The Connections among the US, China and Russia through Safe Assets

-

Rongyu Wang

Abstract

This paper addresses the following problem: how debt chains sewed through government bonds are operated under either full commitment or limited commitment of the valuation of the debt by bond issuing countries. This paper takes the debt relationship of the US, China and Russia as an example to study the problem. This paper finds that even under the full commitment situation, the debt chain is hard to maintain in some circumstances. In the limited-commitment situation, even if safe asset issuance is a reflection of a country’s financial power, because China’s safe asset issued to Russia is denoted by USD, whether or not China encounters Triffin dilemma is ultimately determined by the US.

1 Introduction

This paper aims to study how debt chains sewed through government bonds are operated under either full commitment or limited commitment of the valuation of the debt by bond issuing countries. In my model, the US provides government bonds to China in exchange for liquidity from China, China provides government bonds to Russia in exchange for liquidity from Russia, but the US and Russia has no direct financial relationship.

The government bond is a kind of safe asset. Countries such as the US issue government bond to China, which uses these bonds as a way to store the value of their wealth, which are expected to be preserved in bad states such as economic crisis. That is why financial instruments such as government bonds are classified as safe assets. However, if a country issues too much bond, it will enter a particular financial hardship called Triffin dilemma (Caballero et al., 2019): excessive issuance of safe assets cannot be sustained and hence devaluing the home currency to deflate the debt is possible to happen. The collapse of the Bretton woods system in the 1970s is a widely referred example to evidence the Triffin dilemma.

In this paper, because central banks purchase the risky assets for optimizing a mean-variance utility function, a standard setting for studying portfolio optimization which is nonlinear with respect to the national savings, therefore in this complicated process, the more national savings does not necessarily bring more utility for central banks. Besides, since the demand side of safe asset (e.g., People’s Bank of China) requires national savings to support its function, it may conflict with the interest of the fiscal authority of this country (e.g., the Ministry of Finance of China), which always requires more national savings to support their consumption. Therefore, there may exist a bargaining process when China determines how to allocate its savings to central bank and fiscal authority, which conducts purchasing safe asset and issuing safe asset respectively.

In my model, because only the US and China issue safe assets, therefore only the two countries may encounter the Triffin dilemma. The US have to trade off between issuing more debt to get financed, a fiscal consideration by the U.S. Treasury, and whether to devalue their own currencies, a financial consideration by the Federal Reserve, the central bank of the US. However, in China, the Chinese safe asset issued to Russia is denoted by USD and in this way, China has granted its monetary domain to the the US. In addition, People’s Bank of China can also adjust the value of RMB over RUB, but its purpose is for ensuring that the US, China and Russia are on equilibrium. Note that when devaluation of USD happens, both US and China have to pay a devaluation cost because the value of the debt of both countries are deflated.

In the full-commitment case, this paper finds that even if the US (and hence China) can fully commits to the value of its debt, sometimes the US-China-Russia debt chain still cannot be maintained and reduced to a two-tier debt chain. In the limitedcommitment case, I find that although safe asset issuance is a reflection of a country’s financial power, if the country’s safe asset is not denoted by its own currency, then such financial power is ultimately controlled by the country who issues the currency that is used to denote the safe asset.

The Triffin dilemma studied in my paper is usually termed as the modern version of Triffin dilemma, which centres on the safe assets. Caballero et al. (2017, 2019) and Farhi and Maggiori (2018, 2019) are the most important literatare in areas of safe assets and Triffin dillemma. Caballero et al. (2019) formally gave the definition of the modern version of Triffin dilemma as stated in the introduction. Caballero et al. (2017) and especially Farhi and Maggiori (2018, 2019) studied how the Triffin dilemma was triggered. Farhi and Maggiori (2018) analyzed a safe asset transaction situation between the US and the rest of the world in the core model of their paper. Based on the core model proposed by Farhi and Maggiori (2018), Farhi and Maggiori (2019) analyzed a situation in which both the US and China issue safe assets to the rest of the world and they study how the emergence of China as a significant safe asset issuer affects the US safe asset issuance decisions. This paper extends the literature to analyze the debt chain among three countries and discuss how domestic political activities, i.e., the game between People’s Bank of China and the Finance Ministry of China, affect the safe asset purchasing and issuance in the international sphere. Melting domestic and foreign economic activities in a unified framework features my paper in the literature on safe assets and Triffin dilemma.

The paper is organized as follows. Section 2 sets up the model. Section 3 derives and analyzes the equilibrium under full commitment. Section 4 examines the limited commitment case. Section 5 concludes the paper.

2 The Model

I consider a three-period setting (t=0°, t=0 and t=1). Before the US, China and Russia begin the process of issuing or purchasing safe assets, i.e., at t=0°, there is a pre-stage: the national savings or endowments of the US, China and Russia are determined. More specifically, People’s Bank of China and the Ministry of Finance of China bargains over the total endowments to gain their respective share for purchasing safe asset from the US and issuing safe asset to Russia respectively. The endowments of the US and Russia are denoted by w and w** respectively.

Due to the bargaining between People’s Bank of China and the Ministry of Finance of China, the endowment of China is expected to be divided into two portions: one is used for purchasing safe asset by People’s Bank of China and it is denoted by w*, and one is used for consumption by the Ministry of Finance of China and it is denoted by

2.1 Model Setup

There are three periods t=0°, t=0 and t=1 and a single good. The single good is understood as the composite of all commodities circulating in global economy. The endowment of this good by the US, China and Russia are w, w* and w** respectively.

