Veto Bargaining with Incomplete Information and Risk Preference: An Analysis of Brinkmanship

-

Joongsan Hwang

Abstract

This paper explains brinkmanship with infinitely repeated veto bargaining games, where players have private information. In the basic model, the paper solves for two types of Perfect Bayesian Equilibria. First, in Risk-Taking Equilibria (RTE), the proposer is more risk-seeking and engages in brinkmanship. Secondly, in Risk-Avoiding Equilibria (RAE), the proposer is more risk-averse and does not engage in it. Brinkmanship is likely to fail because the vetoer knows that once she succumbs to brinkmanship, the proposer will learn her weakness and make her worse offers. In the extended model, thresholds represent preconditions for negotiation. In the Threshold Pooling Equilibria (TPE) for the extended model, the vetoer sets a threshold and sticks to it. This way, the vetoer may increase her expected utility.

Give an inch and they’ll take a mile.

American Proverb

1 Introduction

Brinkmanship refers to the strategy of threatening the opponent with disaster to obtain a favorable outcome (Smith et al 2008, p. 390; Snyder 2001, p. 117). Schelling (1967, p. 91) explains brinkmanship the following way.

The creation of risk–usually a shared risk–is the technique of compellence that probably best deserves the name of “brinkmanship.” It is a competition in risk-taking. It involves setting afoot an activity that may get out of hand, initiating a process that carries some risk of unintended disaster. The risk is intended, but not the disaster.

The possible disaster is the leverage the party engaging in brinkmanship has to compel the other side to act. However, the disaster can strike both parties. So usually, the party engaging in brinkmanship also takes on the risk of disaster which means that the party’s action can depend on its evaluation and preference regarding risk (p. 94).

Brinkmanship is a common negotiating strategy. It is found in labor contract, trade deal and peace treaty negotiations among others. A labor union that threatens the employer with a strike knows that a strike is costly for both sides but believes that the threat can get the union a better deal. In negotiating a trade deal, one side might threaten to walk away from the negotiations and start a trade war where both sides suffer high tariffs on exports. Similarly, for peace treaty negotiations, a nation may threaten prolonged war or escalation of war.

Despite the common occurrence of brinkmanship in negotiating deals, brinkmanship often fails. The success of brinkmanship would mean that the disaster did not happen. In history, there are cases where the disaster happened. Also, for the party making the threat, often they backed off or the resulting deal was no better than the deal that they could have gotten without brinkmanship. For example, North Korea is a frequent user of brinkmanship.[1] Its relation with other countries is that it is one of the most isolated countries in the world.[2] In the United States, debt limit fights and government shutdown fights have been common. These fights result in disaster if a deal is not reached. Most end with a deal that does little to change the status quo. Many shutdowns have happened.[3]

This paper is the first paper to study how the use of brinkmanship changes depending on the risk preference of the party engaging in brinkmanship using game theory. Previous papers choose different explanations for brinkmanship. Some explained brinkmanship or strikes with irrational types.[4] It is also the first to explain why brinkmanship is unlikely to succeed by analyzing how information revealed in a repeated game changes players’ interaction. In the basic model of the paper, I solve for the Perfect Bayesian equilibrium (PBE) of a veto bargaining game with incomplete information – players’ types are private information. The game is infinitely repeated and asymmetric. In each period t of the game, the proposer proposes a new policy, action or a good, a t . The vetoer can veto this proposal. By making a proposal that has the risk of being vetoed, the proposer may engage in brinkmanship against the vetoer.

For the basic model, I find Risk-Taking equilibria (RTE) and Risk-Avoiding Equilibria (RAE). Brinkmanship happens and happens only in the RTE. RTEs are caused by the proposer’s risk love and RAEs are caused by the proposer’s risk aversion. The key result of the basic model that differs from models with irrational types is that brinkmanship is unlikely to succeed because in RTEs, the vetoer knows that the proposer will respond rationally to the failure of brinkmanship.

Because the vetoer knows that the parties have to bargain for more policies in the future, the vetoer is reluctant to succumb to the proposer’s brinkmanship. Succumbing to brinkmanship reveals that the vetoer is a “weak” type that succumbs to brinkmanship. Therefore, once the vetoer succumbs, the proposer uses the revelation to make proposals more unfavorable to the vetoer. There is a ratchet effect by which once the veteor accepts a unfavorable offer, the proposer’s offer will not get more favorable for the vetoer. By rejecting a brinkmanship offer, the vetoer builds a reputation to be a type that rejects bad offers. Given the potential future losses, the vetoer is reluctant to accept a brinkmanship offer without compensation for the losses. The difficulty of paying this compensation explains why brinkmanship is unlikely to succeed.

In the extended model, to discuss what the vetoer can do about brinkmanship, I model preconditions for negotiation as thresholds. In reality, before negotiations start, parties may insist that negotiations follow certain rules which limit the outcome of negotiations. For instance, a labor union may insist that the employer must promise that no wage cuts will be made before labor contract negotiations begin. The vetoer sets thresholds since only the vetoer responds to offers in the model. If the vetoer sets a threshold of ψ, until the threshold changes, any offer more unfavorable to the vetoer than ψ is automatically rejected without being seen by the vetoer.

The extension allows me to find Threshold Pooling Equilibria (TPE) where the vetoer sets a favorable threshold at the start of the game and never changes it on the equilibrium path. The TPE exists if the proposer is likely to meet the vetoer’s threshold with an offer favorable to the vetoer. The TPE can raise the veteor’s utility by having the vetoer only see favorable offers. Therefore, preconditions for negotiations can serve as a countermeasure for a proposer who engages in brinkmanship.

2 Literature Review

This paper contributes to the literature on bargaining games. In this literature, Rubinstein (1982) found an equilibrium for an game of pie division where offers are repeated until the players agree on the division. Fanning (2016) is a closely related paper which studies a model where agents divide a dollar. Here, agents imitate the behavior of irrational or “obstinate” agents and engage in brinkmanship. Unlike Fanning (2016), this paper explains brinkmanship using full rational players and risk preference.

This paper is also related to papers that explain the effects of risk preferences in bargaining. Roth (1985, 1989) state that risk aversion is disadvantageous in bargaining. However, Osborne (1985) finds that an increase in risk aversion can be advantageous in bargaining if players are asymmetric.

In my paper, vetoer is reluctant to reveal her type by accepting offers because she might get worse offers from the proposer. Three buyer-seller model papers deal with similar phenomena. In Fudenberg and Tirole (1983), both players may have incomplete information. The buyer may reject an earlier offer because he may get a better offer later. Hart and Tirole (1988) consider both the model where once the purchase is made the buyer can use the good infinitely and the model where the seller rents the good to the buyer for one period at a time. In the latter model, the seller has less leeway to price discriminate because the buyer knows revealing her information can be detrimental. Similar to the rent model, Schmidt (1993) has a finitely repeated game where in each period, one good can be sold. The buyer makes offers to the seller. If the seller reveals her cost, she cannot get information rent afterwards. There is a ratchet effect where revealing a low cost will lead to a low price. Therefore, unless the end of the game is near, the seller does not reveal his cost.

This paper uses a veto bargaining model. Romer and Rosenthal (1978) modeled bargaining in a political setting where an agenda setter has monopoly power over the proposals submitted and voters can reject the proposals. In Cameron (2000, p. 83–122), the president can veto the bill from congress. The president can build a policy reputation by vetoing in order to get a better bill from congress. Ali et al (2023) finds that when the proposer is unsure of the vetoer’s preferences, the proposer makes a sequence of offers to deal separately with different types of vetoers. In Cuellar and Rentschler (2023), the proposer can engage in brinkmanship by threatening the vetoer with a conflict. They find a brinkmanship equilibrium where the threat is probabilistic and the conflict harms both sides.

Fearon (1994), Slantchev (2003), and Powell (2006) study games related to war. Fearon (1994) models international crises and finds that democratic nations are more likely to back down compared to nondemocratic nations. This is because democracies impose higher costs of failure on leaders. In Slantchev (2003), player can learn about each other through negotiations and battlefield outcomes. Slantchev (2003) derives the principle of convergence that once both sides in war agree on the outcome, they can terminate war with a negotiated settlement. Powell (2006) states that war can happen when states are bargaining over sources of military power. Because concessions in bargaining weakens one’s position and leads to more concessions, states may go to war instead.

This paper is also related to the literature on brinkmanship in the context of war and conflict. Schelling (1967, p. 199–200) and Schelling (1981, p. 90–91) explain brinkmanship as deliberately creating the risk of disaster and using this risk to coerce the other party. Schelling (1981, p. 124–125) implies that in brinkmanship, one’s reputation and the other party’s expectations of how one will behave is valuable. This leads the parties to not back down in brinkmanship. In my paper, when the vetoer accepts low offer, the proposer will believe that the vetoer will accept low offers in the future as well. Thus, the vetoer may reject such offers.

