A preconditioned iterative method for coupled fractional partial differential equation in European option pricing

-

Shuang Wu

Abstract

Recently, regime-switching option pricing based on fractional diffusion models has been used, which explains many significant empirical facts about financial markets better. There are many methods to solve the problem, but to the best of our knowledge, effective preconditioners for the second-order schemes have not been proposed. Thus, in this article, an implicit numerical scheme is developed for a regime-switching European option pricing problem under a multi-state tempered fractional model. The scheme is proven to be unconditionally stable and converges quadratically in space and linearly in time. Besides, the resulting linear system is solved using an iterative method, and a preconditioner is proposed to accelerate the rate of convergence. The preconditioner is constructed through circulant approximations to the Toeplitz blocks due to the coefficient matrix, which is is a block matrix with Toeplitz blocks. The spectral analysis of the preconditioned matrix is given, which demonstrates that the spectrum of the preconditioned matrix is clustered around 1. Numerical examples show the efficiency of the proposed method, and an empirical study is also provided.

1 Introduction

Since the 1970s, the classic Black-Scholes (BS) [1] European option pricing model has been proposed for calculating asset values, and is one of the most fundamental and powerful tools in financial mathematics. However, the standard BS model is recognized to have several shortcomings and is unable to account for the phenomenon of many significant empirical events in the financial markets, such as skewed return distribution, and the assumption of constant volatility generates bias. To compensate for the shortcomings of the standard BS model, some alternative models are needed.

Thus, various alternate models have been proposed. Within these models, the Merton jump-diffusion model [2] is one of the earliest alternatives, which is based on a compound Poisson jump process. The Kou jump-diffusion model [3] is based on a double exponential jump-diffusion model. The finite moment logarithmic stability (FMLS) model [4], Carr-Geman-Madan-Yor (CGMY) model [5], and Koponen-Boyarchenko-Levendorski (KoBoL) model [6] are all based on some Lévy processes. The Heston model [7] is used to account for stochastic volatility, where the volatility parameter is stochastic rather than a constant. Recently, a number of models based on regime-switching models have been used to simulate the effects of structural changes in economic conditions or different phases of the business cycle. Hence, to capture more empirical features of the market and respond to state changes effectively, regime-switching models began to emerge. In these models, parameters such as drift and volatility parameters depend on a Markov chain and are allowed to change between regimes.

The option pricing problem based on regime-switching Lévy processes is widely discussed. In [8], the valuation problem of life-contingent lookback options is studied, in which the underlying asset price process is assumed to be an exponential regime-switching Lévy process. The regime-switching option pricing under an exponential Lévy model with coefficients modified by a Markov chain is considered, and the underlying risky asset is controlled through a regime-switching CGMY process [9]. In [10], a regime-switching intensity model for credit risk pricing is considered, where default events are specified by a Poisson process and their intensity is modeled by a Lévy process. Some applications of the option pricing problem based on regime-switching Lévy processes have been proposed in many works of literature. The pricing of some multivariate European options under the Markov-modulated Lévy processes model is studied in [11]. In [12], a problem governing the price of American options followed a geometric regime-switching Lévy process. Besides, the regime-switching model also has lower computational complexity than stochastic volatility models.

For solving the option pricing problem with regime-switching Lévy processes, a number of different numerical methods are studied in [8,12–18]. This study concentrates on resolving the financial problem using the fractional partial differential equation (FPDE)-based approach. In [16], the European option pricing problem under a regime-switching FMLS model governed by a coupled FPDE system is investigated. Two finite difference methods are shown, namely, the implicit finite difference method (IM) and implicit-explicit (IMEX) finite difference method with CGMY and KoBoL models [15]. Besides, the Fourier transform used for the European barrier option value under an FPDE based on some specific Lévy processes has been introduced creatively in [17]. In [14], the European option pricing problem under the FMLS model with stochastic volatility and involving three-dimensional FPDE system is discussed. An explicit closed form for European-style option pricing under the FMLS model based on the FPDE system is discussed in [19]. A fast penalty method is proposed for problems involving the pricing of American options whose underlying asset follows a geometric regime-switching Lévy process in [12]. A power penalty method is proposed for the American option pricing problem based on the geometric Lévy process governed by a nonlinear FPDE system considered in [20]. In [21], the multi-asset option pricing model under the multi-variate CGMY process based on a tempered FPDE is considered. In these studies, the models are essentially first-order discretized in space. To the best of our knowledge, none of them have considered the second-order discretization in space. Hence, one of the primary goals of this research is to consider a second-order implicit finite difference method based on the coupled FPDE.

The contributions of this article are as follows. First, we propose a second-order discretized scheme of space and provide the stability and convergence proof of this scheme. Second, a novel preconditioner is provided for speeding up the Krylov subspace method, and the proof of the spectrum distribution is provided to show that the spectrum of the preconditioned matrix is concentrated around 1. Third, the preconditioner matrix contains the intensity matrix

This article is organized as follows. In Section 2, the model of the tempered FPDE governing multi-state European option pricing is discretized by the implicit second-order scheme with analysis for stability and convergence. A fast preconditioned iterative method for the discrete second-order system and some proofs as well as the implementation of the preconditioner are given in Section 3. In Section 4, numerical experiments and a real-world experiment are given to demonstrate the efficiency of the block preconditioner. Concluding remarks are given in Section 5.

2 Second-order scheme

In this section, the coupled FPDE in regime-switching European option pricing is introduced. Then, its second-order discretized form and matrix form are proposed. The analysis of two basic properties, i.e., stability and convergence, is also given. In [12], the following is the essential form of the tempered FPDE governing multi-state European option pricing:

where

for

2.1 Second-order discretization in space on the implicit scheme

In this subsection, the second-order discretization on the implicit scheme is developed. Because both of the operators

Thus, Model (1) can be converted into:

where

Let

where

The approximation provided in [22] can be used to estimate the two tempered fractional derivatives after the boundary transformation. Let

where

And

Furthermore, the central-difference formula is used to discretize the derivative, which is represented as follows:

Let the notation

with error term of

2.2 Matrix form for the second-order scheme

For simplicity, an

Let vectors

where

with

and

2.3 Stability and convergence analysis

In this subsection, the stability, and convergence of the second-order scheme are discussed. In the analysis, the properties of the coefficient matrix are primary. Hence, a lemma about the property of Toeplitz matrices is provided first.