The strategic interaction among the US, China and Russia in the model cover the following categories: the Nash bargaining between the Central Bank of China, i.e. People’s Bank of China, and the Ministry of Finance of China over the country’s endowment at t=0°; the safe asset transaction between the U.S. Treasury and People’s Bank of China at t=0; the safe asset transaction between the Finance Ministry of China and Bank of Russia at t=0; the trade-off between debt issuance and devaluing USD between the U.S. Treasury and the Federal Reserve.

Consider the safe asset transaction between the U.S. Treasury and People’s Bank of China. Beyond the safe asset transaction, at the mean time, both the U.S. Treasury and People’s Bank of China need some risky real assets to either satisfy their intertemporal consumption optimization purpose or portfolio optimization purpose respectively. The risky real asset happens to be there in the safe asset transaction between the U.S. Treasury and People’s Bank of China are named by, ’the first risky real asset’. The first risky real asset is in perfectly elastic supply and denoted by USD. The nominal bonds, denoted in USD, are issued by the U.S. Treasury to People’s Bank of China.

Within the above strategic interaction, the US encounters two states related to its macroeconomic environment at t=1, which are indexed by H and L. The L state represents a disaster in the macroeconomic environment of the US, which occurs with probability λ ∈ (0, 1). Instead, the H state represents a positive status of the macroeconomic environment of the US, which occurs with the remaining probability 1-λ. Farhi and Maggiori (2018) use the same specification to describe the state US may encounter, and this paper follows their style as well.

The exogenous real return of the first risky real asset is denoted by Rr. In state H, its return is

Both the Ministry of Finance of China and Bank of Russia are willing to invest in some risky asset to satisfy their intertemporal consumption optimization purpose and portfolio optimization purpose respectively. The risky real asset that happens to be there in the strategic interaction between Ministry of Finance of China and Central Bank of Russia is called the second risky real asset. The second risky real asset is in perfectly elastic supply and also denoted by USD. The nominal bonds, denoted in USD, are issued by the Ministry of Finance of China to Central Bank of Russia.

In the interaction between the Ministry of Finance of China and Bank of Russia, because the Chinese debt is also denoted by USD, therefore the Ministry of Finance of China is also specified to encounter the two states H and L which the US encounters. That means, when the US is in good state, then China is also in good state; when the US is in bad state, China is also in bad state. Whether the US devalues USD or not determines the value of Chinese debt. China is tied with the climate of the US macroeconomic environment due to the denomination of Chinese debt by USD.

The exogenous real return of the second risky real asset is denoted as Rr*. In state H, its return is

The following short-hand notations for expectation operators will be used to describe the model. It also helps understand the timing to the model. These expectation operators are referred from Farhi and Maggiori (2018), which also apply in this context. Keeping the consistency of notations helps understand the connection and differences between Farhi and Maggiori (2018) and my model:

Definition (Farhi and Maggiori (2018)): Define E+ [x1] to denote the expectation taken at time t=0+ of random variable x1 the realization of which will occur at t=1. Further define Es [x1] to be the expectation taken at t=0+ conditional on the safe realization of the sunspot, and Er [x1] to be the expectation taken at t=0+ conditional on the risky realization of the sunspot. Define E- [ x1] to be the expectation taken at t=0- before the sunspot realization.

Timing. The event sequence of the model is constructed based on the Calvo timing (Calvo, 1988). At the beginning ( t =

Event Sequence of the Model

The game proceeds as follows. At t=0o, People’s Bank of China and the Ministry of Finance of China bargains over the endowment of China to determine the share each entity possesses. At the meantime, the endowment of the US and Russia are also determined.

At t=0-, the U.S. Treasury determines the amount of reserve asset that will be issued to People’s Bank of China; the Ministry of Finance of China determines the amount of reserve asset that will be issued to Russia. The Federal Reserve invests in the first real risky asset; People’s Bank of China invests in the first real risky asset and the Ministry of Finance of China invests in the second risky real asset; Bank of Russia invests in the second real risky asset. The U.S. Treasury and the Ministry of Finance of China determine their intertemporal consumption at t=0-.

At t=0+, the interest rate about the amount of reserve asset determined by the US is determined by People’s Bank of China, which invests in the reserve asset; the interest rate about the amount of reserve asset issued by the Ministry of Finance of China is determined by Bank of Russia, which invests in the reserve asset. A sunspot for selecting equilibrium is realized for the safe asset transaction between the U.S. Treasury and People’s Bank of China; another sunspot for selecting equilibrium is realized for the safe asset transaction between the Ministry of China and Bank of Russia.

At t=1, supposing a disaster shock comes towards US, the Federal Reserve decides whether to devalue USD; the disaster shock that the US experiences also affects China due to the dollar-denomination of Chinese debt. People’s Bank of China will also consider whether or not to adjust the RMB value over RUB at t=1. However, People’s Bank of China will consider adjusting the value of RMB only if the US and China are off-equilibrium (Proposition 7). The consumption of the Federal Reserve and People’s Bank of China at period t=1 in their respective consumption optimization problems are determined. Besides, the consumption of Bank of Russia at period t=1 in their portfolio optimization problem is also determined.