In Skaperdas (2006), nations decide whether to bargain or go to war. Here, risk aversion causes the nations to prefer bargaining to going to war. If the future is more important to the nations, they are more likely to go to war because setting the dispute once and for all becomes more attractive compared to the costs of armed peace. In Schwarz and Sonin (2008), a potential aggressor can demand concessions from a weaker party by threatening war. The bargaining power of a potential aggressor increases dramatically if she can make probabilistic threats i.e. if she can engage in brinkmanship. The weaker party may go to war if concessions shift the balance of power.

For papers on conflicts, Acharya and Grillo (2015) is the one closed related to this one. In Acharya and Grillo (2015), nations can be rational or “crazy” (bellicose). A rational nation may adopt a madman strategy where it builds a reputation to be crazy. This can lead to limited war. In Powell (2015), a challenger can use military force to gain territory from the defender. However, the defender can engage in brinkmanship by creating the risk of that nuclear war will happen if the challenger does not back down. Powell (2015) finds that the more willing the defender is to raise this risk, the less military force the challenger uses.

In labor economics, Hicks (1963, p. 144–147) implies the “Hicks Paradox” that strikes happen even though they should not. Kennan (1986) explained the paradox by stating that if the outcome of strikes is accurately predicted, the parties should be able to agree on this outcome before the strikes and avoid the cost of strikes. In the context of this paper, the paradox means that the disaster from brinkmanship will never happen. In that case, brinkmanship will always fail and no one will engage in brinkmanship.

Many papers explain the phenomena of strikes while avoiding the Hicks Paradox. Reder and Neumann (1980) explains that incompleteness of bargaining protocols can cause strikes. If the bargaining between the employer and the labor union follows a very detailed set of rules, negotiations can reach a settlement without strikes. However, a situation that is not covered by the bargaining protocol can cause breakdowns in negotiations and strikes.

Some papers explain the phenomenon of strikes by assuming private information. If the parties do not know what contract the other side will accept, the outcome of strikes is uncertain and the paradox no longer applies. Unlike this paper which has infinite periods, some early papers deal with a setting where the game ends once an labor contract is reached. In Mauro (1982), both parties have private information and estimate what would it take for the other party to concede. Incorrect estimates can lead to strikes. Similarly, Tracy (1984) also studies a setting where both sides can have private information. Here, the less the union knows about the firm, the more likely and longer the strikes are.

On the other hand, in Hayes (1984), the firm has information about profitability that the union does not. In Hayes (1984), the union may use strikes as a tool for gaining information. Cheung and Davidson (1991) assumes that a union can represent workers at more than one firm and has private information about its utility. A union representing multiple firms is more likely to strike because it does not want to signal weakness.

Two recent papers that are closely related to this one analyze repeated games where in each period, the parties bargain over a new contract for the period. First, Robinson (1999) defines a game where the firm has private information about its profitability. In the model where this information is subsequently fully revealed, the union does not go on a strike. In the model where this information is not subsequently fully revealed, the union may go on a strike. In Robinson (1999) strikes are a tool to punish the firm not to extract concessions from the firm. Second, in Calabuig and Olcina (2000), both parties have private information. Both try to build reputations of being “stubborn” and irrational which results in strikes.

3 Basic Model

The veto bargaining game has two players, a proposer (he) and a vetoer (she). Only the proposer makes offers. This allows me to demonstrate brinkmanship as a unilateral strategy by the proposer.[5] This is an infinitely repeated game that never ends. Having many periods in the game means that players care about what happens in the future. (While the model would arrive at similar results as long as the number of periods is large. I specifically use infinite periods for simplification.) At the start of the game, the proposer observes S P and the vetoer observes S V . Both are independent private random variables and specify players’ types. In each period, t ∈ {1, 2, …}, proposer offers a proposal or an action, a t , to the vetoer. Then, vetoer decides whether to accept or reject a t . Figure 1 depicts this model.

Game tree for the basic model.

3.1 Payoffs

Players’ payoffs are constructed from period utilities. When the offer is rejected, both players receive 0 utility for the period. This is the disaster that can happen for the players.[6] When the offer is accepted, the proposer’s utility for the period is

where u is the following constant absolute risk aversion (CARA) utility function.

I use CARA utility for the proposer to model the proposer’s risk aversion. CARA utility has useful proprieties that help me to analyze the relation between the proposer’s risk aversion and the proposer’s equilibrium strategies. The most important one is that by Pratt (1964)’s theorem 1, for CARA utility, the higher the proposer’s absolute risk aversion, η, the higher the risk premium. In other words, a more risk-averse proposer requires a greater payment in order for him to take the same amount of risk. Another useful property is that for any η, u(0) = 0. This helps me simplify many formulas.

When the offer is accepted, the vetoer’s utility for the period is

This means that I can interpret the vetoer as a risk-neutral vetoer with CARA utility. (Since the vetoer cannot engage in brinkmanship, her risk preference is not important for the results.) The greater a t is, the more favorable the deal is to the vetoer and the less favorable the deal is to the proposer. This means that a t can also be thought of as a payment offer from the proposer to the vetoer.

The proposer’s and the vetoer’s discount factors are respectively δ P ∈ (0, 1) and δ V ∈ (0, 1). Having separate discount factors lets me distinguish each player’s condition for the PBEs. Players’ maximize the expectation of the discounted sum of their utilities.

3.2 Players’ Types, S P and S V

The image of S P is {p L , p H }. The image of S V is {v L , v M , v H }.[7]

From the values, p H is the greatest and p L is between v L and v M .[8] I denote the probabilities of p L , p H , v L , v M and v H the following way.

When S V = v L , S V = v M or S V = v H , I respectively say that the vetoer is low, medium or high type. I use these terms the same way for the proposer.

4 Results

To describe my equilibria, I first define the equilibrium concept. I solve for Perfect Bayesian Equilibria (PBE)[9] that satisfy the following assumption.

Assumption 1.

The proposer’s offer for any period t is the output of the real-valued function a(S P , b) where b is the proposer’s belief of vetoer’s type as he decides this period’s offer.

The vetoer’s decision for any period t is given by the cut-off function γ(S V , b). The vetoer accepts any offer equal to or greater than γ(S V , b) and rejects any offer below it.

The above equilibrium concept is inspired by Fudenberg et al (1985)’s strong-Markov equilibrium. In Assumption 1, the proposer’s offer depends on S P , his type, and b, the proposer’s belief about the vetoer’s type. The vetoer’s decision depends on the vetoer’s type, S V , and b in addition to the offer for the period t, a t . The vetoer’s decision does not depend on her belief about the proposer’s type because the vetoer reacts to the offers and does not make offers.

The key factor that decides the equilibrium dynamics is what the proposer believes and knows about the vetoer’s type. How the proposer adjusts his belief depends on what the proposer’s current belief is. Unlike in Fudenberg et al (1985) where the game ends when the offer is accepted, in my model, there is always the next offer even if the current offer is accepted. Because of this, vetoer considers what the proposer knows and also considers what her decision tells him about her type and how this will affect her future utility. While the vetoer does not observe the proposer’s belief directly, I find PBEs satisfying Assumption 1, where for the vetoer’s decision, the vetoer can tell the proposer’s belief from the actions of the game.[10]

In Assumption 1, players’ methods of deciding their action do not change between periods. To elaborate, I impose the conditions that the proposer’s offer is the output of a function and that the vetoer’s decision is made by her cut-off function. Once the inputs of the function are known, the period does not matter at all for the player’s strategy for the period. This helps me drastically simplify the players’ strategies in an equilibrium.

An equilibrium satisfying Assumption 1 has Markov properties in that for any period, the player’s strategies and utilities are given by the state indicators, S V , S P and b. In other words, players’ types and the proposer’s beliefs are what matters. The history of the game does not affect the players types and once the proposer’s belief is known, the history has no further useful information.

The following definition lists the three main beliefs that the proposer can have. b0 is the proposer’s initial belief in the game.

Definition 1.

b L means that proposer believes that the vetoer is low type.

b−L means that proposer believes that the vetoer is medium type with probability

b0 means that proposer believes that the vetoer is low type with probability g L , medium type with probability g M and high type with probability g H .

All proofs for this section are in Appendix 1.

4.1 Risk-Taking Equilibria

I define a risk-taking equilibrium (RTE) using players’ strategies.

Definition 2.

A Risk-Taking Equilibrium (RTE) is a PBE satisfying Assumption 1 where the following holds.

