Capital Account Liberalization, Structural Change, and Female Employment

-

Selin Secil Akin

and

Juan Antonio Montecino

and

Juan Antonio Montecino

Abstract

This paper studies the effects of capital account liberalization on female employment and its implications for structural change in developing countries. Using a large industry-level panel of 88 low and low-middle-income countries, we provide evidence that episodes of financial liberalization lead to large declines in female employment in tradable sectors. These declines are driven primarily by structural reallocation effects between sectors, although we also find modest changes in the gender composition of employment within sectors, depending on the sample definition. Based on this evidence, we build a stylized model of a small open economy with tradable and nontradable sectors featuring occupational segregation across genders. We use this framework to study the impact of capital inflows and the female wage penalty on female employment in tradables and the real exchange rate. Our model also implies that when the female burden of non-market home production is sufficiently large, capital inflows will disproportionately hurt female employment relative to male employment.

1 Introduction

Once nearly universally prescribed as a pro-development structural reform, in recent years policymakers and academics have adopted a more cautious stance towards capital account liberalization and began reconsidering the potential benefits of financial globalization. This reconsideration has taken place in the wake of the global financial crisis of 2008–2009 and amidst mounting evidence that unrestricted capital flows are destabilizing, exacerbate inequality, and can promote undesirable forms of structural change.[1] In this paper we ask: what are the gender implications of financial globalization and how do these interact with structural change in a developing country setting?

A growing literature has examined the gendered dimensions of globalization and macroeconomic policies. While this literature is diverse, the emerging consensus is that globalization and macroeconomic policies typically are not gender neutral (Braunstein and Heintz 2008; Seguino 2020; Seguino and Heintz 2012). Previous empirical papers on the gendered impact of globalization have mostly focused on the effects of trade liberalization (Domínguez-Villalobos and Brown-Grossman 2010; Wamboye and Seguino 2015), foreign direct investment (Braunstein and Brenner 2007), and open economy considerations such as real exchange rate undervaluation (Erten and Metzger 2019). By comparison, empirical work on the gender dimensions of financial liberalization remains sparse.

This paper studies the differential effects of financial liberalization policies on female employment from both an empirical and theoretical perspective. On the empirical front, we use a large panel of industry-level data in 88 developing countries for the period 1991–2019. Our empirical strategy exploits differential exposure across sectors to a financial liberalization episode in order to estimate the aggregate effect on female employment. We estimate the dynamic effects of financial liberalization using the local projection approach of Jorda (2005) and restrict our attention to episodes featuring large changes in measured capital account regulations.

We focus on country variation across industries for several reasons. First, female employment is concentrated differentially across industrial sectors.[2] Second, financial liberalization likely has heterogeneous effects across industries depending, for example, on the relative capital intensity of an industry or whether the goods produced can be traded on the world market. It follows that financial liberalization, by affecting the gender composition of employment within sectors and altering the structure of economic activity between sectors, can have distributional implications for female employment.

We find evidence that financial liberalization leads to large declines in female employment in tradable sectors and this effect is driven by two channels. The first channel is a between sector factor reallocation effect. Liberalization squeezes overall tradable employment, which consequently decreases female employment in tradable industries. Second, liberalization also decreases female employment through a within sector change in the gender composition of employment, which reduces the female intensity of tradable sectors.

Our results suggest that on average the sectoral reallocation channel explains most of the negative effect on female employment. Put differently, the key driver of the female employment response is structural change between tradable and nontradable industries. However, we also find evidence that the within sector gender composition effect may be stronger depending on a country’s level of development and how tradable industries are defined. For example, changes in female intensity also quantitatively drive the results for manufacturing sectors and in low income countries.[3]

Motivated by these empirical results, we build a simple two-sector gender disaggregated model with tradable and nontradable goods. The model is therefore in the tradition of the textbook “dependent economy” model of Salter (1959) and Swan (1963) featuring female and male workers. Consistent with our benchmark empirical results, the female employment share is constant in each sector, which we interpret as a strong form of occupational segregation between genders. The small open economy and two-sector structure is appropriate in our setting because it captures the characteristics of a developing country and can explain how changes in capital inflows – due to liberalization – can shift the economy’s sectoral structure.

We present two versions of our model: a benchmark model with fixed labor supply, and an extended version with endogenous labor supply. The findings of our benchmark model show that capital inflows lead to an appreciation of the real exchange rate (RER), expansion of the nontradable sector, and shrinking of the tradable sector. This implies that female employment in tradables decreases. In addition, when the female intensity in the tradable sector is higher than the female intensity in the nontradable sector, a decrease in the gender wage gap leads to a depreciation of the RER and a decrease in female employment in tradables.

In the extended model, household members divide their labor between paid work and the production of home goods. A key feature of this extension is that female household members disproportionately bear the burden of home production, with implications for relative employment across genders in general equilibrium. We show that when women’s burden of home production is sufficiently large, capital inflows will disproportionately hurt female employment relative to male employment. The extended model thus predicts that an overvalued RER will be associated with a decline in the female to male employment ratio. By the same token, a competitive RER undervaluation should coincide with a relative increase in female employment.

The remainder of the paper is structured as follows. Section 2 presents the data employed in the empirical exercise and presents some stylized facts on the female intensity of employment across industries. Section 3 describes the empirical exercise and its results. Section 4 presents our benchmark two-sector model and derives several results on the impact of capital account liberalization in general equilibrium. Finally, Section 5 presents an extension of the model featuring endogenous labor supply and home production.

2 Data

Our empirical strategy exploits differential exposure between tradable and nontradable sectors to a financial liberalization episode in order to estimate the aggregate effect on the female employment in tradable sectors. We have compiled annual data on employment obtained from the ILO. The employment levels are disaggregated by gender and sector, making it possible to construct a country-sector-year panel for 14 industrial sectors and 88 low and low-middle income countries over the years 1991–2019.