At t=0-, the U.S. Treasury needs determine the amount of the reserve asset to issue and its investment in the risky asset. I use b to denote the debt to issue at t=0- and x to denote the first real risky asset to invest at t=0-. By determining x and b, the consumption at t=0, C0, is determined at t=0-. The interest rate on the outstanding debt b is denoted by R. It is determined after t=0-, which is the time point t=0+. At t=0+, the sunspot ω is realized. The sunspot has binary realizations: s indicates a safe equilibrium and it is realized with probability α; r indicates a risky equilibrium and it is realized with probability 1-α. Given the realization of the sunspot, an equilibrium is selected. The interest rate on the outstanding debt R is therefore determined given the realization of ω and b. Hence, the interest rate can be denoted by R(b, ω).

At t=1, if the macroeconomic environment of the US is positive, i.e., the state H happens, then no devaluations could happen; however, if the disaster state L happens, the US will consider whether to devalue USD, which is implemented by the Federal Reserve, to ease its burden to repay the debt or fulfill its commitment, which is conducted by the U.S. Treasury, by not devaluing USD. Therefore, I denote the exchange rate by e ∈ {1, eL}, where eL < 1. e represents the RMB price of a dollar. In state L, e=1 if the US fulfills its commitment to its debt and e < 1 if the US devalues USD to reduce the value of its debt. According to the event sequence, the choice of exchange rate is determined by the amount of the outstanding debt b and the potential sunspot ω. Therefore, the exchange rate at this time period can be denoted by e(b, ω).

Given the exchange rate, the consumption at period 1 expected before t=0+ can also be determined. I denote it by C1(ω). The devaluation of USD is associated with the devaluation cost τ(1 – e (b, ω)). τ is a normalization constant and if USD is completely devalued, the devaluation cost is just ε.

Finally, because the U.S. Treasury meets an intertemporal consumption optimization problem, therefore I denote the discount factor by δ. To ensure the US is indifferent between the timing of consumption, I specify

Based on all above ingredients, the intertemporal consumption problem of the US will be construetd. The U.S. Treasury and the Federal Reserve are assumed risk neutral over the consumption across the two periods. The payoff of the US is the total consumption of t=0 and t=1 minus the devaluation cost, which is given by:

The US needs to choose b, x, C0 and C1(ω) to maximize the above payoff. Given all above specification, the intertemporal consumption problem of the US is written by:

Next, this paper introduces the bargaining between People’s Bank of China and Ministry of Finance of China. In order to optimize its portfolio, People’s Bank of China invests b in the reserve asset issued by the US and x* in the first real risky asset. It also needs to determine its consumption at t=1, which is denoted by

Note that in the above problem, w*, x*, b and

At t=0-, the Ministry of Finance of China needs to determine the amount of reserve asset to issue and its investment in the risky asset as well as its consumption at this period. I use b* to denote the debt to issue at t=0- and

At t=1, if state H happens for the US, then China also experiences a good state, in which because the US does not devalue USD and China does not devalue RMB, the value of Chinese debt is kept. However, if state L happens for the US, then China also experiences a disaster state. The US may consider devalue USD over RMB. In this situation, if China does not devalue RMB, then ultimately USD is devalued over RUB and hence the Chinese debt is devalued. The situation where USD appreciates over RUB is not considered. Suppose, in the disaster state, China also considers adjusting the value of RMB over RUB (either depreciation or appreciation). If the US does not directly announce a devaluation over RUB, the operation by China does not affect the valuation of Chinese debt. I denote as the Rubble (RUB henceforth) price of a dollar.

Like the determination of the RMB price of USD, e, before t=0+, e* is determined by the amount of the outstanding debt b* and b, and the realization of ω* and ω. Therefore, denote the e* before t=0+ by e*(b*, ω*, b, ω). Correspondingly, the RUB price of a RMB before t=0+ is denoted by

The devaluation of Chinese debt is associated with a devaluation cost τ*(1-e*(b*, ω*, b, ω)). τ* is a normalization constant and if the Chinese debt is completely devalued, the devaluation cost is just τ*. I denote the discount factor for China by δ*. To make the consumption at t=0 and t=1 indifferent, I specify

Then this paper organizes the given parameters to construct the intertemporal consumption problem of China. The Ministry of Finance of China and People’s Bank of China are assumed risk neutral on consumption across the two periods. The payoff of China is therefore the total consumption of t=0 and t=1 minus the devaluation cost, which is given by:

China needs to choose b*,

Note that all variables, b*,

I model the savings division problem as a Nash bargaining problem. The formulation of the Nash bargaining problem is based on the debt purchasing problem by People’s Bank of China and the debt issuance problem by Ministry of Finance of China. Therefore, China’s debt purchasing and issuing problem is presented as follows:

Finally, this paper introduces the debt purchasing problem of Bank of Russia. Like its Chinese counterpart, Bank of Russia does not consume at t=0. Bank of Russia invests b* in the safe asset issued by Ministry of Finance of China and x** in the second real risky asset. It also determines its consumption at t=1,

By solving the above portfolio optimization problem, Bank of Russia determines its demand for Chinese safe asset. Note that b*,

The Algebraic Representation of the US-China-Russia Debt Chain Subject to the Expectation that the US Debt and Chinese Debt are Safe in Disaster States

For analytical purpose, in the following I transform the above descriptions of the model into its algebraic representations, given that the value of the US safe asset and Chinese safe asset are kept in disaster states. The algebraic representations are expressed by

The US:

which can be reformulated to

where P = b(Rr – R) and P* = b*(Rr* – R*). P and P* are the exorbitant privileges for the US and China respectively.