Lemma 1

Denote that

Proof

For

Since

According to Lemma 1, the following lemma about the property of the coefficient matrix is obtained to support the analysis.

Lemma 2

For all

where

Proof

The notation

According to the definition of matrix 2-norm, we have

Because

where

Then, the following lemma about the norm of the inverse of the coefficient matrix can be obtained with Lemma 2.

Lemma 3

For

where

Proof

Let the vector norm

where

Remark 1

If

According to the aforementioned lemmas, the following theorems about stability and convergence can be analyzed. Let

Theorem 4

(Stability) The numerical solution obtained from (6) satisfies

where

Proof

Since

Theorem 5

(Convergence) Let

where

Proof

Let

since

Hence, the proof for convergence is done.□

With Theorems 4 and 5, we can know that the second-order scheme in (6) is stable and convergent.

3 Fast preconditioned iterative method

The fast Krylov subspace method is widely used to solve Toeplitz linear systems and is regarded as a fast solver [23]. We know that the computational cost per iteration of the fast Krylov subspace is

In view of the matrix form (7), if the Gaussian elimination approach is used, it yields an algorithm with

For the coefficient matrix

3.1 Block preconditioner

In this subsection, a block preconditioner is proposed. For the accuracy of the preconditioner, a block preconditioner

where

where

3.2 Invertibility analysis and spectral distribution

Theorem 6

(Invertibility) The block preconditioner

Proof

Let the notation

Then, we have

Similarly, we have

so we can obtain that for

With Lemma 2, using similar techniques, we have

where

In the following lemmas and theorems, the spectral distribution of the block preconditioner

Lemma 7

For

where

Proof

With Lemma 3 and Theorem 6, we can know that

Lemma 8

[24] For any

where

Hence, with Lemma

8, the spectra distribution of the block preconditioner

Theorem 9

For any

where

Proof

With Lemma 8, it holds

Let

Hence, we have

Denote that

where

After analyzing the small norm and low rank of the block preconditioner

3.3 Implementation of

P

‒

1

With the guarantee of invertibility, the block preconditioner

where

However, because it is difficult to deal with the inverse part of

Then, a permutation matrix

Remark 2

Suppose that there is a permutation matrix

Then, we can obtain the matrix-vector product

After the permutation method transformation in equation (16) to (17), the matrix is changed from a block matrix of

In order to clearly represent the notations,

In order to speed up the matrix-vector product calculation, the Sherman-Morrison formula can be considered to solve the block diagonal matrix (18).

3.3.1 Case 1: rank (

Q

) = 1

The Sherman-Morrison formula [25] can only be used when the rank of the matrix is 1. Therefore, the case is considered when the rank of

Lemma 10

(Sherman-Morrison formula) [25] Suppose that

The Sherman-Morrison formula

Because

Remark 3

Similar to the Hadamard product, another symbol

where

and

Besides, the part of Formula (19) has repetitions in the numerator and denominator, in the calculation, a part of the calculation can be reduced. And a large number of loop computing can be avoided during calculation using the Hadamard product since vector multiplication can be done directly, which greatly reduces the amount of calculation and speeds up the calculation. Therefore, the operation cost of the matrix-vector product

Remark 4

The ILU factorization is used when rank

4 Numerical experiments

For the experiments, all numerical experiments are carried out in MATLAB (R2019b) on a Laptop with configuration: Intel(R) Core(TM) i7-7700 CPU @ 3.60GHz and 16.0GB RAM. In order to better compare the effectiveness of the proposed preconditioner, the Strang preconditioner is used for comparison [15], which is

When solving the linear system, the generalized minimum residual (GMRES) approach is selected as the Krylov subspace method, the restart is 20, and the stopping criterion is

4.1 Example 1

A coupled tempered FPDE with a known exact solution is taken into consideration in order to illustrate the precision of the suggested implicit method and is presented as:

with

In Table 1, we show the error and convergence rate of the implicit second-order scheme. In this table, the Strang preconditioner

Errors and convergence rate for Example 1

|

|

|

Case (a) | Case (b) | Case (c) | Case (d) | ||||

|---|---|---|---|---|---|---|---|---|---|

| Error | Rate | Error | Rate | Error | Rate | Error | Rate | ||

|

|

|

|

— |

|

— |

|

— |

|

— |

|

|

|

|

1.9079 |

|

1.9184 |

|

1.9185 |

|

1.9201 |

|

|

|

|

1.9560 |

|

1.9592 |

|

1.9583 |

|

1.9597 |

|

|

|

|

1.9786 |

|

1.9797 |

|

1.9790 |

|

1.9796 |

From Table 1, it is apparent that the scheme is stable with a second-order convergence rate when

In Table 2, because the length of space is significantly more than the length of time in a real financial market, the