In order to identify a financial liberalization shock, we adopt the approach proposed by Furceri et al. (2019), which entails looking for large changes in the de jure capital account openness index of Chinn and Ito (2006). Specifically, we define a liberalization episode as a year in which the openness index increases by more than 2 standard deviations. This approach has two main advantages. First, relying on a de jure index of openness – as opposed to a de facto index based on observed capital flows – allows us to measure changes in actual policy. Second, focusing on large changes in the openness index allows us to rule out cyclical change in capital account regulation that may be correlated with macroeconomic conditions and increases the likelihood of only measuring structural policy changes. Together, these two points imply that reverse causality is unlikely in our empirical setting.

To capture the differential exposure of tradable and nontradable industries, we use the tradability index developed by Bykova and Stöllinger (2017). They present two index variables, which are continuous measures of sectors’ tradability: the VAX based measure (TSVAX) and the TS based measure on gross exports (TSX). The TSVAX measure is the ratio of the industry-level value added exports and the industry-level value added. Both components are summed over time and countries. The TSX measure is the ratio of gross exports in each sector divided by the value added in each sector. Similarly, this measure also uses aggregate components by time and country. Sectors’ rankings are similar for both measurements. As suggested by Bykova and Stollinger, we use the VAX-based tradability score. It is methodologically preferable because exports are also calculated with a value-added based measurement. In TSX measure, trade flows are double counted to account for crossing border more than once. In the first measure (VAX-based) this double counting is corrected. We use the time-invariant index in our main specifications but we also employ the time-varying index variable as a robustness check. The reason why we prefer the time-invariant version is that even though the tradability increases over time, the tradability ranking of the sectors does not change (Bykova and Stöllinger 2017).

The remaining variables used in the analysis come from a variety of sources. Data on real GDP per capita is from the Penn World Tables. We obtained the current account balance from the IMF World Economic Outlook.

2.1 Female Employment Intensity Across Industries

Before turning to the empirical analysis, we begin with stylized facts on the female intensity of employment across sectors. Table 1 presents the average female employment shares by countries’ income level and six broadly defined industrial sectors. We sort sectors by their tradability. Overall, female intensity is the highest in the public sector. However, female intensity in different sectors also varies by development level. While agriculture is the most female intensive sector in low income countries, the public sector has the highest female employment share in the rest of the country groups.

Average female employment shares by income and sectors.

| Income group | L | LM | UM | H | Total |

|---|---|---|---|---|---|

| Tradability | |||||

| (from the most tradable to the least tradable) | |||||

| MAN | 0.39 | 0.398 | 0.357 | 0.275 | 0.36 |

| MEL | 0.178 | 0.153 | 0.152 | 0.165 | 0.162 |

| AGR | 0.435 | 0.315 | 0.267 | 0.256 | 0.326 |

| MKT | 0.414 | 0.369 | 0.371 | 0.397 | 0.388 |

| PUB | 0.375 | 0.487 | 0.542 | 0.604 | 0.494 |

| CON | 0.069 | 0.053 | 0.061 | 0.078 | 0.065 |

|

|

|||||

| Tradable | 0.33 | 0.29 | 0.26 | 0.23 | 0.28 |

| Nontradable | 0.29 | 0.30 | 0.32 | 0.36 | 0.31 |

|

|

|||||

| Total | 0.31 | 0.296 | 0.292 | 0.296 | 0.30 |

-

Note: Economic activity codes: AGR, agriculture; CON, construction; MAN, manufacturing; MEL, mining and quarrying; electricity, gas and water supply; MKT, market services; PUB, non-market services. World Bank country classifications by income level: L, low income; LM, lower-middle income; UM, upper-middle income; H, high income.

The second part of Table 1 presents the average female employment shares in tradable and nontradable sectors. In the econometric specifications, our tradability variable is a continuous variable. However, by using the value added tradability score index (TSVAX) by Bykova and Stöllinger (2017), we classify sectors that have higher tradability score than 0.15 as tradable sectors, and the rest as the nontradable sectors. In Table 1, the first three sectors belong to tradable sectors, and the rest are nontradable sectors. Low income countries also have different pattern than the rest when we look at the average female intensity in tradable and nontradable sectors. While female intensity is higher in tradable sectors in low income countries, overall nontradable sectors are more female intensive for the rest of the countries.

Figure 1 shows the conditional means of female employment shares in different income groups in tradable sectors. Two salient features emerge from the figure. First, female intensity in tradable sectors is the highest in low income countries and lowest in high income countries. Second, female intensity is remarkably constant throughout the sample.

Average female employment shares in tradables by income group. World Bank country classifications by income level: L, low income; LM, lower-middle income; UM, upper-middle income; H, high income.

3 Empirical Exercise

We begin by examining the effect of financial liberalization on female employment. To this end, we estimate the following local projection:

Here Δ h Y ijt = ln Y ijt+h − ln Y ijt−1 refers to the cumulative log difference in our outcome variable of interest Y ijt , female employment in income group i and sector j at time t, between periods t − 1 and t + h. The differential exposure of sector j to a liberalization episode is captured by the interaction term LIB it × TI j , where LIB it is a dummy variable indicating the occurrence of an episode in country i at time t, and TI j measures the tradability of sector j’s output. Our main coefficient of interest is β h , which measures the cumulative impulse response h periods after exposure to a financial liberalization episode. The vector X ijt includes lags of the dependent and independent variables, the logarithm of real per capita income, and total sector employment.