Russia:

3 Equilibrium under Full Commitment by the US and China

In this section, I analyze the best case: the US and China will not devalue their currencies once they encounter economic disasters at t=1. The case is also a benchmark: if people know what the US and China would do if they commit to the valuation of their currencies, then people could expect what the US and China would do if their commitments on the valuation of their currencies are limited. The Nash bargaining between People’s Bank of China and the Ministry of Finance of China plays a decisive role in determining the equilibrium debt issuance of the US and China, while the endowment/savings of China and Russia can determine whether the US-China-Russia debt chain can be maintained.

The Nash bargaining between People’s Bank of China and the Ministry of Finance of China happens at

The optimization condition of the debt issuance problem of the US given that the US debt is expected to be safe is written by

R is a function with respect to b and R′ is the derivative of R with respect to b. The safe asset return function can thus be written by R = Rr – 2γ(w* – b)σ2, which reflects the demand for the US safe asset from People’s Bank of China. Substituting the debt demand function into the debt issuance decision problem of the US, I obtain the equilibrium safe asset issuance by the US, which is

where w* is the savings used to purchase safe asset by People’s Bank of China obtained by Nash bargaining with the Ministry of Finance of China.

Then the reserve asset issuance by the Ministry of Finance of China will be analyzed. The optimization condition of the debt issuance problem of China given that the Chinese debt is expected to be safe is written by

Likewise, in this setting, R* is a function with respect to b* and R* is the derivative of R* with respect to b*. Because the Chinese debt is expected to be safe, then the demand for safe Chinese debt from Russia can be written by R* = Rr* – 2γ*(w** – b*)σ*2. Substituting the safe asset demand function to the debt issuance decision problem of China, I obtain the equilibrium safe asset issuance by China, which is

Next, we deal with the Nash bargaining problem between People’s Bank of China and the Ministry of Finance of China. The prerequisite that a bargaining problem arises is that there exist conflicts of interests between the entities that engage in the bargaining. In the context of this paper, a bargaining over the share of total savings of China happens when both People’s Bank of China and the Ministry of Finance of China want more share of the savings to support their portfolio optimization and intertemporal consumption optimization respectively. However, a peaceful division rather than a bargaining over the total savings between People’s Bank of China and the Ministry of Finance of China can also happen.

The reason why the dual phenomena exist is that the mean-variance preference of People’s Bank of China is concave with respect to w* : when

Proposition 1

When

Therefore, the w* in the Nash bargaining problem could be either a bargaining result or a peaceful-division result. As I present below, the smaller the w* is, the smaller w* is. Hence, conversely, a small w* implies a small w*. Proposition 1 implies that if China is less wealthy, bargaining over the total savings of China between People’s Bank of China and the Ministry of Finance of China is more likely to happen.

Proposition 2

The w* of the Nash bargaining problem is

It can be found that

The total savings of the US, w, does not affect w*, the savings allocated to purchase safe asset from the US. Instead, w* and w** play deterministic roles on the value of w*. It is straightforwardly comprehensible that w does not determine the w* but w* determines w* : the fiscal capacity of the US hardly affects how much safe asset to issue to China, but how much safe asset to purchase does depend on the budget of the People’s Bank of China. In addition, the wealthier China is, the more fund can be allocated to People’s Bank of China to purchase the US safe asset, which is in expectation and confirmed by the formula of w* in Proposition 2. Therefore, if the US can fully commit to the value of its issued safe asset, a wealthier China is good for the US in terms of safe asset transaction.

A fresh insight delivered by the formula of w* is that w** also determines the equilibrium safe asset issuance from the US to China. The wealthier Russia is, the more budget will be allocated to People’s Bank of China to purchase safe asset from the US. This operation benefits China: the equilibrium safe asset issuance from China to Russia is up to the savings of Russia. The wealthier Russia is, the more reserve asset China issues to Russia. China hence gets better financed and in turn Chinese government can allocate more fund to purchase safe asset from the US. The formula in Proposition 2 shows the case.

However, remember that it is required that w* ≤ w*. Define F(P*(w**)) by

Then we have

Corollary 1: w* < w* if and only if w* > F(P*(w**)). w* = w* if and only if w* ≤ F(P*(w**)).

It can be proven that

As mentioned, the equilibrium debt issuance from China to Russia depends on the savings of Russia. However, if there is no money allocated to the Ministry of Finance of China, the equilibrium would not even happen, though China does not devalue RMB in disaster state. Therefore, the corner solution w* = w*, or its equivalent condition w* ≤ F(P*(w**)), indicates a situation where China gives up issuing safe asset to Russia and simply purchase safe asset from the US, the situation of which happens when China is less wealthy and it commits to the value of RMB even in the disaster state. The US-China-Russia debt chain can be reduced to US-China debt chain.

Another insight delivered by Corollary 1 is that although the wealth level of China does not affect how much safe asset China issues to Russia, the wealth level of China determines whether China can issue safe asset to Russia or not. Only when China can issue safe asset to Russia, then the wealth level of China does not restrict the amount of safe asset China wants to issue to Russia.

In some circumstances, the US-China-Russia debt chain can be reduced to China-Russia debt chain. If the payoff of People’s Bank of China is negative due to purchasing the safe asset from the US, certainly China will stop doing it. The savings of Russia can determine given an amount of purchased the US safe asset, the payoff of People’s Bank of China is positive or negative.

In the following, I analyze when w* < w*, under what conditions the payoff of People’s Bank of China is positive or negative. Before that, I first introduce the assumption that defines the range of w**.