Iteration numbers and CPU time of three methods for Example 1

|

|

|

IM-nP | IM-P | IM-b-P | |||

|---|---|---|---|---|---|---|---|

| Ite | CPU | Ite | CPU | Ite | CPU | ||

| Case (a) | |||||||

|

|

|

1335.3 | 1.12 s | 19.0 | 0.05 s | 8.0 | 0.02 s |

|

|

|

3855.7 | 9.00 s | 19.0 | 0.08 s | 8.0 | 0.05 s |

|

|

|

9765.9 | 75.68 s | 18.0 | 0.25 s | 8.0 | 0.14 s |

|

|

|

22051.0 | 1103.24 s | 18.0 | 1.13 s | 8.0 | 0.58 s |

| Case (b) | |||||||

|

|

|

4323.9 | 4.64 s | 40.0 | 0.07 s | 10.0 | 0.03 s |

|

|

|

9403.1 | 28.41 s | 37.0 | 0.18 s | 10.0 | 0.09 s |

|

|

|

20435.0 | 383.35 s | 32.0 | 0.60 s | 10.0 | 0.26 s |

|

|

|

36195.0 | 3380.75 s | 27.0 | 2.64 s | 10.0 | 0.29 s |

| Case (c) | |||||||

|

|

|

2943.4 | 3.57 s | 54.0 | 0.14 s | 12.0 | 0.04 s |

|

|

|

7840.5 | 31.19 s | 45.0 | 0.32 s | 12.0 | 0.13 s |

|

|

|

18621.0 | 505.71 s | 35.0 | 1.11 s | 11.0 | 0.54 s |

|

|

|

36383.0 | 4169.38 s | 29.0 | 3.98 s | 11.0 | 1.95 s |

| Case (d) | |||||||

|

|

|

3058.9 | 6.01 s | 138.0 | 0.39 s | 17.0 | 0.09 s |

|

|

|

8194.8 | 138.55 s | 100.0 | 2.13 s | 17.0 | 0.50 s |

|

|

|

19886.0 | 962.88 s | 81.0 | 5.00 s | 16.0 | 1.55 s |

|

|

|

40039.0 | 14661.27 s | 60.0 | 10.83 s | 16.0 | 5.10 s |

From Table 2, it can be seen that when the number of states

4.2 Example 2

In this example, the multi-state KoBoL model (1) is used to evaluate the European call option. The following are the basic parameters:

In Example 2, the different methods with preconditioners are compared in four different cases. In Table 3, we can see that although the Strang preconditioner