Our results suggest that female employment significantly contracts in relatively tradable sectors following a liberalization episode. This can be seen in Figure 2, which depicts the cumulative impulse response

Impulse response of female employment

3.1 Alternative Specifications

Given the large effects reported above, we subject our results to a series of robustness exercises, as reported in Table 2. These include specifications with country-specific time trends (column 2), sector-specific time trends (columns 3 and 6), and additional control variables (columns 4–6). The latter consist of the logarithm of population, in order to account for country level trends in labor supply, financial openness and the current account balance as a percent of GDP, to control for the level of capital account openness and capital flows around a liberalization episode. We also allow for sector heterogeneity in the control variables by interacting the controls with sector dummies (columns 5–6). The large and persistent negative effect on female employment is present and significant in most specifications, though the exact magnitude varies, ranging from a lower bound of 12 % to an upper bound of 30 % after 8 years.

Female employment after 8 years (h = 8).

| Dependent variable: female employment

|

||||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

| LIB it × TI j | −0.282*** | −0.260*** | −0.116** | −0.301*** | −0.183*** | −0.142** |

| (0.0522) | (0.0491) | (0.0519) | (0.0552) | (0.0562) | (0.0556) | |

|

|

||||||

| Observations | 20,899 | 20,899 | 20,899 | 20,031 | 20,031 | 20,031 |

| R 2 | 0.059 | 0.151 | 0.126 | 0.080 | 0.150 | 0.162 |

|

|

||||||

| Year FE | Yes | No | No | Yes | Yes | No |

| Country trend | No | Yes | No | No | No | No |

| Sector trend | No | No | Yes | No | No | Yes |

| Additional controls | No | No | No | Yes | Yes | Yes |

| Sector controls | No | No | No | No | Yes | Yes |

-

Note: This table reports the impulse response function for female employment 8 years after exposure to financial liberalization (LIB it × TI j ). Every specification includes L = 3 lags of the control variables. Year FE refers to the inclusion of year dummies. Country trend refers to a country-specific time trend, while sector trend refers to specifications including a sector-specific time trend. Additional controls include the logarithm of country i population, the level of KAOPEN it , and the current account balance as a percent of GDP. Sector controls refers to specifications where the additional controls have been interacted with sector dummies. Heteroskedasticity and autocorrelation consistent (HAC) standard errors are reported in parenthesis. (*** p<0.01, ** p<0.05, * p<0.1).

3.2 Within and Between Sector Decomposition

We now dig deeper and decompose the overall effect on female employment into the contribution of within sector changes in the female intensity of employment and the contribution of employment reallocation between sectors. Let

Equation (2) simply states that the cumulative change in female employment

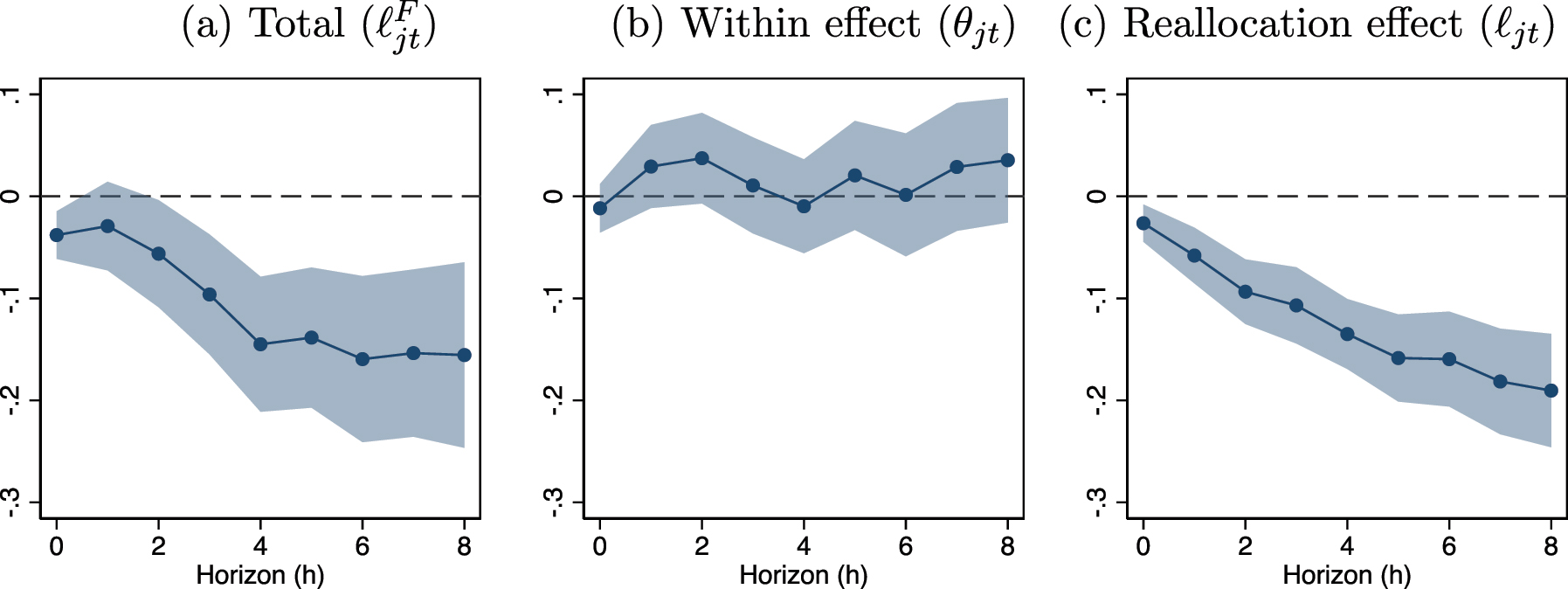

The benchmark decomposition results are reported in Figure 3. As a reference, panel (a) reports the overall effect already discussed above. The contributions of the within sector and reallocation terms are shown in panels (b) and (c), respectively. Consistent with equation (2), at each horizon the impulse responses in panels (b) and (c) must sum to the overall impulse response in panel (a).