Assumption 1

The parameters γ, σ, γ*, δ*, Rr and R satisfy the following relationship:

The following result describes the situations in which the payoff of People’s Bank of China by portfolio optimization is positive:

Proposition 3

Given Assumption 1 and w* > F(P*(w**)), for

In the following, I present the parameter ranges in two scenarios that support positive payoffs of People’s Bank of China by portfolio optimization. These two scenarios are qualitatively decipted in figures in Appendix A. If w** satisfies Proposition 3, the US-China debt chain is unbreakable because the payoff of People’s Bank of China is always positive. Since the given value of w** should always make the payoff of Bank of Russia positive and the payoff of the Ministry of Finance of China is always positive, therefore the China-Russia debt chain is expected to be unbreakable as well. Therefore, for w** satisfying Proposition 3, the US-China-Russia debt chain is maintained.

In the situation where w* = w*, i.e., when China is not wealthy enough, the Finance Ministry of China does not issue safe assets to Russia, but the transaction of second risky real asset is still there. Therefore, the savings of Russia can still determine whether the debt chain the US-China stops functioning or not.

A further result about the payoff of People’s Bank of China by portfolio optimization can be obtained:

Proposition 4

Given w* < F(P*(w**)), the payoff of People’s Bank of China by portfolio optimization is positive if and only if

According to whether the intersection point between F(P*(w**)) and

Therefore, in the cases I have studied, it is possible that a China-Russia debt chain without the US influence may emerge (as implied by Corollary 1), but the US-China debt chain without the influence from Russia is hard to appear (as reflected by Proposition 4).

Again, before concluding this section, this paper emphasizes that as the debt issuer, the payoffs of the U.S. Treasury and the Ministry of Finance of China are never negative in the model.

4 The Equilibrium under Limited Commitment by the US and China

In this section, this paper analyzes the case where the commitments of both the US and China are limited. The devaluation of debt here refers to a partial default of the debt issued by the US and China. Such devaluation is achieved through devaluing USD over RMB and devaluing USD over RUB in the context of this paper. As documented in Farhi and Maggiori (2018), historically, many countries achieve a partial default of their debt through devaluing their home currencies. Therefore, like Farhi and Maggiori (2018), I also model the partial default of the US and China by a devaluation of USD. China can also devalue RMB over RUB. However, the purpose that China adjusts the value of RMB is to ensure the US and China (and hence Russia) is on equilibrium.

In the following, I first analyze the equilibria for a given quantity of debt b and b* and then study the optimal issuance of b and b* from the perspective of the US and China respectively.

If disaster state occurs at t = 1 for the US, the Federal Reserve then determines whether to devalue its currency by solving

The Federal Reserve chooses to devalue USD over RMB if and only if

The intuition is that Federal Reserve chooses eL rather than eH = 1 if the gains from lower real debt repayment to People’s Bank of China are greater than the corresponding devaluation cost τ(1 − eL).

The condition for devaluing USD can be reformulated to the following threshold rule:

If bR > τ, then the US chooses to devalue USD in bad state at t = 1. At t = 0+, People’s Bank of China anticipates that the Federal Reserve will devalue and therefore treat the US safe asset as a perfect substitute for the first risky real asset. People’s Bank of China requires

If bR ≤ τ, then the US does not devalue USD in bad state at t = 1 and its debt to China is therefore safe. The interest rate is then R = Rs(b). The outcome for the US is possible for all b < b̄, where

where w* is given in Proposition 2. Because w* is a function with respect to b**, therefore b̄ is a best response with respect to b**.

I focus on the case where b̄ ≤ w*, which requires τ ≤ Rr w* so that the commitment to China for the US is sufficiently limited so that the US cannot provide China with full insurance. Imposing the condition results in the following relationship: b ≤ b̄ ≤ w*. The first inequality holds because Rs(b) < Rr for all b ∈ [0, b̄], conditional on the debt to China safe. Therefore, b̄ Rr > τ.

Both outcomes (keeping the value of USD over RMB or devaluing USD over RMB) are possible for b ∈ [b, b̄]. I call the interval [b, b̄] the instability zone. USD must be devalued for b ∈ (b̄, w*], which interval is called the collapse zone. Because both b̄ and w* depend on b*, therefore the instability zone of the US and the collapse zone of the US are the best responses with respect to b*. For China, its safe asset issuance b* depends on e*, where e* = e ×

This paper summarizes these results in the lemma below, which fully describes the equilibrium exchange rate function e(b, ω) and debt return function R(b, ω).

Lemma 1

(The Three Zones for the US in the US-China-Russia Debt Chain) Given ẽ*̃, for a given level of b at t = 0−, the structure of continuation optimum for t = 0+ onwards is as follows:

If b ∈ [0, b] (safety zone), there is a unique optimum, the safe optimal issuance, under which the US does not devalue in the disaster state at t = 1. This optimum is as same as the full-commitment equilibrium debt issuance.

If b ∈ (b, b̄] (instability zone), there are two optima: the safe optimal issuance described above; and the collapse optimal issuance under which the US devalues in the disaster state at t = 1, the interest rate on the safe asset is

If b ∈ (b̄, w*] (collapse zone), there is a unique optimum, the collapse optimal issuance described above.