Proposer’s strategy:

a(p L , b L ) = a(p H , b L ) = a(p L , b−L) = v L

a(p H , b−L) = v H

Vetoer’s strategy:

γ(v L , b L ) = v L

γ(v L , b−L) = γ(v H , b L ) = v H

γ(v M , b L ) = v M

∀b ∈ {b−L, b0}: γ(v M , b) = γ(v H , b) = v H

Note that in the above definition, the proposer offers

From the vetoer’s strategy, (iv), (v) and (viii) are the important parts. By (iv) and (viii), when the vetoer’s type has not been revealed, the low type vetoer accepts

Given the above strategies, I explain how the game plays on the equilibrium path for an RTE that is depicted in Figure 2. In the figure, the ovals contain the offers for the periods. In period 1, proposer always acts first believing b0. So the first offer is

Offers on the equilibrium path in an RTE.

The reason that the proposer initially offers

The proposer’s strategy demonstrates the ratchet effect. Once a vetoer accepts an offer, the proposer does not offer a higher offer because the proposer knows that the vetoer is of a type that will accept the previous offer. In fact, when the initial low offer of

In the RTEs, players sources of surplus are different. The proposer’s surplus comes from first-mover advantage and information about the vetoer. The first-mover advantage allows the proposer to propose a low policy or action that the vetoer would not propose. The proposer’s information about the vetoer lets him offer a low policy and action that will still be accepted.

On the other hand, the vetoer’s surplus comes from information rent. The vetoer’s information rent comes from the fact that the vetoer knows her own type but there are circumstances where the proposer thinks that the vetoer’s type can be higher. In period 1, the low type vetoer derives surplus from the fact that the proposer is unable to distinguish her from a medium or high type vetoer. In period 2, the medium type vetoer derives surplus from the fact that the proposer is unable to distinguish her from a high type vetoer. Vetoer’s expected payoff in an RTE is

Proposition 1.

The following is sufficient for an RTE to exist. (i) and (ii) are also necessary for an RTE to exist.

δ V ≥ 0.5

The above proposition explains restrictions that let an RTE exist. (i) and (ii) are satisfied in any RTE. In (i), the left side is the expected cost of brinkmanship for the high type proposer. If brinkmanship fails, it is costly. The right side of (i) is the expected benefit of brinkmanship for the high type proposer. Brinkmanship is beneficial when it succeeds. In (ii), the right side is the expected payoff of the low type proposer when the vetoer is low type. (i) and (ii) contain

To explain (iv), I present Lemma 1. The proof of Lemma 1 and Proposition 1 in Appendix 1 and Lemma 3 in The Supplementary Material explain in more detail the progress and the beliefs of the game.

Lemma 1.

(iv) and Lemma 1 mean that in a RTE, the brinkmanship offer,

Proposition 2.

Suppose δ

V

≥ 0.5,

The above proposition establishes the relationship between the proposer’s risk preference and the existence of RTEs. When the other parameters of the model and

4.2 Risk-Avoiding Equilibria

The following defines the Risk-Avoiding Equilibrium (RAE).

Definition 3.

A Risk-Avoiding Equilibrium (RAE) is a PBE satisfying Assumption 1 where the following holds. Proposer’s strategy:

a(p H , b0) = a(p H , b−L) = v H

a(p H , b L ) = a(p L , b0) = a(p L , b L ) = a(p L , b−L) = v L

Vetoer’s strategy:

γ(v L , b0) = γ(v L , b L ) = v L

γ(v L , b−L) = γ(v H , b L ) = v H

γ(v M , b L ) = v M

∀b ∈ {b−L, b0}: γ(v M , b) = γ(v H , b) = v H

The above definition defines the players’ strategies using the three beliefs defined in Definition 1, b L , b−L and b0. For these beliefs, the proposer only offers v H when he is high type and he believes b−L or b0 and in all other cases, he offers v L . In other words, when the proposer thinks that the vetoer has a positive probability of not being the low type and gets positive utility from v H being accepted, he offers v H . When this is not true, the offer is v L .

From the vetoer’s strategy, (iii) and (vi) are the important parts. In (iii), when the proposer thinks that the vetoer may be the low type, the low type vetoer’s cut-off point is v L . In (vi), when the proposer believes that the vetoer may be the medium or high type, the medium or high type vetoer’s cut-off point is v H .

Now that I have spelt out the players’ strategies, I will explain the progress of the game on the equilibrium path for an RAE. In all periods, the low type proposer offers v L and the high type proposer offers v H . The v L offer is accepted by the low type vetoer and rejected by the medium and high type vetoers. The v H offer is accepted by all types of vetoers.

This means that if the vetoer is low type, the high type proposer can make low offers (v L in this case) and get it accepted in all periods. However, offering v L entails the risk of rejection by the medium and high type vetoers. Thus, for the RAE, brinkmanship refers to the following strategy by the high type proposer. In period 1, he offers v L . If it is accepted, he makes the same offer in subsequent periods. If it is rejected, he offers v H in subsequent periods. This brinkmanship does not happen in the RAE because the proposer weakly prefers to not take the risk of rejection from the brinkmanship. Instead, the high proposer plays it safe by making offers that any type of vetoer will accept.

When the vetoer knows that the proposer is not engaging in brinkmanship, she knows that the proposer is “honest”. In other words, for a proposer who never engages in brinkmanship, his type is fully revealed to the vetoer from his period 1 offer. The low type vetoer accepts an offer of v L because she knows that the low type proposer only offers v L . The medium and high type vetoers accept v H because this is what the high type proposer will offer them and the best offer they can get.

In an RAE, the proposer’s surplus comes from his first-mover advantage. On the equilibrium path, the proposer makes the lowest offer that the types of vetoer that he will make a deal with will accept for sure. Like in an RTE, vetoer’s surplus in an RAE comes from information rent. The vetoer’s surplus is only positive when the vetoer is low or medium type and the proposer is high type. In this case, the vetoer gets surplus because the proposer is unable to distinguish the low or medium type vetoer from the high type vetoer and does not risk rejection by making an offer lower than v H . Vetoer’s expected payoff in an RAE is

Proposition 3.

The following is sufficient for an RAE to exist. (i) is also necessary for an RAE to exist.

δ V ≥ 0.5

The above proposition states a sufficient condition and a necessary condition for the existence of an RAE. The proofs of this proposition in Appendix 1 and Lemma 11 in the Supplementary Material explain the progress of the game and the beliefs in the game in more detail.

In an RAE, the high type proposer decides whether he will play the equilibrium strategy or the brinkmanship strategy discussed earlier. In (i),

Proposition 4.

Suppose δ

V

≥ 0.5 and the parameters of the basic model are given. Then, there exists some

The above proposition establishes that given the other parameters of the model and a sufficiently patient vetoer with δ

V

≥ 0.5, an RAE exists if the proposer is risk-averse enough. In Proposition 4,

4.3 The Relation between the Two Types of Equilibria

The most important differences between RTEs and RAEs are how the proposer’s strategy responds to risk and how the vetoer’s strategy responds to the proposer’s strategy on risk. Therefore, it is natural to ask whether the same set of parameters can allow for both an existence of an RTE and an RAE. In this case, players’ interactions can create an RTE or an RAE. The below proposition establishes that no such set of parameters exists.

Proposition 5.

RTE and RAE do not coexist.

The reason that no RTE and RAE coexist can be explained by the proposer’s preference and actions. In an RTE, the high type proposer is willing engage in brinkmanship by offering

So for the same proposer, the RAE, the equilibrium without brinkmanship creates a condition more favorable for brinkmanship. In an RAE, the vetoer believes that the proposer tells the truth about his type. So when the proposer engages in brinkmanship, the vetoer believes the proposer to be low type. Also, the vetoer believes that v L is the best offer she can get from the low type proposer. Thus, the vetoer does not demand compensation for revealing her own type. So the vetoer’s trust in the proposer’s honesty in a RAE creates a greater incentive for the proposer to deceive the vetoer and engage in brinkmanship.

In an RAE, the high type proposer is unwilling to take the risk of brinkmanship despite the fact that he only has to offer v

L

to engage in brinkmanship. Then, he will prefer not to engage in brinkmanship in a RTE where he has to offer a greater amount,

For certain parameters of the model, Figure 3 answers when an RTE or an RAE exists depending on η, the proposer’s coefficient of absolute risk aversion. In the figure, the lines draw the proposer’s expected benefit from strategies. The “RAE strategy” line draws the right side of Proposition 3’s (i), the expected benefit from the RAE strategy in the RTE or the RAE. The “Brinkmanship in RAE” line draws the left side of Proposition 3’s (i), the expected benefit from brinkmanship in the RAE. The “RTE strategy” line draws the right side of Proposition 1’s (i), the expected benefit from the RTE strategy in the RTE. Note that the “Brinkmanship in RAE” line is above the RTE strategy. The conditions for a brinkmanship are more favorable for the proposer in a RAE compared to an RTE. This is confirmed by the fact that the expected benefit from brinkmanship is higher in a RAE.