Iteration numbers and CPU time of three methods for Example 2

|

|

|

IM-nP | IM-P | IM-b-P | |||

|---|---|---|---|---|---|---|---|

| Ite | CPU | Ite | CPU | Ite | CPU | ||

| Case (a) | |||||||

|

|

|

49.3 | 0.06 s | 18.7 | 0.05 s | 7.0 | 0.02 s |

|

|

|

63.7 | 0.20 s | 15.7 | 0.08 s | 7.0 | 0.04 s |

|

|

|

86.8 | 0.80 s | 12.9 | 0.18 s | 8.0 | 0.13 s |

|

|

|

118.9 | 5.62 s | 11.9 | 0.73 s | 8.0 | 0.60 s |

| Case (b) | |||||||

|

|

|

64.6 | 0.09 s | 24.9 | 0.08 s | 7.0 | 0.02 s |

|

|

|

88.9 | 0.29 s | 17.81 | 0.09 s | 8.0 | 0.05 s |

|

|

|

127.0 | 1.09 s | 14.9 | 0.23 s | 8.0 | 0.14 s |

|

|

|

185.2 | 8.91 s | 13.0 | 0.78 s | 8.0 | 0.65 s |

| Case (c) | |||||||

|

|

|

73.6 | 0.30 s | 38.50 | 0.22 s | 9.0 | 0.04 s |

|

|

|

98.9 | 1.12 s | 29.44 | 0.41 s | 10.0 | 0.13 s |

|

|

|

142.0 | 6.90 s | 22.50 | 1.36 s | 10.0 | 0.59 s |

|

|

|

214.9 | 39.07 s | 17.94 | 3.82 s | 10.9 | 2.42 s |

| Case (d) | |||||||

|

|

|

83.7 | 0.15 s | 40.8 | 0.15 s | 9.0 | 0.03 s |

|

|

|

114.5 | 0.51 s | 31.4 | 0.22 s | 9.8 | 0.10 s |

|

|

|

166.5 | 3.66 s | 25.6 | 0.83 s | 10.0 | 0.43 s |

|

|

|

254.3 | 25.93 s | 19.9 | 2.84 s | 10.9 | 1.84 s |

4.3 Example 3

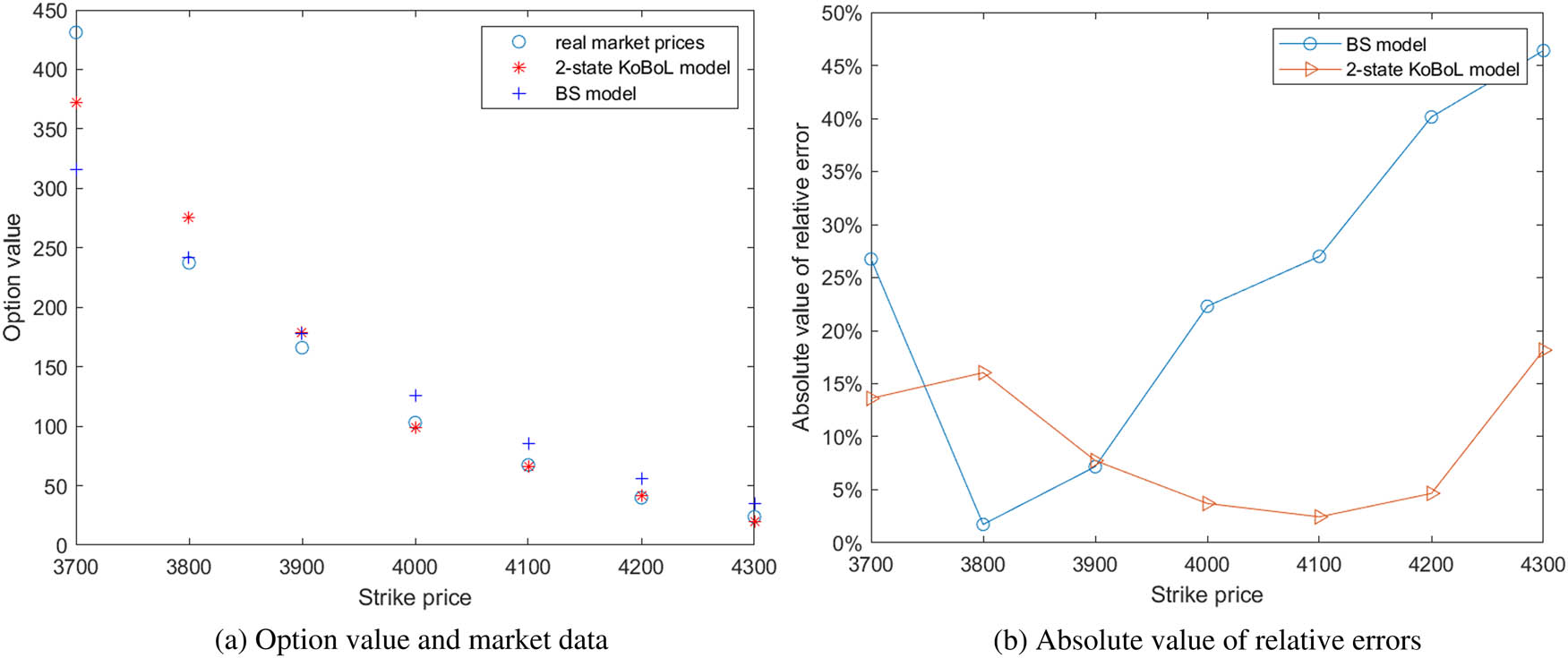

In Example 3, the efficacy of the tempered fractional model and the precision of the proposed numerical approach are demonstrated in a real-world experiment. In this example, the problem of calibrating the European options is compared using the two-state KoBoL model and the BS model. We use the market data of options contract IO2305-C.CFE on March. 10, 2023, to compare the results of calibrating the two-state KoBoL model and the BS model. The parameter settings are as follows:

In Figure 1, the calibrated parameter of the BS model is 0.1957, which is often referred to as the implied volatility, and the parameters for the two-state KoBoL model are

Comparison between two models.

From Figure 1(a), the option prices of the two-state KoBoL model are closer to the real market price. And from Figure 1(b), the absolute value of the relative error of the two-state KoBoL model is smaller than that of the BS model, although there are some sudden movements in the real-world market. It is clear that the two-state KoBoL model is better, and many fundamental empirical facts of financial markets, such as skewed and unexpected huge swings in stock prices, are explained by it.

In Table 4, the GMRES methods with two preconditioners and three different methods are compared with these parameters. It is clear that although the GMRES method using the Strang preconditioner

Iteration numbers and CPU time of three methods for Example 3

|

|

|

IM-nP | IM-P | IM-b-P | |||

|---|---|---|---|---|---|---|---|

| Ite | CPU | Ite | CPU | Ite | CPU | ||

|

|

|

183.2 | 0.30 s | 6.0 | 0.03 s | 5.0 | 0.02 s |

|

|

|

32.7 | 0.20 s | 6.0 | 0.05 s | 5.0 | 0.03 s |

|

|

|

15.2 | 0.28 s | 5.0 | 0.13 s | 5.0 | 0.10 s |

|

|

|

11.2 | 0.74 s | 5.8 | 0.44 s | 5.0 | 0.43 s |

5 Conclusion

In this study, the regime-switching European option pricing based on the fractional diffusion model is studied. In order to reduce the calculation cost of solving the model, a second-order scheme of the implicit finite difference method is used, the analysis of related stability and convergence is given, and a special structure coefficient matrix is provided. The proposed preconditioner of the generalized minimal residual method solves the linear system

In addition, since the application of the Sherman-Morrison formula is limited by the number of states

Acknowledgement

The authors would like to express their sincere thanks to the referees for their valuable suggestions that led to an improved version of this manuscript.

-

Funding information: This work was supported in part by research grants of University of Macau (File Nos. MYRG2020-00208-FST and MYRG2022-00262-FST), Guangdong Basic and Applied Basic Foundation (Grant No. 2020A1515110991), the National Natural Science Foundation of China (Grant No. 12101137), and the Science and Technology Development Fund, Macau SAR under Funding Scheme for Postdoctoral Researchers of Higher Education Institutions 2021 (File No. 0032/APD/2021).

-

Author contributions: All authors have accepted responsibility for the entire content of this manuscript and approved its submission.

-

Conflict of interest: The authors state no conflict of interest.

-

Data availability statement: All data generated or analysed during this study are included in this published article.

References

[1] F. Black and M. Scholes, The pricing of options and corporate liabilities, J. Pol. Econ. 81 (1973), no. 3, 637–654, DOI: https://doi.org/10.1086/260062. 10.1086/260062Search in Google Scholar

[2] R. C. Merton, Theory of rational option pricing, Bell J. Econ. Manage. Sci. 4 (1973), 141–183, DOI: https://doi.org/10.2307/3003143. 10.2307/3003143Search in Google Scholar

[3] S. G. Kou, A jump-diffusion model for option pricing, Manage. Sci. 48 (2002), no. 8, 955–1101, DOI: https://doi.org/10.1287/mnsc.48.8.1086.166. 10.1287/mnsc.48.8.1086.166Search in Google Scholar

[4] P. Carr and L. Wu, The finite moment log stable process and option pricing, J. Finance 58 (2003), no. 2, 753–777, DOI: https://doi.org/10.1111/1540-6261.00544. 10.1111/1540-6261.00544Search in Google Scholar

[5] P. Carr, H. Geman, D. B. Madan, and M. Yor, The fine structure of asset returns: An empirical investigation, J. Bus. 75 (2002), no. 2, 305–332, DOI: https://doi.org/10.1086/338705. 10.1086/338705Search in Google Scholar

[6] S. I. Boyarchenko and S. Z. Levendorskiĭ, Non-Gaussian Merton-Black-Scholes Theory, Statistical Science & Applied Probability, Vol. 9, World Scientific, Singapore, 2002. 10.1142/4955Search in Google Scholar

[7] S. L. Heston, A closed-form solution for options with stochastic volatility with applications to bond and currency options, Rev. Financ. Stud. 6 (1993), no. 2, 327–343, DOI: https://doi.org/10.1093/rfs/6.2.327. 10.1093/rfs/6.2.327Search in Google Scholar

[8] R. J. Elliott and C. J. U. Osakwe, Option pricing for pure jump processes with Markov switching compensators, Finance Stoch. 10 (2006), no. 2, 250–275, DOI: https://doi.org/10.1007/s00780-006-0004-6. 10.1007/s00780-006-0004-6Search in Google Scholar

[9] P. Asiimwe, C. W. Mahera, and O. Menoukeu-Pamen, On the price of risk under a regime switching CGMY process, Asia-Pac. Financ. Mark. 23 (2016), 305–335, DOI: https://doi.org/10.1007/s10690-016-9219-5. 10.1007/s10690-016-9219-5Search in Google Scholar