As disaster state occurs at t = 1 for the US, which contaminates China as well, the Finance Ministry of China determines its optimal consumption contingent on the US devaluation decisions by solving following equations:

where

The intuition is that if the US chooses to devalue USD over RUB, the Chinese debt issuance should ensure that the gains from lower real debt repayment to Bank of Russia are greater than the corresponding devaluation cost

The condition that Chinese debt issuance should satisfy if the US devalues USD can be reformulated to the following rule:

If the US devalues USD over RUB in bad state at t = 1, the Chinese debt issuance should satisfy b* R* > τ*. At t= 0+, Bank of Russia anticipates the US will devalue USD and therefore treat Chinese debt as a perfect substitute for the second risky real asset. Bank of Russia requires

If the US does not devalue USD in bad state at t = 1, supposing the Chinese debt to Russia is safe, then the Chinese debt issuance should satisfy b* R* ≤ τ*. The interest rate of the Chinese debt is then R* = R*s(b*). The outcome of China is possible for all b* < b*, where

I focus on the case where b* ≤ w**, which requires τ* ≤ Rr* w** so that the commitment to Russia for China is sufficiently limited so that China cannot provide Russia with full insurance. Imposing the condition results in the following relationship: b* ≤ b* ≤ w**. The first inequality holds because Rs*(b) < Rr* for all b* ∈ [0, b*], conditional on the debt to Russia safe. Therefore, b* Rr*>τ*.

For b* ∈ [b*, b*], both possibilities (the valuation of USD over RUB not changed or USD devalued over RUB) co-exist. Note that only when the US devalues USD over RUB, the Chinese debt issuance problem can be characterized by the three zones for China (safety zone: [0, b*], instability zone: (b*, b*], collapse zone: (b*, w*]). Otherwise, the Chinese debt value is kept and hence its debt issuance is exactly the case of full commitment. Therefore, the emergence of the three zones for China is the best response to that the US chooses e* =

This paper summarizes these results in the lemma below, which fully describes the equilibrium exchange rate function e*(b*, ω*, b, ω) and debt return function R*(b*, ω*).

Lemma 2

(The Three Zones for China in the US-China-Russia Debt Chain): Given e*, for a given level of b* at t = 0−, the structure of continuation optimum for t = 0+ onwards is as follows:

If b* ∈ [0, b*] (safety zone), there is a unique optimum, the safe optimal issuance, under which China expects the US does not devalue in the disaster state at t = 1. This optimal debt issuance is as same as the full-commitment equilibrium debt issuance.

If b* ∈ (b*, b*] (instability zone), there are two equilibria: the safe optimal issuance described above; and the collapse optimal issuance under which China expects the US devalues in the disaster state at t = 1, the interest rate on the safe asset is

If b* ∈ (b*, w**] (collapse zone), there is a unique optimum, the collapse optimal issuance described above.

In my model, for the US, monetary decisions and fiscal decisions are made by the Federal Reserve and the U.S. Treasury respectively via navigating two conflicting objectives ex post: maintaining the value of USD and easing its fiscal burden by inflating away its debt. Depending on which objective dominates, the economy can be regarded either operating in monetary regime or fiscal regime. The trade-off happens endogenously as an equilibrium of the game, where the ex post stage is described by Lemma 1 and the ex ante stage is described by Proposition 5.

However, for China, because its debt to Russia is also denoted by USD, hence China in fact grants its monetary decisions to the US. The monetary decision and the fiscal decision made by the Finance Ministry of China inevitably conflicts with each other during the process where each entity navigates their respective and conflicting objectives ex post: the US wants to maintain the value of USD over RUB but China wants to deflate its debt, or the US wants to devalue USD over RUB but China wants to maintain the value of its debt. Depending on which objective dominates, the Chinese economy can be regarded either operating in monetary regime commanded by the US or fiscal regime led by the Finance Ministry of China. The trade-off happens endogenously as an equilibrium of the game, where the ex post stage is described by Lemma 2 and the ex ante stage is described by Proposition 6.

4.1 Optimal Debt Issuance of the US and China

Next, I turn to the optimal debt issuance of the US and China. Because I focus on the strategic interaction of the US and China, therefore this paper defines the following functions as a selection device in the form of sunspot: the safe equilibrium is selected if the realization of the sunspot is s, and the collapse equilibrium is selected if the realization of the sunspot is r. Specifically, for the US, I define a function α(b) ∈ [0,1] to denote the t = 0− probability that the continuation equilibrium for t = 0+ onward is the collapse equilibrium.

For China, I define a function α(b*) ∈ [0,1] to denote the t = 0− probability that the continuation equilibrium for t = 0+ onward is the collapse equilibrium.

Given

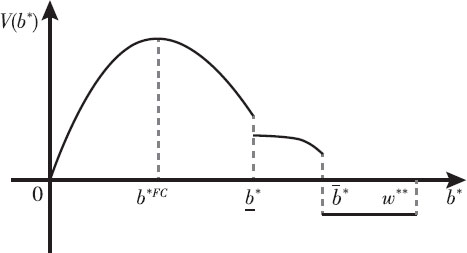

where VFC(b) = b(Rr − Rs(b)) is the full-commitment value function for the US. The formulation shows that maximizing the payoff of the US is equivalent to maximizing the expected wealth transfer from China, minus the expected cost of a prospective devaluation. The value function is illustrated in Figure 2 and Figure 3. I characterize optimal issuance in the proposition below.

The Value Function Describes Case 1 of Proposition 5 (bFC = b)

The Value Function Describes Case 2 of Proposition 5 (bFC = b)

Proposition 5

(Limited-Commitment Optimal Issuance for the US in the US China-Russia Debt Chain) Given

If bFC ∈ (0, b], then the US issues bFC in the safety zone.

If bFC ∈ (b, b̄], then the US issues b in the safety zone or bFC in the instability zone, whichever generates higher net expected monopoly rents.