Decomposition of female employment effect. Note: This figure reports the impulse response of female employment to sectoral exposure to a liberalization episode (LIB i × TI j ). Panel (a) reports the overall cumulative response for total female employment in sector j. Panels (b) and (c) decompose the total response into the contribution of changes in the female employment intensity within a sector and the contribution of sectoral employment reallocation. The shaded areas depict the 95 % confidence interval, which were calculated with heteroskedasticity and autocorrelation consistent (HAC) standard errors.

Perhaps surprisingly, the large effect on overall female employment appears to be primarily driven by sector reallocation effects (panel c). In contrast, the within sector effects on the female intensity of employment (panel b) are modest and statistically insignificant at most time horizons. These results are consistent with a strong form of gender segregation in tradable industries and suggest that the aggregate response of female employment to capital account liberalization is mostly due to resulting structural change, as opposed to changes in the gender composition of employment within sectors.

3.3 Sensitivity to Tradability Measure

Because the definition of tradability plays a central role in the results described above, we carry out a series of sensitivity tests using alternative tradability indexes and sectoral classifications. Specifically, we estimate the same specification as in Figure 3 but replace our exposure variable. These are reported in Table 3. Row (a) reports the overall effect on female employment 4 years after a liberalization episode, while rows (b) and (c) report the within and reallocation components, respectively. Columns (1)–(2) reports results with continuous tradability indexes. The first is our benchmark specification (column 1), which considers a time invariant tradability index. Column (2) reports the results using a time-varying measure of tradability. Next, columns (3)–(4) consider binary sector classifications. In column (3) we define the tradable sector as consisting of agriculture, manufacturing, and mining, while in column (4) we define the tradable sector as consisting of only manufacturing.

Sensitivity of decomposition to alternative tradability measures.

| Tradability index | Binary classification | |||

|---|---|---|---|---|

| Constant | Dynamic | Trad | Manuf | |

| (1) | (2) | (3) | (4) | |

| (a) Female employment

|

−0.123*** | −0.162** | −0.065*** | −0.140*** |

| (0.039) | (0.064) | (0.021) | (0.015) | |

| of which: | ||||

| (b) Within (Δ h θ jt ) | −0.031 | −0.058 | −0.010 | −0.056*** |

| (0.024) | (0.036) | (0.015) | (0.011) | |

| (c) Reallocation (Δ h ℓ ijt ) | −0.091*** | −0.104*** | −0.055*** | −0.084*** |

| (0.018) | (0.035) | (0.007) | (0.015) | |

-

Note: This table decomposes the impulse response of female employment 4 years (h = 4) after exposure to a liberalization episode. Line (a) reports the cumulative effect on overall female employment. Lines (b) and (c) decompose the overall effect into the within sector effect on female intensity and the reallocation effect, respectively. Constant and Dynamic refer, respectively, to specifications with time-invariant and time-varying tradability indexes. Trad defines the tradable sector as consisting of agriculture, manufacturing, and mining. Manuf defines the tradable sector as only consisting of manufacturing. All specifications include time fixed effects and L = 2 lags of the control variables. Heteroskedasticity and autocorrelation consistent (HAC) standard errors are reported in parenthesis. (*** p<0.01, ** p<0.05, * p<0.1).

As reported in Table 3, the decomposition results are similar regardless of which tradability measure is employed. The reallocation effect in row (c) dwarfs the within sector composition effect across most specifications. The exception is when manufacturing is treated as the sole tradable sector. As can be seen in column (4), in this case the contributions of within sector changes in female intensity are sizable and statistically significant.

3.4 Income Group Heterogeneity

As an additional sensitivity exercise, we now present the decomposition results for alternative samples depending on a country’s level of development at the beginning of the sample period. This allows us to check if structural differences between the poorest and the rest of the countries in the sample entail qualitatively different results. In particular, we carry out separate decompositions for countries classified as “low-middle income” and the poorest “low income” and report the cumulative impulse response of each decomposition component 8 years after exposure to a liberalization shock.[4]

The results are as follows. As can be seen in column (1) of Table 4, on average, the decline in female employment is primarily driven by the between sector employment reallocation effect (line c). However, breaking up the sample reveals meaningful heterogeneity between low-middle income (column 2) and the poorest low income (column 3) countries. While the reallocation effect is the driving force for low-middle income countries, changes in within sector female intensity appear to matter much more for low income countries. Indeed, in low income countries the within sector effect is nearly three times as large as the reallocation effect and statistically significant. The overall effect on female employment is also larger for low income countries, with female employment declining nearly 40 % in tradable sectors 8 years after a financial liberalization shock.

Income group heterogeneity.

| Sample: | Baseline | Low-middle | Low |

|---|---|---|---|

| (1) | (2) | (3) | |

| (a) Female employment

|

−0.239*** | −0.156*** | −0.382*** |

| (0.057) | (0.052) | (0.088) | |

| of which: | |||

| (b) Within (Δ h θ jt ) | −0.076** | 0.035 | −0.271*** |

| (0.034) | (0.030) | (0.082) | |

| (c) Reallocation (Δ h ℓ ijt ) | −0.162*** | −0.190*** | −0.104* |

| (0.039) | (0.028) | (0.060) |

-

Note: This table presents decomposition results for alternative country samples 8 years (h = 8) after exposure to a liberalization shock. The “Baseline” results (column 1) coincides with the sample and specification reported in Figure 3 and includes countries classified as both “low income” and “low-middle income.” Columns (2) and (3) restrict the samples, respectively, to countries classified as “low-middle income” and “low income.” Line (a) reports the cumulative effect on overall female employment. Lines (b) and (c) decompose the overall effect into the within sector effect on female intensity and the reallocation effect, respectively. All specifications include time fixed effects and L = 2 lags of the control variables. Heteroskedasticity and autocorrelation consistent (HAC) standard errors are reported in parenthesis. (*** p<0.01, ** p<0.05, * p<0.1).