Proposer’s expected benefit from strategies.13

Figure 3 demonstrate how the expected payoffs, optimal strategies and PBEs change depending on η, the coefficient of absolute risk aversion for the proposer. In the figure, the parameters are such that an RAE exists if and only if Proposition 3’s (i) is satisfied. Also, an RTE exists if and only if Proposition 1’s (i) is satisfied. When η ≳ −0.09, the expected benefit is weakly greater for the RAE strategy compared to the brinkmanship in RAE. This means that the proposer weakly prefers to not deviate and that an RAE exists. When η ≲ −0.32, the expected benefit is greater for the RTE strategy compared to the RAE strategy. Therefore, the proposer weakly prefers to not deviate to the RAE strategy and an RTE exists.[13]

Thus, following Proposition 4, when η ≳ −0.09, the proposer is risk averse enough that a RAE exists. On the other hand, following Proposition 2, when η ≲ −0.32, the proposer is risk-seeking enough that a RTE exists. Since RAEs only exists for η ≳ −0.09 and RTEs only exists for η ≲ −0.32, RTEs and RAEs never coexist as proven in Proposition 5.

4.4 Lack of Pooling Equilibria

A pooling equilibrium of the basic model is a PBE where γ(v L , b0) = γ(v M , b0) = γ(v H , b0). This means that in a pooling equilibrium, the vetoer sets the same initial cut-off point irrespective of her type. Because of this, proposer’s belief never changes from his initial belief of b0. When the proposer believe does not change from b0, the vetoer sticks to her initial cut-off point.

A pooling equilibrium has two advantages to the vetoer. Subsections 4.1 and 4.2 establish that the vetoer’s surplus in an RTE and an RAE comes from information rent. Therefore, never revealing her type induces information rent as the proposer will not be able to bargain down the vetoer. Secondly, never revealing her type means that the proposer has no offers accepted only by the low type vetoer such as brinkmanship offers and that he does not engage in brinkmanship. However, the following proposition shows that under a reasonable condition, the basic model has no pooling equilibria.

Proposition 6.

If the low type proposer’s strategy is that ∀t: a t = a > v L , there exists no PBE where γ(v L , b0) = γ(v M , b0) = γ(v H , b0).

To explain loosely, the fundamental problem with a pooling equilibrium comes from the fact that if the vetoer’s immutable cut-off point is too high for the low type proposer to meet, the low type proposer will make a low offer. In making this offer, the low type proposer will be able to truthfully say, “I cannot afford to make you an offer at the cut-off point. However, I will make a lower offer that I think could be mutually beneficial.” One way the low type proposer can make the vetoer believe this is to persist in the offer. (This is why the antecedent of the proposition has ∀t: a t = a > v L .) If the offer is mutually beneficial, the vetoer who believes this will accept it. If both players are low type, there is a mutually beneficial deal between v L and p L .

Setting a high immutable cut-off point blocks the low type vetoer from acceptable deals. When deals don’t happen, proposer realizes that the high cut-off point is the reason. When he does, it is not optimal for him to insist on the same cut-off point if a mutually beneficial deal exists. He should accept this deal that is lower than the cut-off point deal.

5 Extended Model

5.1 Preconditions and Thresholds

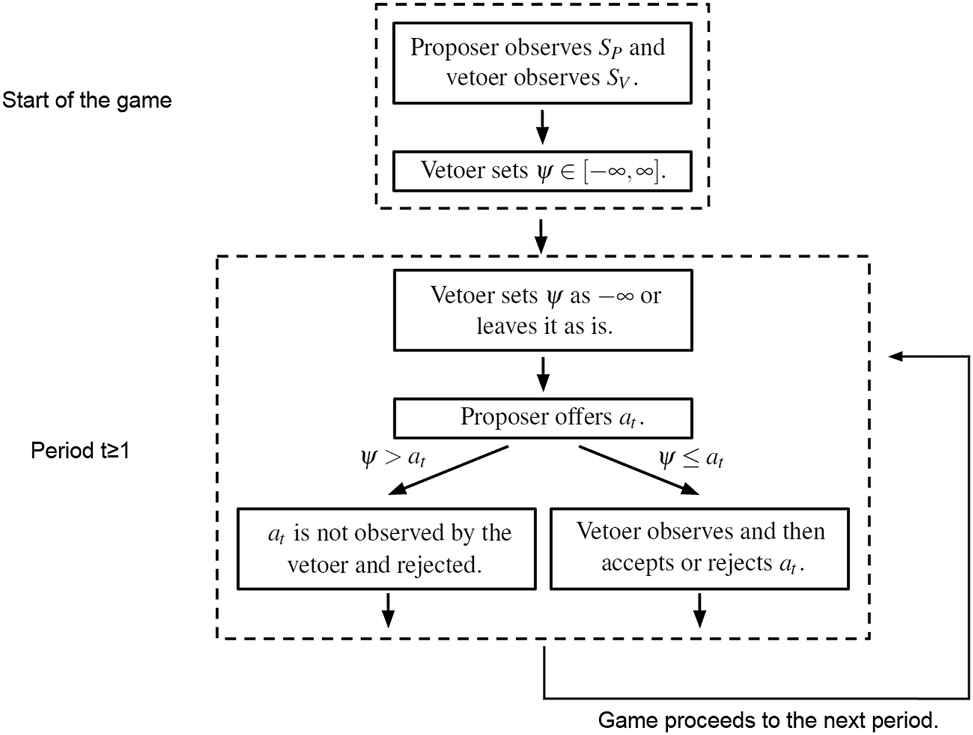

In actual negotiations, the vetoer may announce preconditions for negotiations before negotiations begin or claim unchangeable requirements for a deal at the start of negotiations. The extended model represents such preconditions and requirements using a threshold, ψ. If the vetoer is able to stick to these, they may significantly alter the outcome of negotiations.

I will explain the game for the extended model using Figure 4. In the extended model, at the start of the game, after the players observe their private information, S P and S V , the vetoer sets the public threshold, ψ ∈ [−∞, ∞]. (This means ψ is an element of the extended real line.) Now, the game proceeds the following way in any period for infinitely repeated periods. Before the proposer acts, the vetoer has a chance to set ψ as −∞. If the proposer’s offer, a t is less than ψ, it is automatically rejected and the vetoer does not observe a t . If a t greater than or equal to ψ, as in the basic model, vetoer observes a t and decides whether to accept or reject a t . ψ, the threshold below which all proposals are ignored, cannot be changed freely. ψ = −∞ means that all proposals will be heard. ψ > −∞ can be changed to ψ = −∞ in any period. However, after the vetoer decided to hear all proposals with ψ = −∞, the decision is irreversible.

Game tree for the extended model.

In specifying the threshold, ψ, I am modeling a situation where the veteor can decide to impose conditions what proposals she will consider and announce it but has difficulty adjusting these conditions once they are announced. For instance, in negotiating a labor contract, the labor union may announce that it will not accept any wage lower than $10 per hour. The actual negotiation would be handled by a union leader who repeats in every meeting that she does not have the authority to accept any offer below $10 and that any proposal given to her below $10 will be discarded without being heard or read. If the firm attempts to bargain with the members of the union directly, the members could say that they have entrusted bargaining process to the union leader and they will not bargain directly. Such a situation would correspond to setting ψ = 10 initially and sticking to it.

To rescind the announcement, the union can remove the leader and communicate with the proposing firm directly or retract the announcement. By doing so, the union will hear any proposal the proposing firm makes. However, setting a new consequential threshold different from the previous one may be problematic. Suppose the union leader claims that she has received a new direction from the union members lowering the threshold for negotiation to $9. Then, the union loses credibility for the claim that because it has entrusted its leader with negotiations and because its members will not listen to any proposals, its leader is the only one the firm can talk to.

Now, firm reasons that the union members are in communication with the leader and do change the terms of the negotiation based on new information. In this case, the members should be able to listen to information from the firm and readjust their demands. Additionally, if the previous statement that no offer will be considered below $10 was in fact wrong, the new statement can be wrong as well. The firm will doubt whether the threshold is more than an empty bluff serving as a negotiation tactic. In such circumstances, changing the threshold may effectively mean the abandonment of all thresholds for the current negotiation and negotiations of future labor contracts. This is because the firm will point out that it established that what the union claims as thresholds are in fact subject to change and will not believe any new consequential threshold.

Furthermore, if the union leader states that she will not accept an offer lower than $10 on one day, lowers this threshold to $9 on the next day and lowers this again to $8 the day after that, she is not setting preconditions for bargaining. She is already bargaining with the firm. This section models preconditions that are set for the duration of a negotiation and not offers by the vetoer.

5.2 Threshold Pooling Equilibria

In the extended model, I will focus on threshold pooling equilibria (TPE). Proposition 6 demonstrated that in general, pooling equilibria do not exist for the basic model. However, the introduction of the threshold, ψ in the extended model allows the vetoer to never accept or listen to offers below the threshold. In the TPEs, this threshold will always be the same regardless of her type. This is the key characteristic of the TPEs.