If bFC ∈ (b̄, w*], then the US either issues b in the safety zone or b̄ in the instability zone, whichever generates higher net expected monopoly rents.

where w* is given in Proposition 2.

Given e*, under limited commitment of the US and its issuance in the instability zone or collapse zone, by analogy with the full-commitment problem, the Chinese maximization problem is

where VFC(b*) = b*(R* − Rs(b*)) is the full-commitment value function for China. The formulation shows that maximizing the payoff of China is equivalent to maximizing the expected wealth transfer from Russia, minus the expected cost of a prospective devaluation of USD. The value function is illustrated in Figure 4 and Figure 5. I characterize optimal issuance in the proposition below.

The Value Function Describes Case 1 of Proposition 6(b*FC < b*)

The Value Function Describes Case 2 of Proposition 6(b* < b*FC < b*)

Proposition 6

(Limited-Commitment Optimal Issuance for China in the US-China-Russia Debt Chain) Given e*, under limited commitment of the US and its issuance in the instability zone so that eL is possible to choose or collapse zone so that eL is chosen, optimal issuance by China can be described as follows:

If b*FC ∈ (0, b*], then China issues b*FC in the safety zone.

If b*FC ∈ (b*, b*], then China issues b* in the safety zone or b*FC in the instability zone, whichever generates higher net expected monopoly rents.

If b*FC ∈ (b*, w**], then China either issues b* in the safety zone or b* in the instability zone, whichever generates higher net expected monopoly rents.

If China’s optimal choice of debt issuance corresponds to an inconsistent expectation of e* that the US has chosen, then China adjusts

Whether a Triffin dilemma arises for the US depends on the level of Chinese demand for reserve asset (w*), compared to the safe debt capacity of the US (τ). All else equal, an increase in Chinese demand for safe asset or a decrease in the safe debt capacity activates the Triffin margin. The US then faces a choice between a low level of debt issuance at the boundary of the safety zone and a high level of debt issuance (min {bFC, b}) in the instability zone.

Likewise, whether a Triffin dilemma arises for China depends on the level of Russian demand for reserve asset (w**), compared to the safe debt capacity of China (τ*). All else equal, an increase in the Russian demand for safe asset or a decrease in the safe debt capacity activates the Chinese Triffin margin. Then China faces a choice between a low level of debt issuance at the boundary of the safety zone and a high level of debt issuance (min{b*FC, b*}) in the instability zone.

In the following, I introduce the Proposition 7. Proposition 7 is a refinement of Proposition 5 and Proposition 6 combined. With generality, I consider the case in which

Proposition 7

Given

The US commitment to the value of USD over RMB is limited and issues bFC ∈ (0, b] in the safety zone. China expects the commitment to its debt value is limited and hence issues b* in its safety zone.

The US fully commits to the value of USD over RMB and issues bFC ∈ (0, w*]. China expects the commitment to its debt value is full and hence issues b*FC ∈ (0, w**].

The US commitment to the value of USD over RMB is limited and issues either b or bFC ∈ (b, b]. China issues b* or b*FC ∈ (b*, b*].

If none of the above situation happens, China will adjust the value of

Next I prove Proposition 7. If the US encounters bad state, then the US either chooses full-commitment to the value of USD or a limited-commitment to the value of USD. If the US chooses full commitment, then its value function is V FC(b); if the US chooses limited commitment, then its value function is V (b).

The Chinese debt is also denoted by USD. If the US fully commits to the value of its debt or in the limited-commitment situation, the US chooses e* = 1, then the value function for China is VFC(b*). If the US chooses e* =

Given

Suppose either the US commitment to the value of USD over RMB is limited and issues bFC ∈ (0, b] in the safety zone, or the US fully commits to the value of USD over RMB and issues bFC ∈ (0, b]. In the former situation, China’s value function is V(b*) and issues b* in the safety zone; in the latter situation, China’s value function is VFC(b*) and hence the Chinese debt issuance must be b*FC ∈ (0, w**]. Both situations are confirmation that the US is not devalued over RMB and hence USD is not devalued over RUB.

Suppose the US commitment to the value of USD is limited and issues either b or bFC ∈ (b, b]. Hence, e = eL. The following situations can happen for different parameter specifications:

the Chinese debt issuance is b*FC ∈ (0, w**].

China issues b* or bFC ∈ (b*, b*].

However, in case 1, the expected value of e for China is e = 1. Only case 2 is consistent with the chosen value of e, which is e = eL. If case 1 happens, apparently the US, China and Russia are off equilibrium. In this situation, China adjusts the value of

According to Caballero et al. (2017) and Farhi and Maggiori (2018, 2019), when the debt issuance of a country falls into the instability zone, then the country faces the possibility of a self-fulfilling confidence crisis. Such crisis is just the Triffin dilemma or Triffin event as featured in their models.

According to Proposition 7, if the US enters the instability zone, then China enters the instability zone; if the US commitment to the value of USD is full or the US stays in the safety zone given its commitment is limited, then the Chinese debt issuance is either of full commitment or in the safety zone with a limited commitment. Therefore, from this perspective, it can be said that the Triffin dilemma for the US and the Triffin dilemma for China are synchronized. It is all because the Chinese debt issued to Russia is denoted by USD.