4 The Model

Motivated by our empirical evidence, we now build a simple two-sector gender disaggregated model with tradable and nontradable goods. The model is in the tradition of Salter (1959) and Swan (1963)’s “dependent economy” model extended to feature female and male workers. The purpose of this theoretical exercise is twofold. The first is to provide a consistent framework through which to interpret and explain our empirical results. Thus, we will use the model to show how capital account liberalization can lead to a decline in female employment in the tradable sector through sectoral reallocation effects, holding constant the female intensity of employment within sectors.[5] The second objective is to shed light on other outstanding questions not directly examined in our empirics – e.g. due to a lack of data availability – and to contextualize our results in broader debates, such as the macroeconomic effects of the female wage penalty or the link between capital flows and the aggregate female employment gap in the presence of gendered care work.

Formally, the economy consists of two sectors: the tradable sector and the nontradable sector. Women and men are employed in both sectors but female intensity might be different in each sector. In line with our bencmark results discussed above, the female employment share in each sector (

In the dependent economy model, the terms of trade are exogenous and constant. The tradable sector includes both exportables and importables. In the small economy, the world demand for exportables and the supply for importables are elastic. The price of tradable goods, p T , is exogenous and determined by global factors. In contrast, the price of nontradable goods, p N , is endogenous and determined by local factors. We define the real exchange rate as the relative price of nontradable goods to tradable goods:

Therefore, an increase in q represents an appreciation of the real exchange rate.

4.1 Household Problem

We first present the simple version of our model. In this version, labor supply is fixed and we ignore home production. In the extended version, we will relax the assumption of fixed labor supply and consider unpaid care/household work. We consider a classical economy with full employment:

where

Households are identical in our model and choose to maximize their utility subject to their budget constraint. Households have Cobb–Douglas preferences defined over both goods:

where α ∈ (0, 1). Households earn wages from working and profits from the firms. They face the following budget constraint:

where

As is standard in two-sector models, the optimality condition is given by:

which states that the representative household equates the marginal rate of substitution to the relative price of nontradable goods.

4.2 Firms

Labor is the only factor of production in both sectors. Nontradable and tradable sectors have different production technologies. In the nontradable sector, the production technology is constant returns to scale and the production function can be expressed as

where

where the optimal solution is such that price is a weighted average of female and male wages in the nontradable sector:

The tradable sector’s production technology is decreasing returns to scale and in the following form:

where A > 0 is a productivity shifter, and

The solution gives us the optimal demand for labor, which equalizes the marginal product of labor to the weighted average of wages in the tradable sector,

Perfect labor mobility between sectors implies that a given gender will earn the same wage across sectors. However, wages between genders need not equalize in equilibrium due to the presence of strict occupational segregation. We assume that women have a wage penalty and are paid as a proportion (η < 1) of the male wage. Using this parameter, we can redefine female wages in terms of male wages:

4.3 Aggregate Constraints

To find the economy’s aggregate constraints, we rewrite the budget constraint (6) as follows:

where we made use of the definition of aggregate profit income Π and the full employment condition. If we divide both sides by p T , we get

Market clearing in the nontradable sector requires the supply to equal demand y N = c N . This implies that the aggregate constraint for the tradable sector is simply given by:

4.4 Equilibrium

An equilibrium in this economy consists of (i) consumption choices c

T

and c

N

, (ii) labor allocation decisions

solve the household’s problem;

maximize firm profits;

satisfy the occupational constraints (i.e.

ensure all markets clear.

4.5 Solution

The general equilibrium in this model can be characterized as follows. We combine the aggregate constraints in both sectors, the first order condition from the household’s problem, and the full employment condition to obtain:

Noting that

we will refer to equation (19) as the “market clearing” condition or “MC-schedule.”

Next, we can rearrange the first order conditions of firms in equations (10) and (13) as follows using the wage equations (

Combining these equations, we obtain the following condition:

where we have defined:

We will refer to (22) as the “labor return” or “LR-schedule” because it is this condition that ensures that effective labor returns are equalized between sectors.

It is worth taking a moment to examine the variable z in the LR schedule, which summarizes the impact of the gender-based occupational segregation across sectors. As can be seen in equation (23), the constant z acts as a wedge on the relative marginal products of both sectors and depends on the gender composition of employment in each sector (θ N and θ T ) and on the relative female wage η.

Now that we have reduced the economy to the MC and LR schedules, we have obtained a system of two equations with two unknowns: the real exchange rate q and female employment

General equilibrium – female labor.

4.6 Effect of Capital Inflows

Although we abstract from intertemporal saving and borrowing decisions, we can nevertheless model the macroeconomic effects of a surge of capital inflows as a decrease in the exogenous level of net exports NX. This is arguably a good approximation of the effects of financial liberalization in developing countries.[7] According to equation (19), there is a negative relationship between net exports and the real exchange rate in the MC schedule. As shown in Figure 4, a drop in net exports (↓NX) leads to an upward shift in the MC curve. The new equilibrium occurs at point B . Thus, the RER appreciates and female employment in the tradable sector shrinks. If the female employment share in the tradable sector is larger than the male employment share, reallocation of women’s employment would be higher than men’s.

A few remarks are in order. First, the equilibrium RER appreciation obtained above could be avoided or attenuated by external policy interventions, such as foreign reserve accumulation. In this sense, the comparative statics depicted in Figure 4 should be regarded as holding constant any other policy interventions that are expected to affect the RER. Second, financial liberalization has historically been associated with increased volatility and a higher likelihood of experiencing a currency crisis.[8] In other words, financial liberalization could very well result in RER depreciation if followed by a crisis. The model presented here thus abstracts from these considerations.