[10] D. Hainaut and O. Le Courtois, An intensity model for credit risk with switching Lévy processes, Quant. Finance 14 (2014), no. 8, 1453–1465, DOI: https://doi.org/10.1080/14697688.2012.756583. 10.1080/14697688.2012.756583Search in Google Scholar

[11] G. Deelstra and M. Simon, Multivariate European option pricing in a Markov-modulated Lévy framework, J. Comput. Appl. Math. 317 (2017), 171–187, DOI: https://doi.org/10.1016/j.cam.2016.11.040. 10.1016/j.cam.2016.11.040Search in Google Scholar

[12] S. Lei, W. Wang, X. Chen, and D. Ding, A fast preconditioned penalty method for American options pricing under regime-switching tempered fractional diffusion models, J. Sci. Comput. 75 (2018), no. 3, 1633–1655, DOI: https://doi.org/10.1007/s10915-017-0602-9. 10.1007/s10915-017-0602-9Search in Google Scholar

[13] X. Li, P. Lin, X. C. Tai, and J. Zhou, Pricing two-asset options under exponential Lévy model using a finite element method, arXiv:1511.04950v1, 2015, https://doi.org/10.48550/arXiv.1511.04950.Search in Google Scholar

[14] X. He and S. Lin, A fractional Black-Scholes model with stochastic volatility and European option pricing, Expert Syst. Appl. 178 (2021), 114983, DOI: https://doi.org/10.1016/j.eswa.2021.114983. 10.1016/j.eswa.2021.114983Search in Google Scholar

[15] X. Chen, D. Ding, S. Lei, and W. Wang, An implicit-explicit preconditioned direct method for pricing options under regime-switching tempered fractional partial differential models, Numer. Algorithms 87 (2021), no. 3, 939–965, DOI: https://doi.org/10.1007/s11075-020-00994-7. 10.1007/s11075-020-00994-7Search in Google Scholar

[16] S. Lin and X. J. He, A regime switching fractional Black-Scholes model and European option pricing, Commun. Nonlinear Sci. Numer. Simul. 85 (2020), 105222, DOI: https://doi.org/10.1016/j.cnsns.2020.105222. 10.1016/j.cnsns.2020.105222Search in Google Scholar

[17] A. Cartea and D. del Castillo-Negrete, Fractional diffusion models of option prices in markets with jumps, Phys. A 374 (2007), no. 2, 749–763, DOI: https://doi.org/10.1016/j.physa.2006.08.071. 10.1016/j.physa.2006.08.071Search in Google Scholar

[18] Z. Zhou, J. Ma, and X. Gao, Convergence of iterative Laplace transform methods for a system of fractional PDEs and PIDEs arising in option pricing, East Asian J. Appl. Math. 8 (2018), no. 4, 782–808, DOI: https://doi.org/10.4208/eajam.130218.290618. 10.4208/eajam.130218.290618Search in Google Scholar

[19] W. Chen, X. Xu, and S. P. Zhu, Analytically pricing European-style options under the modified Black-Scholes equation with a spatial-fractional derivative, Quart. Appl. Math. 72 (2014), no. 3, 597–611, DOI: https://doi.org/10.1090/S0033-569X-2014-01373-2. 10.1090/S0033-569X-2014-01373-2Search in Google Scholar

[20] W. Chen and S. Wang, A penalty method for a fractional order parabolic variational inequality governing American put option valuation, Comput. Math. Appl. 67 (2014), no. 1, 77–90, DOI: https://doi.org/10.1016/j.camwa.2013.10.007. 10.1016/j.camwa.2013.10.007Search in Google Scholar

[21] X. Guo, Y. Li, and H. Wang, Tempered fractional diffusion equations for pricing multi-asset options under CGMYe process, Comput. Math. Appl. 76 (2018), no. 6, 1500–1514, DOI: https://doi.org/10.1016/j.camwa.2018.07.002. 10.1016/j.camwa.2018.07.002Search in Google Scholar

[22] M. Chen and W. Deng, High order algorithms for the fractional substantial diffusion equation with truncated Lévy flights, SIAM J. Sci. Comput. 37 (2015), no. 2, A890–A917, DOI: https://doi.org/10.1137/14097207X. 10.1137/14097207XSearch in Google Scholar

[23] R. H. Chan and X. Jin, An introduction to iterative Toeplitz solvers, Fundamentals of Algorithms, Vol. 5, SIAM, Philadelphia, 2007. 10.1137/1.9780898718850Search in Google Scholar

[24] S. L. Lei, D. Fan, and X. Chen, Fast solution algorithms for exponentially tempered fractional diffusion equations, Numer. Methods Partial Differential Equations 34 (2018), no. 4, 1301–1323, DOI: https://doi.org/10.1002/num.22259. 10.1002/num.22259Search in Google Scholar

[25] M. S. Bartlett, An inverse matrix adjustment arising in discriminant analysis, Ann. Math. Statist. 22 (1951), 107–111, DOI: https://doi.org/10.1214/aoms/1177729698. 10.1214/aoms/1177729698Search in Google Scholar

© 2023 the author(s), published by De Gruyter

This work is licensed under the Creative Commons Attribution 4.0 International License.

Articles in the same Issue

- Special Issue on Future Directions of Further Developments in Mathematics

- What will the mathematics of tomorrow look like?

- On H 2-solutions for a Camassa-Holm type equation

- Classical solutions to Cauchy problems for parabolic–elliptic systems of Keller-Segel type

- Control of multi-agent systems: Results, open problems, and applications

- Logical perspectives on the foundations of probability

- Subharmonic solutions for a class of predator-prey models with degenerate weights in periodic environments

- A non-smooth Brezis-Oswald uniqueness result

- Luenberger compensator theory for heat-Kelvin-Voigt-damped-structure interaction models with interface/boundary feedback controls

- Special Issue on Fractional Problems with Variable-Order or Variable Exponents (Part II)

- Positive solution for a nonlocal problem with strong singular nonlinearity

- Analysis of solutions for the fractional differential equation with Hadamard-type

- Hilfer proportional nonlocal fractional integro-multipoint boundary value problems

- A comprehensive review on fractional-order optimal control problem and its solution