In an RTE or an RAE, the bargaining progress demonstrated that the proposer can acquire deals favorable to him using his ability to make offers and bargain down the vetoer. In the TPE, because the vetoer sets a minimum offer that she will accept and sticks to it, the proposer lose the ability to bargain down the vetoer. This lost ability includes the proposer’s ability to succeed in brinkmanship as well. Thus, if the TPE leads the proposer to offer and make deals less favorable to him, the vetoer is better off in a TPE compared to an RTE or an RAE.

For the TPE, players’ strategies adhere to the following assumption.

Assumption 2.

The proposer’s offer for any period is the output of the real-valued function, a′(S P , ψ), where ψ is the threshold that this offer faces.

The vetoer’s decision for any period is given by the function, γ(S V ). The vetoer accepts any offer equal to or greater than γ(S V ) and rejects any offer below it.

Unlike in Assumption 1 of the RTE and the RAE, in the above assumption, players’ strategies are not dependent on the proposer’s belief about the vetoer’s type. Instead, given the vetoer’s type, the vetoer has the same cut-off point for all periods. For the proposer, his offer for any period is determined by the same fuction whose input are his type and the threshold, ψ that applies to his offer.

Using the above definition, the following definition specifies the strategies in a TPE.

Definition 4.

A Threshold Pooling Equilibrium (TPE) is a PBE satisfying Assumption 2 where the following holds

Proposer’s strategy:

Vetoer’s strategy:

At the start of the game, vetoer sets ψ = p H .

In any period, vetoer leaves ψ as is.

γ(S V ) = S V

The vetoer’s strategy means that at the start of the game, vetoer sets the threshold, ψ to equal the high type proposer’s type, p H . Once set, this threshold never changes. From the offers that make through the threshold and are seen by the vetoer, the vetoer accepts any offer equal to or greater than her type, S V .

In the proposer’s strategy, S P < ψ is a case where the current threshold is greater than the proposer’s type S P . In this case, since all offers that make it through the threshold and are accepted give the proposer negative utility, proposer deliberately makes an offer, ψ − 1 that will be rejected without being viewed. The other case, S P ≥ ψ means that there exists some offer that makes it through the current threshold and can give the proposer non-negative utility. Here, from offers that make it through, the offer that the proposer makes is the lowest one that still gives the low type vetoer non-negative utility.

Figure 5 demonstrates how the game plays on the equilibrium path for a TPE. The proposer’s offers are in ovals. At the start of the game, the vetoer sets the threshold to be ψ = p H and never changes it. Because of this, the high type proposer always makes the only offer that makes it through the threshold and gives him non-negative utility which is p H . The vetoer always accepts this offer. On the other hand, the low type proposer never has any offer that makes it through the threshold and gives him non-negative utility. Thus, he always offers p H − 1 which is always rejected without being seen by the vetoer.

Offers on the equilibrium path in a TPE.

The following theorem states that a TPE exists if the proposer is unlikely to be low type.

Proposition 7.

A TPE exists if and only if

Proof. The proof is in Appendix 2.■

In equation (6), f H (p H − v L ) is the low type vetoer’s expected utility in a period where the proposer faces a threshold of ψ = p H . p L − v L is the low type vetoer’s expected utility in a period where the proposer faces a threshold of ψ = p L . Therefore, a TPE exists when the low type vetoer sees a threshold of ψ = p H at least as desirable as a threshold of ψ = p L . When the threshold is always at ψ = p H , it is too high for the low type proposer to make an offer from which the low type can benefit. If the low type vetoer instead always has a threshold of ψ = p L , she can see offers of ψ = p L from all types of proposers. Thus, the expected benefit of this deviation is that the low type vetoer can view the offer from the low type proposer. However, the expected cost of this deviation is that the offer from the high type proposer is reduced.

The vetoer understands that the abandonment of the threshold will mean that vetoer gives up the possibility of a good deal for her. Thus, in a TPE, the vetoer keeps the threshold even if the proposer is low type, deals fail and disasters strike. If, contrary to the assumption of the extended model, changing the threshold to a value above −∞ is possible, the vetoer might try to set a new threshold at a level where she might still get positive utility from a deal and the TPE might not hold. In reality, a vetoer whose strategy is akin to the TPE strategy, sets preconditions for a deal and continues to keep commensurate preconditions for future deals until the situation changes so much that how the vetoer acted previously loses predictive power for the new negotiation.

A TPE exists if and only if the expected benefit is weakly greater than the expected cost. For simplicity, I only deal with PBEs where the threshold is ψ = p H . Although I do not solve for them in this paper, if f H (p H − v L ) < p L − v L , there might be PBEs where ψ = p L .

Vetoer’s expected payoff in an TPE is

The vetoer uses her unchanging high threshold to take all the surplus. Therefore, the proposer’s expected payoff is 0.

I will use the above equation to compare the vetoer’s expected payoffs in an TPE, an RAE and a RTE by discussing how the game plays on the equilibrium paths. It is trivial to see that the expected payoff in equation (7) is always greater than the expected payoff for an RAE in equation (5). The expected benefit of a TPE compared to an RAE is that the threshold of ψ = p H negates the proposer’s first-mover advantage. Unlike in an RAE, the high type proposer can no longer acquire a deal of v H . This is because any offer below the threshold, ψ = p H is not seen by the vetoer. Unlike in an RAE, the proposer can not acquire deals that are no better than rejection for the vetoer because the vetoer will not see them.

The expected cost of a TPE compared to an RAE is 0. If the proposer happens to be low type, all of his offers will be rejected without being seen. However, this is not a loss for the vetoer because the low type proposer’s offer is always v L in the RAE. In the RAE, the low type proposer uses the first-mover advantage to make an offer is no better than nothing for vetoer under the best circumstances.

The expected benefit of a TPE compared to an RTE is twofold. The first is the negation of the first-mover advantage that I have mentioned while comparing the TPE to the RAE. All of the offers the proposer makes in the RTE, v

L

,

Secondly, the proposer’s information about the vetoer becomes useless to him in a TPE. Any offer the proposer makes below the threshold is not seen. Therefore, even if the proposer knows the vetoer’s type, making different offers based on the vetoer’s type like in a RTE is useless. Offers are made at the threshold level unless the proposer sees no offer that both players would accept.

The expected cost of an TPE compared to an RTE is that if both players are low types, there is no longer a deal in period 1. In an RTE, for the same case, the deal of

6 Discussion

6.1 Brinkmanship Failure

Schelling (1981, p. 91, 105) states that limited war can also be a form of brinkmanship when it increases the risk of a major war. A prominent case where brinkmanship failed is President Nixon’s application of the “Madman Theory” to the Vietnam War. The “Madman Theory” was a game theory based approach. According to his chief of staff, H. R. Haldeman, Nixon said the following.

I call it the Madman Theory, Bob. I want the North Vietnamese to believe I’ve reached the point where I might do anything to stop the war. We’ll just slip the word to them that, ‘for God’s sake, you know Nixon is obsessed about Communism. We can’t restrain him when he’s angry–and he has his hand on the nuclear button’–and Ho Chi Minh himself will be in Paris in two days begging for peace.[14]

On Nixon, Defense Secretary Melvin Laird said “… he wanted adversaries to have the feeling that you could never put your finger on what he might do next.”

During the Vietnam War, the theory was applied by warning the North Vietnamese that if no major progress was made in the peace talks by November 1st of 1969, U.S. will be compelled to “take measures of the greatest consequence.” In October, the Soviet ambassador, Anatoly Dobrynin met with Nixon. Dobrynin reported to the Kremlin that Nixon said “he will never (Nixon twice emphasized that word) accept a humiliating defeat or humiliating terms.” Dobrynin warned the Soviets that “It was perfectly clear from the conversation with Nixon that events surrounding the Vietnam crisis now wholly preoccupy the U.S. President. … Apparently, this is taking on such an emotional coloration that Nixon is unable to control himself even in a conversation with a foreign ambassador.” In the same month, for three days, U.S. had nuclear-armed B-52s test the Soviet defenses, dancing around the edges of the country. However, these signals and actions did little to progress the peace talks.[15]

Putin’s actions during the Russian invasion of Ukraine such as the transfer of Nuclear weapons to Belarus have also been interpreted as an application of the “Madman Theory”. Also, like the Vietnam War, this war can also be seen as brinkmanship. Putin’s actions and this war have not lead to a deal in the war.[16]

As stated earlier, debt limit fights and government shutdown fights are common in the United States and for these fights if a deal is not reached, a disastrous effect on the U.S. economy takes place. Most of these fights end with a deal that only changes the status quo slightly.[17] For example, the 2018–2019 government shutdown was the longest in the U.S. Trump started it when Democrats refused to fund a wall along the U.S.-Mexico border. This shutdown ended in a deal that did not fund this wall.[18]

One case where a government shutdown initially seemed to have resulted in a deal that changes the status quo meaningfully is the 2011 debt ceiling deal. This deal established budget caps on how much the government can spend. It also created a “supercommittee” which was supposed to come up with a deficit reduction deal. As an incentive for the committee to come up with a deficit reduction deal, the debt ceiling deal stated that unless the deficit reduction deal is passed by congress, sequestration will happen where across-the-board spending cuts take place. These cuts were split evenly between domestic and defense programs and were disastrous for both parties.[19] The supercommittee failed to reach a deal. Sequestration was delayed and then it took place in March 2023. However, in the same year, a congressional deal succeeded in providing “sequester relief” which reduced the cuts. Also, the budget caps were repeatedly raised allowing the government to spend more money.[20]

Assuming that both parties are rational, the reason that brinkmanship fails may be explained by the basic model of this paper. In the RTE, once the vetoer succumbs to brinkmanship, the proposer realizes that the vetoer is “weak” (low type) and will succumb to brinkmanship again in the future. This leads to worse offers from the proposer in the future. Because of this, the vetoer who is not “weak” (medium or high type) rejects the brinkmanship offer.