4.7 Consequences of a Change in Relative Female Wages

How does the structure of gender-based occupational segregation affect the macroeconomic outcomes in our model? We start by examining the effect of exogenous changes in the female wage penalty. Taking the partial derivative of q with respect to η in the LR schedule, we obtain:

The sign will depend on the sign of the numerator, specifically θ

N

− θ

T

. Since this is a small economy model, we can consider two different cases for low and low-middle income countries. In the first case, we focus on low income countries. In low income countries, female intensity is higher in the tradable sector (θ

T

> θ

N

) as shown in Table 1, so we can conclude that

Decreasing female wage penalty (↑η).

In the second case, we focus on low-middle income countries. In the low-middle income countries, the nontradable sector is more female-intensive (θ

N

> θ

T

) as shown in Table 1, so

When female intensity is higher in the tradable sector, as is the case for the low income countries, the female wage penalty will overwhelmingly affect this sector. A decreasing wage penalty therefore disproportionately increases the effective wage costs of tradable firms. As a result, the tradable sector shrinks and the real exchange rate depreciates. As the income level of the country increases female intensity in tradable sectors declines relative to the one in nontradable sectors. Therefore, the effect of a change in the female wage penalty might be in the opposite direction. In low-middle income countries, even though female intensity is higher in nontradables, the difference is very small. Hence, the effects might be relatively small.

5 Endogenous Labor Supply

In this section, we relax the assumption of a fixed aggregate labor supply. Household members divide their time between paid work and the production of a non-market home good. Even if household members work full time for their paid work, they still need to do some household production. We can consider the production of the home good as care work or another type of unpaid household work such as cleaning or cooking. In the model, we do not present a distinction between the type of household work.

Each household members are now endowed with a unit of labor hours, which they can divide between formal employment or towards the production of a non-market “home” good:

where h g refers to the fraction of time devoted by gender g = {m, f} to home good production.

Household preferences are given by:

where φ > 0 and c H denotes consumption of the home good. We assume that home good production takes the following functional form:

where ɛ > 1 and κ g ∈ (0, 1) denotes the minimum required amount of time for the production of home goods that each household member needs to devote. For equation (27), we impose the restriction that h g > κ g , which states that household members need to spend more time than just the minimum amount for home production.[9] Intuitively, we can think of κ g as representing the norms regarding gender roles in home production. Women usually take a heavier burden of the unpaid care and household work because of social gender norms. In our model, both male and female members have this parameter that reflects the minimum amount of home production. If κ m = κ f , the household is more egalitarian. On the other hand, when women’s required home production is higher than men’s, κ f > κ m , this reflects a more patriarchal household. In order to have a model consistent with reality, we assume that κ f > κ m .

The household’s problem consists of choosing

The first-order conditions for the choice of c T and c N are given, respectively, by:

where λ is the Lagrange multiplier on the household budget constraint. Combining these two equations yields the familiar optimality condition (7) equating the marginal rate of substitution between N and T goods to their relative price q. The first-order conditions for the allocation of labor hours are given by:

5.1 Model Solution

The supply-side of the model remains unchanged from the previous section. Profit maximization by N-sector firms (10) implies q = (1 − (η − 1)θ N )w m , where we have used w f = ηw m . Plugging in the value of q into (29) and combining with (30) and (25), we can solve for the labor supply of each household member:

where we have used the market clearing condition c N = y N and have defined the constant:

It immediately follows that the aggregate labor supply is:

The household’s labor supply functions depend on the level of consumption of nontradables y N , the female wage gap η, and the minimum home production requirements, κ f and κ m . Intuitively, higher consumption of nontradables increases the marginal utility of consuming home goods, which increases the amount of time devoted to home production and consequently leads to a decrease in household labor supply. As can be seen in equation (31), this channel will be weaker for female labor supply due to existence of a female wage gap η < 1.

5.2 Relative Female Employment

An important feature of this model extension is the possibility of an endogenous aggregate female to male employment ratio driven by macroeconomic conditions and, in particular, structural change between tradables and nontradables. This feature is desirable because it makes it possible to relate our framework to the existing empirical literature, which tends to focus on aggregate female employment gaps.[10] Two factors make this feature possible: (i) the inclusion of the minimum home good input requirements κ g , which render the resulting labor supply functions non-homothetic and (ii) the existence of a female wage penalty η < 1, which attenuates the response of female labor supply to changes in y N .

Using (31), we can define the ratio of female to male labor supply G = ℓ f /ℓ m as:

which may be increasing or decreasing in y N depending on the values of η, κ m , and κ f .[11] It can be verified that dG/dy N < 0 when the following condition is satisfied:

This condition states that an expansion in the nontradable sector will lower female employment relative to male employment as long as women’s burden in home good production is disproportionately high (that is, when κ f is sufficiently large). It is worth noting that if the gender wage gap is absent (η = 1), this condition reduces to simply κ f > κ m , in which case an expansion of nontradables always reduces the ratio of aggregate female to male labor supply.

5.3 General Equilibrium

To solve for the equilibrium supply of nontradables, recall that y N = ℓ N , which implies that the full employment condition can be expressed as L = ℓ T + y N . Combining the full employment condition with the aggregate labor supply (32) and solving for y N , we get:

The equilibrium supply of nontradables can therefore be expressed as a decreasing function of the labor employed in the tradable sector: y

N

= y

N

(ℓ

T

), with

Armed with the above equilibrium relationships, we can characterize the general equilibrium link between the RER q, female employment in the T-sector

where we have again used the relation

The general equilibrium is depicted graphically in Figure 6. As in the previous section, the MC and LR schedule (in the upper panel) together uniquely pin down the equilibrium RER and employment structure

RER and employment structure in general equilibrium.