- The θ-derivative as unifying framework of a class of derivatives

- Review Articles

- On the use of L-functionals in regression models

- Minimal-time problems for linear control systems on homogeneous spaces of low-dimensional solvable nonnilpotent Lie groups

- Regular Articles

- Existence and multiplicity of solutions for a new p(x)-Kirchhoff problem with variable exponents

- An extension of the Hermite-Hadamard inequality for a power of a convex function

- Existence and multiplicity of solutions for a fourth-order differential system with instantaneous and non-instantaneous impulses

- Relay fusion frames in Banach spaces

- Refined ratio monotonicity of the coordinator polynomials of the root lattice of type Bn

- On the uniqueness of limit cycles for generalized Liénard systems

- A derivative-Hilbert operator acting on Dirichlet spaces

- Scheduling equal-length jobs with arbitrary sizes on uniform parallel batch machines

- Solutions to a modified gauged Schrödinger equation with Choquard type nonlinearity

- A symbolic approach to multiple Hurwitz zeta values at non-positive integers

- Some results on the value distribution of differential polynomials

- Lucas non-Wieferich primes in arithmetic progressions and the abc conjecture

- Scattering properties of Sturm-Liouville equations with sign-alternating weight and transmission condition at turning point

- Some results for a p(x)-Kirchhoff type variation-inequality problems in non-divergence form

- Homotopy cartesian squares in extriangulated categories

- A unified perspective on some autocorrelation measures in different fields: A note

- Total Roman domination on the digraphs

- Well-posedness for bilevel vector equilibrium problems with variable domination structures

- Binet's second formula, Hermite's generalization, and two related identities

- Non-solid cone b-metric spaces over Banach algebras and fixed point results of contractions with vector-valued coefficients

- Multidimensional sampling-Kantorovich operators in BV-spaces

- A self-adaptive inertial extragradient method for a class of split pseudomonotone variational inequality problems

- Convergence properties for coordinatewise asymptotically negatively associated random vectors in Hilbert space

- Relating the super domination and 2-domination numbers in cactus graphs

- Compatibility of the method of brackets with classical integration rules

- On the inverse Collatz-Sinogowitz irregularity problem

- Positive solutions for boundary value problems of a class of second-order differential equation system

- Global analysis and control for a vector-borne epidemic model with multi-edge infection on complex networks

- Nonexistence of global solutions to Klein-Gordon equations with variable coefficients power-type nonlinearities

- On 2r-ideals in commutative rings with zero-divisors

- A comparison of some confidence intervals for a binomial proportion based on a shrinkage estimator

- The construction of nuclei for normal constituents of Bπ-characters

- Weak solution of non-Newtonian polytropic variational inequality in fresh agricultural product supply chain problem

- Mean square exponential stability of stochastic function differential equations in the G-framework

- Commutators of Hardy-Littlewood operators on p-adic function spaces with variable exponents

- Solitons for the coupled matrix nonlinear Schrödinger-type equations and the related Schrödinger flow

- The dual index and dual core generalized inverse

- Study on Birkhoff orthogonality and symmetry of matrix operators

- Uniqueness theorems of the Hahn difference operator of entire function with a Picard exceptional value

- Estimates for certain class of rough generalized Marcinkiewicz functions along submanifolds

- On semigroups of transformations that preserve a double direction equivalence

- Positive solutions for discrete Minkowski curvature systems of the Lane-Emden type

- A multigrid discretization scheme based on the shifted inverse iteration for the Steklov eigenvalue problem in inverse scattering

- Existence and nonexistence of solutions for elliptic problems with multiple critical exponents

- Interpolation inequalities in generalized Orlicz-Sobolev spaces and applications

- General Randić indices of a graph and its line graph

- On functional reproducing kernels

- On the Waring-Goldbach problem for two squares and four cubes

- Singular moduli of rth Roots of modular functions

- Classification of self-adjoint domains of odd-order differential operators with matrix theory

- On the convergence, stability and data dependence results of the JK iteration process in Banach spaces

- Hardy spaces associated with some anisotropic mixed-norm Herz spaces and their applications

- Remarks on hyponormal Toeplitz operators with nonharmonic symbols

- Complete decomposition of the generalized quaternion groups

- Injective and coherent endomorphism rings relative to some matrices

- Finite spectrum of fourth-order boundary value problems with boundary and transmission conditions dependent on the spectral parameter

- Continued fractions related to a group of linear fractional transformations

- Multiplicity of solutions for a class of critical Schrödinger-Poisson systems on the Heisenberg group

- Approximate controllability for a stochastic elastic system with structural damping and infinite delay

- On extremal cacti with respect to the first degree-based entropy

- Compression with wildcards: All exact or all minimal hitting sets

- Existence and multiplicity of solutions for a class of p-Kirchhoff-type equation RN

- Geometric classifications of k-almost Ricci solitons admitting paracontact metrices

- Positive periodic solutions for discrete time-delay hematopoiesis model with impulses

- On Hermite-Hadamard-type inequalities for systems of partial differential inequalities in the plane

- Existence of solutions for semilinear retarded equations with non-instantaneous impulses, non-local conditions, and infinite delay

- On the quadratic residues and their distribution properties

- On average theta functions of certain quadratic forms as sums of Eisenstein series

- Connected component of positive solutions for one-dimensional p-Laplacian problem with a singular weight

- Some identities of degenerate harmonic and degenerate hyperharmonic numbers arising from umbral calculus

- Mean ergodic theorems for a sequence of nonexpansive mappings in complete CAT(0) spaces and its applications

- On some spaces via topological ideals

- Linear maps preserving equivalence or asymptotic equivalence on Banach space

- Well-posedness and stability analysis for Timoshenko beam system with Coleman-Gurtin's and Gurtin-Pipkin's thermal laws

- On a class of stochastic differential equations driven by the generalized stochastic mixed variational inequalities

- Entire solutions of two certain Fermat-type ordinary differential equations

- Generalized Lie n-derivations on arbitrary triangular algebras

- Markov decision processes approximation with coupled dynamics via Markov deterministic control systems

- Notes on pseudodifferential operators commutators and Lipschitz functions

- On Graham partitions twisted by the Legendre symbol

- Strong limit of processes constructed from a renewal process

- Construction of analytical solutions to systems of two stochastic differential equations

