & Finance 39: 177–91. https://doi.org/10.1016/j.jbankfin.2013.11.011.Search in Google Scholar

Whited, Toni M., and Jake Zhao. 2021. “The Misallocation of Finance.” The Journal of Finance 76 (5): 2359–407. https://doi.org/10.1111/jofi.13031.Search in Google Scholar

Supplementary Material

This article contains supplementary material (https://doi.org/10.1515/bejm-2023-0138).

© 2024 Walter de Gruyter GmbH, Berlin/Boston

Articles in the same Issue

- Frontmatter

- Advances

- Corporate Tax Rates, Allocative Efficiency, and Aggregate Productivity

- Contributions

- Endogenous Financial Friction and Growth

- Decomposing Structural Change

- Industry Impacts of US Unconventional Monetary Policy

- Monetary Policy Transmission in Canada – A High Frequency Identification Approach

- Child Labor, Corruption, and Development

- Inflation Uncertainty from Firms’ Perspective, Overconfidence and Credibility of Monetary Policy

- Does Nominal Wage Stickiness Affect Fiscal Multiplier in a Two-Agent New Keynesian Model?

- To Create or to Redistribute? That is the Question

- Estimating Expected Asset Returns with the Present Value Model of Consumption and Fed Forecasts

Articles in the same Issue

- Frontmatter

- Advances

- Corporate Tax Rates, Allocative Efficiency, and Aggregate Productivity

- Contributions

- Endogenous Financial Friction and Growth

- Decomposing Structural Change

- Industry Impacts of US Unconventional Monetary Policy

- Monetary Policy Transmission in Canada – A High Frequency Identification Approach

- Child Labor, Corruption, and Development

- Inflation Uncertainty from Firms’ Perspective, Overconfidence and Credibility of Monetary Policy

- Does Nominal Wage Stickiness Affect Fiscal Multiplier in a Two-Agent New Keynesian Model?

- To Create or to Redistribute? That is the Question

- Estimating Expected Asset Returns with the Present Value Model of Consumption and Fed Forecasts