5.4 Financial Liberalization

We conclude by reexamining the effects of financial liberalization, modeled as an exogenous rise in capital inflows and the associated deterioration in net exports NX. As above, the capital inflows increase consumption of the tradable goods, leading to a RER appreciation. As shown in the top panel of Figure 6, this entails to an upward shift in the MC schedule and shrinking female employment in tradables, corresponding to a transition from equilibria A to B . In other words, the implications of financial liberalization for structural change and female employment in the tradables is qualitatively unaffected by endogenizing the labor supply choice.

What does qualitatively change, however, is the response of the aggregate female to male employment ratio G = ℓ f /ℓ m . As can be seen in the bottom panel of Figure 6, when the tradable sector shrinks in response to a surge of capital inflows, aggregate female employment disproportionately decreases relative to male employment. This is indicated by a movement from points C to D . As already noted, this result assumes that the burden of home production falls disproportionately on women, which is arguably the empirically relevant case.

Put differently, the model predicts that large RER appreciations should have larger effects on female employment than on male employment. Similarly, in this framework a competitive RER undervaluation should be expected to disproportionately stimulate female employment, which is consistent with the empirical results reported by Erten and Metzger (2019).

6 Conclusion

This paper has presented evidence that episodes of capital account liberalization in developing economies lead to large declines in female employment in tradable industries. Moreover, our decomposition results suggest that, on average, this decline is primarily driven by structural change between tradable and nontradables, with a negligible contribution from within sector changes in the gender composition of employment. One important nuance, however, concerns the poorest low income countries in our sample, for which within sector female intensity effects are both large and statistically significant.

We argue that our benchmark results are consistent with a model of a two-sector small open economy featuring occupational segregation along gender lines. Though stylized, the model analytically reproduces our main empirical results on the link between capital account liberalization and declining female employment in tradable sectors. The model also yields additional insights on the macroeconomic implications of occupational segregation in a dependent economy setting and on the relationship between capital flows and the aggregate female employment gap when home production burdens are distributed unevenly between genders.

One feature that perhaps merits further attention is the link between the female relative wage and the equilibrium RER. When the tradable sector is relatively female intensive as in low income countries, gender discrimination or other factors leading to an increase in the gender wage gap will indirectly boost the competitiveness of exports and lead to an expansion of tradable industries. Whether this intuition is robust to an endogenous determination of the relative wage or what the normative implications are for social welfare is an open question.

Though we have conceived of the model as an analytically tractable reduced form, it could be extended to allow for richer intra-household dynamics and a “non-unitary” household with bargaining between its members. Indeed, unitary household models abstract from power dynamics based on gender inequality. In addition, preferences and constraints may vary across household members depending on their age and care responsibilities. A more detailed treatment of these issues could consider different levels of income pooling, as well as the consequences of alternative forms of conflict and coordination within the household.

Appendix

A Additional Figures

Decomposition of female employment effect – low-middle income sample. Note: This figure reports the impulse response of female employment to sectoral exposure to a liberalization episode (LIB i × TI j ). Panel (a) reports the overall cumulative response for total female employment in sector j. Panels (b) and (c) decompose the total response into the contribution of changes in the female employment intensity within a sector and the contribution of sectoral employment reallocation. The shaded areas depict the 90 % confidence interval, which were calculated with heteroskedasticity and autocorrelation consistent (HAC) standard errors.

Decomposition of female employment effect – low income sample. Note: This figure reports the impulse response of female employment to sectoral exposure to a liberalization episode (LIB i × TI j ). Panel (a) reports the overall cumulative response for total female employment in sector j. Panels (b) and (c) decompose the total response into the contribution of changes in the female employment intensity within a sector and the contribution of sectoral employment reallocation. The shaded areas depict the 90 % confidence interval, which were calculated with heteroskedasticity and autocorrelation consistent (HAC) standard errors.

References

Agenor, Pierre-Richard. 2007. “The Analytics of Segmented Labor Markets.” In Adjustment Policies, Poverty, and Unemployment: The IMMPA Framework, Chapter 1, edited by Pierre-Richard Agenor, Alejandro Izquierdo, and Henning Tarp Jensen, 8–66. Wiley-Blackwell.Search in Google Scholar

Borrowman, Mary, and Stephan Klasen. 2020. “Drivers of Gendered Sectoral and Occupational Segregation in Developing Countries.” Feminist Economics 26 (2): 62–94. https://doi.org/10.1080/13545701.2019.1649708.Search in Google Scholar

Braunstein, Elissa, and Mark Brenner. 2007. “Foreign Direct Investment and Gendered Wages in Urban China.” Feminist Economics 13 (3–4). https://doi.org/10.1080/13545700701439432.Search in Google Scholar

Braunstein, Elissa, and James Heintz. 2008. “Gender Bias and Central Bank Policy: Employment and Inflation Reduction.” International Review of Applied Economics 22 (2). https://doi.org/10.1080/02692170801889643.Search in Google Scholar

Bykova, Alexandra, and Roman Stöllinger. 2017. “Tradability Index: A Comprehensive Measure for the Tradability of Output.” wiiw Statistical Report (6).Search in Google Scholar

Caraway, Teri L. 2006. “Gendered Paths of Industrialization: A Cross-Regional Comparative Analysis.” Studies in Comparative International Development 41 (1): 26–52. https://doi.org/10.1007/bf02686306.Search in Google Scholar

Chinn, Menzie D., and Hiro Ito. 2006. “What Matters for Financial Development? Capital Controls, Institutions, and Interactions.” Journal of Development Economics 81 (1). https://doi.org/10.1016/j.jdeveco.2005.05.010.Search in Google Scholar

Domínguez-Villalobos, Lilia, and Flor Brown-Grossman. 2010. “Trade Liberalization and Gender Wage Inequality in Mexico.” Feminist Economics 16 (4). https://doi.org/10.1080/13545701.2010.530582.Search in Google Scholar