If the party engaging in brinkmanship is irrational, brinkmanship will likely fail in reality. An irrational proposer may demand unrealistically too much from the vetoer. Also, an irrational proposer may not honor deals. In this case, the vetoer should not make concessions to get an unreliable deal.[21] Finally, if a proposer does not rationally consider deals, the vetoer should make nominal concessions instead of material concessions.

For some of the examples of brinkmanship I have listed, people who were subject to brinkmanship stated or hinted less rigorously similar reasons for not succumbing to brinkmanship.[22] For the Russian invasion of Ukraine, Ukrainian President Zelenskyy insinuated that making concessions for someone who repeatedly engages in brinkmanship or whose promise is unreliable will lead to bad outcomes.[23] During the 2018–2019 government shutdown, House Speaker Nancy Pelosi said that if Trump got what he wanted though the shutdown, he will continue to apply the strategy for future demands as well.[24]

In reality, a vetoer may be unsure whether the proposer is bluffing as Nixon was during the Vietnam war or will actually cause a disaster. If he is bluffing, the vetoer should not succumb to it since the disaster will not materialize. If he is not bluffing, the aforementioned reasons for not succumbing to brinkmanship still apply. So the vetoer should still not succumb.

6.2 Brinkmanship Success

Lemma 1 shows some necessary conditions for the existence of an RTE. From it, I deduce necessary conditions for the success of brinkmanship. First, early brinkmanship cannot be too unfavorable for the vetoer. In Lemma 1,

Russia was involved in the First and Second Chechen Wars, the Russo-Georgian War, the Syrian civil war and the Russian invasion of Crimea. From those wars, Russia and Putin may have learnt that the west is unwilling to risk its relationship with Russia by seriously confronting Russia. This may have lead to Russia’s involvement in more wars and the Russian invasion of Ukraine.[25] Russia seems to fulfill at least the first two necessary conditions for the success of brinkmanship. It is unclear whether the last condition is fulfilled. First, given the high costs of a breakdown in relationships or war with Russia, the west may have seen losses suffered by other nations to be acceptable. Second, the west may have placed more value on the long term benefits of a favorable relationship with Russia compared to the losses of other nations.[26]

While we do see cases where brinkmanship succeeds in reality, such cases seem rare and satisfying the necessary conditions for success like those in Lemma 1 seem difficult. Countries, political parties and firms and unions have long term relations they care about. Usually, they will be unwilling to accept the long term consequences of succumbing to brinkmanship. This unwillingness violates the second condition. The last condition means that the vetoer must believe that a better deal for the vetoer is likely to be unacceptable for the proposer. However, in many cases, the vetoer would know that this is false because going back to the status quo before the brinkmanship should be acceptable to both parties. For instance, in a limited war, it is hard to argue that nations would find going back to the status quo before the war unacceptable. For strikes, both the firm and the union are informed about inflation, cost of living, profitability and so on. Therefore, both sides know that a deal in line with these measures should be acceptable to both.

6.3 The Effect of Preconditions on Bargaining

Imposing preconditions on negotiations or the advance of negotiations happens frequently in reality. For instance, consider the Israel-Palestine peace negotiations during the Obama administration. In negotiating the renewal of direct talks with Israel, Palestinian President Mahmoud Abbas had many demands. He demanded a total Israeli settlement freeze. He asked that talks be based on the 1967 lines. He requested the release of 104 Palestinians. He was able to get some prisoners released in return for suspending the Palestinian campaign for U.N. During the ensuing peace talks, a Israeli representative insisted that Israel never place any map on the table till the security conditions were settled. Eventually, the talks failed.[27] During the Russian Invasion of Ukraine, Ukrainian President Zelenskyy announced that Russia must pull back its troops to where they were before the invasion ere negotiations resumed.[28]

TPEs demonstrate that sticking to preconditions (the threshold in the extended model) can increase the vetoer’s payoff and that preconditions can be an effective response to brinkmanship. Imposing preconditions is different from brinkmanship. When engaging in brinkmanship, the proposer is flexible. Based on whether the vetoer succumbs to brinkmanship, the proposer changes the subsequent offers. However, the vetoer who imposed preconditions never deviates from them. Therefore, not flexibility but steadfastness is required.

Furthermore, while a proposer engaging in brinkmanship makes an offer that may be unacceptable and has a risk of failure, a vetoer sets preconditions that she thinks are likely to be accepted. An acceptable precondition might be a return to the status quo. This is because walking away from brinkmanship is expected to happen frequently but that walking away from preconditions is not expected to happen. Since this vetoer will not try something different when the preconditions don’t work, she tries to set preconditions that will lead to a deal.

In the basic model, high cut-off points fail because if the vetoer examines all offers, the proposer is going to try the make the worst offer the vetoer will accept. Therefore, to have preconditions that are likely to work, the vetoer must commit to not examining any offer that does not meet the preconditions. This allows her to be steadfast in her preconditions. The vetoer must convince the proposer that this commitment is solid. Bargaining on the strictness of preconditions negates the commitment to the preconditions. In reality, commitment may involve refusing to talk about anything else and refusing to read documents until preconditions are agreed upon. Also, the vetoer could leave the negotiations to representatives who are the only people to talk to and who argue they are not allowed to negotiate preconditions.

7 Conclusion

In the basic model, I solved for two types of PBEs, the RTE and the RAE. In the RTE, the proposer engages in brinkmanship by making a low brinkmanship offer,

The extended model explains what the vetoer can do against the proposer and his first-mover advantage. It also explains what the vetoer can do against brinkmanship. The vetoer can negate the first-mover advantage by announcing preconditions for negotiation and sticking to the preconditions. In the extended model, such preconditions are modeled using a threshold, ψ. If the proposer makes an offer below the threshold, it is automatically rejected without being seen by the vetoer. In the TPE, vetoer sets a high threshold at the beginning of the game and does not change it. This leaves no room for brinkmanship. The TPE may raise the vetoer’s expected payoff. The TPE demonstrates that setting preconditions that the proposer can accept may reduce brinkmanship.

Appendix 1. Lemma and Proofs for Section 4

Only Lemma 1 is here. All other lemmas are in the Supplementary Material. Lemma 1 is used to prove Lemma 3. Lemma 2 is used to prove Lemma 3 and Proposition 1. Lemma 3 is used to prove Propositions 1 and 5. Lemma 4 is used to prove Propositions 1 and 3.

Proof of Lemma 1.

Using Definition 2, I can figure out how the game plays on the equilibrium path. The proposer offers

Suppose that the vetoer is low type and

If the vetoer rejects the period 1 offer, proposer believes b−L. If the proposer is high type, starting from period 2, the vetoer can get an utility of v H − v L by accepting v H which will not change the proposer’s belief. If the vetoer accepts the period 1 offer, proposer believes b L . Then, on the equilibrium path, vetoer’s utility for every period starting from period 2 is 0. Inequality (8) means that the vetoer prefers to deviate.■

Proposition 1 is used to prove Proposition 2. Lemma 5 is used to prove Lemma 6. Lemma 6 and 7 are used to prove Lemmas 8 and 9. Lemma 8 is used to prove Propositions 2 and 4. Lemma 9 is used to prove Proposition 2.

Proof of Proposition 1.