- Two-distance vertex-distinguishing index of sparse graphs

- Regularity and abundance on semigroups of partial transformations with invariant set

- Liouville theorems for Kirchhoff-type parabolic equations and system on the Heisenberg group

- Spin(8,C)-Higgs pairs over a compact Riemann surface

- Properties of locally semi-compact Ir-topological groups

- Transcendental entire solutions of several complex product-type nonlinear partial differential equations in ℂ2

- Ordering stability of Nash equilibria for a class of differential games

- A new reverse half-discrete Hilbert-type inequality with one partial sum involving one derivative function of higher order

- About a dubious proof of a correct result about closed Newton Cotes error formulas

- Ricci ϕ-invariance on almost cosymplectic three-manifolds

- Schur-power convexity of integral mean for convex functions on the coordinates

- A characterization of a ∼ admissible congruence on a weakly type B semigroup

- On Bohr's inequality for special subclasses of stable starlike harmonic mappings

- Properties of meromorphic solutions of first-order differential-difference equations

- A double-phase eigenvalue problem with large exponents

- On the number of perfect matchings in random polygonal chains

- Evolutoids and pedaloids of frontals on timelike surfaces

- A series expansion of a logarithmic expression and a decreasing property of the ratio of two logarithmic expressions containing cosine

- The 𝔪-WG° inverse in the Minkowski space

- Stability result for Lord Shulman swelling porous thermo-elastic soils with distributed delay term

- Approximate solvability method for nonlocal impulsive evolution equation

- Construction of a functional by a given second-order Ito stochastic equation

- Global well-posedness of initial-boundary value problem of fifth-order KdV equation posed on finite interval

- On pomonoid of partial transformations of a poset

- New fractional integral inequalities via Euler's beta function

- An efficient Legendre-Galerkin approximation for the fourth-order equation with singular potential and SSP boundary condition

- Eigenfunctions in Finsler Gaussian solitons

- On a blow-up criterion for solution of 3D fractional Navier-Stokes-Coriolis equations in Lei-Lin-Gevrey spaces

- Some estimates for commutators of sharp maximal function on the p-adic Lebesgue spaces

- A preconditioned iterative method for coupled fractional partial differential equation in European option pricing

- A digital Jordan surface theorem with respect to a graph connectedness

- A quasi-boundary value regularization method for the spherically symmetric backward heat conduction problem

- The structure fault tolerance of burnt pancake networks

- Average value of the divisor class numbers of real cubic function fields

- Uniqueness of exponential polynomials

- An application of Hayashi's inequality in numerical integration

Articles in the same Issue

- Special Issue on Future Directions of Further Developments in Mathematics

- What will the mathematics of tomorrow look like?

- On H 2-solutions for a Camassa-Holm type equation

- Classical solutions to Cauchy problems for parabolic–elliptic systems of Keller-Segel type

- Control of multi-agent systems: Results, open problems, and applications

- Logical perspectives on the foundations of probability

- Subharmonic solutions for a class of predator-prey models with degenerate weights in periodic environments

- A non-smooth Brezis-Oswald uniqueness result

- Luenberger compensator theory for heat-Kelvin-Voigt-damped-structure interaction models with interface/boundary feedback controls

- Special Issue on Fractional Problems with Variable-Order or Variable Exponents (Part II)

- Positive solution for a nonlocal problem with strong singular nonlinearity

- Analysis of solutions for the fractional differential equation with Hadamard-type

- Hilfer proportional nonlocal fractional integro-multipoint boundary value problems

- A comprehensive review on fractional-order optimal control problem and its solution

- The θ-derivative as unifying framework of a class of derivatives

- Review Articles

- On the use of L-functionals in regression models

- Minimal-time problems for linear control systems on homogeneous spaces of low-dimensional solvable nonnilpotent Lie groups

- Regular Articles

- Existence and multiplicity of solutions for a new p(x)-Kirchhoff problem with variable exponents

- An extension of the Hermite-Hadamard inequality for a power of a convex function

- Existence and multiplicity of solutions for a fourth-order differential system with instantaneous and non-instantaneous impulses

- Relay fusion frames in Banach spaces

- Refined ratio monotonicity of the coordinator polynomials of the root lattice of type Bn

- On the uniqueness of limit cycles for generalized Liénard systems

- A derivative-Hilbert operator acting on Dirichlet spaces

- Scheduling equal-length jobs with arbitrary sizes on uniform parallel batch machines

- Solutions to a modified gauged Schrödinger equation with Choquard type nonlinearity

- A symbolic approach to multiple Hurwitz zeta values at non-positive integers

- Some results on the value distribution of differential polynomials

- Lucas non-Wieferich primes in arithmetic progressions and the abc conjecture

- Scattering properties of Sturm-Liouville equations with sign-alternating weight and transmission condition at turning point

- Some results for a p(x)-Kirchhoff type variation-inequality problems in non-divergence form

- Homotopy cartesian squares in extriangulated categories

- A unified perspective on some autocorrelation measures in different fields: A note

- Total Roman domination on the digraphs

- Well-posedness for bilevel vector equilibrium problems with variable domination structures

- Binet's second formula, Hermite's generalization, and two related identities

- Non-solid cone b-metric spaces over Banach algebras and fixed point results of contractions with vector-valued coefficients

- Multidimensional sampling-Kantorovich operators in BV-spaces

- A self-adaptive inertial extragradient method for a class of split pseudomonotone variational inequality problems

- Convergence properties for coordinatewise asymptotically negatively associated random vectors in Hilbert space

- Relating the super domination and 2-domination numbers in cactus graphs

- Compatibility of the method of brackets with classical integration rules

- On the inverse Collatz-Sinogowitz irregularity problem

- Positive solutions for boundary value problems of a class of second-order differential equation system

- Global analysis and control for a vector-borne epidemic model with multi-edge infection on complex networks

- Nonexistence of global solutions to Klein-Gordon equations with variable coefficients power-type nonlinearities

- On 2r-ideals in commutative rings with zero-divisors

- A comparison of some confidence intervals for a binomial proportion based on a shrinkage estimator

- The construction of nuclei for normal constituents of Bπ-characters

- Weak solution of non-Newtonian polytropic variational inequality in fresh agricultural product supply chain problem