Erten, Bilge, and Martina Metzger. 2019. “The Real Exchange Rate, Structural Change, and Female Labor Force Participation.” World Development 117. https://doi.org/10.1016/j.worlddev.2019.01.015.Search in Google Scholar

Erten, Bilge, Anton Korinek, and José Antonio Ocampo. 2021. “Capital Controls: Theory and Evidence.” Journal of Economic Literature 59 (1): 45–89. https://doi.org/10.1257/jel.20191457.Search in Google Scholar

Evelyn, F. Wamboye, and Stephanie, Seguino. 2015. “Gender Effects of Trade Openness in Sub-Saharan Africa.” Feminist Economics 21 (3).10.1080/13545701.2014.927583Search in Google Scholar

Furceri, Davide, Prakash Loungani, and Jonathan D. Ostry. 2019. “The Aggregate and Distributional Effects of Financial Globalization: Evidence from Macro and Sectoral Data.” Journal of Money, Credit and Banking 51 (1). https://doi.org/10.1111/jmcb.12668.Search in Google Scholar

Ghosh, Atish R., Mahvash Qureshi, Jun Il Kim, and Juan Zalduendo. 2014. “Surges.” Journal of International Economics 92: 266–85. https://doi.org/10.1016/j.jinteco.2013.12.007.Search in Google Scholar

Ghosh, Atish R., Jonathan D. Ostry, and Mahvash Qureshi. 2016. “When Do Capital Inflow Surges End in Tears?” American Economic Review: Papers & Proceedings 106: 581–5. https://doi.org/10.1257/aer.p20161015.Search in Google Scholar

Ghosh, Atish R., Jonathan D. Ostry, and Mahvash Qureshi. 2017. Taming the Tide of Capital Flows: A Policy Guide. Massachusetts Institute of Technology.10.7551/mitpress/9780262037167.001.0001Search in Google Scholar

Harris, John, and Michael Todaro. 1970. “Migration, Unemployment and Development: A Two-Sector Analysis.” American Economic Review 60.Search in Google Scholar

Jorda, Oscar. 2005. “Estimation and Inference of Impulse Responses by Local Projections.” The American Economic Review 95 (1). https://doi.org/10.1257/0002828053828518.Search in Google Scholar

Kucera, David, and Sheba Tejani. 2014. “Feminization, Defeminization, and Structural Change in Manufacturing.” World Development 64: 569–82. https://doi.org/10.1016/j.worlddev.2014.06.033.Search in Google Scholar

Salter, W.E.G. 1959. “Internal and External Balance: The Role of Price and Expenditure Effects.” Economic Record 35. https://doi.org/10.1111/j.1475-4932.1959.tb00462.x.Search in Google Scholar

Saraçoğlu, Dürdane, Emel Memiş, Ebru Voyvoda, and Burça Kızılırmak. 2018. “Changes in Global Trade Patterns and Women’s Employment in Manufacturing, 1995–2011.” Feminist Economics 24 (3): 1–28. https://doi.org/10.1080/13545701.2018.1435899.Search in Google Scholar

Seguino, Stephanie. 2016. “Global Trends in Gender Equality.” Journal of African Development 18 (1): 1–30. https://doi.org/10.5325/jafrideve.18.1.0009.Search in Google Scholar

Seguino, Stephanie. 2020. “Engendering Macroeconomic Theory and Policy.” Feminist Economics 26 (2). https://doi.org/10.1080/13545701.2019.1609691.Search in Google Scholar

Seguino, Stephanie, and James Heintz. 2012. “Monetary Tightening and the Dynamics of US Race and Gender Stratification.” American Journal of Economics and Sociology 71 (3). https://doi.org/10.1111/j.1536-7150.2012.00826.x.Search in Google Scholar

Stiglitz, Joseph E. 2004. “Capital-Market Liberalization, Globalization, and the IMF.” Oxford Review of Economic Policy 20. https://doi.org/10.1093/oxrep/grh004.Search in Google Scholar

Swan, Trevor W. 1963. Longer Run Problems of the Balance of Payments. The Australian Economy.Search in Google Scholar

Tejani, Sheba, and William Milberg. 2016. “Global Defeminization? Industrial Upgrading and Manufacturing Employment in Developing Countries.” Feminist Economics 22 (2): 24–54. https://doi.org/10.1080/13545701.2015.1120880.Search in Google Scholar

© 2023 Walter de Gruyter GmbH, Berlin/Boston

Articles in the same Issue

- Frontmatter

- Editorial

- The Gendered Effects of Globalization: Recent Evidence from Developing Countries

- Research Foundation

- Protectionism and Gender Inequality in Developing Countries

- Capital Account Liberalization, Structural Change, and Female Employment

- Symposia Articles

- What Predicts the Growth of Small Firms? Evidence from Tanzanian Commercial Loan Data

- Trade Liberalization and Gender Inequality in India: A Task Content of Occupations Approach

- Can Online Platforms Promote Women-Led Exporting Firms?

- When Women’s Work Disappears: Marriage and Fertility Decisions in Peru

- Trade Boomers: Evidence from the Commodities-for-Manufactures Boom in Brazil

Articles in the same Issue

- Frontmatter

- Editorial

- The Gendered Effects of Globalization: Recent Evidence from Developing Countries

- Research Foundation

- Protectionism and Gender Inequality in Developing Countries

- Capital Account Liberalization, Structural Change, and Female Employment

- Symposia Articles

- What Predicts the Growth of Small Firms? Evidence from Tanzanian Commercial Loan Data

- Trade Liberalization and Gender Inequality in India: A Task Content of Occupations Approach

- Can Online Platforms Promote Women-Led Exporting Firms?

- When Women’s Work Disappears: Marriage and Fertility Decisions in Peru

- Trade Boomers: Evidence from the Commodities-for-Manufactures Boom in Brazil