I will prove sufficiency first. In the RTE of the sufficiency proof, the proposer’s belief is formed the following way. Proposer can have 3 beliefs, b0, b

L

and b−L. His belief is initially b0. From b0, proposer’s belief can change to b

L

or b−L. Proposer’s belief can also change from b−L to b

L

. However, once the proposer believes b

L

, his belief is fixed. A proposer who believes b0 at the start of period t has the same belief at the start of period t + 1 if the vetoer accepts an offer a

t

≥ v

H

or rejects an offer

I will check whether the above specification is consistent with a PBE. For a proposer who believes b0, a

t

≥ v

H

will always be accepted and

For a proposer who believes b L , low type vetoer will accept a t ≥ v L and reject a t < v L . So when these happen, he can believe b L at the start of period t + 1. For a proposer who believes b−L, medium and high type vetoers will accept a t ≥ v H and reject a t < v H . So upon acceptance or rejection of a t ≥ v H , he can believe b−L at the start of period t + 1. Upon rejection of a t < v H , he can believe b−L at the start of period t + 1. Also, upon acceptance of a t < v H , he can believe b L at the start of period t + 1.

I will prove that the proposer’s strategy is optimal. Once the proposer believes b L or b−L, the only case in which the proposer changes his belief is from b−L to b L which is off the equilibrium path. Therefore, by Definition 2’s (v)∼(viii), low type proposer finds a t = v L optimal for any period t where he believes b L or b−L. Similarly, by Definition 2’s (v) and the fact that once the proposer believes b L , proposer’s belief is fixed, high type proposer finds a t = v L optimal for any period t where he believes b L . By Definition 2’s (vi) and (viii) and the aforementioned fact that the belief change is off the equilibrium path, high type proposer finds a t = v H optimal for any period t where he believes b−L.

Consider a proposer who believes b0 at the start of period t. In period t, any offer below

Suppose this proposer is low type. Proposer’s payoff from the RTE strategy with

If a

t

≥ v

H

, a

t

is accepted. However, the proposer’s utility for the period is less than 0. Proposer’s belief after veteor acts in this period is still b0. Proposer is better off offering

I will compare

Suppose the proposer is high type. If a

t

≥ v

H

, a

t

is accepted. Proposer’s belief remains the same at the start of period t + 1. This means from a

t

≥ v

H

, proposer prefers a

t

= v

H

. The proposer prefers a

t

= v

H

to

If

Consider a strategy where proposer plays only v

H

from period t till some period t′ > t. At period t′, proposer switches to

Weak inequality (9) means

This means proposer weakly prefers to switch at period t′ − 1 instead.

Now, I will prove that the vetoer’s strategy is optimal. By Definition 2, proposer never offers more than v H . High type vetoer’s utility is always 0 or less. A cut-off point of v H for the high type vetoer is optimal for all future periods. Given this, the cut-off point is also optimal for the current period.

If the proposer’s belief as he makes the offer is b L , proposer’s belief and offer will not change in the future. Therefore, low and medium type vetoer’s strategy is optimal when proposer’s belief as he made the offer was b L .

Suppose that in period t, the proposer’s belief as he makes the offer is b−L. I will solve for the low or medium type vetoer’s optimal strategy. If a t ≥ v H , proposer’s belief will be the same at the start of period t + 1, therefore, the vetoer’s strategy is optimal.

On the equilibrium path, low type proposer offers a t = v L and high type proposer offers a t = v H . Off the equilibrium path, if a t < v H and a t ≠ v L , vetoer can believe that the proposer is high type. Off the equilibrium path, if a t = v L , vetoer can believe that the proposer is low type.

Consider the above cases of vetoer’s beliefs about the proposer. According to his strategy in Definition 2, low type proposer who believes b−L will always offer b L in period t and the future. Low or medium type vetoer’s strategy is optimal when she believes the proposer to be low type. Consider the case where she believes the proposer to be high type. If she accepts a t < v H , proposer changes his belief to b L and offers v L in all subsequent periods. If she rejects a t < v H , proposer offers v H in all subsequent periods. When I apply Lemma 4 to (iii), I get the following.

In this case, the lower or medium type vetoer weakly prefers to reject a t < v H .

Suppose that in period t, the proposer’s belief as he makes the offer is b0. Consider the low or medium type vetoer’s optimal strategy. If the vetoer rejects

Therefore, the low type vetoer’s strategy is optimal. I will transform the above equation.

If

Note that the above inequality also holds when

Necessity is proven by Lemma 3.■

Proof of Proposition 2.

Since Proposition 1’s (iii) and (iv) are already satisfied, an RTE exists if and only if Proposition 1’s (i) and (ii) hold. I will start with Proposition 1’s (i).

By

Therefore, by the intermediate value theorem, there exists some

Now I will move on to Proposition 1’s (ii).

If

In this case, by the intermediate value theorem, there exists some

Lemma 10 is used to prove Lemma 11 and Proposition 3. Lemma 11 is used to prove Propositions 3 and 5. Proposition 3 is used to prove Proposition 4.

Proof of Proposition 3.

I will prove sufficiency first. In the RAE for the sufficiency proof, the proposer’s belief is formed the following way. The proposer can have 3 beliefs, b0, b L and b−L. Proposer initially believes b0. A proposer who believes b0 can switch his belief to b L or b−L. A proposer who believes b−L can change his belief to b L . However, once a proposer believes b L , his belief will never change. Consider a proposer who believes b0 at the beginning of period t. If the vetoer accepts or rejects a t ≥ v H , proposer does not change his belief. Also, if the vetoer rejects a t < v L , proposer does not change his belief. If the vetoer accepts a t < v H , proposer changes his belief to b L . If the vetoer rejects a t ∈ [v L , v H ), proposer changes his belief to b−L. A proposer who believes b−L at the start of period t changes his belief to b L if a t < v H is accepted. Otherwise, his belief is the same at the beginning of period t + 1.

I will check whether the above specification is consistent with an RAE. For a proposer who believes b0 at the start of period t, a t ≥ v H will always be accepted and a t < v L will always be rejected. So these do not change his belief. No vetoer type will reject a t ≥ v H in period t. Upon such rejection, proposer can keep his belief. a t < v L will not be accepted by any type of vetoer. So upon such acceptance, the proposer can believe b L at the start of period t + 1. a t ∈ [v L , v H ) will only be rejected by the medium and high types. So upon such rejection, the proposer can believe b−L at the start of period t + 1. If it is accepted, he can believe b L at the start of period t + 1.

Consider a proposer who believes b L at the start of period t. Low type vetoer will accept a t ≥ v L and reject a t < v L . So when these happen, proposer can keep his beliefs. Low type vetoer does not reject a t ≥ v L nor accept a t < v L . When these happen, proposer can believe b L at the start of period t + 1.

Consider a proposer who believes b−L at the start of period t. Medium and high type vetoers will accept a t ≥ v H and reject a t < v H . So when these happen, proposer can keep his beliefs. Medium and high type vetoers do not reject a t ≥ v H . When such rejection happens, proposer can believe b−L at the start of period t + 1. Medium and high type vetoers do not accept a t < v H . When such acceptance happens, proposer can believe b L at the start of period t + 1.

Now, I will prove the proposer’s optimality. Consider a low type proposer who believes b0 or b L , he can never get a positive utility from medium type or high type vetoers. From the low type vetoer, his maximum utility is p L − v L . By offering v L every period, he can get the maximum utility every period from her. A low type proposer who believes b−L can never get positive utility. Therefore, his strategy is optimal.

Consider a high type proposer who believes b L at the beginning of period t. The proposer’s belief will not change in the future. If the proposer believes b L , offering v L from now on is optimal. If the high type proposer instead believes b−L at the beginning of period t, he believes that a t < v H will be rejected. For him, offering v H from now on is optimal.

Suppose the high type proposer believes b0 at the beginning of period t. Any offer below v L will be rejected and any offer satisfying a t ≥ v H will be accepted. Such offers do not change the proposer’s belief. Therefore, from those offers, proposer weakly prefers v H . Any offer a t ∈ [v L , v H ) will be accepted by the low type vetoer and rejected by the medium and high type vetoers. From a t ∈ [v L , v H ), proposer weakly prefers a t = v L . I will compare the remaining options, a t = v H and a t = v L . I can apply Lemma 10 to (i).

If a t = v L is accepted, proposer believes b L . If it is rejected, proposer believes b−L. At period t, proposer weakly prefers a t = v H to a t = v L .

Next, I will prove the high type vetoer’s optimality. By the proposer’s strategy, his utility is always 0 or less. A cut-off point of v H for all future periods gives him 0 utility for all future periods. Given this, a cut-off point of v H is also optimal for the current period.

Moving on, I will prove the low or medium type vetoer’s optimality. If the proposer believes b L , his belief will not change. Therefore, the vetoer’s strategy for this case is optimal.

Suppose the proposer believes b−L or b0. If the proposer offers a t = v L , the vetoer can believe that the proposer is low type. In this case, the vetoer’s strategy is optimal because a low type proposer will always offer v L in future periods.

If the proposer offers a t ∈ R1 − {v L }, the vetoer can believe that the proposer is high type. Vetoer finds it optimal to accept a t ≥ v H in this case. Applying Lemma 4 to (ii) gives the following.