The purpose of Chinese adjustment of

If the US encounters bad state, to ensure the US, China and Russia are in equilibrium, e* and hence

The US commitment to the value of USD over RMB is limited but issues bFC in the safety zone. Then, I. given 1)

II. Given

The US fully commits to the value of USD over RMB and hence e = 1. China expects the US fully commits to the value of USD over RMB and e = 1. Because China has not adjusted the value of RMB over RUB, therefore the value of USD over RUB is kept as well. Hence, e* = 1.

I. Given a)

In this situation, the US commitment to the value of USD over RMB is limited and issues safe asset in the instability zone. China expects that the US commitment to the value of USD over RMB is limited and the US issues safe asset in the instability zone. Therefore, given 1)

II. Given a)

In this situation, the US commitment to the value of USD over RMB is limited and issues safe asset in the instability zone. China expects that the US commitment to the value of USD over RMB is limited and the US issues safe asset in the instability zone. Therefore, given

III. Given

In this situation, the US commitment to the value of USD over RMB is limited and issues safe asset in the instability zone. China expects that the US commitment to the value of USD over RMB is limited and the US issues safe asset in the instability zone. Therefore, given 1)

IV. Given

In this situation, the US commitment to the value of USD over RMB is limited and issues safe asset in the instability zone. China expects that the US commitment to the value of USD over RMB is limited and the US issues safe asset in the instability zone. Therefore, given

Issuing safe asset is often viewed as a symbol to reflect a country’s financial power. People cannot forget that some Chinese safe assets issued to foreign countries are also denoted by USD, which links the Chinese financial power to the US. Such inalienability between USD and Chinese safe assets has determined that the Chinese financial power may be not independent. It is ultimately controlled by the US. Therefore, intuitively, if a country’s safe assets are all denoted by its own currency, then the country’s financial power can be independent.

5 Conclusion

In this paper, I majorly address the following problem: the supply of and demand for safe assets among the US, China and Russia under full commitment or limited commitment towards the value of USD. The core that organizes the model is the Nash bargaining between the People’s Bank of China by portfolio optimization and the Ministry of Finance of China by intertemporal consumption optimization. The Nash bargaining has determined that even under full commitment by both the US and China, the US-China-Russia debt chain is hard to maintain in certain circumstances.

In the full-commitment case, this paper finds that even if the US (and hence China) can fully commits to the value of its debt, sometimes the US-China-Russia debt chain still cannot be maintained and reduced to a two-tier debt chain. In the limitedcommitment case, I find that although safe asset issuance is a reflection of a country’s financial power, if the country’s safe asset is not denoted by its own currency, then such financial power is ultimately controlled by the country who issues the currency that is used to denote the safe asset.

The future extension of the paper is to further delve into the bottom tier’s role in determining the maintenance or collapse of a debt chain such as the US-China-Russia debt chain as considered in this paper. In the model presented in this paper, it can be observed that Russia indeed plays pivotal role in determining the maintenance or collapse of the US-China-Russia debt chain in scenarios where either the US commitment to its debt is full/limited or the Chinese commitment to its debt is full/ limited. However, Russia’s function in the debt chain could be larger than what have been discovered in this model.

References

Caballero, R. J., Farhi, E., & Gourinchas, P. O. (2017). Rents, Technical Change, and Risk Premia - Accounting for Secular Trends in Interest Rates, Returns on Capital, Earning Yields, and Factor Shares. American Economic Review, 107, 5, 614–620.10.1257/aer.p20171036Search in Google Scholar

Caballero, R. J., Farhi, E., & Gourinchas, P. O. (2019). The Safe Assets Shortage Conundrum. Journal of Economic Perspectives, 31 (3), 29–46.10.1257/jep.31.3.29Search in Google Scholar

Calvo, G. (1988). Serving Public Debt: The Role of Expectations. American Economic Review, 78, 647–661.Search in Google Scholar

Farhi, E., & Maggiori, M. (2018). A Model of the International Monetary System. Quarterly Journal of Economics, 133(1), 295–355.10.1093/qje/qjx031Search in Google Scholar

Farhi, E., & Maggiori, M. (2019). China versus the United States: IMS Meets IPS. AEA Papers and Proceedings, 109, 476–481.10.1257/pandp.20191057Search in Google Scholar

© 2024 Rongyu Wang, Published by DeGryuter

This work is licensed under the Creative Commons Attribution 4.0 International License.

Articles in the same Issue

- Frontmatter

- Cumulative Tariff Cost Rate and Structure in the Global Value Chain: A Theoretical and Empirical Study

- Transportation Network Density, Domestic Market Integration and Excess Sensitivity of Household Consumption

- The Too-Big-to-Fail Premium in Tier-2 Capital Bonds and Additional Tier-1 Capital Bonds Primary Markets: Evidence from China

- Drivers of Portfolio Flows into Chinese Debt Securities Amidst China’s Bond Market Development

- The Connections among the US, China and Russia through Safe Assets

- Research on How the Digital Economy Contributes to Achieving A High-Level and Balanced Development of the Elderly Care Service Industry

Articles in the same Issue

- Frontmatter

- Cumulative Tariff Cost Rate and Structure in the Global Value Chain: A Theoretical and Empirical Study

- Transportation Network Density, Domestic Market Integration and Excess Sensitivity of Household Consumption

- The Too-Big-to-Fail Premium in Tier-2 Capital Bonds and Additional Tier-1 Capital Bonds Primary Markets: Evidence from China

- Drivers of Portfolio Flows into Chinese Debt Securities Amidst China’s Bond Market Development

- The Connections among the US, China and Russia through Safe Assets

- Research on How the Digital Economy Contributes to Achieving A High-Level and Balanced Development of the Elderly Care Service Industry