- Mean square exponential stability of stochastic function differential equations in the G-framework

- Commutators of Hardy-Littlewood operators on p-adic function spaces with variable exponents

- Solitons for the coupled matrix nonlinear Schrödinger-type equations and the related Schrödinger flow

- The dual index and dual core generalized inverse

- Study on Birkhoff orthogonality and symmetry of matrix operators

- Uniqueness theorems of the Hahn difference operator of entire function with a Picard exceptional value

- Estimates for certain class of rough generalized Marcinkiewicz functions along submanifolds

- On semigroups of transformations that preserve a double direction equivalence

- Positive solutions for discrete Minkowski curvature systems of the Lane-Emden type

- A multigrid discretization scheme based on the shifted inverse iteration for the Steklov eigenvalue problem in inverse scattering

- Existence and nonexistence of solutions for elliptic problems with multiple critical exponents

- Interpolation inequalities in generalized Orlicz-Sobolev spaces and applications

- General Randić indices of a graph and its line graph

- On functional reproducing kernels

- On the Waring-Goldbach problem for two squares and four cubes

- Singular moduli of rth Roots of modular functions

- Classification of self-adjoint domains of odd-order differential operators with matrix theory

- On the convergence, stability and data dependence results of the JK iteration process in Banach spaces

- Hardy spaces associated with some anisotropic mixed-norm Herz spaces and their applications

- Remarks on hyponormal Toeplitz operators with nonharmonic symbols

- Complete decomposition of the generalized quaternion groups

- Injective and coherent endomorphism rings relative to some matrices

- Finite spectrum of fourth-order boundary value problems with boundary and transmission conditions dependent on the spectral parameter

- Continued fractions related to a group of linear fractional transformations

- Multiplicity of solutions for a class of critical Schrödinger-Poisson systems on the Heisenberg group

- Approximate controllability for a stochastic elastic system with structural damping and infinite delay

- On extremal cacti with respect to the first degree-based entropy

- Compression with wildcards: All exact or all minimal hitting sets

- Existence and multiplicity of solutions for a class of p-Kirchhoff-type equation RN

- Geometric classifications of k-almost Ricci solitons admitting paracontact metrices

- Positive periodic solutions for discrete time-delay hematopoiesis model with impulses

- On Hermite-Hadamard-type inequalities for systems of partial differential inequalities in the plane

- Existence of solutions for semilinear retarded equations with non-instantaneous impulses, non-local conditions, and infinite delay

- On the quadratic residues and their distribution properties

- On average theta functions of certain quadratic forms as sums of Eisenstein series

- Connected component of positive solutions for one-dimensional p-Laplacian problem with a singular weight

- Some identities of degenerate harmonic and degenerate hyperharmonic numbers arising from umbral calculus

- Mean ergodic theorems for a sequence of nonexpansive mappings in complete CAT(0) spaces and its applications

- On some spaces via topological ideals

- Linear maps preserving equivalence or asymptotic equivalence on Banach space

- Well-posedness and stability analysis for Timoshenko beam system with Coleman-Gurtin's and Gurtin-Pipkin's thermal laws

- On a class of stochastic differential equations driven by the generalized stochastic mixed variational inequalities

- Entire solutions of two certain Fermat-type ordinary differential equations

- Generalized Lie n-derivations on arbitrary triangular algebras

- Markov decision processes approximation with coupled dynamics via Markov deterministic control systems

- Notes on pseudodifferential operators commutators and Lipschitz functions

- On Graham partitions twisted by the Legendre symbol

- Strong limit of processes constructed from a renewal process

- Construction of analytical solutions to systems of two stochastic differential equations

- Two-distance vertex-distinguishing index of sparse graphs

- Regularity and abundance on semigroups of partial transformations with invariant set

- Liouville theorems for Kirchhoff-type parabolic equations and system on the Heisenberg group

- Spin(8,C)-Higgs pairs over a compact Riemann surface

- Properties of locally semi-compact Ir-topological groups

- Transcendental entire solutions of several complex product-type nonlinear partial differential equations in ℂ2

- Ordering stability of Nash equilibria for a class of differential games

- A new reverse half-discrete Hilbert-type inequality with one partial sum involving one derivative function of higher order

- About a dubious proof of a correct result about closed Newton Cotes error formulas

- Ricci ϕ-invariance on almost cosymplectic three-manifolds

- Schur-power convexity of integral mean for convex functions on the coordinates

- A characterization of a ∼ admissible congruence on a weakly type B semigroup

- On Bohr's inequality for special subclasses of stable starlike harmonic mappings

- Properties of meromorphic solutions of first-order differential-difference equations

- A double-phase eigenvalue problem with large exponents

- On the number of perfect matchings in random polygonal chains

- Evolutoids and pedaloids of frontals on timelike surfaces

- A series expansion of a logarithmic expression and a decreasing property of the ratio of two logarithmic expressions containing cosine

- The 𝔪-WG° inverse in the Minkowski space

- Stability result for Lord Shulman swelling porous thermo-elastic soils with distributed delay term

- Approximate solvability method for nonlocal impulsive evolution equation

- Construction of a functional by a given second-order Ito stochastic equation

- Global well-posedness of initial-boundary value problem of fifth-order KdV equation posed on finite interval

- On pomonoid of partial transformations of a poset

- New fractional integral inequalities via Euler's beta function

- An efficient Legendre-Galerkin approximation for the fourth-order equation with singular potential and SSP boundary condition

- Eigenfunctions in Finsler Gaussian solitons

- On a blow-up criterion for solution of 3D fractional Navier-Stokes-Coriolis equations in Lei-Lin-Gevrey spaces

- Some estimates for commutators of sharp maximal function on the p-adic Lebesgue spaces

- A preconditioned iterative method for coupled fractional partial differential equation in European option pricing

- A digital Jordan surface theorem with respect to a graph connectedness

- A quasi-boundary value regularization method for the spherically symmetric backward heat conduction problem

- The structure fault tolerance of burnt pancake networks

- Average value of the divisor class numbers of real cubic function fields

- Uniqueness of exponential polynomials

- An application of Hayashi's inequality in numerical integration