If the veteor accepts a t < v H , she will only be offered v L after period t. If the vetoer rejects a t < v H , she can get v H − S V in all future periods. Vetoer’s strategy is optimal.

Necessity is proven by Lemma 11.■

Proof of Proposition 4.

Apply Proposition 3. An RAE exists if and only if the following holds.

By Lemma 8’s (1),

Therefore, there exists some η for which formula (10) holds. By Lemma 8’s (2),

Therefore, there exists some η for which formula (10) doesn’t hold. The intermediate value theorem completes the proof.■

Proof of Proposition 5.

Suppose an RTE exists. I start by combining Lemma 3’s (1) and (2).

However, this means that the necessary condition for Lemma 11 does not hold.■

Proof of Proposition 6.

I will use proof by contradiction. Suppose that I am at the PBE.

In any period where the proposer’s belief is b0 as he acts, vetoer rejects any offer below

If

Let aH,t be the high type proposer’s period t offer. If

Suppose

Suppose

I define the set, {p

t

|t ≥ 1}. By the least-upper-bound property, this set has an infimum, which I will call

For any ɛ > 0, there exists some t such that

Appendix 2. Proof for Section 5

Proof of Proposition 7.

For this proof ψ t is the value of ψ in period t after the vetoer has had a change to change ψ at the beginning of the period. I will start by describing the proposer’s beliefs in the TPE. Proposer’s belief is either b0 or b L . If the proposer believes b0, his belief can change to b L . However, once the proposer believes b L , his belief never changes. When players receive their private information, proposer’s belief is b0. If the proposer observes ψ ≠ p H as he decides his offer, proposer’s belief then and afterwards is b L . This is the only case where the proposer’s belief changes.

I will check that the proposer’s belief is consistent with a PBE. If the proposer believes b L , since he believes that the vetoer’s type is low type with probability 1. His belief can always remain the same in the future.

Suppose ψ t = p H . This means that the vetoer set ψ = p H at the start of the game and never changed it so the vetoer did not deviate for these decisions. For any period before t, if the vetoer did not observe the offer, the vetoer did not accept or reject the offer. If the vetoer observed the offer, the offer was p H or greater. If this offer is accepted, the vetoer did not deviate for this action. If this offer is rejected, the vetoer did deviate for this action and the proposer can keep his belief in this period at the next period. Therefore, if ψ t = p H , the proposer can have his original belief from the start of the game, b0, as he acts in period t.

Suppose ψ1 ≠ p H . This means that the vetoer deviated at period 1 or before. In either case, proposer can believe b L as he acts in period 1. Suppose, for some t ≥ 2, ψ t ≠ p H and ψ t ≠ −∞. Then, ψ1 ≠ p H . Suppose, for some t ≥ 2, ψ t = −∞. If ψ1 = p H , that means that the vetoer deviated at the beginning of some period t′ < t. In this case, the proposer can believe b L in period t′.

Now, I will prove the proposer’s optimality. If the proposer believes b0 as he acts in period t, that means ψ t = p H . For proposer of any type, his maximum utility in period t or any period after is 0. Therefore, Definition 4’s (i) is optimal.

If the proposer believes b L as he acts in period t, ψ t ≠ p H . Proposer believes any offer a t ≥ max{v L , ψ t } will be accepted and any offer a t < max{v L , ψ t } will be rejected or not seen. Therefore, when S P < ψ t , ψ t − 1 is optimal and when S P ≥ ψ t , a t = max{v L , ψ t } is optimal.

I move on to the vetoer’s optimality. If a vetoer of any type follows the strategy in Definition 4, her expected payoff is positive. If a vetoer of any type sets ψ > p H at the start of the game, her expected payoff is non-positive. If ψ t ≤ p L , a t = max{v L , ψ t }. Therefore, if the vetoer sets ψ ≤ p L at the start of the game, she weakly prefers to never change it. Also, from ψ ≤ p L , she weakly prefers to set ψ = p L at the start of the game.

Suppose that ψ never changes in any period. Then, setting ψ = p L at the start of the game gives the medium and high type vetoers non-positive expected utility. I will compare setting ψ = p H to ψ = p L at the start of the game for the low type vetoer. The low type vetoer’s payoff from the former is

The low type vetoer’s payoff from the latter is

Formula (6) means that the vetoer weakly prefers ψ = p H to ψ = p L at the start of the game. If the formula is violated, at the start of the game, the low type vetoer prefers to set ψ = p L and never change it.

Suppose the vetoer sets ψ ∈ (p L , p H ] at the start of the game. If the vetoer follows Definition 4’s (iv) and does not change ψ, the expected utility is non-negative in every period. Therefore, the vetoer weakly prefers to not change ψ. If the vetoer does not change ψ, high type proposer will offer ψ in every period and low type proposer will offer ψ − 1 every period. If the vetoer never changes ψ ∈ (p L , p H ] that is set at the start of the game, vetoer weakly prefers ψ = p H .

Finally, in period t, for a given ψ t , Definition 4’s (iv) is optimal. This is because by Definition 4’s (i), vetoer’s acceptance or rejection does not affect how the proposer will play in the future.■

References

Acharya, Avidit, and Edoardo Grillo. 2015. “War with Crazy Types.” Political Science Research and Methods 3 (2): 281–307. https://doi.org/10.1017/psrm.2014.23.Search in Google Scholar

Ali, S. Nageeb, Navin Kartik, and Andreas Kleiner. 2023. “Sequential Veto Bargaining with Incomplete Information.” Econometrica 91 (4): 1527–62. https://doi.org/10.3982/ecta20658.Search in Google Scholar

Asselin, Pierre. 2002. A Bitter Peace: Washington, Hanoi, and the Making of the Paris Agreement. The University of North Carolina Press.Search in Google Scholar

Barrett, Ted, Dana Bash, Kate Bolduan, Annalyn Censky, Tom Cohen, Candy Crowley, et al.. 2011. “Debt Ceiling: Timeline of Deal’s Development.” CNN (August 2, 2011). http://www.cnn.com/2011/POLITICS/07/25/debt.talks.timeline/index.html (accessed May 13, 2024).Search in Google Scholar

Ben, Birnbaum, and Amir Tibon. 2014. “The Explosive, Inside Story of How John Kerry Built an Israel-Palestine Peace Plan – and Watched it Crumble.” The New Republic (July 20, 2014). https://newrepublic.com/article/118751/how-israel-palestine-peace-deal-died (accessed February 5, 2024).Search in Google Scholar

Bresnahan, John, and Jake Sherman. 2013. “Budget Agreement Reached.” POLITICO (December 10, 2013). https://www.politico.com/story/2013/12/budget-deal-update-patty-murray-paul-ryan-100960 (accessed May 13, 2024).Search in Google Scholar

Bresnahan, John, Jennifer Scholtes, and Caitlin Emma. 2019. “Sweeping Budget Deal Passes House Despite Weak GOP Support.” POLITICO (July 25, 2019). https://www.politico.com/story/2019/07/25/house-gop-budget-vote-1433848 (accessed May 13, 2024).Search in Google Scholar

Cadelago, Christopher. 2018. “Trump Owns the Shutdown. And He’s OK with that.” POLITICO (December 23, 2018). https://www.politico.com/story/2018/12/23/government-shutdown-2018-trump-white-house-1074565 (accessed May 11, 2024).Search in Google Scholar

Calabuig, Vicente, and Gonzalo Olcina. 2000. “Commitment and Strikes in Wage Bargaining.” Labour Economics 7 (3): 349–72. https://doi.org/10.1016/s0927-5371(00)00002-6.Search in Google Scholar

Cameron, Charles M. 2000. Veto Bargaining: Presidents and the Politics of Negative Power. Cambridge University Press.10.1017/CBO9780511613302Search in Google Scholar

Chambers, Francesca, and Zac Anderson. 2025. “Donald Trump Revives ‘Tough’ Approach to Iran, Warns against Nuclear Weapon.” USA Today (February 4, 2025). https://www.usatoday.com/story/news/politics/2025/02/04/donald-trump-taking-aggressive-approach-iran/77557208007/ (accessed July 27, 2025).Search in Google Scholar

Cheung, Francis K., and Carl Davidson. 1991. “Bargaining Structure and Strike Activity.” Canadian Journal of Economics: 345–71. https://doi.org/10.2307/135627.Search in Google Scholar

Cuellar, Pablo, and Lucas Rentschler. 2023. Threat, Commitment, and Brinkmanship in Adversarial Bargaining. Working Paper.Search in Google Scholar

Detsch, Jack, and Robbie Gramer. 2024. “Russia’s Nuclear Weapons are Now in Belarus.” Foreign Policy (March 14, 2024). https://foreignpolicy.com/2024/03/14/russia-nuclear-weapons-belarus-putin/ (accessed May 13, 2024).Search in Google Scholar